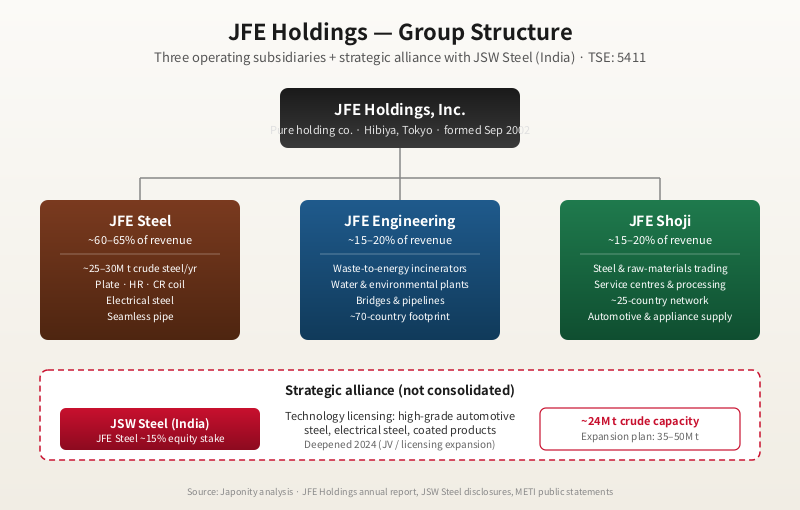

Steel is one of the industries where Japan still matters disproportionately to the global economy, and within Japan the contest is essentially a duopoly. Nippon Steel is the larger half of that duopoly and dominates the international press — its long pursuit of US Steel has done more than any other recent event to put a Japanese steelmaker on Western front pages. The other half is JFE Holdings, formed in September 2002 by the merger of NKK Corporation (Nippon Kokan, founded 1912) and Kawasaki Steel (spun off from Kawasaki Heavy Industries in 1950), headquartered in Tokyo’s Hibiya district and listed on the Tokyo Stock Exchange under code 5411. JFE produces approximately 25–30 million tonnes of crude steel a year — clearly Japan’s number two — but the more interesting story is what sits next to the steel mill: JFE Engineering, an environmental and infrastructure contractor with reference projects in roughly seventy countries; JFE Shoji, a globally connected trading arm; and, since 2024, a deepened strategic alliance with India’s JSW Steel that gives JFE direct exposure to one of the few large steel markets still growing structurally. Sitting over all of it is a decarbonisation question — direct-reduced iron (DRI) using hydrogen, fed into electric arc furnaces (EAF) — that will determine whether JFE’s blast-furnace base is an asset or a stranded liability by the 2040s.

Two postwar mills, one 2002 merger

To understand JFE Holdings, it helps to understand that the company is essentially the union of the two largest Japanese steelmakers that were not part of the Nippon Steel lineage. NKK — Nippon Kokan Kabushiki Kaisha — was founded in 1912 in Kawasaki, became Japan’s first integrated private steelmaker focused on tubular and plate products, and through the postwar decades built out the Keihin and Fukuyama works into globally competitive sites. Kawasaki Steel was spun off from Kawasaki Heavy Industries in 1950 as part of the Occupation-era restructuring of Japan’s heavy industry, and went on to build the Chiba East and Mizushima works into reference-grade integrated mills.

By the late 1990s, with East Asian capacity expanding rapidly and Korean and Chinese rivals investing in larger-frame blast furnaces, both companies concluded that consolidation was the only path to remain globally competitive. The merger was completed in September 2002, creating JFE Holdings as a pure holding company over JFE Steel, JFE Engineering and the predecessor of JFE Shoji. The “JFE” brand is typically read as “Japan Future Engineering”.

The structural logic of the merger has aged reasonably well. Nippon Steel and JFE Holdings between them account for roughly two-thirds of Japanese crude-steel output, and the duopoly has kept domestic pricing rational through a difficult two decades. Where the merger has been less obviously successful is international ambition: neither JFE Steel nor the wider group has built a footprint outside Japan comparable to ArcelorMittal’s, Nippon Steel’s US Steel push, or POSCO’s Indian and Indonesian capacity additions. The JSW alliance is the most explicit attempt to close that gap.

Segment portfolio: how the holding company is actually structured

JFE Holdings reports through three principal operating segments — Steel, Engineering and Trading — plus a small “other” line. The shape of the portfolio is unusual for an Asian steel group: most of JFE’s domestic peers either spun off their engineering and trading arms decades ago or kept them subordinated to the steel mill. JFE Engineering and JFE Shoji are, by contrast, genuinely standalone operating companies with their own brand presence overseas.

| Segment | Operating subsidiary | Approximate revenue share | Representative business |

|---|---|---|---|

| Steel | JFE Steel Corporation | ~60–65% | Integrated steel production (~25–30M tonnes crude), plate, hot & cold rolled, electrical steel, seamless pipe |

| Engineering | JFE Engineering Corporation | ~15–20% | Waste-to-energy incinerators, water and environmental plants, bridges, pipelines, offshore wind foundations |

| Trading | JFE Shoji Corporation | ~15–20% | Steel and raw-materials trading, processing, distribution in Japan and ~25 countries |

| Other / Corporate | JFE Techno-Research, others | ~2–3% | Materials testing, IT services, technical consulting |

JFE Steel is the centre of mass — the segment that drives consolidated earnings volatility and absorbs the bulk of decarbonisation capex. Its operating base is a small number of very large integrated works: East Japan Works (Chiba and Keihin sites, with Keihin in the process of significant blast-furnace closure and reshaping) and West Japan Works (Kurashiki, Mizushima and Fukuyama sites). JFE Steel produces the full integrated-mill product range — plate, hot-rolled coil, cold-rolled coil, surface-treated sheets, electrical steel for transformers and motors, seamless pipe for energy infrastructure, and rail and structural sections — and has historically held particularly strong global positions in high-grade electrical steel and large-diameter line pipe.

JFE Engineering: the under-the-radar global infrastructure arm

If the steel business is what JFE’s investors watch quarter to quarter, JFE Engineering is the segment most likely to surprise foreign visitors. The subsidiary traces back to NKK’s engineering division and is one of Japan’s largest dedicated environmental and infrastructure contractors. It builds waste-to-energy incinerators — Japan is one of the world’s largest markets for municipal-solid-waste incineration, since landfill is geographically impractical — and has exported that technology aggressively, with reference plants across South-East Asia, the Middle East, Europe and Africa. JFE Engineering’s own materials describe a footprint extending across roughly seventy countries.

Beyond incineration, the business covers water and wastewater treatment plants, gas and oil pipelines, steel bridges (it built or co-built several of Japan’s signature long-span bridges, including segments of the Akashi Kaikyō and the Trans-Tokyo Bay highway), offshore wind monopile and jacket foundations, and steel-frame stadium and arena structures. For European and Middle-Eastern municipalities considering Japanese waste-to-energy reference designs, or for offshore-wind developers in Asian waters sourcing certified foundation steel, JFE Engineering is one of a small number of Japanese counterparties capable of taking responsibility for full EPC delivery.

From a group strategy standpoint, JFE Engineering functions as a partial hedge against the steel cycle. Engineering revenue is project-driven and long-cycle, with margins less correlated with iron-ore and coking-coal prices. In years when steel earnings are compressed by raw-material spikes, the engineering project backlog has historically smoothed consolidated profit.

JFE Shoji: the trading arm with a longer reach than the mill

JFE Shoji, the group’s trading arm, is structurally similar to the steel-affiliated trading houses inside Nippon Steel (Nippon Steel Trading) and Kobe Steel (Shinsho), but with notably wider international processing capacity. JFE Shoji operates steel-service centres and processing facilities across roughly 25 countries, primarily in Asia and North America, where it cuts, slits and pre-processes JFE Steel coil and plate for automotive, electrical-appliance and construction-grade end-users. For Japanese automakers manufacturing in Thailand, Indonesia, Mexico and the southern United States, JFE Shoji is one of the two principal Japanese-origin steel-supply channels, alongside Nippon Steel’s affiliated network.

The strategic value of the trading arm is twofold. It gives JFE Steel direct visibility into demand patterns in markets where the group does not own primary capacity, and it provides a vehicle to participate in growth markets such as India, South-East Asia and Mexico without committing to greenfield blast-furnace investment — which has become economically and politically harder to justify under a decarbonisation lens.

JFE vs Nippon Steel: a structural comparison

Foreign analysts and partners frequently ask how JFE Holdings differs from Nippon Steel beyond raw scale. The honest answer is that the two companies pursue similar product portfolios but with materially different strategic emphasis.

| Dimension | JFE Holdings | Nippon Steel |

|---|---|---|

| Crude steel output (Japan-based) | ~25–30M tonnes/yr | ~40M+ tonnes/yr (Japan); higher group total incl. overseas |

| Founding / formation | 2002 (NKK + Kawasaki Steel merger) | 2012 (Nippon Steel + Sumitomo Metal merger); lineage to 1934 Japan Iron & Steel |

| Overseas integrated capacity | Limited; primarily via JSW Steel strategic alliance (India) | Substantial; AM/NS India JV, Brazil, Thailand, pending US Steel acquisition |

| Engineering / infrastructure subsidiary | JFE Engineering — major standalone business (~15–20% of group revenue) | No equivalent at comparable scale |

| Trading arm | JFE Shoji — ~25 countries, large standalone footprint | Nippon Steel Trading — meaningful but more steel-tied |

| Decarbonisation pathway emphasis | Hydrogen DRI + EAF + carbon capture pilots | Hydrogen DRI (“Super COURSE50”), hydrogen blast furnace, EAF |

| Tokyo Stock Exchange code | 5411 | 5401 |

The cleanest reading: Nippon Steel has chosen scale and global vertical integration, while JFE has chosen a more diversified holding-company structure with a meaningful non-steel earnings stream and selective overseas exposure through alliance rather than ownership. Neither approach is obviously superior; they reflect different judgements about where the global steel industry is heading and how Japanese companies should position within it.

The JSW Steel alliance: India as the missing growth engine

JFE’s most consequential international move of the past decade was the deepening of its alliance with JSW Steel of India. JFE first took an equity stake in JSW in 2010 — approximately 15 percent — and signed a series of technology-transfer agreements covering high-grade automotive steel, electrical steel and coated-product technology. JSW Steel is part of the Jindal-family-controlled JSW Group, one of India’s largest industrial conglomerates, and is itself one of the world’s larger steelmakers, with crude-steel capacity of roughly 24 million tonnes and announced expansion plans toward 35–50 million tonnes over the coming decade.

India is the strategically interesting market because it is one of the few major economies where steel demand is structurally growing rather than plateauing or contracting. Urbanisation, infrastructure build-out, automotive manufacturing growth, and the absence of the demographic and decarbonisation drags that constrain Japanese, Korean and European demand combine to support continued capacity expansion. For JFE, the JSW alliance is a way of participating in that growth without either deploying capital into a difficult greenfield Indian build or absorbing the regulatory and labour-relations complexity of full ownership.

In 2024 the alliance was further deepened through joint-venture and technology-licensing arrangements covering electrical steel and other downstream product lines, structured to support the growing Indian electric-vehicle and grid-equipment supply chain. For foreign partners that source steel products from India for downstream conversion, the JFE-JSW alliance is increasingly relevant: high-grade electrical steel and automotive-grade coil produced in JSW facilities under JFE technology licences are becoming more available in Indian markets, with corresponding implications for global supply allocation.

The hydrogen DRI question

The biggest open strategic question for JFE Holdings — and for Japanese integrated steel more broadly — is the decarbonisation pathway. Roughly 70 percent of Japanese crude steel is produced via the integrated blast-furnace / basic-oxygen-furnace (BF/BOF) route, which uses coking coal as both reductant and energy source and is among the most carbon-intensive industrial processes in the economy. Japanese steel accounts for approximately 14 percent of national CO₂ emissions; JFE Steel alone is one of the country’s larger single emitters.

The roadmap on which JFE and Nippon Steel have publicly converged combines three technology levers. First, hydrogen direct-reduced iron (DRI) — using hydrogen instead of coke to reduce iron ore in a shaft furnace, producing solid sponge iron that is then melted in an electric arc furnace. The chemistry is well understood at small scale; the engineering challenge is scaling to commercial mill volumes and securing low-cost green or blue hydrogen. Second, the electric arc furnace (EAF) route, which can melt scrap and DRI together at materially lower CO₂ intensity than a blast furnace. Third, carbon capture, utilisation and storage (CCUS) applied to remaining blast-furnace operations as a bridging measure.

JFE Steel has announced pilot and demonstration projects across all three pathways. The company’s medium-term decarbonisation plan targets meaningful CO₂-reduction milestones through the 2030s with a longer-horizon ambition of near-carbon-neutrality by 2050, broadly consistent with the Japanese government’s “Green Transformation” (GX) policy framework and the GX League industrial pact. Public NEDO and METI funding for hydrogen DRI development has been allocated to support pilot work at JFE Steel sites, alongside parallel programmes at Nippon Steel. The Keihin works restructuring — including the planned closure of one of the site’s blast furnaces — is part of how JFE is rationalising capacity ahead of the transition.

The honest read on timing: hydrogen DRI at commercial scale is unlikely before the early-to-mid 2030s, and the economics depend critically on the cost of low-carbon hydrogen, which remains higher than coking coal per tonne of iron. The transition will require sustained government support, customer willingness to pay green-steel premiums, and probably some form of carbon-border adjustment or domestic carbon pricing. European automakers under EU carbon-border-adjustment-mechanism (CBAM) pressure, and global appliance and electrical-equipment OEMs with scope-3 targets, are increasingly relevant counterparties — their willingness to pay for verified low-carbon Japanese steel will partly determine the pace of rollout.

Leadership, governance and what to watch

JFE Holdings is led by a holding-company executive team with operating presidents at each of JFE Steel, JFE Engineering and JFE Shoji. The group has rotated leadership through the steel side historically, with significant board attention to capital allocation between the steel decarbonisation programme and the engineering and trading arms. As with most Japanese listed companies, governance has shifted in recent years toward a higher proportion of independent directors and clearer disclosure on capital efficiency and decarbonisation targets.

For foreign partners, three threads are worth watching closely over the next 24 months. First, the pace and scale of the JSW Steel alliance expansion — particularly any movement on joint downstream investments in India or third-country exports of JSW-produced JFE-technology steel. Second, the trajectory of hydrogen DRI pilot work, both at JFE Steel sites and through international collaboration; this will signal whether Japanese integrated steel can credibly transition or whether scrap-and-EAF will dominate by default. Third, JFE Engineering’s offshore-wind and waste-to-energy backlog, which is a clean read on Japan’s renewable-infrastructure build-out and on JFE’s ability to compete with Korean and European EPC contractors in third-country markets.

FAQ

What is JFE Holdings and how did it form?

JFE Holdings is Japan’s second-largest steel group, formed in September 2002 by the merger of NKK Corporation (Nippon Kokan, founded 1912) and Kawasaki Steel (spun off from Kawasaki Heavy Industries in 1950). It is a pure holding company over three principal operating subsidiaries: JFE Steel (integrated steel production, approximately 25–30 million tonnes of crude steel per year), JFE Engineering (environmental plants, bridges and infrastructure EPC), and JFE Shoji (steel and raw-materials trading). The group is headquartered in Tokyo’s Hibiya district and is listed on the Tokyo Stock Exchange under code 5411. The “JFE” brand is typically read as “Japan Future Engineering”.

How does JFE compare to Nippon Steel?

Nippon Steel is larger — approximately 40 million tonnes of Japan-based crude-steel output versus JFE’s ~25–30 million — and has pursued aggressive international vertical integration through its AM/NS India joint venture, Brazilian and Thai operations, and pending US Steel acquisition. JFE has pursued a more diversified holding-company structure with meaningful non-steel earnings through JFE Engineering and JFE Shoji, and has approached international growth primarily through strategic alliance, particularly with India’s JSW Steel, rather than direct ownership. Both companies are pursuing hydrogen direct-reduced-iron and electric-arc-furnace decarbonisation pathways with broadly similar 2050 net-zero ambitions.

What is JFE Engineering, and what does it actually build?

JFE Engineering Corporation is JFE Holdings’ environmental and infrastructure EPC subsidiary. Its core businesses are waste-to-energy incinerators (Japan is one of the world’s largest markets for municipal-solid-waste incineration, since geography makes landfill impractical), water and wastewater treatment plants, gas and oil pipelines, steel bridges (including segments of major Japanese long-span bridges), offshore-wind monopile and jacket foundations, and steel-frame stadium and arena structures. Its overseas footprint extends across roughly seventy countries, primarily through incinerator and environmental-plant exports. The business generates approximately 15–20 percent of group revenue and is a meaningful diversifier against steel-cycle volatility.

What is the JFE-JSW Steel alliance, and why does India matter?

JFE Steel took an approximately 15 percent equity stake in India’s JSW Steel in 2010 and signed technology-transfer agreements covering high-grade automotive steel, electrical steel and coated products. The alliance was further deepened in 2024 through additional joint-venture and licensing arrangements. JSW Steel is part of the Jindal-family JSW Group and has approximately 24 million tonnes of crude-steel capacity with announced expansion plans toward 35–50 million tonnes. India matters strategically because it is one of the few major economies where steel demand is structurally growing; the alliance gives JFE exposure to that growth without committing to greenfield Indian capacity investment.

How is JFE approaching decarbonisation?

JFE Steel is pursuing the same broad technology pathway as Nippon Steel and most other integrated steelmakers: hydrogen direct-reduced iron (DRI) using hydrogen instead of coke in a shaft furnace, fed into electric arc furnaces (EAF); selective expansion of scrap-based EAF capacity; and carbon capture, utilisation and storage (CCUS) on remaining blast-furnace operations as a bridging measure. Pilot and demonstration projects are underway, with NEDO and METI funding support under Japan’s Green Transformation (GX) framework. Commercial-scale hydrogen DRI is unlikely before the early-to-mid 2030s. The economic viability depends on the cost of low-carbon hydrogen and customer willingness to pay green-steel premiums — relevant to European automakers under CBAM pressure and to global appliance and electrical-equipment OEMs with scope-3 targets.

Working with JFE Holdings

For automakers and appliance OEMs sourcing high-grade Japanese steel, electrical-equipment manufacturers procuring grain-oriented electrical steel for transformers, municipalities and EPC partners evaluating waste-to-energy or offshore-wind foundation contracts, or Indian and South-East Asian processors interacting with JSW-JFE technology-licensed product, JFE Holdings sits across a uniquely broad slice of Japan’s industrial capacity — only some of which is obvious from the headline steel-tonnage number. Japonity’s business matching service helps foreign organisations identify the right JFE operating subsidiary (Steel, Engineering or Shoji), navigate METI and NEDO programmes for joint decarbonisation projects, and structure introductions through appropriate Japanese commercial and trading-house channels. Contact us via the business matching page to begin a structured engagement.

Related from Japonity — Japan’s heavy industry & materials

- Mitsubishi Heavy Industries — Japan’s defence renaissance has a prime contractor

- DMG Mori — The Japan-Germany machine-tool union that quietly became #2 globally

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →