Nissan Motor Co., Ltd. enters 2026 as the most structurally compromised of Japan’s three big automakers. Global production fell to approximately 3.1 million vehicles in fiscal 2024 — down from a 5.7 million peak in 2017 — operating margin has compressed to low single digits, and the company has spent the last twenty-four months attempting and abandoning three escape routes: a deeper Renault realignment, a Honda merger that collapsed in February 2025, and an aggressive restructuring plan that has put approximately 20,000 jobs and seven plants on the line. The Ghosn era ended in 2018; the Renault entanglement did not. For foreign suppliers, capital partners and licensors, the deal structure that still constrains every Nissan move is the first thing to understand.

How Nissan got here: the post-Ghosn unwinding

Carlos Ghosn was arrested at Haneda Airport on 19 November 2018, charged with under-reporting compensation and misuse of company assets. He was forced out as chairman within days, and in December 2019 he escaped Japan in a music-equipment case bound for Beirut — a sequence so cinematic it has obscured what it actually did to Nissan. Two decades of Ghosn-era integration with Renault, executed at speed under one centralising chief, were abruptly stranded without the political glue that held them together. The cross-shareholding, the joint platforms, the Common Module Family architecture, the shared procurement spine — all of it remained, but the trust did not.

The result was six years of slow, expensive disentanglement. Nissan replaced Hiroto Saikawa (who was himself forced out in 2019 over related compensation disclosures) with Makoto Uchida in December 2019. Uchida’s mandate was to stabilise. He largely failed. Operating profit collapsed during COVID-19, recovered briefly on the back of supply-constrained pricing in 2022–2023, then collapsed again as the US market normalised, Chinese EV competitors took share, and Nissan’s product pipeline aged. By late 2024, the board had concluded Uchida could not deliver the turnaround. He was replaced in April 2025 by Ivan Espinosa, a relatively young Mexican executive who had run Nissan’s product planning function — a deliberate signal that the company was looking for operational sharpness over diplomatic continuity.

The Renault deal: what was restructured in 2023, what remains

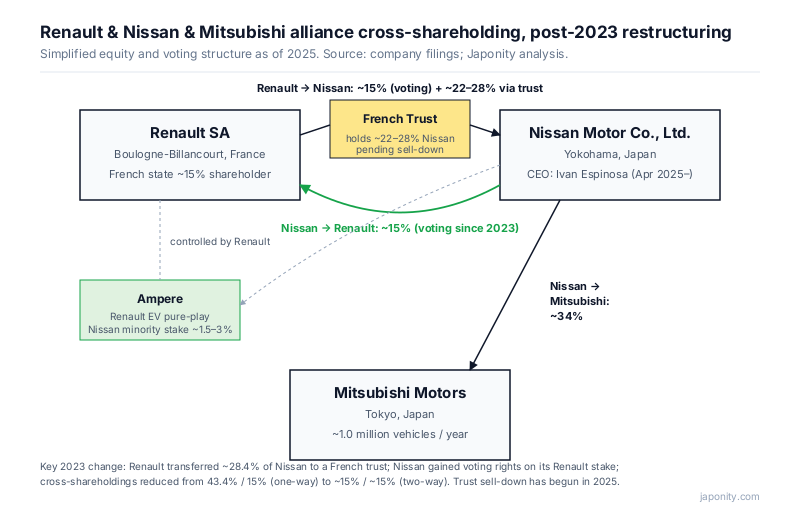

The single most important fact about Nissan is that it is not a fully independent company. The Renault–Nissan–Mitsubishi alliance, formed in 1999 when Renault rescued a then-bankrupt Nissan, has been the dominant constraint on Nissan’s strategic choices for a quarter-century. Until 2023, the structural asymmetry was acute: Renault held 43.4 per cent of Nissan with full voting rights; Nissan held 15 per cent of Renault with no voting rights. Ghosn used this imbalance to run both companies; his successors have spent six years trying to fix it.

The November 2023 restructuring was the formal correction. Renault transferred approximately 28.4 per cent of its Nissan shares into a French trust, to be sold down over time. Both parties now hold 15 per cent of each other with voting rights — formally equal, structurally still entangled. The trust mechanism is the key technical detail foreign investors miss: Renault has not given up the economic exposure, it has parked it pending an orderly sell-down. As of mid-2025, Renault has begun executing tranches of those sales, but the overhang on Nissan’s share price — and the strategic uncertainty about who eventually buys those shares — remains.

The post-2023 cross-shareholding structure looks deceptively clean on paper. In practice, Nissan and Renault still co-own Ampere (Renault’s EV pure-play), still operate joint platforms in B- and C-segment vehicles, and still share Alliance Operations functions in procurement, logistics and quality. Mitsubishi sits inside the alliance at 34 per cent owned by Nissan, contributing roughly 1 million vehicles a year and meaningful Southeast Asian distribution. For a supplier or licensor approaching “Nissan,” the practical question is which legal entity, which platform programme and which alliance governance body actually has decision rights — and the answer changes by programme.

| Entity / Stake | Held by | Approximate % | Voting rights |

|---|---|---|---|

| Nissan Motor Co., Ltd. | Renault SA (direct) | ~15% | Yes |

| Nissan Motor Co., Ltd. | Renault French trust (pending sell-down) | ~22–28% | Suspended / neutralised |

| Renault SA | Nissan Motor Co., Ltd. | ~15% | Yes (since 2023) |

| Mitsubishi Motors | Nissan Motor Co., Ltd. | ~34% | Yes |

| Ampere (Renault EV unit) | Nissan Motor Co., Ltd. (minority strategic stake) | ~1.5–3% | Yes |

Foreign acquirers occasionally float the idea that Nissan is “in play” because Renault is selling down. That misreads the situation. The Renault sell-down is being executed through a French-government-influenced trust, into a market with a managed pace and credible Japanese government interest in preserving Nissan’s domestic ownership profile. A clean foreign takeover of Nissan is not, at present, a plausible scenario — and the Honda merger episode of 2024–2025 explained why.

The Honda merger that wasn’t, December 2024 – February 2025

In December 2024, Honda and Nissan announced they had entered talks toward a holding-company merger, with Mitsubishi as a potential third participant. The combined entity would have been the world’s third-largest automaker by volume, with a stated goal of pooling EV and software development capacity to compete with BYD, Tesla and a consolidating Chinese sector. The strategic logic was real. The execution was not.

By early February 2025, the talks had collapsed. The proximate trigger was governance: Honda reportedly proposed converting the merger structure into one in which Nissan would become a Honda subsidiary, rather than an equal partner in a new holding company. Nissan’s board rejected the restructured terms. Both companies issued statements ending the merger discussions, though they retained a narrower technical co-operation framework on EV platforms and software.

The failure mattered for three reasons. First, it confirmed that Nissan’s board would not accept a subordinate position even in distress — a posture that constrains future restructuring options. Second, it left Nissan needing a standalone turnaround plan, which Espinosa was appointed to deliver. Third, it signalled to Foxconn, BYD and other industrial acquirers that the Japanese government and Nissan’s senior leadership view a foreign takeover or a domestic subordination differently, and neither was likely to clear quickly. Foxconn’s Jun Seki, a former Nissan executive, has continued to make exploratory noises through 2025; the Japanese policy response so far has been to make clear that any deal will have to satisfy METI and pass review under the Foreign Exchange and Foreign Trade Act.

The 2024–2026 restructuring plan: scale, plants, cost

In November 2024 Nissan announced an emergency restructuring plan: approximately 9,000 jobs cut globally, a 20 per cent reduction in global production capacity, and an explicit target of returning to operating profitability by fiscal 2026. By May 2025, under Espinosa, the plan was expanded: approximately 20,000 job reductions and seven plant closures globally, including reported closures or consolidations at facilities in Mexico, Argentina, India, South Africa and Thailand.

The Sunderland plant in the United Kingdom — Nissan’s largest European production base, employing approximately 6,000 people and producing the Qashqai, Juke and Leaf — has been confirmed as retained, with Nissan publicly committing to an EV-led future there as part of a broader UK industrial policy understanding. The Smyrna, Tennessee plant in the United States, Nissan’s largest North American facility, has also been confirmed as retained but with reduced shifts and a shifted product mix away from sedan production. Yokohama HQ remains the global centre of gravity, but its bargaining power inside the alliance has visibly compressed.

The US business is the most operationally consequential of these geographies. Nissan and Infiniti sales in the United States peaked in 2017 at approximately 1.59 million vehicles; by 2024 the combined figure had fallen below 940,000. The proximate causes are well documented inside the industry: an ageing product line-up, late entry into the most popular SUV and pickup segments, sustained quality and recall headlines, and a financing-led sales push during the late Ghosn era that left a depressed residual-value problem for which Nissan dealers are still paying. The 2025–2026 product refresh — a new Rogue, a redesigned Murano, the Ariya EV’s continued rollout and a forthcoming next-generation Leaf — is the operational bet.

The product reality: EVs, Infiniti and the China problem

Nissan’s claim on the EV future rests on the Leaf, which launched in 2010 and was, for several years, the best-selling battery EV in the world. The Leaf’s first-mover advantage was real, and it was substantially squandered. Tesla overtook it on premium positioning; BYD overtook it on cost; Hyundai-Kia overtook it on product cadence. The 2022 Ariya was Nissan’s attempt at a credible second-generation EV at a higher price point; reception has been mixed, with software, charging speed and pricing all cited as weaknesses against Tesla, Hyundai’s Ioniq 5/6 and the BYD Atto range.

Infiniti — Nissan’s premium brand, launched in 1989 in the United States — has been in structural decline for a decade. Volumes have fallen to under 60,000 vehicles annually in the US from peaks above 130,000, the brand has effectively withdrawn from Europe, and the product line consists of a small number of ageing SUVs and sedans. Industry analysts have repeatedly questioned whether Infiniti is viable as a standalone premium nameplate or whether Nissan should consolidate it. Espinosa’s 2025 commentary has signalled retention but with a narrowed product focus.

China is the third strategic problem. Nissan’s joint venture with Dongfeng was, until 2020, one of the company’s most reliable profit engines, with annual sales above 1.5 million vehicles. By 2024 the figure had fallen below 700,000. Chinese consumers have shifted aggressively to domestic NEV (new energy vehicle) brands — BYD, Geely, Li Auto, Nio, Xpeng — and Japanese brands have not adapted product, pricing or software fast enough. Nissan has announced accelerated localisation of new EV models in China, but the trajectory is decline-mitigation rather than recovery.

What foreign suppliers, investors and licensors need to understand

The structural constraints that bind Nissan create both risk and opportunity for overseas counterparties. Five practical points deserve attention.

- Alliance procurement still matters. A large share of Nissan’s parts procurement is run through Alliance Purchasing Organization, jointly with Renault. Tier-one suppliers selling into a Nissan platform are often, in practice, selling into a Renault-Nissan platform — pricing, quality and qualification standards are aligned. Approaching Nissan procurement without understanding the alliance dimension is a common new-entrant mistake.

- EV and software partnerships are the open lane. Nissan has been explicit that it needs external partners on battery cells, charging infrastructure, software-defined vehicle architecture and ADAS. The Honda technical co-operation framework that survived the merger collapse remains active. Foreign technology suppliers with credible IP and a willingness to localise engineering presence have access points that did not exist five years ago.

- Capital partnerships are governance-heavy. Any equity-level transaction with Nissan — joint ventures, strategic stakes, plant investments — will involve Japanese government touchpoints (METI, JBIC), alliance governance and a board that has demonstrated it will reject subordination terms. Foreign acquirers should expect 12–24 month timelines and structure expectations accordingly.

- The dealer and parts aftermarket is fragmented. Nissan’s US dealer network in particular is under stress, with consolidation and turnover at the dealer-group level. Aftermarket parts distributors, telematics partners and used-vehicle financing entrants have unusual openings in 2025–2026 as the network rebuilds.

- The yen is doing some of the work. At ¥150-plus to the dollar, Nissan’s domestic cost base is structurally underpriced to dollar-denominated counterparties. Component sourcing, R&D partnerships and licensing all benefit from the currency tailwind, which has materially widened the spread between Japanese and Korean or Chinese supplier pricing on like-for-like work.

2026–2030 outlook

The base case for Nissan over the next four years is a slow, contested standalone turnaround. Operating profit recovery to roughly 4 per cent margin by fiscal 2026 is the stated target; consensus analyst expectations sit modestly below that. The Renault sell-down will continue at a managed pace, the Honda technical framework will deepen on specific programmes without re-opening a merger, and the US business will stabilise on the back of the 2025–2026 product refresh rather than return to its 2017 peak. China will remain a managed decline. The Ariya, next-generation Leaf and a new family of EVs built on a software-defined vehicle architecture jointly developed with Honda are the credible upside cases.

The downside scenario — a renewed cash crunch, a forced governance change, a Foxconn or Chinese strategic approach that the Japanese government finds politically acceptable, or a Renault sell-down that destabilises the share price — remains live. Foreign counterparties signing multi-year contracts with Nissan in 2026 should price both scenarios into their commercial terms. That is the honest read of a company that is no longer the asset Ghosn inherited, but is not yet the asset Espinosa is trying to build.

FAQ

What is the current ownership structure of Nissan and Renault?

Following the November 2023 alliance restructuring, Renault holds approximately 15 per cent of Nissan with voting rights, with a further roughly 22–28 per cent of Nissan shares parked in a French trust for orderly sell-down. Nissan holds approximately 15 per cent of Renault with voting rights for the first time. Nissan also owns approximately 34 per cent of Mitsubishi Motors. The structure is formally more balanced than the pre-2023 asymmetry but the strategic entanglement remains substantial.

Why did the Honda–Nissan merger fail in February 2025?

The merger talks, announced in December 2024, collapsed when Honda reportedly proposed restructuring the transaction so that Nissan would become a Honda subsidiary rather than an equal participant in a new holding company. Nissan’s board rejected those revised terms. A narrower technical co-operation framework on EV platforms and software has been retained.

Who is the current CEO of Nissan?

Ivan Espinosa, who took over from Makoto Uchida in April 2025. Espinosa previously ran Nissan’s product planning function and was appointed as a deliberate signal that the company was prioritising operational and product execution over diplomatic continuity with the alliance.

How large is Nissan’s planned restructuring?

Under the expanded May 2025 plan, Nissan has targeted approximately 20,000 global job reductions and seven plant closures or consolidations across markets including Mexico, Argentina, India, South Africa and Thailand. The Sunderland (UK) and Smyrna (Tennessee) plants have been retained, with reduced shifts and shifted product mix at the latter.

What is happening to Carlos Ghosn?

Ghosn remains in Lebanon, where he fled in December 2019. He is the subject of an active Interpol Red Notice issued by Japan, and Japanese authorities have continued to pursue extradition, which Lebanon has declined to grant. The original criminal case against him in Japan remains formally open. Nissan reached a US Securities and Exchange Commission settlement related to disclosure failures in 2019 and pursued related civil claims against Ghosn in multiple jurisdictions.

Working with Nissan and its supply ecosystem

If your firm is evaluating a supplier qualification with Nissan or the Alliance Purchasing Organization, an EV or software partnership with Nissan’s R&D function, a capital-level transaction, or a regional distribution and aftermarket opportunity, Japonity’s editorial and business-matching teams introduce qualified overseas counterparties to vetted Japanese partners, including OEMs, tier-one suppliers and government-adjacent industrial bodies. Contact our business-matching desk to begin.

Related from Japonity — Japan’s automakers

- Toyota Motor Corporation — Multi-pathway powertrain strategy from the world’s #1 automaker

- Honda Motor — The motorcycle giant the auto press forgot

- Mazda Motor Corporation — The Hiroshima underdog that bet on internal combustion

- Subaru Corporation — The boxer-engine niche player that built America

- Suzuki Motor — India’s market king — Maruti Suzuki’s ~40%+ share

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →