Toyota Motor Corporation builds roughly one in every nine cars produced on the planet, posts the largest profits of any Japanese listed company, and is, by some distance, the loudest sceptic of an all-battery automotive future. The contradiction is intentional. Understanding why is the single most useful exercise for any foreign supplier, fleet buyer, licensor or investor trying to read the Japanese automotive sector over the next decade.

The shape of the company

Toyota produces in the region of 10 million vehicles a year across roughly fifty plants in twenty-eight countries. Its consolidated revenue runs in the low tens of trillions of yen, making it the highest-earning industrial firm in Japan by a wide margin. Lexus, its premium marque launched in 1989, accounts for roughly a tenth of unit volume but a disproportionate share of margin. Daihatsu (wholly owned), Hino (majority owned, trucks), and equity stakes in Subaru, Mazda, Suzuki, Isuzu and Panasonic-affiliated battery ventures complete what is, in effect, a federation of Japanese manufacturers built around Toyota’s balance sheet.

The company is still controlled, in influence if not in equity, by the Toyoda family. Akio Toyoda, great-grandson of founder Sakichi Toyoda and grandson of Kiichiro Toyoda, stepped up to chairman in 2023 after fourteen years as president. Koji Sato, a lifer who ran the Lexus and Gazoo Racing brands, holds the CEO seat. Continuity of leadership is the norm; outside hires into the executive committee are vanishingly rare. The headquarters remain in Toyota City, Aichi prefecture, a town renamed for the company in 1959 and still organised around its plants.

The Toyota Production System is the moat

Most foreign analysts know Toyota for the Toyota Production System (TPS) — kanban cards, andon cords, just-in-time delivery, jidoka, kaizen — and most underestimate how operationally embedded it remains. TPS is not a poster on a meeting-room wall. It is the operating grammar of every supplier in Toyota’s keiretsu, transmitted through engineer secondments, supplier development programmes, and decades of joint problem-solving sessions on the shop floor.

The practical effect for outsiders is twofold. First, Toyota’s per-vehicle manufacturing cost is structurally lower than that of Western volume manufacturers, which is why the company can absorb the heavy R&D bill of running four powertrain technologies in parallel. Second, breaking into the supply base is slow. Tier-1 suppliers — Denso, Aisin, Toyota Industries, Toyota Boshoku, JTEKT — are not just vendors; they are extensions of the company, with cross-shareholdings, board overlap and, in Denso’s case, a roughly quarter ownership by Toyota itself. Foreign component makers do win business, but typically through a multi-year qualification process that begins with a smaller programme and graduates upward.

The multi-pathway strategy, explained

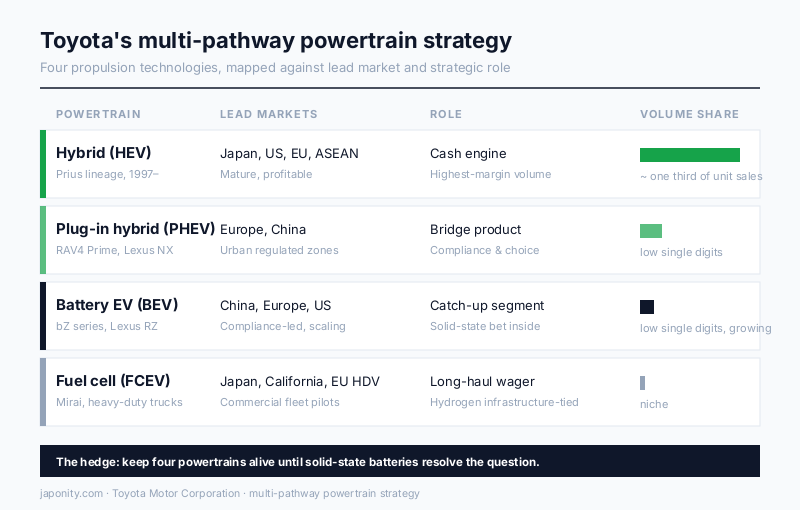

Where Toyota’s competitors — Volkswagen, General Motors, Ford, Hyundai — committed publicly to all-battery roadmaps in the early 2020s, Toyota chose to hedge. Its public position, articulated repeatedly by Akio Toyoda and reinforced by Sato, is that the powertrain mix should follow customer demand and local grid realities rather than regulatory deadlines. In practice this means selling four distinct propulsion technologies simultaneously.

| Powertrain | Lead market | Strategic role |

|---|---|---|

| Hybrid (HEV) | Japan, US, Europe, ASEAN | Cash engine; Prius lineage; highest-margin volume |

| Plug-in hybrid (PHEV) | Europe, China | Bridge product for regulated urban centres |

| Battery EV (BEV) | China, Europe, US (compliance-led) | Catch-up segment; bZ-series and Lexus EVs |

| Fuel cell (FCEV) | Commercial vehicles, Japan, California | Long-haul trucking and heavy-duty bet; Mirai is the test bed |

The bet underneath the bet is on solid-state batteries. Toyota holds more solid-state-related patents than any other automaker — by some counts more than the next several combined — and has publicly committed to bringing the technology to market in the second half of the 2020s. If solid-state delivers on its promised energy density and charge times, Toyota’s late move into pure BEVs becomes a deliberate leap-frog rather than a fumble. If it does not, the company’s hybrid cash flow buys it time the all-EV bettors do not have.

Foreign readers should resist two common misreadings of this strategy. It is not Luddism — Toyota was the global pioneer of hybrid drivetrains with the 1997 Prius and remains the volume leader in the segment by a wide margin. Nor is it a quiet retreat from electrification — capital expenditure on BEV-dedicated plants in North Carolina, Aichi and elsewhere runs into the trillions of yen. It is, more accurately, a refusal to concede that one technology will win in every market segment at the same time.

China is the unsolved problem

The exception to the multi-pathway story is China, where the speed of the local BEV transition has overtaken every foreign manufacturer’s planning assumptions. BYD, Geely, Nio, Li Auto, Xpeng and a long tail of domestic brands now account for the majority of new passenger-vehicle sales, and Japanese makers as a group have lost share in successive years. Toyota’s joint ventures with FAW and GAC remain profitable but are no longer growing in line with the wider market.

The response, in motion since 2024, is a sharper localisation of R&D in Shanghai, partnerships with Tencent for in-vehicle software and Momenta for advanced driver assistance, and a faster cadence of China-specific BEV models. Whether this is enough to defend share against domestic incumbents with deeply integrated battery supply chains is the open question. For foreign suppliers of software, sensors and electronics, Toyota’s China operation is currently the most receptive part of the company to non-keiretsu vendors — a notable break from precedent.

Woven, TRI and the software question

Toyota’s bet on software is concentrated in two entities. Toyota Research Institute (TRI), founded in 2016 in Silicon Valley under Gill Pratt, focuses on machine learning, robotics and materials informatics. Woven by Toyota, headquartered in Nihonbashi, runs the vehicle software platform Arene, the high-definition mapping subsidiary Woven Maps, and the Woven City prototype near Mount Fuji — a fenced-off urban testbed for autonomy, hydrogen distribution and connected-home systems that opened its first phase in 2024.

The corporate logic is to keep the software stack in dedicated subsidiaries with looser cultural ties to the mothership, then pull capabilities back into mainline vehicle programmes as they mature. This is structurally similar to what Mercedes-Benz has done with MB.OS and what Volkswagen attempted, with rather more difficulty, through Cariad. Toyota’s advantage is patience and balance-sheet depth; its disadvantage is the same software-talent constraint that every legacy automaker faces, compounded by Japanese labour-market rigidity at senior engineering levels.

Supply-chain ecosystem and the keiretsu reality

For foreign suppliers, the practical map of Toyota looks less like one company and more like a constellation. Denso, the largest Tier-1, is roughly a quarter owned by Toyota and supplies the bulk of fuel-injection, thermal-management and inverter content. Aisin (formerly Aisin Seiki) handles transmissions and chassis components. Toyota Industries, the original parent company, makes forklifts, looms and powertrain components. Toyota Boshoku does seats and interiors. JTEKT, formed by the merger of Toyoda Koki and Koyo Seiko, supplies steering and bearings. Beyond this inner circle sit hundreds of Tier-2 and Tier-3 firms, many family-owned, concentrated in Aichi and the surrounding prefectures.

The keiretsu structure has loosened materially in the last decade — Toyota no longer treats single-sourcing from a captive supplier as a default — but the gravitational pull remains. Foreign suppliers who succeed tend to share three characteristics. They offer technology the Japanese keiretsu cannot match (high-end semiconductors, specific sensor types, certain software stacks). They invest in Japanese engineering presence and account management. And they accept that the first programme will be small, the qualification cycle long, and the price expectation severe — but that subsequent programmes will compound rapidly if the first one goes well.

Defences, governance and the cost of getting it wrong

Toyota’s defences against hostile change are formidable, though rarely codified as anti-takeover devices in the Western sense. Cross-shareholdings with affiliates and lenders, a stable retail shareholder base, the symbolic weight of the Toyoda family, and the company’s centrality to the Japanese industrial economy together make any contested action — activist, hostile bidder, foreign acquirer — close to unthinkable. Activist funds occasionally take small positions; they almost never succeed in forcing strategic change.

Governance reform has nonetheless progressed. Independent directors now make up the majority of the board. Toyota was one of the first major Japanese listed companies to disclose detailed climate-related financial information on a TCFD basis, and its sustainability reporting is regarded as best-in-class among Asian industrial firms. Compensation remains modest by US standards but has begun to incorporate longer-vested equity components. For foreign institutional investors, Toyota is no longer the governance laggard it was perceived to be a decade ago; whether it is now a leader depends on which yardstick one applies.

FAQ

Can foreign companies license Toyota technology, particularly hybrid or fuel-cell IP?

Yes, selectively. Toyota has historically licensed hybrid technology to other automakers — Ford and Mazda are the best-known cases — and made roughly twenty-four thousand of its hybrid patents royalty-free for a period ending in 2030. Fuel-cell patents have likewise been opened for use in commercial-vehicle and stationary applications. Bespoke licensing arrangements outside these public pools are negotiated case-by-case and typically require a strategic, not merely transactional, rationale.

Who actually owns Toyota?

Toyota is a publicly listed company on the Tokyo Stock Exchange with a free float in the majority. The largest individual shareholders are Japanese financial institutions, Toyota-affiliated entities (notably Toyota Industries, which holds a cross-shareholding) and global index funds. The Toyoda family’s direct equity stake is small in percentage terms but their governance influence remains substantial through board representation and informal authority.

Is Toyota actually behind on EVs, or is the multi-pathway story a strategic choice?

Both, and the distinction matters. On current model count and BEV unit share, Toyota lags BYD, Tesla, Hyundai and Volkswagen. On hybrid volume, solid-state-battery patent depth and overall powertrain R&D spend, it is at or near the global top. The strategy is a deliberate hedge; whether the hedge pays off depends on solid-state commercialisation timelines and the trajectory of grid decarbonisation in Toyota’s main markets.

How do you become a Toyota supplier?

The path runs through one of three doors: the regional purchasing offices (North America in Erlanger, Kentucky; Europe in Brussels; Asia-Pacific from Bangkok and Singapore), an existing Tier-1 such as Denso or Aisin as a sub-supplier, or a technology partnership at the R&D level that graduates into procurement. Expect a multi-year qualification cycle, regular on-site audits, and active supplier development support once you are in. Price discipline is severe but payment terms and programme stability are unusually strong by global standards.

Is Toyota vulnerable to a hostile takeover or activist campaign?

In practice, no. Cross-shareholdings, the company’s national-strategic status, and the cohesion of its retail and institutional shareholder base make hostile action close to impossible. Activist funds have taken positions and occasionally publicised governance concerns, but no campaign has succeeded in changing strategic direction. Foreign acquirers should not regard Toyota as a target in any meaningful planning horizon.

Working with Toyota and its supply ecosystem

The right way for foreign firms to engage with Toyota is rarely to engage with Toyota directly. The mothership procures through a long-conditioned set of regional purchasing offices and qualified Tier-1 partners, and breaking into that flow without a local presence, a Japanese-language account team and a specific technology gap to fill is exceptionally hard. The more productive starting points are Toyota’s Tier-1 and Tier-2 affiliates, its R&D arms (TRI in Silicon Valley, Woven in Tokyo), and the network of independent regional manufacturers — Subaru, Mazda, Hino, Daihatsu — that sit inside Toyota’s broader gravitational field with looser procurement structures.

For foreign fleet buyers, licensors and investors, the equivalent advice is to read Toyota’s public communications closely and discount the sell-side noise. Akio Toyoda’s statements on EV scepticism are not throwaway provocations; they are a precise articulation of the company’s capital-allocation posture. The investor day deck and the supplier convention transcripts are more informative than most analyst reports.

Japonity’s Business Matching service introduces qualified foreign companies — suppliers with differentiated technology, fleet operators with cross-border needs, licensors with strategic IP — to the Japanese automotive ecosystem, with a particular focus on Toyota-adjacent firms in Aichi, Mie and Shizuoka prefectures. Engagements are scoped from a single introduction to a structured market-entry programme; the common element is the assumption that the Japanese counterparty deserves the same diligence the foreign side expects in return.

Related from Japonity — Japan’s automakers

- Honda Motor — The motorcycle giant the auto press forgot

- Nissan Motor — Post-Ghosn, post-Honda — what the Renault entanglement still means

- Mazda Motor Corporation — The Hiroshima underdog that bet on internal combustion

- Subaru Corporation — The boxer-engine niche player that built America

- Suzuki Motor — India’s market king — Maruti Suzuki’s ~40%+ share

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →