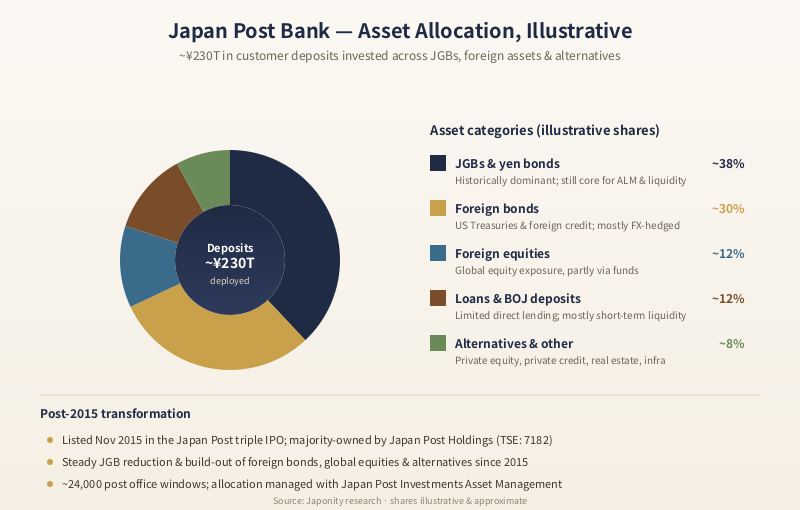

With approximately ¥230 trillion in customer deposits, Japan Post Bank (ゆうちょ銀行) is Japan’s largest bank by deposit base — a savings behemoth roughly ten times larger than the megabank deposit franchises against which it is so often compared. Created in October 2007 out of the postwar Postal Savings System and listed in 2015 as part of Japan’s triple IPO, it has long functioned as the country’s most prolific buyer of Japanese Government Bonds. Since 2015, however, a quiet revolution has been underway: a multi-trillion-yen pivot into US Treasuries, foreign credit, global equities and alternatives that has effectively turned the bank into Asia’s largest pension-fund-like institution.

A Bank Unlike Any Other in Japan

To understand Japan Post Bank, it helps to dispense with the word “bank” for a moment. The institution does not lend to corporations. It does not chase corporate banking league tables. Its mortgage business runs almost entirely through partner banks. What it does — at a scale no other Japanese financial institution can match — is gather household deposits through approximately 24,000 post office windows scattered across every prefecture, mountain town and island in the country, and then invest those deposits in financial markets.

In effect, Japan Post Bank is a giant deposit-funded investment vehicle wearing the regulatory clothing of a commercial bank. Its sheer size makes its allocation decisions globally consequential. When the bank tilts its portfolio by even a few percentage points, that shift can be measured in tens of trillions of yen — enough to move sovereign bond markets and ripple through global asset prices.

The bank is listed on the Tokyo Stock Exchange under code 7182, with Japan Post Holdings retaining a majority stake. Its headquarters sits in Shinagawa, Tokyo, and the institution is led by president Kazumasa Yoshida.

From Postal Savings System to Listed Bank

The history of Japan Post Bank is inseparable from one of the most enduring institutions of the modern Japanese state: the Postal Savings System (郵便貯金), which traces its roots back to 1875. For more than a century, ordinary Japanese households used the local post office not only to send mail but also to save money — a system reinforced by the country’s culture of thrift, its dense post office network and explicit government backing.

By the 1990s, the Postal Savings System had grown into the largest single pool of household savings on the planet, with funds channeled through the Fiscal Investment and Loan Program (財政投融資, FILP) into infrastructure, public corporations and policy lending. To critics — including a generation of reform-minded politicians led by Junichiro Koizumi — this concentration of household savings inside a state-run conduit had become a structural distortion of Japan’s financial system.

The 2005–2007 postal privatization reform broke up Japan Post into separate corporate entities. In October 2007, the savings business was spun out as Japan Post Bank Co., Ltd. under the umbrella of Japan Post Holdings. Eight years later, in November 2015, the famous “triple IPO” listed Japan Post Holdings, Japan Post Bank and Japan Post Insurance simultaneously on the Tokyo Stock Exchange — one of the largest equity offerings in Japanese history and a symbolic completion of the privatization project.

The Scale of Deposits: Bigger Than Any Megabank

For non-Japanese readers, the deposit numbers can seem implausible. Approximately ¥230 trillion in customer deposits places Japan Post Bank in a category by itself within Japan, comfortably larger than the deposit bases of the three megabank groups — Mitsubishi UFJ Financial Group (MUFG), Sumitomo Mitsui Financial Group (SMFG) and Mizuho Financial Group — even though those groups have larger total balance sheets thanks to their corporate lending books and overseas operations.

| Institution | Approx. customer deposits | Lending profile | Network |

|---|---|---|---|

| Japan Post Bank (7182) | ~¥230 trillion | No direct corporate lending; mortgages via partners | ~24,000 post office windows nationwide |

| MUFG Bank (subsidiary of 8306) | Considerably smaller deposit base | Full corporate, retail and global lending | Domestic branches plus extensive overseas network |

| Sumitomo Mitsui Banking Corp. (subsidiary of 8316) | Considerably smaller deposit base | Full corporate and retail lending | Domestic and global corporate network |

| Mizuho Bank (subsidiary of 8411) | Considerably smaller deposit base | Full corporate and retail lending | Domestic and global corporate network |

The reason for the gap is structural. Megabanks compete for deposits primarily in urban areas and through corporate cash management. Japan Post Bank, by contrast, inherited a century-old retail savings franchise built on the densest physical footprint in Japan — including thousands of rural and small-town post offices where it remains, in practice, the only deposit-taking institution within easy reach. For pensioners, farmers and households in regional Japan, “the post office” and “the bank” have long been synonymous.

The JGB-Buying Machine

For most of its history, Japan Post Bank channeled this enormous deposit base into a single instrument: Japanese Government Bonds (JGBs). At its peak, the bank held the largest single-institution JGB portfolio in Japan, dwarfing the holdings of any megabank, life insurer or trust bank. This was not an accident but a design feature of the postwar financial system, which used post office savings to absorb sovereign issuance and to fund FILP at favorable yields.

As the Bank of Japan’s balance sheet ballooned under quantitative and qualitative easing (QQE) from 2013 onwards — and especially after the 2016 introduction of yield curve control — JGB yields collapsed and a heavy JGB book became progressively less remunerative. For Japan Post Bank, with its enormous deposit base and limited loan business, this created a structural pressure that no megabank faced to the same degree: roll over hundreds of trillions of yen of assets into instruments yielding close to zero, or look elsewhere.

It chose the latter.

The Post-2015 Diversification: Becoming a Pension Fund in All But Name

Since the 2015 IPO, Japan Post Bank’s investment strategy has been transformed. The bank’s medium-term plans, public investor presentations and securities filings have all pointed in the same direction: a methodical reduction of JGB exposure and a steady build-up of foreign bonds (chiefly US Treasuries and high-grade foreign credit), foreign equities, alternative investments and private market exposures.

The mechanics of this shift matter. The bank does not, as a rule, take large directional currency bets; the bulk of its foreign bond exposure is hedged, which means the economics depend not only on foreign yields but on cross-currency basis swaps and hedging costs. When those costs rise — as they did sharply during US Federal Reserve tightening cycles — the hedged yield pickup over JGBs can compress dramatically, which in turn forces re-allocations.

Alternative investments — including private equity, private debt and real estate funds — have been built up through partnerships and through the group’s own asset management arm, Japan Post Investments Asset Management. The shift is partial rather than wholesale; the bank still holds a very large stock of JGBs and short-dated yen instruments for liquidity, regulatory and ALM reasons. But the directional trend is unmistakable: a savings bank reborn as something closer to a giant institutional asset allocator.

In aggregate terms, the picture that emerges is of an institution whose risk profile, return drivers and asset mix increasingly resemble those of a national pension fund. The comparison most often invoked — fairly or not — is with the Government Pension Investment Fund (GPIF), whose ~¥200 trillion or so of assets makes it the world’s largest pension fund. Japan Post Bank is now, by some measures, an asset allocator on a comparable scale, even though it operates under banking rather than pension regulation.

What Japan Post Bank Does — and Does Not — Do

For corporates and overseas investors trying to map the institution to a Western analogue, the easiest way is to enumerate what Japan Post Bank explicitly does and does not do.

What it does

- Retail deposits at unmatched scale: approximately ¥230 trillion gathered through post office windows, ATMs and online channels, including ordinary deposits, time deposits and the popular TEIGAKU (定額) savings product.

- Securities investment: the deposits are deployed into JGBs, foreign sovereigns, foreign credit, global equities, alternatives and money-market instruments — the asset management function that now defines the institution.

- Payments and remittances: ATMs, domestic transfers, payroll deposits, public pension payouts and a high-volume small-ticket remittance business that takes advantage of the post office network.

- Investment trust and insurance distribution: through post office counters, the bank distributes investment trusts and (via the group) insurance products to retail savers.

- Cards and consumer finance: the JP BANK CARD line and partnerships covering credit, debit and prepaid use cases.

What it does not do

- Direct corporate lending, in the manner of MUFG, SMBC or Mizuho. Mortgages and consumer loans are intermediated via partner banks rather than originated directly on Japan Post Bank’s balance sheet.

- Large-scale international branch banking. Unlike the megabanks, which have built out substantial overseas wholesale franchises, Japan Post Bank’s overseas footprint is largely an investment one, executed through the markets.

- Investment banking and capital markets origination in the front-office sense. The bank is a buyer and holder of securities, not a syndicate desk.

Why This Matters for Japan — and for Global Markets

The scale of Japan Post Bank’s portfolio is such that its allocation choices have consequences well beyond its own balance sheet. Three implications stand out.

First, sovereign bond markets. A meaningful reduction in JGB holdings by Japan Post Bank — even of a few percentage points — represents tens of trillions of yen of demand that must be replaced by other buyers. As the Bank of Japan gradually normalizes monetary policy, the question of who absorbs JGB issuance becomes a first-order concern, and Japan Post Bank’s behavior is closely watched by policymakers and primary dealers alike.

__BIZPHOTO__

Second, global fixed income. Japan Post Bank is one of the largest single foreign holders of US Treasuries and a meaningful buyer of euro-denominated and emerging-market sovereign and credit instruments. Its hedging behavior, in turn, is a material driver of cross-currency basis markets.

Third, alternative assets. As the bank expands into private equity, private credit, infrastructure and real estate funds, it has become a sought-after limited partner for global asset managers seeking long-duration, patient capital. That role is likely only to deepen in the coming decade.

The Strategic Question: What Is a Deposit-Funded Asset Manager Worth?

The question that hovers over Japan Post Bank — and that its public market valuation has had to grapple with since the 2015 IPO — is essentially this: how should investors value a bank that does not really lend? Conventional bank valuation frameworks emphasize net interest margin, loan growth and credit quality. Japan Post Bank’s earnings profile is driven instead by securities portfolio yield, FX hedging costs, equity market beta and the cost discipline of running a vast retail deposit franchise.

The plausible analogues — large insurers, pension funds, sovereign wealth funds, asset managers — each capture only part of the picture. The bank’s continued majority ownership by Japan Post Holdings, the government’s residual stake in the holdco, and the social policy role of the post office network add further layers of complexity that pure-financial frameworks do not capture.

What is clear is that Japan Post Bank is no longer the institution that listed in 2015. Its asset mix, its risk profile and its role in global capital markets have all evolved. For overseas partners — whether asset managers seeking LP capital, sovereign issuers studying demand for their paper, or technology vendors selling into Japan’s largest retail deposit-taker — understanding this evolution is now essential.

FAQ

What is Japan Post Bank?

Japan Post Bank (ゆうちょ銀行) is Japan’s largest bank by customer deposits, with approximately ¥230 trillion gathered through approximately 24,000 post office windows. It was created in October 2007 from the postwar Postal Savings System and listed on the Tokyo Stock Exchange (code 7182) in November 2015 as part of the Japan Post triple IPO.

Why is Japan Post Bank’s deposit base so much larger than the megabanks’?

The bank inherited a savings franchise that dates back to 1875 and the densest physical footprint of any financial institution in Japan. In rural areas and small towns, the post office is often the only deposit-taking outlet within easy reach, which produces a structurally larger household deposit base than the megabanks can match — even though the megabanks have larger total balance sheets thanks to corporate lending.

Does Japan Post Bank lend to companies?

No. Japan Post Bank does not undertake direct corporate lending in the way Japan’s megabanks do. Its mortgage and consumer loan business is largely intermediated through partner banks. The institution functions primarily as a deposit-funded investor in securities and other assets.

How has Japan Post Bank’s investment strategy changed since 2015?

Historically the bank’s deposits were invested overwhelmingly in Japanese Government Bonds. Since the 2015 IPO, the bank has steadily diversified into foreign bonds (notably US Treasuries), foreign equities and alternative investments such as private equity, private credit and real estate funds, working through its in-house asset management arm and external partners.

How is Japan Post Bank owned and governed?

Japan Post Bank is listed on the Tokyo Stock Exchange under code 7182. Japan Post Holdings retains a majority stake, while Japan Post Holdings itself remains partly owned by the Japanese government. The bank is headquartered in Shinagawa, Tokyo, and is led by president Kazumasa Yoshida.

Working with Japan Post Bank

For overseas asset managers, technology vendors, sovereign issuers and corporate partners, Japan Post Bank represents one of the most significant pools of long-duration capital in Asia — and one of the country’s most consequential retail financial institutions. Whether you are pitching an alternatives strategy, supplying core banking technology to a 24,000-window network, or seeking to understand demand dynamics for sovereign or credit issuance in Japan, building the right relationship matters.

Japonity’s Business Matching service connects overseas companies with leading Japanese financial institutions, technology partners and corporates. Explore opportunities at /business-matching/.

Related from Japonity — Japan Post Group

- Japan Post Holdings — The half-privatized postal-banking-insurance empire

- Japan Post Insurance — The post-office life insurer rebuilding after the 2019 scandal

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →