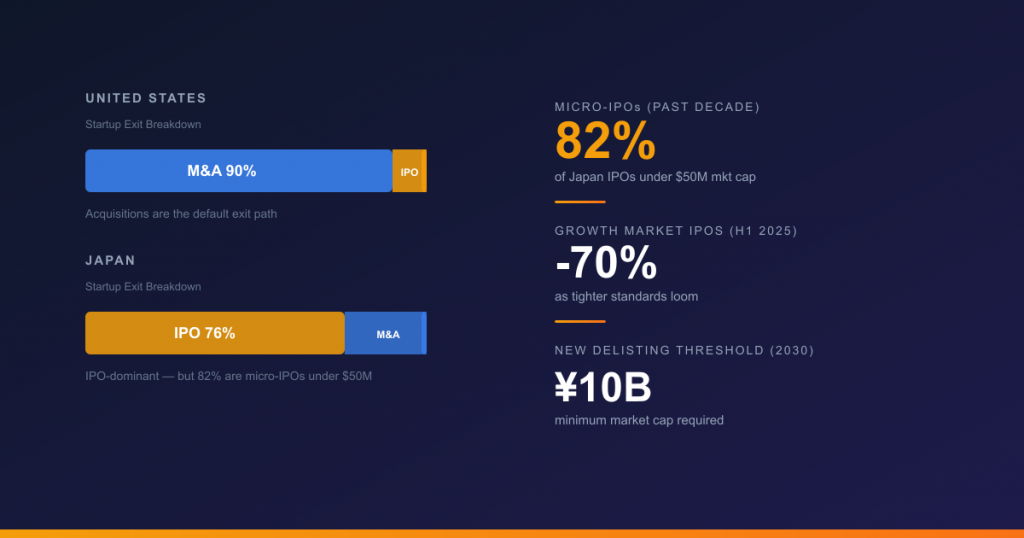

In most of the world, the biggest startup exits happen through acquisitions. In the United States, roughly 90% of venture-backed exits are M&A deals. In Japan, the ratio is inverted — about 76% of startup exits are IPOs. That sounds like good news until you realize most of those IPOs are tiny, illiquid, and leave companies trapped in a low-growth limbo.

The Micro-IPO Machine

Japan has one of the most active IPO markets in the world by deal count. But the numbers are misleading. Over the past decade, small offerings — under $50 million in market capitalization — accounted for 82% of Japan’s total IPOs. For context, that figure is 76% in India and 55% in Hong Kong.

The Tokyo Stock Exchange’s Growth Market (formerly Mothers and JASDAQ Growth) has historically set a very low bar for listing. Companies could go public with market caps of just a few billion yen — $20 to $40 million. The delisting threshold was only 4 billion yen (~$27 million) after 10 years on the market.

The result: Japanese startups routinely list at what would be a Series B or C stage in the United States. They reach just enough revenue to qualify, then rush to IPO — not because they’re ready for public markets, but because the system makes it easy and the alternatives barely exist.

What Happens After These IPOs

The academic evidence is stark. A study of over 700 JASDAQ IPOs between 1991 and 2001 found “dramatic and continuing operating underperformance” after listing. Companies expand aggressively around the offering, then suffer a “striking decline” soon afterward.

The pattern continues today. Mercari, Japan’s most celebrated VC-backed IPO, debuted in 2018 at a valuation of roughly $7.4 billion after surging 77% on its first day of trading. As of early 2026, its market cap has fallen to approximately $3.6 billion — a nearly 50% decline from peak. FreakOut Holdings, once celebrated as a fast-growing ad-tech IPO, has underperformed the Nikkei 225 by over 35% in the past year.

These are not isolated cases. Micro-IPOs trap companies in a cycle of low liquidity, minimal analyst coverage, and limited access to follow-on capital. Institutional investors largely ignore sub-10 billion yen companies — there simply isn’t enough float or trading volume to justify a position.

Why M&A Barely Exists as an Exit

In the US and Europe, the default startup exit is acquisition. A larger company buys the startup, the founders and investors get liquidity, and the technology gets integrated into a bigger platform. In Japan, this path is culturally and structurally blocked.

- Selling equals failure — In Japanese business culture, a founder who sells their company through M&A is widely perceived as having given up. The social stigma is real and affects everything from hiring to future fundraising.

- Fierce independence — Japanese companies, even small ones, are deeply attached to organizational independence. Historical experiences with acquisitions that went poorly have reinforced a preference for staying autonomous.

- Underdeveloped infrastructure — Japan lacks the diversity of merger models, specialized M&A professionals, and standardized processes for startup acquisitions that make deals routine in the US.

- The easy IPO alternative — When listing requirements are low, the path of least resistance is to go public. Why negotiate a complex acquisition when you can list on the Growth Market in 12 to 18 months?

The numbers bear this out. While Japan recorded a record 3,702 domestic M&A deals in 2024 — up 20.5% year-over-year — and total M&A activity approached $350 billion in 2025, the vast majority of that volume comes from large-cap corporate deals, cross-shareholding unwinding, and PE-led restructuring. Startup-specific M&A remains a fraction of the market.

The TSE Is Forcing Change

The Tokyo Stock Exchange knows the micro-IPO model is broken. In a landmark reform, TSE announced that Growth Market companies will need to maintain a market capitalization of at least 10 billion yen (~$64 million) within five years of listing, starting in 2030. Companies that fail to reach this threshold face three options: delist voluntarily, transfer to the Standard Market (which requires at least 1 billion yen in tradable share market cap), or move to a regional exchange.

The impact is already visible. In the first half of 2025, IPOs on the Growth Market plunged roughly 70% year-over-year as tighter listing standards loomed. Small IPOs fell to 43 deals in 2025 — the fewest since 2013. Meanwhile, total IPO proceeds actually rose 33% to $8 billion, the highest since 2018, driven by a few large deals.

The market is clearly bifurcating: fewer companies are going public, but those that do are going public at larger scale. This is exactly what institutional investors have been asking for.

Early Signs of an M&A Culture

Several forces are converging to make startup acquisitions more common in Japan:

- Foreign acquirers are paying attention — KKR’s acquisition of Fuji Soft, Alimentation Couche-Tard’s $38.5 billion offer for Seven & i Holdings, and growing inbound interest from US, Singapore, and Cayman Islands-based acquirers all signal that Japan’s corporate assets — including startups — are undervalued and attracting global interest.

- Tighter IPO standards push founders toward M&A — As the Growth Market raises its bar, some startups that would have pursued a micro-IPO will instead consider acquisition as a viable and even preferable exit.

- Corporate venture capital creates deal flow — Japan’s disproportionately large CVC presence means many startups already have deep relationships with potential acquirers. As M&A stigma fades, these relationships become natural acquisition pipelines.

- Secondary markets are emerging — Platforms like FUNDINNO MARKET are beginning to create liquidity for unlisted shares, giving founders and early investors an alternative to premature IPOs.

The Mercari Question

Mercari remains the case study that everyone in Japan’s startup ecosystem studies. It proved that a Japanese startup could reach unicorn status, go public at scale, and build a consumer product used by tens of millions. But its post-IPO trajectory — a market cap that has halved from its peak — also illustrates the challenge of sustaining growth as a public company in Japan’s capital markets.

The question is whether the next generation of Japanese startups — Sakana AI, SmartHR, and others approaching or already at unicorn valuations — will follow the same path, or whether the structural reforms underway will create a fundamentally different exit environment. SmartHR, notably, has remained private despite being one of Japan’s most well-funded SaaS companies. That patience would have been almost unthinkable a decade ago.

What This Means for International Investors

Japan’s exit ecosystem is in transition. The old model — easy micro-IPOs, almost no M&A, and chronic underperformance post-listing — is being actively dismantled by regulatory reform, foreign capital, and a new generation of founders who have seen how exits work in the rest of the world.

For international investors, this creates a specific window. Japanese startups are still valued at a significant discount to US and European peers, partly because the exit environment has historically been so poor. As that environment improves — larger IPOs, more M&A, growing secondary markets — the valuation gap should narrow. The investors who enter now, while the market is still being reformed, stand to benefit the most from the structural repricing ahead.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →