Yamaha Motor Co., Ltd. is one of the world’s top three motorcycle makers by units, the dominant force in outboard marine engines with roughly 40 to 45 percent of the global market, and — surprising almost everyone outside the electronics manufacturing industry — a top-tier maker of surface-mount technology robots for assembling printed circuit boards. Outside Japan, the brand is still mostly conflated with the unrelated Yamaha Corporation, the piano and orchestral instrument maker from which it formally split in 1955. That conflation hides the second Hamamatsu engineering powerhouse, sitting alongside Honda in the same Shizuoka prefecture industrial belt, running a portfolio of land, water, air, and factory-floor businesses that no other transport company in the world matches.

Two Yamahas, one ancestor

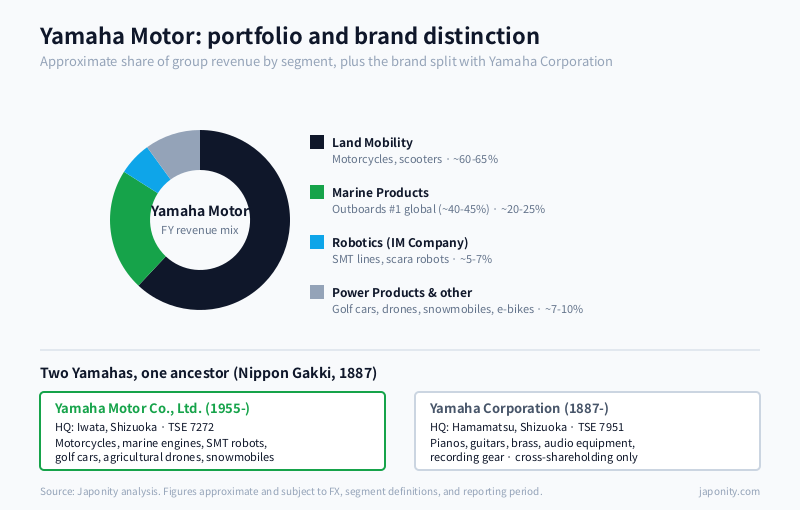

The brand confusion is a feature of the company’s origin story, not a bug. Yamaha Corporation, founded in 1887 as Nippon Gakki by Torakusu Yamaha, made organs, then pianos, then the full range of orchestral instruments. After the Second World War, Nippon Gakki had idle propeller-manufacturing capacity that had served wartime aircraft production. Genichi Kawakami, the fourth president of Nippon Gakki, decided in 1953 to repurpose it for motorcycles. The first Yamaha motorcycle, the YA-1 — a 125cc two-stroke single, nicknamed the Red Dragonfly — rolled off the line in 1955. The motorcycle operation was then spun off the same year as Yamaha Motor Co., Ltd., a separate legal entity from Nippon Gakki (renamed Yamaha Corporation in 1987).

The two Yamahas share the tuning-fork logo, the brand name, and a cross-shareholding relationship that persists to this day. They do not share management, factories, products, or strategic direction. Yamaha Motor is headquartered in Iwata, Shizuoka — a thirty-minute drive from Hamamatsu, where Honda and Suzuki also have deep roots — and reports separately to the Tokyo Stock Exchange under ticker 7272. For overseas partners, the practical implication is simple: if your interest is instruments or audio, you want Yamaha Corporation. If your interest is in any engine that moves a person, a boat, a circuit board, or a payload over a rice field, you want Yamaha Motor.

The Hamamatsu engineering cluster, explained

Hamamatsu is to Japanese engine engineering what Detroit was to American autos in the 1950s. Honda was founded there in 1948. Suzuki has been there since 1909, originally as a loom maker. Yamaha Motor’s Iwata headquarters sits twenty kilometres east, in the same prefectural manufacturing corridor. The three companies share a labour pool, a network of small precision-component suppliers, a culture of dynamometer testing and racing as product development, and a habit of recruiting from the same regional engineering universities.

What the cluster produces is a particular kind of company: founded after the war, focused on small to mid-displacement engines, and pushed almost from day one into export markets because the domestic post-war economy was too small to absorb the output. None of the three has a zaibatsu or keiretsu wrapper. None of the three has historically chased volume through merger. The result is three of the most independent and engineering-led publicly listed companies in Japan, all within a one-hour drive of each other.

The segment mix that hides the diversity

Yamaha Motor’s consolidated reporting groups its operations into four headline segments. The motorcycle business — what Yamaha calls the Land Mobility segment — dominates revenue. Marine products are the second-largest revenue line and, depending on the year, contribute a disproportionately large share of operating profit. Robotics, special-purpose vehicles, and other businesses round out the rest.

| Segment | Approx. share of group revenue | Representative products | Competitive position |

|---|---|---|---|

| Land Mobility (motorcycles, scooters) | ~60-65% | YZ, YZF-R, MT, Tracer, Tenere, NMAX, PCX-class commuters | #2 or #3 global by units (Honda #1) |

| Marine Products | ~20-25% | Outboard motors, WaveRunner PWC, sport boats | #1 global outboard, ~40-45% share |

| Robotics (IM Company) | ~5-7% | Surface-mount technology lines, scara robots, semiconductor handlers | Top 5 global in SMT |

| Power Products & other | ~7-10% | Golf cars, snowmobiles, ATV/SSV, agricultural drones, electric bicycles | Mixed — dominant in golf cars and snowmobiles |

Segment definitions and exact shares vary by year and FX, but the structural pattern is consistent. Two-thirds of revenue rides on motorcycles. One-fifth rides on outboards and personal watercraft. The remaining sliver is where the diversification story lives: an industrial-robotics business that almost no investor follows, a golf-cart business that dominates the global course market alongside Club Car and E-Z-GO, and an agricultural drone line that has quietly become the standard in Japanese rice production.

Motorcycles: a deliberate not-Honda strategy

Yamaha sells motorcycles in roughly 180 countries and ships in the neighbourhood of five to six million units a year, depending on the cycle. The geographic centre of gravity is identical to Honda’s — Indonesia, Vietnam, Thailand, the Philippines, India, Brazil — but the product mix and brand positioning are deliberately different. Where Honda’s emerging-market line-up is built around bulletproof commuter platforms (the Wave, the Dream, the Activa), Yamaha leans more heavily on sportier styling, performance halo, and the MotoGP-derived YZF-R lineage. The NMAX and Aerox sport scooters, the MT naked street range, and the Tracer adventure-touring family are Yamaha’s distinct calling cards.

The strategic logic is unit economics, not vanity. By positioning slightly above Honda in design and below the European premium marques in price, Yamaha targets the emerging-Asia customer moving up from a first commuter to a second, more aspirational bike. That customer pays more per unit, generates more in financing, and is stickier in after-sales parts. Yamaha will not catch Honda’s roughly 19 to 20 million units a year, and is unlikely to try. The ambition is to remain a clear and profitable number two or three, with a brand premium that compounds over the cycle.

The marine business: the quiet world champion

If there is one segment where Yamaha Motor is genuinely the global leader, it is outboard marine engines. The company holds roughly 40 to 45 percent of the global outboard market by units in recent years, ahead of Mercury Marine (the Brunswick subsidiary), Suzuki Marine, Honda Marine, and Tohatsu. In high-displacement outboards above 200 horsepower — the segment that powers offshore sport-fishing boats, twin and triple engine centre-consoles, and commercial vessels — Yamaha’s share is even higher in many markets, with the U.S. Gulf Coast and Florida fishing communities being particularly loyal.

The business is also the category leader in personal watercraft under the WaveRunner brand. Yamaha launched the first sit-down jet-ski-style watercraft in 1986, opening a category that Bombardier (Sea-Doo) and Kawasaki (Jet Ski) later expanded. WaveRunner remains the volume leader in many markets.

Why the marine business matters disproportionately to group profit comes down to three things. The outboard market is structurally consolidated — four or five global players, slow technology cycle. Marine engines run at much higher average selling prices than commuter motorcycles, with a single 425-horsepower V8 outboard retailing for the price of a small car. And the after-sales attach rate is high: engines need servicing, controls, propellers, and accessories, and dealers are loyal to a few brands. The result is a business that looks small in unit terms but punches well above its weight in margin.

The factory-floor business almost no investor knows

Yamaha Motor’s IM Company — IM stands for Intelligent Machinery — makes surface-mount technology machines for printed circuit board assembly. If you have ever wondered who built the line that placed the tiny resistors and capacitors onto the motherboard of your laptop, your smartphone, your car’s ECU, or your home appliance’s controller, the answer is one of a handful of companies. ASM Pacific Technology, Hanwha, Fuji, Panasonic, Juki, and Yamaha are the global leaders. Yamaha sits comfortably in the top five and is particularly strong in mid-volume electronics contract manufacturing in Asia.

The internal logic is engine-adjacent: Yamaha has historically been good at high-precision motion control, mass-produced mechanical assemblies, and rapid iteration. Those capabilities translated naturally from outboard cylinder honing and motorcycle lines into the scara robots and pick-and-place heads that run an SMT line. The business is not a major revenue contributor, but it is quietly profitable, B2B-only, and does not move with consumer cycles.

For overseas electronics manufacturers, Yamaha’s SMT line does not get the same airtime as ASM or Fuji in industry press, but it is widely used in Vietnam, Thailand, India, Mexico, and southern China contract manufacturing. The relationships are usually structured through Yamaha’s regional electronics-machinery distributors.

Niche dominance: golf cars, snowmobiles, drones

Yamaha’s smaller business lines, taken together, form a portfolio of category-defining niches. Yamaha Golf-Car has been one of the three global leaders in golf carts for decades, alongside Club Car (Ingersoll Rand) and E-Z-GO (Textron). The product has expanded beyond golf courses into low-speed neighbourhood vehicles, hospitality fleets at resorts, and industrial people-movers at large industrial sites. The U.S. market is the dominant geography, with Yamaha’s Newnan, Georgia plant serving as the production hub.

Snowmobiles are a category Yamaha entered in 1968 alongside Polaris, Bombardier (Ski-Doo), and Arctic Cat. Yamaha announced in 2024 that it would wind down its core snowmobile manufacturing while continuing parts and service. The exit signals a tightening of the portfolio around higher-margin segments.

Agricultural drones are the most recent and most interesting category. Yamaha’s RMAX unmanned helicopter, launched in the 1990s, became the standard for crop spraying in Japan’s rice paddies long before consumer drones existed. The current FAZER R and YMR-series multirotor drones extend the line into modern electric designs. In Japan, where small paddies and rapid ageing of the farmer population make manual labour scarce, the agricultural aviation business has more strategic optionality than its revenue share suggests.

Capital structure and the Toyota relationship

Yamaha Motor is listed on the Tokyo Stock Exchange under ticker 7272. The two largest historical shareholders are Toyota Motor Corporation and Yamaha Corporation (the musical instruments company), each holding roughly ten percent of outstanding shares in a long-standing cross-shareholding arrangement. The Toyota relationship is the older and stranger of the two: it dates to 1960s joint development of high-revving Toyota sports-car engines (including the legendary Toyota 2000GT, whose twin-cam head was developed by Yamaha) and has continued through periodic collaborations, most recently around V8 and V10 engines for Lexus.

Yoshihiro Hidaka took over as president and representative director in 2018 and has continued to lead the company through the post-pandemic rebound, EV transition planning for two-wheelers, and the portfolio rationalisation that included the snowmobile wind-down. Management is professional rather than founder-led; the Kawakami family is no longer in operational positions, though its influence on company culture is still visible in how Yamaha approaches new categories.

The electric two-wheeler question

The defining strategic question for the next five to ten years is the same one facing Honda, Suzuki, and every other established motorcycle maker: how does the company defend its position in emerging-market commuter two-wheelers as Chinese, Indian, and Taiwanese electric-scooter brands push aggressively into the same geographies?

Yamaha’s answer so far has been measured. The company has rolled out electric models in selected geographies, joined exploratory work on shared battery-swapping standards alongside Honda, KTM, and others, and continues to invest in its high-end internal-combustion line-up — particularly the YZF-R series and the MT naked range — for brand halo. The strategic risk is real: if Chinese electric two-wheelers achieve cost parity in Indonesia and Vietnam before Yamaha has a competitive platform, the #2 or #3 global position becomes structurally harder to defend. The opportunity is that marine, robotics, and golf-car businesses are not exposed to the same disruption curve.

The supplier and partner ecosystem

Yamaha Motor’s supplier base is regionally diversified across Japan, Indonesia, India, Vietnam, Thailand, Brazil, and the United States, reflecting the localisation of motorcycle and marine production. Domestic Tier-1 relationships span precision casting, forging, fuel-injection systems, and electronic control units. The company is more open to non-affiliated and overseas suppliers than the larger automakers, with engineering credibility as the primary qualification criterion rather than corporate-group membership. The relevant counterpart inside Yamaha is rarely Tokyo headquarters — it is usually the segment business unit, often at Iwata or the relevant overseas regional office.

Why Yamaha Motor warrants its own thesis

The simplest way to misread Yamaha Motor is to file it as a motorcycle maker with side businesses. The accurate read is closer to the Honda thesis: a portfolio of engine-platform businesses, each addressing a different geography and a different cycle, held together by a culture of mechanical engineering and incremental product iteration. The motorcycle business is the largest by revenue, but its profitability is volatile. The marine business is smaller but more durable. The robotics business is small but does not move with consumer cycles. The niche businesses — golf cars, agricultural drones, electric bicycles — are individually small but collectively meaningful, and several of them have category-leading positions that no investor narrative captures.

For overseas observers, the practical implication is to stop confusing Yamaha Motor with Yamaha Corporation. The two share a brand and a tuning-fork logo. They do not share a strategy, a balance sheet, or a destination. Yamaha Motor is the second engineering powerhouse of Hamamatsu, the global outboard champion, and the SMT-line maker most investors have never heard of. It deserves its own thesis.

FAQ

Is Yamaha Motor the same company as Yamaha pianos?

No. Yamaha Motor Co., Ltd. and Yamaha Corporation are two separate publicly listed companies that share a brand name, a logo (the three crossed tuning forks), and a cross-shareholding relationship. Yamaha Corporation, founded in 1887 as Nippon Gakki, makes musical instruments and audio equipment. Yamaha Motor was spun off from Nippon Gakki in 1955 to focus on motorcycles and now makes motorcycles, marine engines, industrial robots, golf cars, and agricultural drones. The two companies have independent management and report separately to the Tokyo Stock Exchange.

Why is Yamaha so dominant in outboard motors?

Yamaha holds roughly 40 to 45 percent of the global outboard motor market. The dominance reflects four decades of dealer-network investment in coastal communities worldwide, a particularly strong position in the high-horsepower segment used for sport fishing and commercial vessels, a slower technology cycle than consumer products that rewards incumbents with deep service infrastructure, and a structurally consolidated competitor set — Mercury, Suzuki, Honda, and Tohatsu being the main alternatives. Replacing an outboard motor brand requires retraining a local dealer base and rebuilding parts inventory, which creates high switching costs.

What is the relationship between Yamaha Motor and Toyota?

Toyota Motor Corporation owns approximately ten percent of Yamaha Motor’s outstanding shares, and Yamaha holds a smaller reciprocal stake in Toyota. The relationship dates to the 1960s, when Yamaha developed and built the twin-cam cylinder head for the Toyota 2000GT sports car. It has continued through periodic high-performance engine collaborations, including V8 and V10 engines for Lexus performance cars. The cross-shareholding is strategic rather than operational; the two companies do not share platforms in their main product lines.

What is Yamaha Motor’s IM Company and why does it matter?

The IM Company (Intelligent Machinery) is Yamaha Motor’s industrial robotics and surface-mount technology business. It makes pick-and-place machines and scara robots used in electronics manufacturing to assemble printed circuit boards. Yamaha is one of the top five global suppliers in this category, with particular strength in mid-volume Asian contract manufacturing. The business is small in revenue terms — mid-single-digit percentage of the group — but it is high-margin, B2B-only, and structurally insulated from consumer cycles, making it a quiet diversifier in the portfolio.

Is Yamaha exiting any of its businesses?

Yamaha announced in 2024 that it would wind down its core snowmobile manufacturing programs while continuing to support existing customers with parts and service. This is part of a wider portfolio rationalisation focused on higher-margin and higher-growth segments. Marine, motorcycles, golf cars, robotics, and agricultural drones remain core. The company has not signalled any intent to exit other businesses; if anything, the agricultural-drone and electric-bicycle lines are getting more investment, not less.

Working with Yamaha Motor

For overseas suppliers, technology partners, and licensors, Yamaha Motor’s diversified portfolio means engagement happens through the relevant business segment rather than corporate headquarters. Motorcycle drivetrain components, marine propulsion and fuel-injection systems, surface-mount technology partnerships, agricultural-drone sensors and propulsion, and golf-car battery and electric drivetrain components are all distinct procurement worlds, each with its own technical evaluation process and regional centre. Tier-1 qualification typically begins at Iwata, at the regional motorcycle production hubs in Indonesia, India, or Thailand, or at the U.S. Marine Group and Newnan golf-car facility.

Beyond direct Yamaha engagement, the broader Hamamatsu-Iwata engineering supplier cluster — shared in part with Honda and Suzuki — is itself a substantial market for foreign component, materials, and software suppliers. Precision-casting houses, fuel-injection specialists, electronics-control suppliers, and lightweight-materials makers in this corridor serve all three Hamamatsu engine companies and are typically more accessible than equivalents in the Toyota or Mitsubishi keiretsu networks.

If your company supplies components, systems, or technology relevant to motorcycles, outboard marine engines, surface-mount industrial robotics, agricultural drones, or low-speed electric vehicles — or if you are looking to license Japanese technology in any of these categories into your home market — Japonity’s business matching service can help structure a credible first conversation with the right counterpart inside Yamaha Motor or its supplier network.

Related from Japonity — Japan’s mobility — autos and Hamamatsu engineering

- Toyota Motor Corporation — Multi-pathway powertrain strategy from the world’s #1 automaker

- Honda Motor — The motorcycle giant the auto press forgot

- Suzuki Motor — India’s market king — Maruti Suzuki’s ~40%+ share

- Subaru Corporation — The boxer-engine niche player that built America

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →