From a converted cork factory on the western edge of Hiroshima, Mazda Motor Corporation has spent a century carving out the most idiosyncratic position in the Japanese auto industry. With annual revenue of approximately ¥5.0 trillion, fewer than 50,000 employees, and a global vehicle output that rarely exceeds 1.3 million units, it sits well outside the volume tier occupied by Toyota, Honda and Nissan. Yet Mazda has done something none of them have managed: it has pushed average transaction prices into near-premium territory in the United States, kept the internal combustion engine at the centre of its R&D roadmap, brought the Wankel rotary back from the dead as a range extender, and persuaded Toyota to take a quiet 5 percent stake and co-build a plant in Alabama. For a company headquartered in Fuchu-cho, a town of 50,000 people that most foreign visitors have never heard of, the strategic ambition is unusually contrarian.

A Hiroshima company that refused to leave Hiroshima

Mazda was founded in January 1920 as Toyo Cork Kogyo, a manufacturer of cork substitutes for a country cut off from European supply during the First World War. The pivot to vehicles came in the early 1930s under Jujiro Matsuda, whose surname — rendered into a Romanised approximation of the Zoroastrian deity Ahura Mazda — eventually became the corporate brand. The company’s first three-wheel truck rolled out of Hiroshima in 1931.

The defining moment of Mazda’s twentieth century came on 6 August 1945. The atomic bomb destroyed roughly 70 percent of central Hiroshima, but the Toyo Kogyo headquarters in Fuchu-cho, about five kilometres from the hypocentre, survived structurally intact. Within weeks the surviving factory was producing trucks again, and the company became one of the early industrial anchors of the city’s reconstruction. That history is not incidental: Mazda still pays Hiroshima Toyo Carp baseball club’s stadium naming rights, employs a disproportionate share of the prefecture’s manufacturing workforce, and remains the only major Japanese automaker whose headquarters has never moved to Tokyo or Nagoya.

The cultural consequence runs deeper than civic loyalty. Mazda engineers tend to spend entire careers inside the company, often inside the same Hiroshima campus. Cross-pollination with Toyota City or the Tokyo-Yokohama corridor is comparatively rare. The result is an engineering monoculture that critics have sometimes called insular but that supporters credit with the brand’s unusual coherence: Mazdas drive like Mazdas, look like Mazdas, and sound like Mazdas in a way that more globally distributed peers find harder to replicate.

The rotary: an engineering bet that defined the brand

In 1961, then-president Tsuneji Matsuda licensed the Wankel rotary engine from NSU of Germany, a technology that almost every other licensee — including Mercedes-Benz, Citroën and General Motors — eventually abandoned. Mazda persisted. The 1967 Cosmo Sport was the first twin-rotor production car in the world. Over the next four decades, the rotary defined Mazda’s identity through the RX-7 (1978-2002) and RX-8 (2003-2012): small, light, high-revving engines that delivered sports-car performance from a compact package.

The rotary also nearly killed the company. The 1973 oil shock exposed the engine’s poor fuel economy, sales collapsed, and Mazda was rescued by Sumitomo Bank in a restructuring that imposed years of conservative management. The RX-8 was finally withdrawn in 2012 on emissions grounds, and for eleven years the rotary disappeared from showrooms entirely. Then in 2023, Mazda reintroduced it — not as a sports-car powerplant but as a 830cc single-rotor range extender for the MX-30 R-EV, a plug-in hybrid crossover sold primarily in Europe. It is a characteristic Mazda move: keeping a heritage technology alive by re-tasking it for a use case that no one else thought to pursue.

SkyActiv: the contrarian engine roadmap

While most Japanese rivals shifted their R&D spend toward hybrids in the 2000s and battery EVs in the 2010s, Mazda made a deliberate counter-bet on the internal combustion engine. The SkyActiv programme, launched in 2011 under then-CEO Takashi Yamanouchi and powertrain chief Mitsuo Hitomi, aimed to wring efficiency gains out of conventional petrol and diesel architectures that rivals had written off as a dead end.

The most ambitious output of that programme was SkyActiv-X, introduced in 2019. It is the world’s first commercial petrol engine to use spark-controlled compression ignition (SPCCI), running with a diesel-like lean mixture under most operating conditions and reverting to conventional spark ignition only when needed. The engineering achievement is real, but commercial uptake has been muted; the technology arrived just as European regulators were pulling forward EV mandates, and Mazda found itself defending a powertrain philosophy that the broader industry had moved past. The company has since reframed SkyActiv as part of a “multi-solution” strategy that runs efficient combustion engines alongside hybrids and a forthcoming dedicated EV platform expected around 2027-2028.

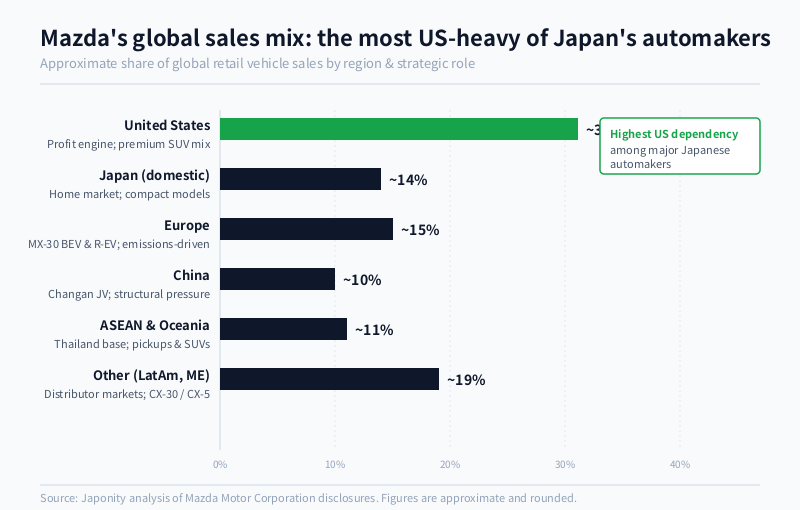

The unusual US-heavy sales mix

Mazda’s geographic distribution is the most American-tilted of any major Japanese automaker. Roughly 30-32 percent of its global retail volume goes to a single country: the United States. Toyota’s US share of its global sales is closer to 25 percent; Honda’s is in a similar range; Nissan’s is lower. The asymmetry is partly a legacy of the Ford era (1979-2008), when Ford built a 33 percent controlling stake in Mazda and integrated the company deeply into US distribution. It is also a product of the brand’s recent positioning, which has pushed average transaction prices for CX-50, CX-70 and CX-90 SUVs into US$40,000-60,000 territory — territory that competes more with Acura and lower-trim BMW X3 than with mainstream Toyota and Honda.

The strategic implication is double-edged. On the upside, the United States is the most profitable mainstream auto market in the world, and Mazda’s premium SUV mix earns operating margins well above what its global volume would otherwise suggest. On the downside, the company is unusually exposed to single-market risk: shifts in US dollar-yen exchange rates, in tariff policy, and in the pace of US EV adoption all hit Mazda’s earnings harder than they hit more geographically balanced peers. The Alabama joint plant with Toyota is partly a hedge against the first two of those risks; the EV roadmap, including the planned 2027-2028 platform, is the hedge against the third.

| Region | Approx. share of global retail sales | Strategic role |

|---|---|---|

| United States | ~30-32% | Profit engine; premium SUV mix (CX-50, CX-70, CX-90) |

| Japan (domestic) | ~13-15% | Home market; compact and kei-adjacent models |

| Europe | ~14-16% | MX-30 BEV and R-EV; emissions-driven electrification |

| China | ~9-11% | JV with Changan; under structural pressure |

| ASEAN & Oceania | ~10-12% | Thailand production base; pickup and SUV demand |

| Other (LatAm, ME, etc.) | ~15-20% | Distributor markets; CX-30 / CX-5 backbone |

The Toyota tie that nobody talks about enough

In August 2017, Mazda and Toyota disclosed a cross-shareholding: Toyota took 5.05 percent of Mazda, and Mazda took a smaller stake of about 0.25 percent in Toyota. The headline was small. The substance was not. The two companies committed to jointly develop electric vehicle technology, to share connected-car platforms, and to co-build a new US assembly plant in Huntsville, Alabama. That plant, Mazda Toyota Manufacturing USA, opened production in 2021 with capacity for approximately 300,000 vehicles per year, split between Mazda’s CX-50 and Toyota’s Corolla Cross.

For Mazda, the deal solved three problems at once. It gave the company access to Toyota’s hybrid and EV technology stacks at a fraction of the cost of building them alone. It provided a US production footprint at a moment when local content rules were tightening. And it offered a stable strategic anchor against the volatility of Chinese JV partners and European emissions regulators. For Toyota, the value was thinner but real: Mazda’s chassis dynamics and design language remain among the best in the industry, and Toyota was happy to keep a friendly minority position in a company with attractive engineering DNA.

Moro era: a CEO who knows the United States

Masahiro Moro became Representative Director, President and CEO of Mazda in June 2023, succeeding Akira Marumoto. Moro spent the bulk of his career on the commercial side, including a decisive stint as CEO of Mazda North American Operations from 2016 to 2022. Under his leadership, the US subsidiary executed the brand’s premium repositioning, raised dealer service standards, and rebuilt the retail network around larger, higher-margin SUVs. His promotion to global CEO was, in effect, a bet by the Hiroshima board that the company’s future hinges on the success of that US strategy.

Moro’s public statements have emphasised three priorities: defending the combustion business through SkyActiv hybrids and the rotary R-EV during the transition period; launching a dedicated EV platform around 2027-2028; and using the Toyota partnership to compress development timelines. The message to investors has been calibrated — Mazda is neither apologising for its late EV start nor pretending to compete with BYD on volume. The pitch is that a 1.3-million-unit specialist brand can earn premium margins by being unmistakably itself.

What this means for foreign partners

For foreign buyers, investors and licensors evaluating Mazda, four practical implications follow from this strategic profile.

First, Mazda is the most accessible of the major Japanese automakers for a non-Toyota-scale supplier or technology partner. Its smaller volumes and concentrated decision-making in Hiroshima mean shorter procurement cycles than Toyota City and faster engineering engagement than Yokohama. Suppliers of lightweighting materials, NVH solutions, premium interior components and combustion-efficiency technologies report comparatively responsive technical dialogue.

Second, the US dimension matters operationally. The Alabama plant, the North American R&D centre in Irvine, California, and the broader US dealer network all sit downstream of decisions made in Hiroshima, but day-to-day procurement and engineering work increasingly happens on US time zones. Foreign suppliers with a US footprint may find that route more efficient than direct Japan engagement.

Third, the brand’s premium positioning creates a specific opportunity for high-end interior, infotainment and audio partners. Mazda has consistently sourced premium audio from Bose for higher trims and has shown willingness to differentiate cabin experience as a brand pillar. For Japanese craft suppliers — textiles, woods, paint chemistries — Mazda is a more receptive customer than mass-market rivals.

Fourth, the Toyota relationship reshapes how Mazda evaluates new technology partners. Technologies that overlap with Toyota’s existing stack — hybrid systems, hydrogen fuel cells, connected services — will almost always route through the partnership. Technologies that complement rather than substitute — advanced combustion, lightweight materials, premium audio, niche electrification components — remain open territory.

The contrarian bet, summarised

Mazda’s strategic identity rests on a set of choices that look mistaken in isolation and coherent only in combination. Staying in Hiroshima limits the talent pool but builds an unusually deep engineering culture. Doubling down on combustion looks anachronistic but earns near-premium pricing today. Reintroducing the rotary as a range extender is commercially marginal but signals brand continuity to a customer base that buys Mazdas precisely because they are not Toyotas. Concentrating sales in the United States raises geopolitical risk but funds the entire R&D budget. Accepting a Toyota minority stake compromises strategic autonomy but provides survival insurance through the EV transition.

It is a portfolio of contrarian bets that, viewed from Fuchu-cho, is not contrarian at all. It is what a 1.3-million-unit specialist has to do to remain independent in an industry whose volume tier is consolidating around three or four global giants. For foreign partners, Mazda is the rare large Japanese automaker that still behaves like a focused engineering firm rather than a multinational conglomerate. That is its risk and its appeal.

FAQ

Is Mazda still independent, or is Toyota effectively controlling it?

Mazda remains independent. Toyota holds approximately 5.05 percent of Mazda’s shares (acquired in 2017) and Mazda holds a small reciprocal stake in Toyota. That is well short of any controlling threshold. The relationship is structured as a strategic alliance with joint EV development, a shared Alabama plant and selective platform cooperation, not as a parent-subsidiary arrangement. Mazda’s board, executive team and Hiroshima headquarters operate autonomously.

Why did Mazda bring back the rotary engine?

The 2023 MX-30 R-EV uses a single-rotor 830cc Wankel engine as a range extender for a plug-in hybrid system, not as the primary drivetrain. The reasoning is practical: rotary engines are small, light, and run smoothly at constant load — characteristics that suit a generator more than a traditional sports-car application. Reintroducing the rotary also preserves a piece of brand heritage that resonates with a specific enthusiast customer base.

How exposed is Mazda to the US market?

Approximately 30-32 percent of Mazda’s global retail volume goes to the United States, the highest US dependency among major Japanese automakers. This concentration generates strong margins thanks to a premium SUV mix (CX-50, CX-70, CX-90) but also exposes the company to US tariff policy, dollar-yen volatility and the pace of US EV adoption. The Alabama joint plant with Toyota mitigates some of the tariff risk by localising production.

What happened to Mazda’s relationship with Ford?

Ford acquired a 25 percent stake in Mazda in 1979 and raised it to a controlling 33.4 percent in 1996, using Mazda as a platform partner for vehicles such as the Ford Escape and Mazda Tribute. Following Ford’s own financial crisis in the late 2000s, it began selling down its position from 2008 onward, with the final divestment completed by 2015. The two companies retain commercial relationships in selected markets but no longer share equity.

Does Mazda have a credible electric vehicle strategy?

Mazda’s EV strategy is later and smaller-scale than rivals. The MX-30 BEV (introduced 2020) is its only fully electric model in most markets and has had limited commercial impact. The company has announced a dedicated EV platform expected around 2027-2028 and is leveraging the Toyota alliance for shared technology. The official position is that hybrids and efficient combustion engines will bridge the transition period, with full battery electric vehicles arriving in volume late this decade. Investors should view Mazda as an EV laggard with a structured catch-up plan, not as a leader.

Working with Mazda

Japonity helps foreign buyers, investors, licensors and component suppliers engage with Japanese automakers across the value chain — from Tier 1 supplier introductions to technology licensing and capital partnership discussions. If you are evaluating Mazda as a customer, technology partner or investment target, we can help structure the right entry point. Visit our business matching page to start a conversation.

Related from Japonity — Japan’s automakers

- Toyota Motor Corporation — Multi-pathway powertrain strategy from the world’s #1 automaker

- Honda Motor — The motorcycle giant the auto press forgot

- Nissan Motor — Post-Ghosn, post-Honda — what the Renault entanglement still means

- Subaru Corporation — The boxer-engine niche player that built America

- Suzuki Motor — India’s market king — Maruti Suzuki’s ~40%+ share

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →