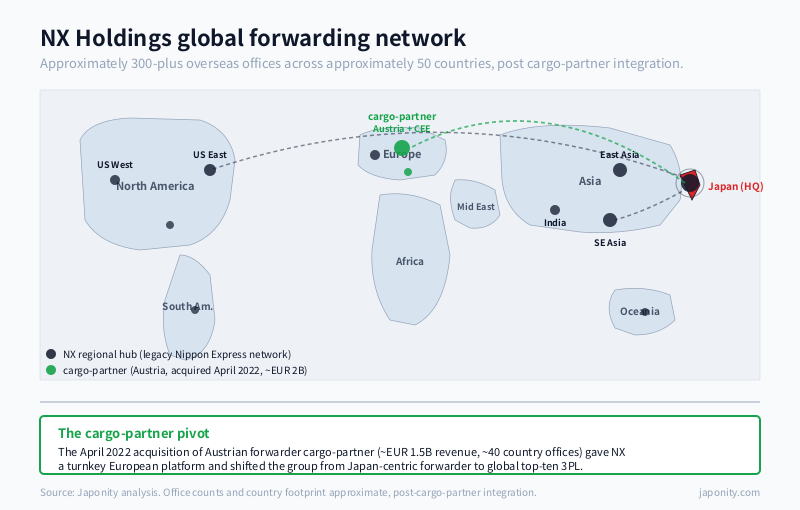

NX Holdings, Inc. — the Tokyo-listed parent that most foreigners still know by the older name Nippon Express — is the Japanese logistics company that the country’s domestic parcel chatter tends to forget. While Yamato and Sagawa fight over Takkyubin boxes inside the archipelago, NX Holdings runs approximately 700 group entities and operates in approximately 50 countries from roughly 300-plus overseas offices, generating around two trillion yen of revenue and ranking inside the global top ten of third-party logistics providers by forwarding volume. In April 2022 it completed the largest international acquisition in its history — Austria-headquartered cargo-partner GmbH, an Asia-Europe air-and-sea forwarder, for approximately two billion euros — and gave itself, for the first time, a credible European platform to match its long-established Japanese and pan-Asian network. The combined business is now arguably Japan’s most internationally exposed logistics franchise, and one of the more interesting forwarding stories outside the integrators.

From a 1937 government-linked freight house to a global forwarder

Nippon Express Co., Ltd. (日本通運) was incorporated in October 1937, formed out of a consolidation of Japanese freight-forwarding businesses with origins in rail-linked cargo handling and a degree of government involvement that was characteristic of the era. For most of the post-war period it operated as the country’s dominant general-cargo forwarder and heavy-haulage specialist, with a domestic trucking and warehousing footprint that no rival could match. Its head office sits in Tokyo’s Chiyoda Ward, on the western side of Tokyo Station, and the company has been a fixture of the Tokyo Stock Exchange for decades — today trading under code 9147.

What separated Nippon Express from the rest of the domestic field, from very early on, was its appetite for international forwarding. While most Japanese transport companies remained essentially domestic until the 1990s, Nippon Express was building cross-border freight, customs-brokerage, and warehousing capacity through the post-war Japanese export boom. By the time the country’s manufacturers — Toyota, Sony, Panasonic, Komatsu, the trading houses — were placing factories across Southeast Asia, North America, and Europe, Nippon Express had already followed them with its own offices, in many cases co-locating with the customer’s overseas production base. That historic pull from outbound Japanese manufacturing is the spine of the international network the holding company runs today.

The corporate restructuring came in January 2022. Nippon Express Holdings, Inc. — subsequently rebranded NX Holdings, Inc. — was established as the listed pure-holding parent, with Nippon Express Co., Ltd. continuing underneath as the principal Japanese operating subsidiary, and the overseas regional businesses (NX Americas, NX Europe, NX East Asia, NX South Asia & Oceania, and so on) reorganised as regional holdings under the same umbrella. The change was structural rather than cosmetic. It separated the listed corporate-governance function from the operating P&L, made it possible to bolt on large overseas acquisitions without disturbing the Japanese parent, and signalled a strategic posture in which the international segment was no longer a side business attached to a domestic trucker.

What NX Holdings actually does

NX Holdings is not a parcel company. That single sentence is the most important fact for any reader trying to slot the group into a Western mental map. It does not run a household Takkyubin-style network; it does not chase Amazon last-mile volumes; it does not compete with Yamato or Sagawa in the consumer parcel market. What it does is move freight — air, sea, road, and rail — across borders for corporate customers, alongside a substantial domestic trucking, warehousing, and heavy-haulage business in Japan.

The group’s revenue mix, in round terms, breaks into a handful of identifiable lines. Air and ocean freight forwarding, including cargo-partner’s European book, is the largest international engine and accounts for a meaningful share of consolidated revenue. Contract logistics and warehousing — running customer warehouses, distribution centres, and value-added fulfilment under multi-year service contracts — is the next major leg, and is the one NX is actively trying to grow in the United States and continental Europe. Domestic transportation, principally Japanese trucking and rail-linked freight for industrial customers, remains a large and reliable, if slower-growing, contributor. And heavy haulage — the moving of nuclear reactor components, power-plant turbines, factory installations, and other oversized cargo — sits as a specialist segment with a small but defensible competitive moat, supplemented since 2020 by NX’s acquisition of Italy’s Franco Tosi Meccanica heavy-transport business.

| Operator | Approx. revenue scale | Centre of gravity | What they actually do |

|---|---|---|---|

| NX Holdings (Nippon Express) | ~JPY 2T+ | International forwarding + Japanese B2B trucking | Global air/ocean forwarding, contract logistics, heavy haulage, domestic freight |

| Yamato Holdings | ~JPY 1.7T+ | Japanese B2C parcel | Takkyubin home delivery, e-commerce fulfilment, moving services |

| SG Holdings (Sagawa Express) | ~JPY 1.4T+ | Japanese B2B + B2C parcel | Hikyaku parcel, B2B trucking, growing e-commerce share |

| Japan Post Logistics (Japan Post Holdings unit) | ~JPY 2T+ logistics segment | Universal-service mandate | Yu-Pack parcel, Japan Post Logistics (ex-Toll restructured), cross-border mail |

Comparisons are approximate, definitions and segment boundaries differ from operator to operator, and the four companies are not strictly substitutable — they compete in overlapping but distinct corners of the Japanese logistics market. The point of the table is to fix the order of magnitude and to make explicit that NX is the only one of the four that is built around international freight forwarding rather than around Japanese last-mile parcel.

The cargo-partner acquisition: buying a European platform

For most of the twenty-first century, Nippon Express’s European presence was creditable but thin — a network of branches inherited from following Japanese manufacturing customers into Germany, the United Kingdom, the Netherlands, and a handful of central European countries. It was good enough for Japan-Europe outbound freight, particularly air, but it lacked the intra-European trucking, the customs-brokerage density, and the logistics-park footprint that European corporate customers expected from a top-tier forwarder. By the late 2010s, that gap had become strategically uncomfortable: if NX wanted to position itself as a top-ten global forwarder competing for the same multinational contracts as DHL, Kuehne+Nagel, DB Schenker, DSV, and Expeditors, it needed European scale.

The answer arrived in 2022. In April of that year, Nippon Express Holdings completed the acquisition of cargo-partner GmbH — the Austrian-headquartered international freight-forwarding group with strong Asia-Europe air and sea capability, a network of roughly forty country offices concentrated in central, eastern, and southern Europe, and reported revenues of approximately 1.5 billion euros in the period before closing. The deal value was reported at approximately two billion euros and was, by a wide margin, the largest cross-border M&A transaction in Nippon Express’s history.

The strategic logic was specific. Cargo-partner brought NX a turnkey European platform with deep intra-European trucking, a strong Vienna-anchored air-cargo gateway, and significant exposure to the Asia-Europe trade lane that NX was already running freight on from the Japanese side. The fit was complementary rather than overlapping — cargo-partner’s European customer book was not duplicating NX’s existing Japan-multinational accounts, and cargo-partner’s Asia footprint was small enough that there was little inside-the-acquired-business cannibalisation risk with NX Asia. From a financial standpoint, the deal was an immediate revenue-mix shift: post-completion, the share of group revenue earned outside Japan jumped materially, and the company’s exposure to the European logistics market went from peripheral to material in a single transaction.

The international segment is now the strategic centre of gravity

Read the company’s investor materials of the past three years and a single direction is visible. NX is reorganising itself around the proposition that international forwarding, plus contract logistics anchored to that forwarding, is the growth engine and the margin upgrade — and that the Japanese domestic business, while structurally large and cash-generative, is no longer the strategic centre of gravity.

Three things follow from that posture. The first is geographic expansion through acquisition. Cargo-partner in Europe was the headline transaction; alongside it, smaller bolt-ons in Vietnam, India, Southeast Asia, and the United States have filled in regional gaps. The second is portfolio rotation within Japan: divestments of non-core domestic businesses, particularly in real-estate-adjacent and security-related operations that no longer fit a freight-forwarding identity, have been used to fund the international build. The third is the deliberate decoupling of identity from the legacy Nippon Express brand. NX Holdings now positions itself externally — particularly to non-Japanese corporate customers — as a global logistics group that happens to be headquartered in Tokyo, rather than as a Japanese national champion that also does international business.

The competitive set is global, not Japanese

For investors trying to value NX Holdings, the most useful peer group is no longer Yamato, Sagawa, and Japan Post. It is DHL Global Forwarding, Kuehne+Nagel, DSV, DB Schenker, CEVA Logistics, and Expeditors International — the global forwarding majors. On most measures of air-freight tonnage and ocean-freight TEU handled annually, NX sits inside the global top ten, comfortably ahead of regional forwarders but a meaningful step behind DHL and Kuehne+Nagel at the top of the table. The gap is not a function of capability but of book size, and the M&A strategy of the past three years has been an explicit attempt to close it.

What NX brings to that peer group that the European-headquartered forwarders do not is the depth of its Japanese corporate relationships. Toyota, Honda, the trading houses, the major pharmaceutical and electronics manufacturers, and the semiconductor-equipment makers have long-standing forwarding contracts with Nippon Express that pre-date the current generation of logistics-team buyers at the customer companies. Those relationships are not unassailable — global forwarders compete hard for the Japanese multinational book — but they are stickier than the typical European or American account, and they give NX a defensible volume base out of Asia that the European majors have to fight for one tender at a time.

The reverse is also true. Inside Europe, NX is the challenger rather than the incumbent. Cargo-partner gives it a credible mid-tier position in central and eastern Europe, but in the largest European logistics markets — Germany, the UK, France — it is competing against home-market champions with longer customer histories and deeper local labour networks. Closing that gap is the next ten-year project, and is the principal reason analysts expect further mid-sized European acquisitions over the coming cycle.

Leadership and the holding-company governance shift

The holding-company restructure of January 2022 was implemented under the leadership of Mitsuru Saito, who became president and representative director of the newly created NX Holdings at that time and continues to lead the group. Saito’s tenure has been defined by the cargo-partner acquisition, the rebranding from Nippon Express Holdings to NX Holdings, and the parallel programme of domestic portfolio rotation. The corporate posture under his leadership is recognisably different from that of the pre-2022 Nippon Express — more outward-facing, more comfortable with cross-border M&A risk, and more willing to talk publicly about international forwarding revenue as the dominant strategic narrative rather than as a complement to the Japanese trucking core.

Board-level governance has shifted in parallel. The holding structure has made it cleaner to separate strategic capital-allocation decisions from operating execution; the regional sub-holdings (NX Europe, NX Americas, and so on) report into the parent with a degree of P&L visibility that did not exist under the unified Nippon Express structure. For foreign counterparties this matters less for governance theory than for practical procurement: when a European customer signs an NX contract today, the contracting entity, the legal jurisdiction, and the operating accountability all sit inside the regional sub-holding rather than being routed through Tokyo.

What this means for foreign partners and 3PL counterparties

For foreign companies evaluating Japanese logistics partners, NX Holdings occupies a different square on the board from Yamato. If the question is Japanese consumer parcel delivery — last-mile, perishable, subscription box, DTC — Yamato, Sagawa, and Japan Post are the relevant set. If the question is cross-border industrial freight, multimodal forwarding, contract logistics tied to a Japanese manufacturer’s supply chain, or heavy and oversized cargo, NX is the natural counterparty and is often the only Japanese-headquartered operator with both the domestic and the overseas footprint to execute end-to-end.

Three specific use-cases recur. The first is European exporters and importers using NX or cargo-partner for Asia-Europe air and sea freight, particularly where Japanese-quality customs and documentation matters at the Japan end. The second is American and European brand owners building Japanese fulfilment and contract logistics under multi-year service contracts, where NX competes with both global 3PLs and Japanese specialists like Mitsui-Soko and Yusen Logistics. The third is project cargo — power generation equipment, semiconductor fabrication tooling, factory relocations — where the heavy-haulage capability inherited from the long Nippon Express history and reinforced by the Franco Tosi acquisition gives NX a genuine technical edge.

The investor case sits alongside that operational story. A patient holder of NX Holdings is essentially betting on three things: that the international segment continues to outgrow the Japanese domestic segment; that cargo-partner integration delivers the revenue and margin synergies underwriting the 2022 deal; and that the next round of European and American bolt-on acquisitions can be financed without straining the balance sheet or diluting the existing equity base. The competitive set against which to benchmark progress is global, not Japanese, and the relevant peers — DHL, Kuehne+Nagel, DSV — set a high bar for forwarding margin and capital efficiency.

FAQ

What is the difference between NX Holdings and Nippon Express?

NX Holdings, Inc. is the listed pure-holding parent company, established in January 2022 in the corporate restructuring that also produced the NX brand. Nippon Express Co., Ltd. continues as the principal Japanese operating subsidiary, handling domestic Japanese freight, trucking, warehousing, and heavy haulage. The international business sits under regional sub-holdings — NX Europe, NX Americas, NX East Asia, NX South Asia & Oceania — that report into the same parent.

Why did Nippon Express rebrand as NX Holdings?

The January 2022 restructuring created a pure-holding parent and separated listed corporate governance from operating execution. The NX brand was chosen as an internationally legible identity that does not require non-Japanese customers to know the legacy Nippon Express name. The change was strategic as well as cosmetic — it made large cross-border acquisitions (notably cargo-partner) easier to bolt onto the group structure without disturbing the Japanese operating subsidiary.

What is cargo-partner and why was the acquisition important?

cargo-partner GmbH is an Austrian-headquartered international freight-forwarding group with strong Asia-Europe air and sea capability and a network concentrated in central, eastern, and southern Europe. Nippon Express Holdings completed the acquisition in April 2022 for approximately two billion euros — the largest cross-border deal in its history. The transaction gave NX a turnkey European platform, materially shifted the consolidated revenue mix toward non-Japanese sources, and positioned the group to compete with DHL, Kuehne+Nagel, and DSV on a more equal footing.

How large is NX Holdings’ overseas network?

Approximately 300-plus overseas offices and operating sites in roughly 50 countries, including the cargo-partner network. The group operates regional sub-holdings in Europe, the Americas, East Asia, and South Asia & Oceania, with the network biased toward Asia-Pacific and central Europe and a deliberate ongoing build-out in the United States and Western Europe.

Does NX Holdings compete with Yamato, Sagawa, or Japan Post?

Only at the edges. NX is built around international forwarding, contract logistics, heavy haulage, and Japanese B2B trucking — it does not run a consumer parcel network and does not compete in the Takkyubin or Yu-Pack segment. The four companies share the broad label of “Japanese logistics” but occupy different segments of the market and serve different customer bases.

Working with NX Holdings

NX Holdings is the natural counterparty for any organisation moving cross-border industrial freight to or from Japan, building Japanese contract logistics under a multi-year service contract, or executing project cargo and heavy-haulage operations across Asia and Europe. If you are evaluating Japanese forwarding partners for an Asia-Europe trade lane, scoping a Japanese 3PL build, or comparing NX with global integrators like DHL and Kuehne+Nagel on a specific corridor, Japonity can introduce qualified contacts inside the group and structure a market-fit conversation. Start with our business-matching service.

Related from Japonity — Japan’s logistics & forwarding

- Yamato Holdings — Japan’s parcel-delivery king — Kuroneko and the Amazon problem

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →