Japan is quietly putting a third of its companies up for sale. Not through a fire sale or a crisis, but through demographics: more than a million business owners are reaching their 80s with no one to take over. The result is a record-breaking M&A market — and one of the most underexploited buying opportunities in the developed world.

The demographic time bomb under Japan’s economy

Japan’s small and medium enterprises (SMEs) are the backbone of its economy — over 99% of all companies and roughly 70% of private-sector jobs. They are also overwhelmingly family-owned, and their founders are running out of time.

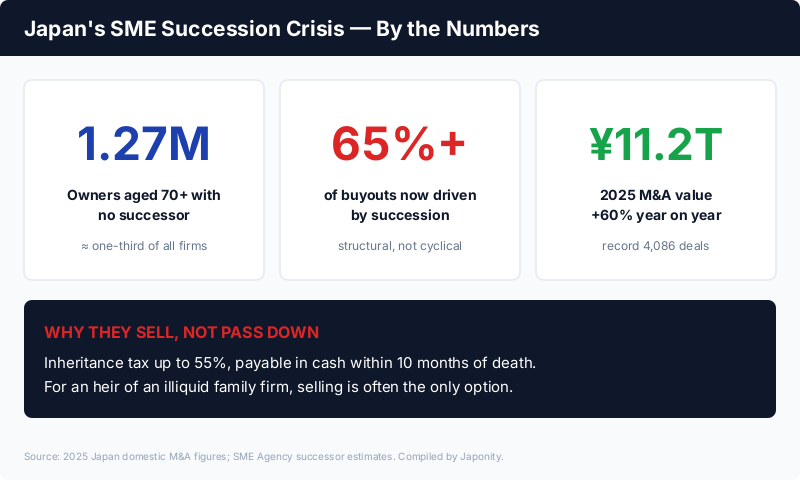

By 2025, an estimated 1.27 million SME owners aged 70 or older had no identified successor — close to one-third of all Japanese companies. These are not failing businesses. Many are profitable, decades-old firms with loyal customers, skilled workforces, and defensible niches. They are simply ownerless.

The reason is generational. The entrepreneurs who built these companies during the post-war boom are now in their 70s and 80s. Their children, raised in an affluent Japan, largely chose careers at global corporations or in the cities rather than inheriting a regional manufacturer or wholesaler. The traditional model — hand the company to your eldest son — has quietly collapsed.

Japan’s own Small and Medium Enterprise Agency has warned for years that without intervention, the country risks losing millions of jobs and a vast store of accumulated know-how purely to a lack of successors. Tens of thousands of otherwise healthy SMEs face closure each year for this single reason.

Why it became a sale, not a shutdown

For a long time, the default outcome of an heirless company was dissolution — the owner simply wound it down at retirement. Two forces have turned that default into a transaction.

1. Punitive inheritance economics. Japan levies among the world’s steepest inheritance taxes, reaching 55% on the largest estates. For the heir of a privately held company, that bill is brutal: it must typically be settled in cash within 10 months of death. Heirs who inherit illiquid shares in a family firm often have no way to pay except to sell the business fast. Passing the company down can be more financially dangerous than selling it.

2. The plumbing finally exists. Bank lending was never designed for ownership transfers, and public markets are out of reach for a ¥500-million-revenue regional firm. What changed is the rise of a dedicated succession-M&A industry: brokers, search funds, and private equity (PE) firms that specialise in matching ageing owners with buyers — increasingly with the help of technology. M&A Research Institute, for example, built a fast-growing business using algorithmic matching to pair sellers with buyers in months rather than years.

Once selling became both financially necessary and operationally easy, the floodgates opened.

A record-breaking M&A year

The numbers from 2025 tell the story:

| Metric | 2025 | Trend |

|---|---|---|

| Domestic M&A deals | 4,086 | All-time high, +10.4% YoY |

| Total deal value | ¥11.2 trillion | +59.9% YoY |

| Owners 70+ without a successor | ~1.27 million | ≈ 1/3 of all firms |

| Succession-driven share of buyouts | 65%+ | Structural, not cyclical |

| SMEs facing annual closure risk | 50,000+ | Persistent |

This is not a one-year spike. Because the driver is demographic, the deal flow is expected to stay elevated for the rest of the decade. Analysts now describe succession as a structural floor under Japanese M&A — the opposite of the boom-bust cycles that characterise most acquisition markets.

Who is buying

The buyer base is broadening fast, and that is what makes this interesting for international readers.

- Domestic private equity. Japanese and pan-Asian PE funds have moved aggressively into the lower-mid market, where succession deals cluster. PE now sits at the centre of the buyout market, with succession transactions making up the majority of their pipeline.

- Search funds and individual acquirers. A new generation of operator-buyers — often returning MBAs — is acquiring single companies to run, a model imported from the US and now growing quickly in Japan.

- Strategic corporates unwinding the keiretsu. Separately, Japan’s largest companies are dismantling decades-old cross-shareholdings under governance reform, releasing a wave of corporate carve-outs and asset sales. This “keiretsu unwind” has added tens of billions of dollars of additional deal volume on top of SME succession.

- Foreign buyers. The weak yen has made Japanese cash flows historically cheap in dollar and euro terms. Foreign strategic and financial buyers are increasingly willing to acquire Japanese SMEs outright — something that was culturally rare a decade ago and is now actively encouraged by sellers who simply want a credible, well-funded home for their life’s work.

Why this matters for global buyers and investors

For international operators, investors, and corporate development teams, Japan’s succession crisis is a textbook case of a structural gap becoming an entry point.

You are buying quality at a discount, not a turnaround. Unlike distressed M&A, succession sellers are typically handing over healthy, cash-generative businesses. The “problem” is the owner’s age, not the company’s performance. Many are precisely the kind of specialised, high-quality “hidden champion” suppliers Japan is famous for.

Valuations remain reasonable. Lower-mid-market Japanese SMEs still trade at multiples well below comparable US or European assets, and the weak yen amplifies the advantage for foreign capital.

The competitive set is thin. Most ageing owners have never run a sale process, and many would prefer a buyer who commits to preserving jobs, the company name, and supplier relationships over the highest bidder. A credible foreign or institutional partner who understands Japanese business etiquette can win deals that pure price-maximisers cannot.

The risks are real and worth naming plainly:

- Cultural and relationship continuity. SME value in Japan is often embedded in the founder’s personal relationships with customers and suppliers. Retention of the seller through a transition period is frequently essential.

- Workforce expectations. Lifetime-employment norms mean buyers are expected to protect jobs, not strip costs. Aggressive restructuring destroys the very goodwill you paid for.

- Due diligence opacity. Many SMEs run on paper, personal trust, and minimal English documentation. Diligence takes patience and local partners.

None of these are dealbreakers. They are the predictable friction points you design around — and the reason a thoughtful entrant earns a structural advantage.

How to start: a practical entry path

- Pick a vertical where you have an operating edge — a sector where you can credibly add distribution, technology, or international reach to a Japanese SME.

- Partner with a local intermediary early. Succession-M&A brokers, regional banks, and PE co-investors are the discovery layer; cold-sourcing rarely works.

- Lead with continuity, not price. Make explicit commitments on jobs, brand, and the founder’s transition role. In succession deals, trust is the differentiator.

- Budget for a hands-on transition. Plan to retain the seller and key staff for 12–24 months and to invest in the documentation and systems the company never built.

- Use the yen window. Currency tailwinds are cyclical; the demographic supply is not. The combination is what makes the present moment unusual.

The bottom line

Japan is not selling its companies because they are weak. It is selling them because an entire generation of founders is retiring at once, with no one at home to take over and a tax code that punishes inaction. That has turned a demographic problem into the developed world’s largest, most durable supply of acquirable, profitable small businesses.

For global buyers willing to do the relationship work, the window is open now — backed by a weak yen, a thin field of competitors, and sellers who care more about a good home than a high price. As Japan builds out its succession infrastructure and foreign capital crowds in, that arbitrage will narrow. The operators who move while it is wide will own the bridge between a retiring generation of Japanese founders and the next.

Frequently asked questions

How many Japanese companies have no successor?

By 2025, an estimated 1.27 million SME owners aged 70 or older had no identified successor — roughly one-third of all companies in Japan. Tens of thousands of otherwise healthy firms face closure each year for this reason alone.

Why are owners selling instead of passing the business to family?

Two reasons. Children of the founder generation have largely pursued careers elsewhere, and Japan’s inheritance tax — up to 55%, payable in cash within 10 months — makes passing down an illiquid family company financially dangerous. A sale is often the only way to preserve the business and its jobs.

Can foreign companies acquire Japanese SMEs?

Yes, and increasingly so. The weak yen makes Japanese cash flows cheap for foreign buyers, and many sellers now prioritise a credible, well-funded home for their company over the highest bid. The keys are leading with continuity — commitments on jobs, brand, and the founder’s transition — and partnering with a local intermediary for sourcing and diligence.

Looking to acquire, invest in, or partner with a Japanese company? Contact Japonity — we connect international buyers and investors with Japan’s best companies, products, and technologies.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →