In April 2010, on the floor of the Tokyo Stock Exchange, a 108-year-old mutual life insurer rang the bell as a public company. Dai-ichi Mutual Life Insurance — founded in 1902 as Japan’s first mutual life insurer — had spent more than a century owned by its policyholders. Then, in a single day, it became Dai-ichi Life Insurance Company, a listed entity with a market capitalization that briefly made it one of the largest IPOs of the year and the first major Japanese life insurer to demutualize. Five years later, the same company would write a check of approximately $5.7 billion for Protective Life Corp of Birmingham, Alabama, transforming itself from a domestic incumbent into a top-30 player in the world’s largest life-insurance market. Today, as Dai-ichi Life Holdings (TSE: 8750), the group spans Japan, the United States, Australia, and a minority equity position in Janus Henderson — a global asset manager listed in New York. For foreign asset managers, reinsurers, and acquirers looking at Japan’s shrinking domestic life pie, Dai-ichi is the case study of what happens when a Japanese life insurer decides the math no longer works at home.

From mutual to listed: the 2010 demutualization

The Japanese life-insurance industry was built on mutuals. For most of the twentieth century, the country’s largest life insurers — Nippon Life, Dai-ichi Mutual, Meiji Yasuda, Sumitomo Life — were owned by their policyholders, with no shareholders, no listed equity, and no obvious mechanism for raising capital from public markets. The structure worked when life-insurance penetration was rising, premium income was growing, and Japanese savers had limited alternatives. By the late 2000s, none of those conditions held.

Dai-ichi moved first. In April 2010, after years of internal preparation and regulatory navigation, the company converted from a mutual into a stock-form joint-stock company and listed on the Tokyo Stock Exchange the same day. Approximately 8 million former policyholders received shares or cash compensation. The IPO was, by some measures, the largest in the world that year. More importantly, it gave Dai-ichi something its peers still lacked: a listed currency for acquisitions, a transparent market valuation, and a shareholder base that would expect — and force — capital discipline.

The contrast with Japan’s other life giants is stark. Nippon Life, the largest by premium income, remains a mutual to this day. Meiji Yasuda — formed by the 2004 merger of Meiji Life and Yasuda Life — is also still mutual. Sumitomo Life is mutual. Of the four traditional giants, Dai-ichi is the only one whose strategic decisions are visible in quarterly disclosures and whose CEO faces equity analysts every three months. That visibility is both a constraint and a weapon.

Why the domestic life market is shrinking

The numbers behind Dai-ichi’s overseas push are not subtle. Japan’s population peaked around 2008 and has been declining ever since. The cohort that buys life insurance most aggressively — households in their thirties and forties with young children and mortgages — has been shrinking for two decades. New policy sales at the major Japanese life insurers have been broadly flat to declining for years, and ultra-low interest rates have made it difficult to generate spread on the bond-heavy general-account portfolios that traditionally backed long-duration liabilities.

Japanese life insurers cannot grow their way out of this by selling more policies to the same shrinking pool. They have three options: consolidate domestically, pivot into asset accumulation and savings products (variable annuities, foreign-currency-denominated whole life), or buy growth abroad. Dai-ichi has done all three — but it is the third leg that distinguishes it.

Protective Life: the $5.7 billion US bet

In June 2014, Dai-ichi announced an agreement to acquire Protective Life Corp, a mid-sized US life insurer headquartered in Birmingham, Alabama. The deal closed in February 2015 at a value of approximately $5.7 billion, paid entirely in cash. At the time, it was one of the largest outbound acquisitions by a Japanese life insurer and a clear statement of intent: Dai-ichi would not be a domestic-only story.

Protective gave Dai-ichi several things at once. It delivered scale in the world’s largest life-insurance market, with a position generally cited as among the top 30 US life insurers by various measures. It provided exposure to a product mix — term life, universal life, and a substantial annuity book — that complemented Dai-ichi’s Japan-heavy general-account business. And it brought Protective’s signature capability: the acquisition and management of closed blocks of life-insurance policies from other US carriers exiting non-core lines. In the years since 2015, Protective has continued to execute that strategy, acquiring blocks from major US life insurers and reinsurance counterparties.

Crucially, Dai-ichi has run Protective with significant operational autonomy. The Birmingham headquarters remained, the management team continued, and the Japanese parent has resisted the temptation — common in cross-border insurance M&A — to centralize underwriting or product decisions in Tokyo. For US reinsurers, brokers, and asset managers, Protective remains the relevant counterparty; Dai-ichi is the capital provider and strategic backstop.

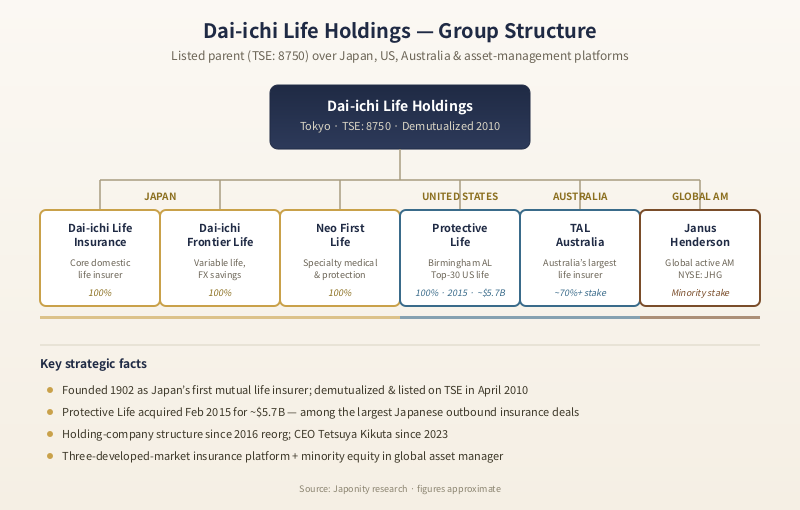

The Dai-ichi Life Holdings group structure

The current corporate architecture dates to a 2016 reorganization, when Dai-ichi Life Insurance — the listed entity from 2010 — restructured itself into Dai-ichi Life Holdings, with the operating life-insurance business becoming a subsidiary. The change was less cosmetic than it might appear: it allowed the group to manage Japan, US, and Australia operations as parallel subsidiaries rather than forcing the overseas businesses to sit awkwardly under a domestic Japanese life insurer.

Under the Holdings parent (TSE: 8750), the group includes Dai-ichi Life Insurance Company — the original domestic life business and still the largest single subsidiary by assets — alongside Dai-ichi Frontier Life, which focuses on variable life and foreign-currency-denominated savings products distributed largely through bank channels; and Neo First Life, a specialty insurer focused on medical and protection products. Outside Japan, the holdings include Protective Life in the United States, TAL — the Australian life insurer in which Dai-ichi holds a stake of approximately 70 percent or more, and which is generally regarded as Australia’s largest life insurer by some measures — and a minority equity position in Janus Henderson Group (NYSE: JHG), the global active asset manager formed by the 2017 merger of Janus Capital and Henderson Group.

The Janus Henderson stake is strategically distinct from the insurance subsidiaries. It gives Dai-ichi exposure to the economics of third-party asset management — fee income that scales with AUM rather than with policy sales — and a foothold in a sector where Japanese life insurers have historically been buyers of asset-management services rather than owners of capacity. The relationship runs deeper than passive equity: Janus Henderson is a significant manager of Dai-ichi’s investment assets in certain mandates, and the cross-shareholding reflects an alignment of interests that has survived several rounds of asset-management industry consolidation.

How Dai-ichi compares with Japan’s other life giants

For foreign counterparties trying to understand where Dai-ichi sits in the Japanese life landscape, a three-way comparison with the largest mutuals is the most useful frame.

| Insurer | Structure | Founded | Overseas footprint | Strategic posture |

|---|---|---|---|---|

| Dai-ichi Life Holdings | Listed (TSE: 8750), demutualized 2010 | 1902 | Protective Life (US, 100%), TAL (Australia, ~70%+), Janus Henderson stake | Aggressive overseas M&A; listed-company capital discipline |

| Nippon Life | Mutual (unlisted) | 1889 | Stakes in Reliance Nippon (India), MLC (Australia), Great-West Lifeco (Canada) interests | Selective minority stakes; largest by domestic premium |

| Meiji Yasuda Life | Mutual (unlisted) | 1881 (Meiji); 2004 merger | StanCorp Financial (US, 100%) | One major US platform; otherwise Japan-focused |

Three observations follow. First, Dai-ichi is the only one of the three with a listed share price and the disciplines that come with it. Second, it has the most diversified overseas footprint — not just one big US acquisition but a multi-platform structure spanning insurance and asset management across three developed markets. Third, the demutualization gave it a structural advantage in M&A: cash, shares, and analyst-validated currency in a way the mutuals lack.

The leadership question

Tetsuya Kikuta became president and CEO of Dai-ichi Life Holdings in 2023, succeeding the leadership that had executed the Protective deal and the holding-company reorganization. Kikuta’s mandate, in broad strokes, has been to extend the diversification strategy while addressing the cultural and governance work that follows any cross-border insurance combination. Dai-ichi has, like most Japanese listed companies, also faced increased scrutiny under Tokyo Stock Exchange reforms pushing companies trading below book value to articulate concrete plans for improving return on equity — pressure that the mutual peers do not face in the same way.

The leadership transition also coincides with a generational shift in how Japanese financial institutions think about overseas expansion. The first wave — Dai-ichi’s Protective deal, MUFG’s Morgan Stanley investment, SMBC’s various overseas footprints — was about deploying surplus capital from a saturated home market. The current wave is more deliberate: building integrated cross-border platforms, sharing investment capabilities across subsidiaries, and treating overseas units as growth engines rather than passive holdings. Dai-ichi’s group structure — with operating subsidiaries in three developed markets and a stake in a global asset manager — is one of the more developed examples of this second-wave thinking among Japanese life insurers.

What foreign counterparties should understand

For foreign asset managers, reinsurers, brokers, and potential acquirers, several practical points follow from Dai-ichi’s structure.

For asset managers, Dai-ichi is one of the largest pools of institutional capital in Japan and has demonstrated willingness to invest meaningfully with overseas managers — both via direct mandates from the Tokyo investment office and via the Janus Henderson relationship. Mandates from Japanese life insurers have historically been concentrated in foreign credit, structured products, and increasingly in private markets as ultra-low domestic yields force a search for spread. Dai-ichi’s listed status makes its investment shifts more visible than those of its mutual peers, which sometimes makes it a useful weathervane for the industry.

For reinsurers, the relevant counterparties are the operating subsidiaries — Dai-ichi Life Insurance in Japan, Protective in the US, TAL in Australia — not the holding company. Reinsurance treaty negotiations, longevity-risk transfers, and closed-block transactions all sit at the operating level. That said, the holding-company structure means that capital-allocation decisions across the three insurance platforms are visible to a single Tokyo-based management team, which can accelerate decisions on large transactions.

For potential M&A counterparties, Dai-ichi’s behaviour since 2015 suggests a clear pattern: it will pay full prices for high-quality platforms in developed insurance markets, it will leave operating management largely in place, and it will integrate at the holding-company level rather than collapsing operations into Tokyo. The Protective and TAL track records are the empirical basis for this. Sellers prioritizing continuity for their management and policyholders have, on the available evidence, found Dai-ichi a relatively predictable buyer.

For the broader question of Japan’s life-insurance future: Dai-ichi is the listed proxy. Its share price, its capital allocation choices, and its annual disclosures are the most transparent window into how a major Japanese life insurer is responding to demographic decline, ultra-low rates, and the structural reality that the domestic pie is shrinking. The mutuals will make similar choices, but they will make them more quietly. Dai-ichi makes them in public — and the rest of the global insurance industry has been watching since 2010.

FAQ

When was Dai-ichi Life founded and when did it list?

Dai-ichi was founded in 1902 as Dai-ichi Mutual Life Insurance Company — Japan’s first mutual life insurer. It demutualized and listed on the Tokyo Stock Exchange in April 2010, the first major Japanese life insurer to do so. The current listed parent, Dai-ichi Life Holdings, was established through a 2016 reorganization. TSE code 8750.

What is Protective Life and why did Dai-ichi buy it?

Protective Life Corp, headquartered in Birmingham, Alabama, is a US life insurer with a substantial term life, universal life, and annuity business, and a specialism in acquiring closed blocks of policies from other carriers. Dai-ichi announced the acquisition in 2014 and closed it in February 2015 for approximately $5.7 billion in cash. The deal gave Dai-ichi a top-30 US life-insurance position and a hedge against the structural decline of the Japanese domestic life market.

What is TAL and what is Dai-ichi’s stake?

TAL is an Australian life insurer headquartered in Sydney and is generally regarded as one of Australia’s largest life insurers by certain measures. Dai-ichi holds a controlling stake of approximately 70 percent or more, acquired in stages over several years. TAL operates as a stand-alone subsidiary under the Dai-ichi Holdings umbrella.

What is the relationship with Janus Henderson?

Dai-ichi holds a minority equity stake in Janus Henderson Group (NYSE: JHG), the global active asset manager formed by the 2017 merger of Janus Capital and Henderson Group. The relationship is both equity-based and operational: Janus Henderson manages a portion of Dai-ichi’s investment assets, and the cross-shareholding aligns interests across asset-management mandates.

Who runs Dai-ichi Life Holdings?

Tetsuya Kikuta has served as president and CEO of Dai-ichi Life Holdings since 2023. The group is headquartered in Tokyo and listed on the Tokyo Stock Exchange under code 8750.

Working with Dai-ichi Life

For foreign asset managers exploring Japanese institutional mandates, reinsurers negotiating treaties with Protective or TAL, brokers structuring closed-block transactions, or strategic counterparties considering cross-border insurance M&A, Dai-ichi Life Holdings is one of the most relevant counterparties in the Asia-Pacific life-insurance landscape. Japonity’s business matching service helps overseas firms identify the right point of contact within complex Japanese financial groups — whether the relevant entity is the Tokyo holding company, a domestic insurance subsidiary, or an overseas platform such as Protective Life or TAL — and navigate the introduction process from a position of context.

Related from Japonity — Japan’s life insurers

- Nippon Life Insurance — Japan’s largest life insurer — the unlisted mutual giant

- Meiji Yasuda Life — Japan’s #3 life insurer — mutual holdout, StanCorp US

- Sumitomo Life Insurance — Japan’s #4 life insurer — the third mutual holdout + Symetra US

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →