Executive Summary

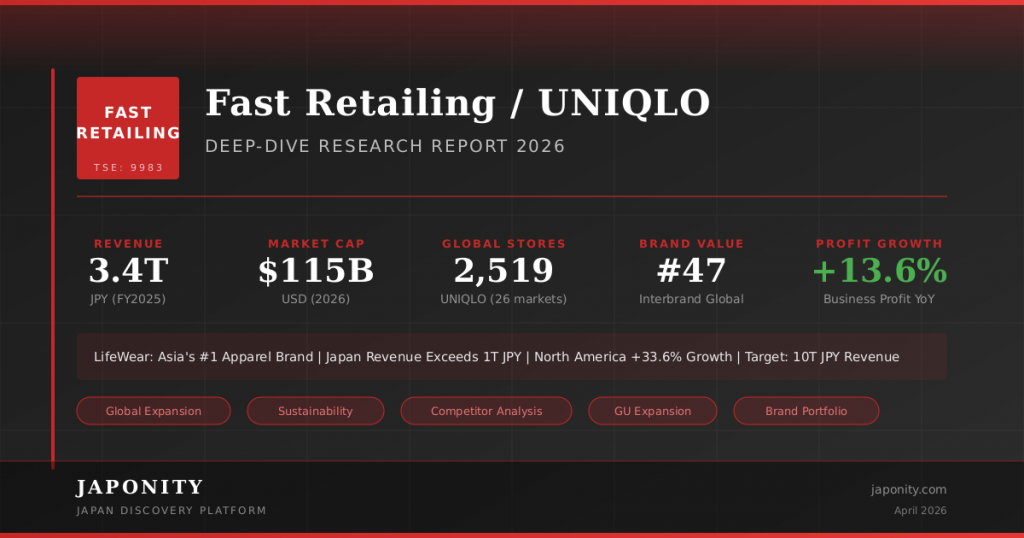

Fast Retailing Co., Ltd. (TSE: 9983), the parent company of UNIQLO, is Asia’s largest apparel company and ranks among the top three clothing retailers globally alongside Inditex (Zara) and H&M Group. In fiscal year 2025 (ended August 31, 2025), the company posted record revenue of ¥3.4 trillion (≈US$22.2 billion), with business profit of ¥551.1 billion (+13.6% YoY). UNIQLO Japan crossed the ¥1 trillion revenue milestone for the first time, while UNIQLO International generated ¥1.91 trillion — nearly double domestic sales. With a market capitalization exceeding US$115 billion, founder Tadashi Yanai‘s ambitious target of ¥10 trillion in group revenue is no longer a distant dream. This report examines Fast Retailing’s financial performance, global strategy, competitive positioning, brand portfolio, sustainability initiatives, and business opportunities for international partners.

Company Overview

| Item | Details |

|---|---|

| Official Name | Fast Retailing Co., Ltd. (株式会社ファーストリテイリング) |

| Founded | 1963 (as Ogori Shoji); 1991 renamed Fast Retailing |

| Headquarters | Yamaguchi, Japan (global HQ operations in Tokyo Midtown) |

| Chairman, President & CEO | Tadashi Yanai (柳井 正) |

| Employees | ~120,000+ (consolidated) |

| Listed | Tokyo Stock Exchange Prime Market (9983) |

| Market Cap | ~US$115 billion (as of early 2026) |

| Core Brand | UNIQLO — 2,519 stores in 26 markets |

| Other Brands | GU, Theory, PLST, Comptoir des Cotonniers, Princesse tam.tam |

| FY2025 Revenue | ¥3.4005 trillion (≈US$22.2B) |

History & Key Milestones

- 1984 — Tadashi Yanai opens the first “Unique Clothing Warehouse” store in Hiroshima

- 1994 — IPO on Hiroshima Stock Exchange

- 1998 — Fleece jacket boom propels UNIQLO into national prominence

- 2001 — First overseas stores open in London

- 2002 — Acquires Theory (U.S. premium brand)

- 2005 — Enters South Korea and Hong Kong

- 2006 — Launches GU as a low-price sister brand

- 2006 — First Shanghai store opens, beginning Greater China expansion

- 2009 — Acquires Comptoir des Cotonniers and Princesse tam.tam (France)

- 2012 — Opens global flagship stores in New York (5th Avenue) and San Francisco

- 2013 — Unveils the “LifeWear” brand concept

- 2018 — UNIQLO International revenue surpasses Japan domestic for the first time

- 2020 — Launches RE.UNIQLO sustainability program

- 2024 — GU opens first U.S. flagship in SoHo, New York

- 2025 — UNIQLO enters Interbrand’s Top 100 Global Brands at #47 (brand value: US$17.7B)

- FY2025 — UNIQLO Japan crosses ¥1 trillion revenue; group revenue reaches ¥3.4T

The LifeWear Philosophy

At the core of UNIQLO’s global appeal is LifeWear — a concept officially unveiled in 2013 and globally campaigned from 2016 with “The Science of LifeWear.” Unlike fast fashion competitors that chase rapid trend cycles, LifeWear represents the fusion of art and science to create simple, high-quality, functional clothing designed for everyday life.

Core Principles

| Principle | Description | Key Products |

|---|---|---|

| Simplicity | Timeless designs free from fleeting trends | Supima Cotton T-shirts, Oxford shirts |

| Innovation | Proprietary fabric technology developed with Toray Industries | HEATTECH, AIRism, Ultra Light Down |

| Quality | Materials and construction rivaling premium brands at accessible prices | Cashmere sweaters, merino knitwear |

| Universality | Clothing designed for all genders, ages, and body types worldwide | U collection (with Christophe Lemaire) |

Why LifeWear resonates globally: Tadashi Yanai has stated that UNIQLO is “not a fashion company — it’s a technology company.” While Zara plans new designs weekly, UNIQLO plans production of wardrobe essentials up to a year in advance, investing heavily in fabric R&D with Toray. This “anti-fast-fashion” positioning has proven especially appealing in Europe, where consumers increasingly value quality, longevity, and sustainability over disposable trends.

Global Expansion Timeline

UNIQLO’s transformation from a regional Japanese retailer to a global apparel powerhouse has followed a deliberate, multi-decade strategy:

| Phase | Period | Key Markets | Strategy |

|---|---|---|---|

| Domestic Dominance | 1984–2000 | Japan | Suburban roadside stores; fleece boom; SPA model |

| Initial International | 2001–2005 | UK, China, South Korea | Flagship-first approach; lessons from London failure/restart |

| Asia Acceleration | 2006–2014 | Greater China, SE Asia, Taiwan | Massive China rollout; 100+ stores in Shanghai alone |

| Western Push | 2014–2020 | USA, Europe, Australia | NYC/Paris/Berlin flagships; brand awareness building |

| Global Parity | 2020–present | All regions | International revenue surpasses Japan; Europe flagship model expansion |

Store Network (as of August 2025)

| Region | UNIQLO Stores | % of Total |

|---|---|---|

| Japan | 794 | 31.5% |

| Greater China (Mainland + HK + Taiwan) | ~1,000+ | ~40% |

| Southeast Asia, India & Australia | ~400+ | ~16% |

| South Korea | ~130 | ~5% |

| Europe | ~120+ | ~5% |

| North America | ~75+ | ~3% |

| Total UNIQLO | 2,519 | 100% |

Note: The Fast Retailing Group total (including GU, Theory, etc.) exceeds 3,600 stores globally.

Financial Analysis

Consolidated Revenue & Profitability Trend

| Fiscal Year (ending Aug) | Revenue (¥T) | Revenue (US$B) | Business Profit (¥B) | BP Margin | Net Income (¥B) |

|---|---|---|---|---|---|

| FY2022 | 2.301 | ~17.0 | 297.3 | 12.9% | 273.3 |

| FY2023 | 2.767 | ~19.5 | 381.1 | 13.8% | 296.2 |

| FY2024 | 3.104 | ~21.0 | 485.3 | 15.6% | 371.9 |

| FY2025 | 3.401 | ~22.2 | 551.1 | 16.2% | 433.0 |

| FY2026E (revised) | 3.800 | ~24.8 | 650.0 | 17.1% | 450.0 |

Key financial takeaways:

- Revenue CAGR of ~14% over the past 3 years, consistently outpacing the global apparel market

- Business profit margin expanded from 12.9% to 16.2% in three years, driven by operational efficiency and inventory management

- Net income of ¥433 billion (+16.4% YoY) in FY2025 — 59% growth from FY2022

- Dividend: ¥500/share (FY2025) → ¥520/share forecast (FY2026)

- Q1 FY2026 (Sep–Nov 2025): Revenue ¥1.028T (+14.8%), business profit ¥205.6B (+31.0%) — exceptional start

Revenue Breakdown by Segment (FY2025)

| Segment | Revenue (¥B) | YoY Change | Business Profit (¥B) | BP Margin |

|---|---|---|---|---|

| UNIQLO Japan | 1,026.0 | +10.1% | 181.3 | 17.7% |

| UNIQLO International | 1,910.2 | +11.6% | 305.3 | 16.0% |

| – Greater China | 650.2 | -4.0% | 89.9 | 13.8% |

| – SE Asia, India & Australia | 619.4 | +14.6% | — | — |

| – North America | 369.5 | +33.6% | — | ~15% (est.) |

| – Europe & South Korea | ~271.1 | Strong growth | — | — |

| GU | ~302 | — | — | — |

| Global Brands | ~163 | — | — | — |

| Group Total | 3,400.5 | +9.6% | 551.1 | 16.2% |

Critical insight: UNIQLO International now generates 1.86x the revenue of UNIQLO Japan. North America grew fastest at +33.6%, while Greater China — still the largest overseas market — saw a rare decline of -4.0%.

Regional Strategy Deep Dive

Greater China: The Largest — and Most Challenging — Market

Greater China remains UNIQLO’s single largest overseas market at ¥650.2 billion in revenue, but FY2025 marked a turning point with a -4.0% revenue decline and -12.5% profit contraction. The slowdown reflects broader consumer caution in China’s economy and intensifying competition from domestic brands like Anta and Li-Ning. However, Q1 FY2026 showed recovery with a pickup in China sales contributing to the 41.6% international profit growth.

North America: The Fastest-Growing Frontier

North America delivered +33.6% revenue growth to ¥369.5 billion — the standout region in FY2025. Fast Retailing is aggressively expanding with planned flagship stores in Chicago, Boston, and additional locations in New York. Despite US tariff headwinds, CFO Takeshi Okazaki confirmed that tariff impact was limited to a 2-3% effect on operating profit, and the company absorbed it in Q1 FY2026 while beating expectations. North America is expected to achieve a ~15% business profit margin in FY2026.

Europe: The Flagship-First Model

UNIQLO is adopting a large flagship store strategy following its European model, with notable openings in Rome, Edinburgh, London, Milan, Nice, Antwerp, Birmingham, and Munich. European consumers have shown a strong affinity for the LifeWear concept, with the quality-and-sustainability positioning resonating particularly well. Revenue and profit across the region posted significant gains.

Southeast Asia, India & Australia: The Growth Engine

This region delivered +14.6% revenue growth to ¥619.4 billion, driven by growing middle-class demand. Fast Retailing continues to expand rapidly in India, Vietnam, Indonesia, Thailand, and the Philippines, seeing this region as the next major growth driver alongside North America.

Competitor Comparison: UNIQLO vs. Zara vs. H&M

The global apparel industry is dominated by three giants with fundamentally different strategies:

| Metric | Fast Retailing (UNIQLO) | Inditex (Zara) | H&M Group |

|---|---|---|---|

| Latest Revenue | ¥3.4T / ~US$22.2B (FY2025) | €38.6B / ~US$42B (FY2024) | SEK 234B / ~US$22.3B (2024) |

| Market Cap | ~US$115B | ~US$160B | ~US$28B |

| Gross Margin | ~55% | 58.3% | ~53% |

| Operating Margin | 16.2% | ~20% | 7.4% |

| Revenue Growth (YoY) | +9.6% | +10.5% | -0.7% |

| Store Count | 2,519 (UNIQLO only) | 5,563 | ~4,300 |

| Design Philosophy | LifeWear — timeless essentials | Fast fashion — weekly new arrivals | Fast fashion — affordable trends |

| Supply Chain Model | SPA (plan 1 year ahead) | Ultra-fast (design-to-shelf: 2 weeks) | Mixed (4–6 months lead time) |

| Key Advantage | Fabric technology (Toray partnership) | Speed-to-market, real-time data | Scale, multi-brand portfolio |

| Interbrand 2025 Rank | #47 (new entry) | Top 50 | Top 100 |

Competitive analysis:

- Inditex remains the revenue leader at nearly 2x Fast Retailing’s scale, but Fast Retailing’s market cap-to-revenue ratio is significantly higher, reflecting investor confidence in growth trajectory

- H&M is struggling — flat revenue, 7.4% operating margin, and declining brand perception signal structural challenges

- Fast Retailing occupies a unique niche: neither fast fashion nor luxury, LifeWear’s “essential clothing” positioning avoids the discounting pressures that erode margins for trend-driven competitors

- Growth trajectory: Fast Retailing is gaining market share, growing faster than both rivals in key Western markets

Brand Portfolio

Beyond UNIQLO, Fast Retailing operates a multi-brand portfolio spanning price points and demographics:

| Brand | Positioning | Stores (Feb 2025) | Key Markets | Status |

|---|---|---|---|---|

| UNIQLO | LifeWear — functional essentials | 2,519 | Global (26 markets) | Core growth engine |

| GU | Trend-driven, low-price | 478 | Japan, Asia, US (new) | Global expansion beginning |

| Theory | Premium workwear/modern essentials | ~250 | US, Japan, Asia | Stable contributor |

| PLST | Affordable quality everyday wear | ~80 | Japan | Domestic niche brand |

| Comptoir des Cotonniers | French casual womenswear | ~100 | France, Europe | Receivership (July 2025) |

| Princesse tam.tam | French lingerie | ~50 | France | Receivership (July 2025) |

GU: The Next Growth Story

GU is positioned as Fast Retailing’s second pillar of growth, targeting 1,000 global stores and contributing ~¥700 billion toward the group’s ¥10 trillion revenue target. Key moves include:

- September 2024: Opened first U.S. flagship in SoHo, New York — the brand’s first store outside Asia

- Simultaneously launched U.S. e-commerce site and mobile app

- Plans for further US and European expansion are being developed

- While UNIQLO focuses on timeless essentials, GU targets trend-conscious younger consumers at lower price points

Sustainability & ESG Strategy

Fast Retailing has positioned sustainability as a core business priority through multiple initiatives:

RE.UNIQLO Program

| Initiative | Details | Scale |

|---|---|---|

| Clothing Collection | Customers return used UNIQLO items at stores worldwide | ~9.5 million items collected (FY2025) |

| RE.UNIQLO STUDIO | In-store repair, remake, and resale services | 67 stores across 23 countries (Oct 2025) |

| Recycled Down | Down from collected jackets reused in new products | Multiple hybrid down products in 2025 lineup |

| Molecular Recycling | First use of customer-donated polyester recycled into new fabric | Debuted with Swedish Olympic team uniforms (2024) |

| Donation Program | Collected items donated to refugees and communities via UNHCR | Target: 1,061,000 items distributed (2025-2026) |

Environmental Targets

- 50% sustainable materials by 2030 — currently at 18.2% (2024), requiring significant acceleration

- Supply chain traceability: Cotton (2023) → Cashmere (2024) → Wool (2025)

- BlueCycle jeans: Water-saving denim finishing technology reducing water usage by up to 99%

- DRY-EX: Partially made from recycled PET bottles

Leadership: Tadashi Yanai’s Vision

Tadashi Yanai (born 1949) is not just a CEO — he is the architect of Japan’s most successful global retail brand and the richest person in Japan with a net worth of US$61.8 billion (Forbes 2026, #32 globally).

Management Philosophy

| Principle | Description |

|---|---|

| 23 Management Principles | Carried by every employee globally. #1: “Respond to customer needs and create new customers“ |

| Global One, Zen-in Keiei | “All employees managing” — every employee thinks and acts from a global perspective |

| The Fourth Frontier | Latest vision: “Challenge, Take Action, Achieve” — pushing beyond current boundaries |

| Anti-Fashion Philosophy | “We totally ignore fashion” — focusing on what people actually need, not trend cycles |

Revenue ambition: Yanai has publicly targeted ¥5 trillion in group revenue within a few years, followed by ¥10 trillion — which he describes as “not an unrealistic goal.” At FY2025’s ¥3.4T and 10%+ annual growth, ¥5T could be achievable by FY2028–2029.

Business Opportunities for International Partners

Fast Retailing’s growth trajectory creates multiple entry points for international businesses:

| Opportunity Area | Details | Target Partners |

|---|---|---|

| Fabric & Material Innovation | UNIQLO’s partnership with Toray produces HEATTECH, AIRism, and Ultra Light Down — new sustainable materials are actively sought | Textile manufacturers, biotech startups |

| Supply Chain & Logistics | Expanding into new Western markets requires local logistics, warehousing, and last-mile delivery partners | 3PL providers, warehouse operators |

| Retail Real Estate | Flagship-first strategy in Europe and North America demands prime retail locations | Commercial real estate developers |

| Sustainability Technology | RE.UNIQLO needs recycling, molecular-level textile processing, and circular economy solutions | Recycling technology companies |

| E-commerce & Digital | Omnichannel expansion, especially for GU’s global launch and UNIQLO’s digital transformation | E-commerce platforms, tech vendors |

| GU Brand Partnerships | GU’s Western expansion (post-NYC flagship) creates opportunities for marketing, localization, and retail operations | Marketing agencies, retail consultancies |

| Distribution & Export | Japanese-made specialty items and collaborations (UT graphic T-shirts, +J, etc.) for local market adaptation | Distributors, licensing partners |

Outlook & Key Risks

Growth Drivers

- North America & Europe remain under-penetrated with massive growth potential (~75+ and ~120+ stores vs. 794 in Japan alone)

- GU’s global debut could replicate UNIQLO’s international success at a lower price point

- Brand momentum: Interbrand Top 100 entry at #47 signals accelerating global brand recognition

- Margin expansion: Business profit margin improving from 12.9% (FY2022) to a projected 17.1% (FY2026E)

- India & Southeast Asia: Fast-growing middle class offers a multi-decade demand runway

Key Risks

- China slowdown: Greater China revenue declined -4.0% in FY2025; recovery pace is uncertain

- US tariffs: While manageable at 2-3% profit impact, escalation could pressure margins

- Currency exposure: Yen fluctuations significantly impact reported results

- Succession risk: Tadashi Yanai (age 76) holds outsized influence; succession planning is critical

- Brand portfolio challenges: Comptoir des Cotonniers/Princesse tam.tam entered receivership in July 2025

- Competition from domestic Chinese brands: Anta, Li-Ning challenging UNIQLO in Asia’s largest market

FY2026 Forecast (Revised Upward)

| Metric | FY2025 Actual | FY2026E (Revised) | Change |

|---|---|---|---|

| Revenue | ¥3.401T | ¥3.800T | +11.7% |

| Business Profit | ¥551.1B | ¥650.0B | +17.9% |

| Operating Profit | ¥564.2B | ¥650.0B | +15.2% |

| Net Income | ¥433.0B | ¥450.0B | +3.9% |

| Dividend | ¥500/share | ¥520/share | +4.0% |

Japonity Research Services

This report was produced by Japonity Research. We provide in-depth research and analysis on Japanese companies for international businesses exploring partnerships, market entry, or investment opportunities in Japan.

Our services include:

- Company deep-dive reports (financial analysis, market position, strategic outlook)

- Industry landscape mapping (competitive analysis, market sizing)

- Partner/supplier identification and introduction facilitation

- Market entry strategy consulting for Japan and Asia-Pacific

Contact us at info@japonity.com to discuss your research needs.

Published: April 2026 | Data as of FY2025 (ended August 2025) and Q1 FY2026 (ended November 2025)

Sources: Fast Retailing IR, Interbrand, Inditex Annual Report, H&M Group Annual Report, Bloomberg, Forbes, FashionUnited, Business of Fashion

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →