Tsuruha Holdings is, depending on the day and the metric, either the largest or the second-largest drugstore chain in Japan. By store count it operates roughly two thousand five hundred outlets nationwide across half a dozen banner brands; by revenue it has alternated with Welcia Holdings at the top of the league table for most of the past decade. Both facts are now being rewritten by a single corporate event. In 2024, Tsuruha and Welcia — the two largest Japanese drugstore groups, each majority-influenced by the Aeon group — announced plans to merge, in a transaction that, if completed as currently described, would create the largest drugstore operator in Asia by store count, with roughly five thousand three hundred outlets and combined revenue in the order of three trillion yen. Behind that announcement lies an unusual chain of events: a multi-year activist campaign by Oasis Management, the Hong Kong–based fund run by Seth Fischer, which between 2022 and 2024 pressed Tsuruha’s board to reform governance and pursue exactly the kind of consolidation that has now been agreed. For foreign cosmetics, over-the-counter pharmaceutical and food-and-beverage brands selling into Japan, the combined Tsuruha-plus-Welcia entity will become the single most important non-grocery retail channel in the country.

From a Hokkaido pharmacy to a national platform

Tsuruha’s official founding year is 1929, when Junichi Tsuruha opened Tsuruha Yakkyoku, a small pharmacy in Asahikawa, a regional centre in central Hokkaido. The shop traded through the depression, the Pacific War and the post-war reconstruction in the same family-pharmacy mode common across pre-modern Japan: a licensed pharmacist behind the counter, a narrow assortment of prescription and patent medicines, and customer relationships measured in decades. The shift from neighbourhood pharmacy to chain-store operator did not begin until the 1960s, when Junichi’s successors started opening additional outlets across Hokkaido. Hokkaido remained the strategic core: a sparsely populated, weather-defined market where one chain could plausibly serve every regional centre from Hakodate to Wakkanai before any national competitor took the trouble to follow.

The decisive expansion arrived in the late 1990s and 2000s, when Tsuruha pivoted from a Hokkaido regional chain to a national consolidator. The group moved into Tohoku, Kanto, the Tokai region and Kansai, partly through new store openings but increasingly through acquisitions of mid-sized regional drugstore operators. Tsuruha Holdings listed on the Tokyo Stock Exchange under code 3391. Kusuri No Aoki provided a foothold in Hokuriku; Bunbun Do anchored the chain’s presence in Kyushu; Lady Drug strengthened the Tokai-region footprint; the cosmetics-specialty banner Choshikatsu added a higher-margin urban format. Each acquired chain kept its local brand and store identity but migrated onto a common merchandising, supply-chain and information-systems platform — a federation model rather than a single national rebrand. The result, by the early 2020s, was a group of roughly two thousand five hundred stores under six or seven banner names, with Tsuruha Drug as the principal national flag.

Group headquarters remain in Sapporo, an unusual choice for a Japanese national retailer of this scale and a deliberate one. The Hokkaido base signals to investors and acquired regional operators that Tsuruha is not a Tokyo conglomerate buying up the provinces but a regional consolidator that grew outward from one. The chairmanship has remained with the founding family — Toru Tsuruha as chairman, with Jun Tsuruha holding senior operating responsibility — alongside a professionalised management team and an increasingly independent board.

The banner portfolio

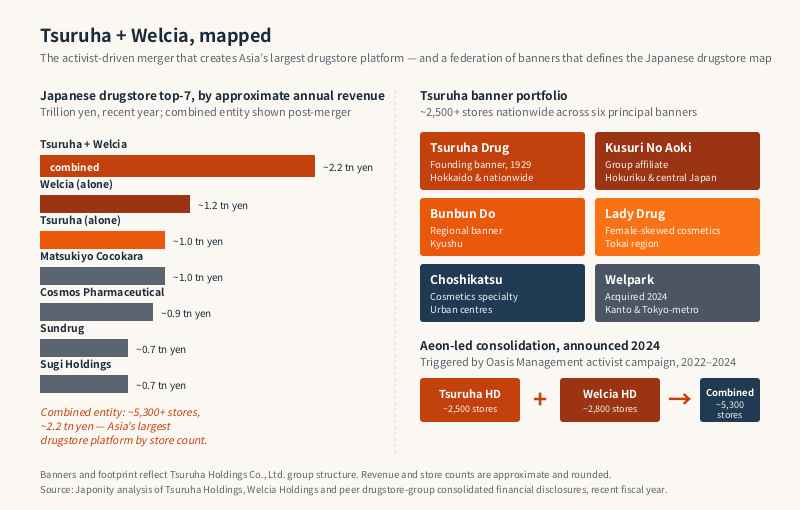

What makes Tsuruha harder to read than a single-brand chain is the federation of operating banners that sit beneath the holding company. Each banner has a defined geographic territory, a slightly different format mix and a distinct customer profile, and the group has been careful to preserve local brand equity rather than collapse everything into a Tsuruha flag.

| Banner | Acquired or established | Principal region | Format and customer focus |

|---|---|---|---|

| Tsuruha Drug | Founding banner, 1929 | Nationwide, anchored in Hokkaido and Tohoku | Standard drugstore with pharmacy, OTC, cosmetics and daily goods |

| Kusuri No Aoki | Group affiliate | Hokuriku and central Japan | Drugstore with strong fresh-food and household-goods mix |

| Bunbun Do | Group banner | Kyushu | Regional drugstore, daily essentials and pharmacy |

| Lady Drug | Group banner | Tokai region | Drugstore with female-skewed cosmetics assortment |

| Choshikatsu | Specialty format | Urban centres | Cosmetics-focused specialty store, narrower assortment |

| Welpark | Acquired 2024 | Kanto | Standard drugstore, strengthens Tokyo-metro coverage |

| Kusuri No Fukutaro and other regional banners | Various | Local pockets | Smaller regional operators retained under original names |

Three things follow from the structure. First, Tsuruha is not a single store concept replicated across the map; it is a portfolio of locally familiar names sitting on a shared supply chain. Second, the geographic footprint is genuinely national rather than concentrated around Tokyo and Osaka — Hokkaido and Tohoku, where competitors are thinner, anchor the chain’s defensible share. Third, the Welpark acquisition completed in 2024 was strategically aimed at exactly the gap Tsuruha had in Kanto, the largest and most contested drugstore market in Japan, where Welcia and Matsumoto Kiyoshi historically held the strongest hands.

The Japanese drugstore boom, and where Tsuruha sits in it

To understand why Tsuruha matters, foreign observers need a quick reframing of what a Japanese drugstore actually is. The category does not resemble Boots in the United Kingdom or CVS in the United States, both of which lead with pharmacy and personal care and treat food as ancillary. A modern Japanese drugstore is a hybrid daily-essentials channel. A typical store sells prescription pharmaceuticals at a counter staffed by a registered pharmacist, a deep assortment of OTC medicines, a serious cosmetics section with mid-market and prestige brands, household goods, baby and pet products, alcohol, snacks, frozen food and an increasingly competitive fresh-and-prepared-food shelf. Pricing is sharp, opening hours are long, and the loyalty programmes are mature.

The consequence is that drugstores have spent the past fifteen years quietly cannibalising market share from supermarkets, convenience stores and general-merchandise stores. The category now exceeds eight trillion yen in annual sales, growing through both inflation and category expansion even as the rest of Japanese retail flatlines. Foreign visitors notice the boom indirectly, through the inbound-tourism cosmetics rush at Matsumoto Kiyoshi or Don Quijote stores in Shinjuku and Dotonbori; domestically the more important story is the suburban drugstore that has become the default daily-essentials destination for an aging consumer who finds the supermarket aisle too long and the convenience store too expensive.

| Drugstore group | Approximate annual revenue | Approximate store count | Aeon group relationship |

|---|---|---|---|

| Welcia Holdings | ~1.2 tn yen | ~2,800 | Aeon consolidated subsidiary |

| Tsuruha Holdings | ~1.0 tn yen | ~2,500 | Aeon strategic stake |

| Cosmos Pharmaceutical | ~0.9 tn yen | ~1,400 | Independent |

| Sundrug | ~0.7 tn yen | ~1,400 | Independent |

| Matsukiyo Cocokara | ~1.0 tn yen | ~3,300 | Independent |

| Sugi Holdings | ~0.7 tn yen | ~1,600 | Independent |

| Genky DrugStores | ~0.2 tn yen | ~400 | Independent |

The combined Tsuruha-plus-Welcia entity, if the merger closes as currently described, would lead every meaningful metric — revenue around two-and-a-quarter trillion yen, store count above five thousand three hundred — by a margin large enough that the remaining independents will need to consider their own consolidation moves.

The Oasis Management activist campaign, 2022 to 2024

The proximate trigger for the Tsuruha-Welcia merger was an activist campaign by Oasis Management, the Hong Kong–headquartered fund run by Seth Fischer. Oasis began accumulating Tsuruha shares in 2022 and by 2023 had become one of the largest non-strategic holders, with a position reported in the high single digits as a percentage of outstanding shares. The fund’s public argument was a familiar mix of corporate-governance and capital-efficiency themes, applied to a chain that critics had long described as undermanaged relative to its scale.

Three specific demands recurred across Oasis’s letters, presentations and proxy materials. The first was board independence and the introduction of outside directors with genuine retail and capital-markets experience. The second was a sharpening of capital allocation — particularly a willingness to use the balance sheet for value-creating mergers and acquisitions rather than continuing organic growth at a Japanese pace. The third, and most consequential, was that Tsuruha should engage seriously with Aeon and Welcia on the question of a combination, on the argument that the drugstore industry’s fragmentation was a structural drag on margins and that the Aeon-Welcia-Tsuruha triangle was the obvious geometry for consolidation.

The Tsuruha board resisted at first and then negotiated. Through 2023 the company adjusted its board composition and engaged Aeon in more visible strategic dialogue. In early 2024 the Tsuruha and Welcia boards announced, in coordination with Aeon, plans for an integration through a share exchange and holding-company restructuring that would combine the two chains under a single listed parent. The announcement explicitly cited governance reform, supply-chain integration and the need to compete with the largest Asian retailers as drivers. By the standards of Japanese activism, the campaign is one of the cleaner success stories: a foreign fund identified a structural opportunity, pressured a founding-family chain through standard governance channels, and ultimately moved the strategic dial.

The Aeon angle

The corporate logic of the merger cannot be understood without Aeon. Aeon has been Welcia’s controlling shareholder for years, and has held a strategic stake in Tsuruha that has expanded through successive transactions, putting it in a position to influence and ultimately to facilitate a combination between the two. For Aeon, the strategic prize is straightforward. Drugstores are the fastest-growing daily-essentials format in Japan, and Aeon already owns the largest by store count. Owning a controlling interest in the merged Tsuruha-Welcia entity would consolidate the channel that has been quietly eating share from Aeon’s own general-merchandise and supermarket businesses, turning external disruption into internal cannibalisation. It would also give the Aeon group, taken as a whole, a credible claim to operate the largest drugstore platform in Asia at a moment when health-and-beauty retail is the most attractive sub-segment of the broader Asian retail landscape.

For Tsuruha and Welcia separately, the combination delivers synergies the chains have struggled to realise individually. Procurement scale across OTC, cosmetics and packaged-food categories will sharpen unit economics. A single private-label programme — drawing on Aeon’s Topvalu platform alongside the chains’ own labels — can spread development costs across more than five thousand stores. Logistics integration and store-level format rationalisation will reduce duplication. And digital and loyalty-programme integration with Aeon’s WAON e-money and Aeon Card stack will deepen customer-data assets that fragmented chains cannot easily build alone.

What the merger means for foreign brands

For foreign cosmetics, OTC pharmaceutical, packaged-food and household-goods brands selling into Japan, the post-merger Tsuruha-Welcia entity will become the single most important non-grocery retail customer in the country. The practical implications run in several directions.

Cosmetics will feel the change most immediately. The combined chain will drive volume for Korean, French, Italian, American and increasingly Southeast Asian beauty brands in Japan. Inbound-tourism stores in Tokyo, Osaka and Sapporo will become a single negotiating counterparty. The Choshikatsu specialty banner, focused on a higher-tier cosmetics customer, offers a different doorway from the standard drugstore floor. Listing into either the standard or specialty network will become a structurally bigger prize and a structurally harder negotiation.

Over-the-counter pharmaceuticals and health-and-wellness products will face a similar reconfiguration. Japanese drugstores already act as the primary channel for self-care categories in which European and American brands have struggled to crack the supermarket route. A single five-thousand-store buyer will streamline distribution for foreign self-care, vitamins and supplements brands but will concentrate decision-making in a way that rewards mature Japan-market capability and penalises those still treating Japan as a test market.

Packaged food, beverages and household goods will move next. The drugstore format has been quietly building its share in food, and the post-merger entity will sit alongside Aeon’s grocery operations as a serious channel for snacks, frozen food, soft drinks and household consumables. Foreign suppliers with credible Japanese-market unit economics — correct pack sizes, Japanese-language labelling and a domestic distribution partner — will find a far more concentrated buyer than the segment offered five years ago.

Governance, family legacy and what comes next

The Tsuruha story is unusual within the Japanese founding-family playbook because the family has retained chairmanship while accepting both foreign activist pressure and Aeon-led strategic integration. Toru Tsuruha’s chairmanship and Jun Tsuruha’s senior operating role anchor the founding-family thread, while the post-merger entity will involve a leadership structure shared with Welcia and coordinated with Aeon. Few large Japanese family chains have navigated this kind of three-cornered negotiation as openly. The Oasis campaign’s success is partly a function of how willing the family and the board ultimately were to accept governance reform rather than entrench against it.

Execution risk between announcement and closing remains real. Japanese consolidations of this scale routinely take eighteen to thirty months to integrate, and the combined entity will need to satisfy competition review, integrate two large logistics and IT estates, and rationalise overlapping store networks in Hokkaido, Tohoku and Kanto. Foreign brands should expect a transitional period of one to two years of conservative assortment decisions, followed by a strategic-realignment phase in which a meaningful share of category positions will be reset.

The longer-term arc is the more interesting question. A combined Tsuruha-Welcia entity under Aeon-group strategic influence will, almost by definition, be the most important Japanese platform for the consumer categories most exposed to inbound tourism, an aging domestic population and the slow Japanese embrace of imported consumer brands. For Japan-watchers, it is the single retail story most worth tracking through the rest of the decade.

FAQ

Is Tsuruha really larger than Welcia?

By store count, Tsuruha and Welcia have been roughly comparable in recent years, with Welcia typically reporting a slightly higher store count after recent acquisitions and Tsuruha reporting around two thousand five hundred outlets across its banner network. By revenue the two groups have alternated at the top of the league table from year to year, with Welcia frequently reported as the marginal leader and Tsuruha in close second. The Cosmos Pharmaceutical, Matsukiyo Cocokara and Sundrug groups follow at meaningful distance. The point of the merger is precisely that the top two have decided the duel is less valuable than the combination.

What did Oasis Management actually demand?

Oasis Management, the Hong Kong–based fund run by Seth Fischer, accumulated a meaningful Tsuruha position between 2022 and 2023 and pressed for three principal changes: stronger board independence with experienced outside directors, sharper capital allocation including a willingness to undertake transformative mergers and acquisitions, and serious strategic engagement with Aeon and Welcia on consolidation. The campaign was conducted through standard governance channels — shareholder letters, proxy proposals, investor presentations — and ultimately succeeded in moving the Tsuruha board towards the merger announced in 2024.

How does the Aeon group fit into the picture?

Aeon is Welcia’s controlling shareholder and holds a strategic stake in Tsuruha that grew through successive transactions, putting the Aeon group in a position to influence and ultimately to facilitate the merger between the two chains. For Aeon, the merged entity consolidates the Japanese drugstore segment, hedges against the format’s continuing share gains at the expense of Aeon’s own general-merchandise and supermarket businesses, and creates a platform that the Aeon group can claim, with some justification, to be the largest drugstore operator in Asia by store count.

What banners does Tsuruha operate today?

The principal banner is Tsuruha Drug, the original Hokkaido and Tohoku flag. Other banners include Kusuri No Aoki in Hokuriku and central Japan, Bunbun Do in Kyushu, Lady Drug in the Tokai region, the cosmetics-specialty banner Choshikatsu, and Welpark in Kanto following the 2024 acquisition. The group also retains a number of smaller regional banner names rather than rebranding every acquired chain to a single national flag. The federation approach preserves local customer equity while sharing supply-chain and merchandising infrastructure.

What does the post-merger entity mean for foreign brands?

A combined Tsuruha-and-Welcia entity will become the single most important non-grocery retail channel in Japan for cosmetics, over-the-counter pharmaceuticals, health-and-wellness products and a fast-growing food-and-beverage assortment. Foreign brands should expect a more concentrated negotiating counterparty, longer and more demanding listing processes, and disproportionately larger volume opportunities for those that secure shelf space. The transitional period between announcement and full integration will favour suppliers with mature Japan-market capability and disadvantage those still treating Japan as an exploratory market.

Working with Tsuruha

For overseas cosmetics, over-the-counter pharmaceutical, health-and-wellness, food and household-goods brands evaluating Japan-market entry or channel expansion, the post-merger Tsuruha-and-Welcia platform will define the route to the modern Japanese drugstore consumer for the rest of the decade. Japonity introduces qualified overseas companies to Japanese retailers, distributors and brand-development partners through its business matching service. If you are exploring a Japan listing, a private-label opportunity, a distribution partnership or a strategic relationship with one of the consolidating Japanese drugstore platforms, get in touch to start a conversation.

Related from Japonity — Japan’s drugstore chains

- Welcia Holdings — Japan’s biggest drugstore chain — and the impending Tsuruha merger

- Matsukiyo Cocokara — The tourist-favourite drugstore — Japan’s #3 after Welcia-Tsuruha

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →