In the global automotive industry, Suzuki Motor Corporation is a paradox. It is Japan’s fourth-largest carmaker by volume yet barely visible on American roads. It builds engines for boats, motorcycles, and all-terrain vehicles alongside its cars. And it commands a market share — approximately 40% to 42% — in India that no Japanese rival has ever come close to matching, through its 58%-owned subsidiary Maruti Suzuki India. While Toyota chased global scale and Honda chased prestige, Suzuki quietly built two of the most defensible moats in the industry: dominance of Japan’s kei car segment at home, and dominance of the world’s third-largest auto market abroad. The architect of that strategy, the late Osamu Suzuki, ran the company for more than four decades. His successors now face the harder question: can emerging-market dominance survive the electric transition?

The Hamamatsu loom maker who became a motoring giant

Suzuki Loom Works was founded in 1909 in Hamamatsu, Shizuoka Prefecture, by Michio Suzuki, a carpenter’s son who designed pedal-powered weaving looms for the local cotton industry. Hamamatsu, a manufacturing town on Japan’s Pacific coast, would later also become the birthplace of Honda and Yamaha — an industrial cluster as consequential to Japanese mobility as Detroit was to America.

By the 1930s Michio Suzuki was already prototyping small cars, but wartime priorities and postwar austerity delayed the pivot. The company’s first finished motor vehicle was the “Power Free” — a 36cc bicycle-mounted engine — launched in 1952. Three years later came the Suzulight, a 360cc minicar that helped define what would become Japan’s regulated kei (light) vehicle category. Suzuki has never left that category since.

The choice to start small was not romantic. Postwar Japan had limited steel, limited fuel, and a population that needed mobility cheaper than a full-size sedan. The economics of the loom business — high precision, low cost, mass-produced for a price-sensitive customer base — translated more naturally into minicars than into the luxury vehicles American manufacturers were exporting. That early commitment to small-engine engineering would become a structural advantage Suzuki has never relinquished.

The kei car kingdom

Kei cars — small vehicles capped by Japanese law at 660cc engines and roughly 3.4 meters in length — account for approximately 35% to 40% of new car sales in Japan. They benefit from lower taxes, cheaper insurance, and exemption from the requirement to prove off-street parking in some municipalities. For decades, Daihatsu (now wholly owned by Toyota) and Suzuki have traded the top two positions in this segment, with Honda’s N-Box occasionally taking the single best-selling nameplate. Suzuki’s Wagon R, Alto, Spacia, and Hustler are the backbone of its domestic business.

The strategic significance of kei dominance is often underestimated by foreign observers. Kei vehicles are highly engineered packages — minimal weight, tight tolerances, and razor-thin margins that reward manufacturing discipline. The skills Suzuki refined building 660cc minicars for Japan translated directly into building affordable 800cc and 1.0-liter cars for India, where price sensitivity is similarly severe and infrastructure similarly demanding.

India: the bet that defined a company

In 1981, when most Japanese automakers were focused on cracking the United States, Osamu Suzuki accepted an invitation from the Indian government to partner with state-owned Maruti Udyog. India in 1981 had a closed economy, an annual passenger car market of fewer than 40,000 vehicles, and no domestic manufacturer capable of building a modern small car. Suzuki took a 26% stake. Toyota, Nissan, and Honda had all passed on the opportunity.

The Maruti 800, launched in 1983, was effectively a rebadged Suzuki Alto. It became the car that motorised India’s emerging middle class. Maruti Udyog was progressively privatised, listed on Indian exchanges, and renamed Maruti Suzuki India. Today Suzuki owns approximately 58% of Maruti Suzuki India, which itself commands approximately 40% to 42% of India’s passenger vehicle market — roughly the share that General Motors held in the United States at its mid-twentieth-century peak.

The numerical scale is staggering. Maruti Suzuki produces well over 1.5 million vehicles annually in India. India is now Suzuki’s single largest market by units sold, larger than Japan, and the Indian passenger car market overtook Japan’s around 2022 to become the world’s third-largest after China and the United States.

Equally important is the dealer and service infrastructure Suzuki has spent four decades building across India. Maruti Suzuki has well over 3,000 sales outlets and an even larger service network reaching into India’s second- and third-tier cities, where most foreign automakers still struggle to maintain coverage. In an emerging market, distribution depth is the genuine moat — more durable than any single product cycle. Rebuilding such a network from scratch would take a competitor approximately a decade and require billions of dollars of investment, with no guarantee of matching Suzuki’s brand familiarity in semi-urban and rural India.

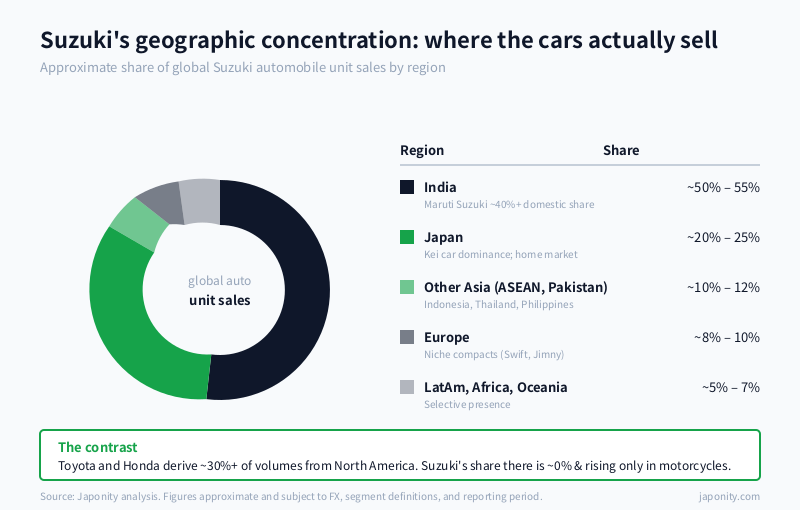

Global sales: where Suzuki actually sells cars

The geographic concentration of Suzuki’s business has no parallel among major Japanese automakers. Toyota and Honda derive roughly a third of their volumes from North America. Suzuki withdrew from the US passenger car market in 2012 and has never returned. The table below shows the approximate distribution of Suzuki’s global automobile unit sales by region.

| Region | Approximate share of global auto unit sales | Strategic role |

|---|---|---|

| India | ~50% – 55% | Volume engine; Maruti Suzuki ~40%+ domestic share |

| Japan | ~20% – 25% | Kei car dominance; high-margin home market |

| Europe | ~8% – 10% | Niche compacts (Swift, Vitara, Jimny) |

| Other Asia (Pakistan, Indonesia, Thailand, Philippines) | ~10% – 12% | Affordable small cars; ASEAN production hubs |

| Latin America, Africa, Oceania | ~5% – 7% | Selective presence, often via local partners |

| North America | ~0% (motorcycles, marine only) | Withdrew from US passenger cars in 2012 |

This is not the portfolio of a global generalist. It is the portfolio of a specialist that decided, deliberately, where it could win and where it could not.

The Volkswagen divorce

In 2009, Osamu Suzuki announced a capital and technology alliance with Volkswagen. VW would take approximately 19.9% of Suzuki and Suzuki would buy approximately 1.5% of VW. The strategic logic was clean on paper: Suzuki gained access to diesel and hybrid technology; VW gained an entry point into the small-car segments and emerging markets where it lagged. Osamu Suzuki later described it as having looked promising for “about a year.”

The partnership unravelled over what Suzuki perceived as VW’s attempt to treat it as a subsidiary rather than an equal partner — including disputes over technology access and Suzuki’s separate sourcing arrangement with Fiat for diesel engines. In 2011, Suzuki publicly asked Volkswagen to sell back its stake. VW refused. Suzuki took the case to the International Court of Arbitration in London. In 2015, the arbitration ruled that VW must divest. Suzuki repurchased the shares. The episode is now a case study in Japanese boardrooms on the perils of letting a larger partner near your equity.

The Toyota tie-up: a different model

In 2019, Suzuki and Toyota took the lessons of the VW episode and constructed a relationship deliberately designed to avoid them. Toyota acquired approximately 4.94% of Suzuki, and Suzuki acquired a roughly equivalent stake in Toyota — small, symmetric, and explicitly framed as a capital alliance rather than a controlling stake. Toyota offers Suzuki access to its hybrid and battery-electric platforms; Suzuki offers Toyota its small-car expertise and Indian manufacturing footprint.

For Toyota, the appeal is straightforward: India is the only large auto market in which it has never built a strong position, and partnering with the market leader is cheaper than competing with it. For Suzuki, the appeal is technological: the capital cost of developing a competitive EV platform from scratch exceeds what a company of its size can comfortably absorb.

The early outputs of the partnership are already visible. Toyota has begun selling rebadged versions of Maruti Suzuki vehicles in India under its own brand, while Suzuki has gained access to Toyota’s hybrid technology and shared component development. Both companies have also coordinated on a joint electric vehicle and battery investment in India estimated at multiple billions of dollars. The arrangement is, in many ways, a textbook example of what a Japanese-style equity alliance is supposed to look like when both sides understand the limits of control.

Beyond cars: motorcycles, outboards, ATVs

Suzuki’s non-automotive businesses are easy to overlook from Japan but are globally significant. The motorcycle business — Suzuki sold its first motorcycle, the Power Free, in 1952 — remains a top-five global player, with strong positions in India, Indonesia, and the Philippines. The GSX-R sportbike lineage has defined Japanese supersport motorcycling for four decades.

The marine outboard engine business is, in some respects, even more strategically valuable. Suzuki is one of the world’s three largest manufacturers of outboard motors, alongside Yamaha and the American firm Mercury Marine. Outboard engines are high-margin, low-cyclicality products sold into a relatively wealthy global recreational boating market. They are also a useful hedge: marine demand is uncorrelated with automotive cycles. Suzuki also operates a meaningful all-terrain vehicle business, particularly in North America, where its cars are absent but its powersports products are well-distributed.

The Osamu Suzuki era and after

Osamu Suzuki — born Osamu Matsuda, who took the Suzuki name when he married into the founding family in 1958 — became president in 1978 and chairman in 2000, and remained the company’s dominant strategic voice until his retirement in 2021. He died in late 2024. His son Toshihiro Suzuki, who became president in 2015 and chairman in 2021, now leads the company. The succession has been deliberate, generational, and family-anchored — a pattern more reminiscent of Toyota than of the professionalised boards of Honda or Nissan.

The strategic question facing Toshihiro Suzuki is whether emerging-market dominance is a durable franchise in an electric and software-defined automotive era. India has the world’s most price-sensitive large-car market and one of its least developed EV charging networks. Suzuki has announced a multi-billion-dollar Indian EV investment plan in partnership with Toyota, including local battery production. Whether Chinese entrants — BYD, Great Wall, MG — can replicate the manufacturing-and-distribution depth that Suzuki spent forty years building in India is the single most important question for the company’s next decade.

Why Suzuki is Japan’s most underrated automaker

Suzuki rarely features in Western coverage of the Japanese automotive industry, which tends to fixate on Toyota’s scale, Honda’s engineering, and Nissan’s troubles. Yet Suzuki has done something none of those companies has done: built a near-monopoly position in a market of more than 1.4 billion people. Its market capitalisation is a fraction of Toyota’s, but its return on capital in India has been, for decades, among the highest in the global auto industry. Kei dominance in Japan plus emerging-market dominance abroad is not a glamorous strategy. It is, however, an extraordinarily resilient one.

For Japanese policymakers concerned about the country’s industrial future in Asia, Suzuki is also the closest thing to a national champion in a region where Chinese brands are advancing rapidly. The next ten years will determine whether the company built around an old loom maker’s small-engine instincts can carry that franchise into an electric era.

FAQ

Why does Suzuki dominate the Indian car market?

Suzuki entered India in 1981 through a partnership with state-owned Maruti Udyog at a time when Toyota, Honda, and Nissan all declined the opportunity. Through approximately four decades of localisation, dealer-network depth, and small-car expertise inherited from Japan’s kei segment, Suzuki — via its approximately 58%-owned Maruti Suzuki India — has built a domestic share of around 40% to 42%.

Why did Suzuki end its alliance with Volkswagen?

The 2009 capital and technology alliance with Volkswagen broke down over disputes about technology access, Suzuki’s separate engine-sourcing arrangement with Fiat, and what Suzuki characterised as VW treating it as a subsidiary. The matter was referred to international arbitration, and in 2015 the tribunal ordered VW to return its approximately 19.9% stake to Suzuki.

What is a kei car and why does it matter?

Kei (light) cars are a regulated Japanese vehicle category with engines capped at 660cc and length capped at around 3.4 meters, benefiting from lower taxes and insurance. They account for approximately 35% to 40% of new car sales in Japan. Suzuki and Daihatsu have led this segment for decades, and the kei business is highly profitable for both companies.

Why did Suzuki withdraw from the United States?

Suzuki exited the US passenger car market in 2012 after years of declining sales and an unsustainable cost structure for what had become a small-volume operation. It maintains a US presence in motorcycles, marine outboard engines, and ATVs, but no longer sells cars in North America.

Who runs Suzuki today?

Toshihiro Suzuki, son of the late Osamu Suzuki, has served as president since 2015 and chairman since 2021. He inherits a company still strongly shaped by his father’s four-decade tenure but now navigating the electric transition and increasing Chinese competition in Suzuki’s core emerging-market territories.

Working with Suzuki

Suzuki’s global supply chain spans automotive components, motorcycle parts, marine engineering, and electronic systems, with major manufacturing hubs in Japan, India, Hungary, Thailand, Indonesia, and Pakistan. For overseas partners — component suppliers, software vendors, EV-charging operators, marine distributors, dealer-network investors — Suzuki’s procurement structure is unusual among Japanese OEMs in that decisions are often made closer to the regional market, particularly in India.

If you are exploring a partnership, supply, or distribution opportunity with Suzuki or Maruti Suzuki India, Japonity’s business matching service can connect your company with the right counterparties in Japan and in Suzuki’s major overseas hubs.

Related from Japonity — Japan’s automakers

- Toyota Motor Corporation — Multi-pathway powertrain strategy from the world’s #1 automaker

- Honda Motor — The motorcycle giant the auto press forgot

- Nissan Motor — Post-Ghosn, post-Honda — what the Renault entanglement still means

- Mazda Motor Corporation — The Hiroshima underdog that bet on internal combustion

- Subaru Corporation — The boxer-engine niche player that built America

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →