Walk through Nihonbashi at dusk and you can read Mitsui Fudosan’s strategy in the skyline itself: the gleaming Coredo complexes anchoring the old merchant quarter, the cranes rising over Yaesu, the silhouette of Tokyo Mid-Town Hibiya across the moat, and — further out — the LaLaport malls ringing every major suburb in the country. Then look across the Pacific to 50 Hudson Yards in Manhattan and the new 270 Park Avenue tower that JPMorgan calls home. One company built, owns, or co-developed all of it. If Mitsubishi Estate is the patient landlord of Marunouchi, Mitsui Fudosan is the restless developer that keeps redrawing the map.

The aggressive developer in a conservative industry

Japanese real estate is famously oligopolistic. Three companies — Mitsui Fudosan, Mitsubishi Estate, and Sumitomo Realty & Development — control the bulk of central Tokyo’s prime office stock and a meaningful share of the country’s commercial development pipeline. Yet within that triumvirate, each plays a distinct role. Mitsubishi Estate is the dignified landlord of Marunouchi, content to compound rent on a portfolio of trophy assets it has held for a century. Sumitomo Realty is the build-to-lease machine, a margin-obsessed operator that owns more office towers in Tokyo than almost anyone else. Mitsui Fudosan is something different again: a developer that treats Japan as a single, integrated portfolio of urban-renewal projects, suburban retail, hospitality, logistics, and — increasingly — overseas property bets.

The numbers tell part of the story. Mitsui Fudosan’s revenue mix is unusually balanced for a Japanese real-estate giant: leasing is the anchor, but property sales (condominiums, investor-grade buildings), management, and a sprawling “other” segment that includes hotels, logistics, and overseas operations each contribute meaningfully. Where Mitsubishi Estate prefers the stability of long-leased Marunouchi towers, Mitsui Fudosan is willing to develop, flip, securitize, and re-deploy capital across asset classes. It is the closest thing Japan’s property industry has to an entrepreneurial flywheel.

From Mitsui zaibatsu to listed developer

The company traces its origins to the real-estate operations of the Mitsui zaibatsu, the merchant-banking conglomerate that dominated pre-war Japanese commerce. Mitsui Fudosan was incorporated in 1941 as a separate entity to manage the group’s property holdings, and after the post-war zaibatsu dissolution it emerged as an independent, listed developer — though the Mitsui group cross-shareholding lattice and the historical headquarters location in Nihonbashi still tie it culturally to its merchant-house roots.

Nihonbashi is not incidental. The neighbourhood was the commercial heart of Edo-era Tokyo, the kilometre-zero of the old Tōkaidō road, and the original home of Mitsui’s dry-goods business (which became the Mitsukoshi department store). For decades, Mitsui Fudosan has treated Nihonbashi as both a sentimental anchor and a flagship redevelopment site, gradually rebuilding the district through the Coredo Nihonbashi, Coredo Muromachi, and Nihonbashi Mitsui Tower projects. The bet is straightforward: a quarter that lost its glamour to Marunouchi and Ginza in the 20th century can be re-engineered as a mixed-use destination for the 21st.

Tokyo Mid-Town and the redevelopment playbook

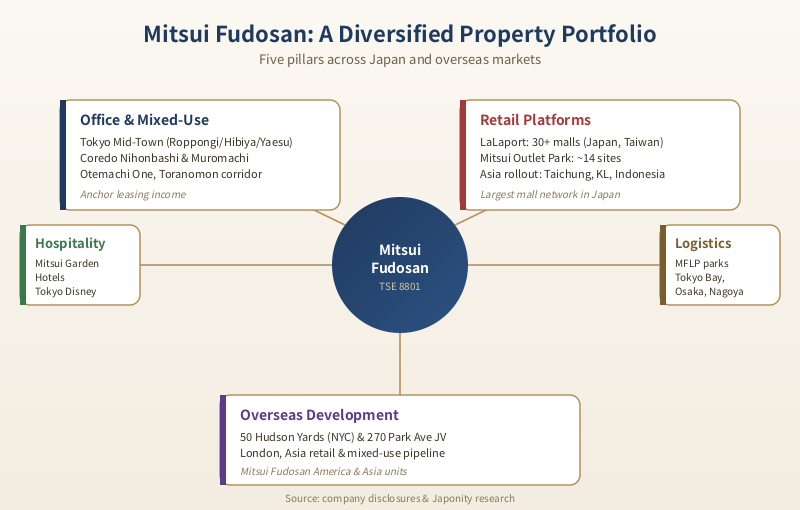

If Nihonbashi is the heritage play, Tokyo Mid-Town is the brand. Mitsui Fudosan has now opened three Mid-Town complexes — Roppongi (2007), Hibiya (2018), and Yaesu (2023) — each a mixed-use tower combining offices, luxury retail, a hotel, residential, and curated public space. Mid-Town Roppongi, built on the former site of the Defence Agency, established the template: cluster a Ritz-Carlton, premium offices, a Suntory Museum of Art, and landscaped grounds into a single integrated district, then charge a premium for every square metre. Hibiya and Yaesu adapted the formula to different audiences — culture-and-tourism in Hibiya, mobility and commuter-flow in Yaesu, where the complex sits directly above Tokyo Station’s Yaesu exit.

The playbook has become an export. Mitsui Fudosan’s role in the wider Toranomon-Azabudai corridor, its development of the Otemachi One complex, and its participation in Shibuya-area projects all draw on the same logic: large-footprint redevelopments that bundle Class-A office, luxury hospitality, retail, and cultural amenities into single brand-managed destinations. It is closer to the Hudson Yards model than to traditional Japanese office leasing.

| Segment | What it does | Examples | Strategic role |

|---|---|---|---|

| Leasing | Office & retail rent from owned buildings | Tokyo Mid-Town, Coredo Nihonbashi, Otemachi One | Recurring cash-flow anchor |

| Property Sales | Condominium development, investor-grade asset sales | Park Tower / Park Court / Park Mansion brands | Capital-velocity and ROE driver |

| Management | Building management, brokerage, REIT advisory | Mitsui Fudosan Realty, Nippon Building Fund | Fee income, low capital intensity |

| Other (Retail / Hotels / Logistics / Overseas) | LaLaport, Mitsui Outlet Park, Mitsui Garden Hotels, MFLP logistics, US/Asia projects | LaLaport Taichung, 50 Hudson Yards, MFLP Funabashi | Diversification and growth optionality |

LaLaport: suburban Japan as a national mall network

Where Mitsubishi Estate’s footprint is concentrated in a few square kilometres of central Tokyo, Mitsui Fudosan extends across the entire archipelago — and that is largely a story about LaLaport. The chain of regional shopping malls, the largest in Japan with more than thirty locations, has become a category-defining piece of suburban infrastructure: each LaLaport typically combines a hypermarket-scale anchor, two or three department-store-style fashion floors, a sprawling food court, cinemas, and family-oriented entertainment, all wrapped around a transit-accessible site near the urban fringe.

The economic logic is subtle. LaLaport is not a pure landlord business — Mitsui Fudosan develops, owns, and operates the malls, capturing leasing fees, percentage rents, and ancillary revenue (parking, advertising, services). Crucially, the chain has become a brand that local governments actively court: a new LaLaport anchors town-centre planning around it, drives land-value uplift, and pulls in tax revenue. That gives Mitsui Fudosan unusual negotiating leverage in site acquisition and zoning, particularly in second-tier cities where retail catchment is fragmented.

The format has also travelled. LaLaport Taichung opened in Taiwan in 2024, joining earlier overseas deployments in Shanghai and Kuala Lumpur, and additional projects in Indonesia are in the pipeline. The same logic applies to Mitsui Outlet Park, the company’s outlet-mall format, which now spans roughly fourteen sites in Japan plus locations in Malaysia and Taiwan. Together, LaLaport and Outlet Park give Mitsui Fudosan a retail platform that no domestic peer can match, and a credible export model in markets where the Japanese suburban-mall template still has whitespace.

Hospitality, logistics, and the un-glamorous middle

Around the edges of the headline projects sit two businesses that quietly anchor Mitsui Fudosan’s portfolio. The Mitsui Garden Hotels chain operates dozens of mid-scale urban hotels across Japan, plus a handful overseas, providing a steady stream of operating income that complements the lumpier development cycles. Combined with the company’s role as developer and operator behind the official hotels of the Tokyo Disney Resort — including Tokyo Disneyland Hotel and the Tokyo DisneySea Hotel MiraCosta — hospitality contributes a meaningful, tourism-correlated income line that has rebounded sharply with the post-pandemic surge in inbound visitors.

Logistics is the more recent story. Through the Mitsui Fudosan Logistics Park (MFLP) brand, the company has built one of Japan’s largest portfolios of modern, large-floorplate logistics facilities, riding the structural shift from manual-pick warehouses to mechanised distribution centres serving e-commerce, 3PL, and parcel networks. MFLP facilities cluster around major metropolitan demand centres — the Tokyo Bay area, Osaka, Nagoya — and are increasingly packaged into the company’s REIT-style structures, recycling capital back into new development.

The American bet: 50 Hudson Yards and 270 Park

Japanese property developers have a complicated history with US real estate. The late-1980s round of trophy-asset purchases — Rockefeller Center, the Pebble Beach golf resort — ended in tears and provided a generation of cautionary material for business-school case studies. Mitsui Fudosan’s contemporary American strategy is deliberately different, executed through its US subsidiary Mitsui Fudosan America with a focus on development partnerships rather than late-cycle trophy buys.

50 Hudson Yards, the 58-storey tower co-developed with Related Companies and Oxford Properties on Manhattan’s far west side, is the most visible example. Mitsui Fudosan is a major equity partner in the project, which is anchored by BlackRock as the lead tenant and exemplifies the same playbook the company runs in Tokyo: a large-scale mixed-use redevelopment of an under-utilised urban site, layered with premier-tier corporate tenants. The 270 Park Avenue project — JPMorgan Chase’s new global headquarters on the site of the demolished Union Carbide tower — is even more emblematic: Mitsui Fudosan participates as joint-venture partner in one of the most ambitious office developments in recent New York history.

The thesis is that Manhattan, London, and a handful of other gateway markets are structurally similar to Tokyo’s prime districts: supply-constrained, brand-tenant-led, and resilient across cycles. The execution risk is real, but the strategic intent is consistent — extend the Mid-Town redevelopment template to global cities where Japanese institutional capital is welcome and Mitsui Fudosan’s development capability is differentiated.

Mitsui Fudosan vs Mitsubishi Estate vs Sumitomo Realty

The cleanest way to understand Mitsui Fudosan is to place it alongside its two direct peers. The three companies all sit at the apex of Japanese property, but their portfolios and strategic temperaments diverge sharply.

| Mitsui Fudosan (8801) | Mitsubishi Estate (8802) | Sumitomo Realty (8830) | |

|---|---|---|---|

| Heart of the portfolio | Nihonbashi, Tokyo Mid-Town, LaLaport | Marunouchi (~30 buildings) | Shinjuku & central Tokyo office towers |

| Retail platform | LaLaport (~30+), Mitsui Outlet Park (~14) | Marunouchi Naka-dori retail, Premium Outlets JV | Limited; office-focused |

| Hospitality | Mitsui Garden Hotels, Tokyo Disney Resort hotels | Royal Park Hotels, Hotel The Celestine | Villa Fontaine |

| International posture | Aggressive — 50 Hudson Yards, 270 Park, LaLaport overseas | Selective — UK, US prestige assets | Domestic-heavy |

| Strategic style | Diversified developer / portfolio recycler | Patient blue-chip landlord | Build-to-lease, ROE-disciplined |

The three are not strictly comparable — Sumitomo Realty in particular runs a deliberately leaner, office-leasing-centred model that prioritises return on equity over portfolio breadth — but the contrast highlights Mitsui Fudosan’s distinctive bet. It is the firm that has chosen to own the entire urban stack, from premier downtown towers down to suburban malls, regional outlets, logistics parks, and overseas trophy developments. That breadth is both its competitive moat and its principal exposure: more cycles to manage, more capital to recycle, more execution surface across more asset classes.

Governance, sustainability and the next decade

Listed on the Tokyo Stock Exchange Prime Market under code 8801, Mitsui Fudosan has come under the same investor pressure as the rest of corporate Japan to lift capital efficiency, unwind cross-shareholdings, and articulate clearer mid-term targets. Under CEO Takashi Ueda, the company has emphasised three planks: domestic redevelopment leadership (the Toranomon-Azabudai corridor, continued Nihonbashi build-out, additional Mid-Town openings), accelerated overseas growth (further US development, Asian retail expansion), and a transition to a lower-carbon real-estate portfolio.

The sustainability programme commits the group to long-dated decarbonisation targets, with operational net-zero milestones for its owned portfolio and increasing emphasis on green building certifications, on-site renewable generation, and embodied-carbon reduction in new developments. For a developer whose product is, by its nature, carbon-intensive — concrete, steel, glass, decades of operational energy — the credibility of that commitment is now a meaningful equity-story variable as well as a regulatory one.

Why Mitsui Fudosan matters

For foreign companies trying to read Japan’s real-estate landscape, Mitsui Fudosan is the most useful single firm to understand. It is the developer most willing to take on large-scale mixed-use projects, the operator behind the suburban retail platform most foreign consumer brands first encounter when they enter Japan, the hospitality partner behind some of the most visited tourist sites in the country, and the Japanese property investor with the most active overseas development pipeline. Its strategy is, in a sense, a microcosm of how Japan as a whole is trying to position itself: globally engaged, domestically dense, hospitality-rich, sustainability-conscious, and unusually patient about the long arc of urban regeneration.

Mitsubishi Estate may be the landlord. Sumitomo Realty may be the disciplined operator. But Mitsui Fudosan is the developer that keeps redrawing the map — and for businesses thinking about Japan as a market, a location, or a partner, that makes it the firm whose next move is most worth watching.

FAQ

What does Mitsui Fudosan actually do?

Mitsui Fudosan is a diversified real-estate developer and operator. Its core businesses are commercial leasing (offices and retail), property sales (condominiums and investor-grade buildings), property management, and a wide “other” segment covering retail facilities (LaLaport, Mitsui Outlet Park), hotels (Mitsui Garden Hotels and the Tokyo Disney Resort hotels it operates), logistics (Mitsui Fudosan Logistics Park), and overseas development.

How is it different from Mitsubishi Estate?

The simplest way to think about it: Mitsubishi Estate is the long-term landlord of Marunouchi, where it owns roughly thirty buildings within a few hundred metres of Tokyo Station, and runs a comparatively concentrated portfolio. Mitsui Fudosan is the more diversified, more entrepreneurial developer — built around redevelopments (Nihonbashi, Tokyo Mid-Town, the Toranomon-Azabudai corridor), a nationwide retail platform (LaLaport, Mitsui Outlet Park), hospitality, logistics, and overseas growth.

What is LaLaport?

LaLaport is Mitsui Fudosan’s chain of large suburban shopping malls, the biggest such network in Japan with more than thirty locations. Each LaLaport typically combines a large grocery anchor, two to three floors of fashion and lifestyle retail, an extensive food court, cinemas, and family entertainment. The brand has also been exported, with LaLaport Taichung in Taiwan and additional projects in Southeast Asia.

Why is Mitsui Fudosan investing in New York?

Mitsui Fudosan America has taken meaningful equity positions in two of the most ambitious recent Manhattan developments: 50 Hudson Yards (co-developed with Related Companies and Oxford Properties, anchored by BlackRock) and 270 Park Avenue (JPMorgan Chase’s new global headquarters). The strategic rationale is that supply-constrained gateway markets such as Manhattan and central London resemble central Tokyo in their long-run dynamics, and Mitsui Fudosan’s large-mixed-use development capability is a differentiated export.

How can a foreign company work with Mitsui Fudosan?

The most common entry points are commercial leasing in one of Mitsui Fudosan’s Tokyo office complexes (Tokyo Mid-Town, Coredo Nihonbashi, Otemachi One and others), opening retail or food and beverage units in LaLaport or Mitsui Outlet Park properties, or partnering on development projects through Mitsui Fudosan America for US deals or the group’s Asia teams for regional retail. Japonity can help map the right counterpart and structure an initial introduction.

Working with Mitsui Fudosan

For foreign brands, investors, and operators, Mitsui Fudosan is one of the most strategically important Japanese counterparties to understand — a developer that touches central-Tokyo office stock, the country’s dominant suburban retail platform, the Tokyo Disney Resort hotels, a fast-growing logistics portfolio, and a globally significant overseas development pipeline. If you are exploring Tokyo office leasing, a Japanese retail rollout, a hospitality partnership, or co-investment in mixed-use redevelopment, Japonity can help you identify the right entry point and arrange an introduction. Start with our business matching service.

Related from Japonity — Japan’s real estate giants

- Mitsubishi Estate — The Marunouchi landlord — ~30 buildings in Tokyo’s prime district

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →