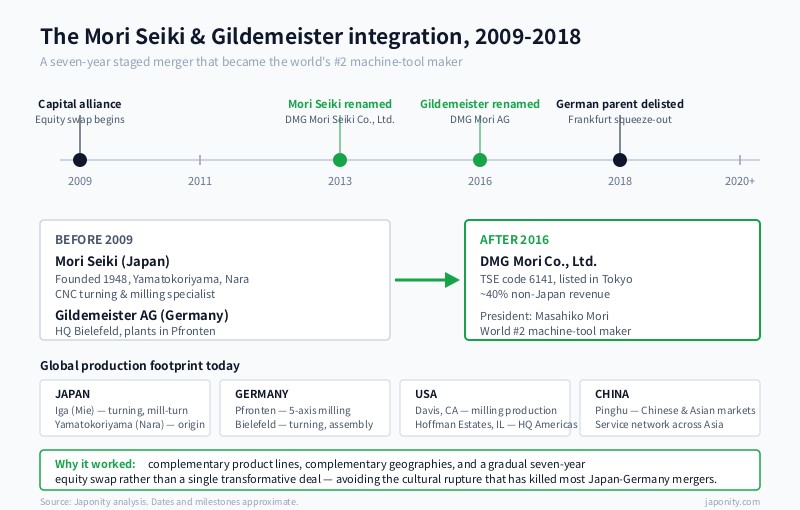

DMG Mori Co., Ltd. is the world’s second-largest machine-tool maker by revenue, behind only the privately held Yamazaki Mazak — but unlike every other entrant in the global top ten, it is the product of an unusually durable cross-border industrial marriage. The company was assembled between 2009 and 2016 from Mori Seiki, the Japanese CNC turning and milling specialist founded in 1948 in Yamatokoriyama, Nara, and Gildemeister AG, the Bielefeld-based group that had grown into Europe’s largest machine-tool maker by the late 2000s. Roughly 40% of revenue now comes from outside Japan. For foreign aerospace, automotive, and medical-device manufacturers, DMG Mori is the closest thing the industry has to a global one-stop shop for high-precision CNC turning, milling, multi-axis and additive equipment, backed by an Industry 4.0 software stack — DMG Mori Adamos, the IIoT cloud, and the Celos control system — that few competitors can match end-to-end.

The merger that was not supposed to work

Cross-border industrial mergers between Japanese and Western firms have an uneven historical record. The graveyard includes Daimler-Mitsubishi Motors, the messier patches of the Renault-Nissan alliance, and a long list of less famous failures where governance frictions, cultural mismatches, and dual-headquarters paralysis quietly killed value. The Mori Seiki-Gildemeister combination, by contrast, has worked — and the reason it worked is instructive.

The starting position in 2009 was unusual. Mori Seiki and Gildemeister were not direct competitors. Mori Seiki was the dominant Japanese player in CNC turning centres and was strong in horizontal and vertical machining centres for medium-to-large workpieces, with a manufacturing base in Iga (Mie Prefecture) and the original Yamatokoriyama works in Nara. Gildemeister, through its DMG brand, had built Europe’s broadest line in vertical and 5-axis milling, mill-turn and ultrasonic-assisted machines, with major plants in Pfronten (Bavaria) and Bielefeld (North Rhine-Westphalia). Their product lines overlapped meaningfully in only a handful of segments. Their geographies — Japan and East Asia versus Europe — were complementary rather than redundant.

The two companies signed a capital and business alliance in 2009 and proceeded to swap equity stakes gradually over the following seven years rather than executing a single transformative transaction. Mori Seiki took an initial minority stake in Gildemeister, sales channels were unified, then production sites began cross-licensing each other’s controls and modules. In 2013 the Japanese parent renamed itself DMG Mori Seiki to signal the integration was no longer reversible. In 2016 the German parent renamed itself DMG Mori Aktiengesellschaft. Mori Seiki then increased its stake in the German company further, eventually delisting the parent’s shares from the Frankfurt exchange in 2018 after a domination and profit-and-loss transfer agreement. From the outside, what looked like a slow process was, internally, a deliberate sequence designed to avoid the cultural rupture that has killed almost every other Japan-Germany industrial merger of comparable scale.

Where DMG Mori sits in the global machine-tool league table

Machine-tool industry share data is notoriously messy: definitions vary (does an EDM machine count? what about additive systems?), some leaders are private and disclose little, and FX swings move year-on-year rankings around. The shape below is approximate but the relative ordering has been stable for several years.

| Group | HQ | Approx. machine-tool revenue rank | Strength |

|---|---|---|---|

| Yamazaki Mazak | Oguchi, Aichi (private) | #1 | Multi-tasking, integrex mill-turn, US/Asia footprint |

| DMG Mori | Nara / Bielefeld (TSE 6141) | #2 | 5-axis milling, turning, Industry 4.0 software |

| Trumpf | Ditzingen, Germany (private) | #3 | Laser cutting, sheet-metal, EUV power lasers |

| Okuma | Oguchi, Aichi (TSE 6103) | #4 | Turning centres, full-line domestic Japan supplier |

| Makino | Tokyo (TSE 6135) | #5-6 | EDM, high-precision milling for tooling/aerospace |

| FANUC | Oshino, Yamanashi (TSE 6954) | Separate league | CNC controls (dominant), robots, ROBODRILL |

| Hardinge / GF Machining | Berthoud (US) / Geneva | #7-10 range | Grinding, EDM, micro-precision |

| Doosan Machine Tools (DN Solutions) | Changwon, South Korea | #7-10 range | Turning, automotive supply base |

Two points worth noting. First, FANUC is in the table only as a reference: it is not strictly a machine-tool builder, but as the dominant supplier of CNC controls to most of the rest of the industry — including DMG Mori’s own Celos-on-Siemens and Celos-on-FANUC variants — it shapes economics across the sector. Second, the gap between Mazak and DMG Mori at the top is real but narrowing in 5-axis and mill-turn segments where DMG Mori’s German heritage gives it depth that Mazak has historically had to build organically.

The product line: turning, milling, multi-axis, additive

DMG Mori sells approximately 180 different machine models across roughly half a dozen categories. CNC turning centres — the legacy Mori Seiki strength — remain a large revenue contributor, with the NLX and NTX series anchoring the line. The NTX series is the company’s mill-turn flagship: a single machine that performs full turning, full milling, and Y-axis off-centre work in one setup, the kind of equipment that aerospace and medical OEMs increasingly demand to compress part flow and reduce fixturing variance.

On the milling side, the DMU and DMC series (German heritage) provide 3- to 5-axis vertical and horizontal machining for everything from automotive die work to titanium aerospace structures. The duoBLOCK and monoBLOCK frame designs, originally a Pfronten development, are now produced at Iga and Davis (California) as well, with parts and modules shipped between plants under a unified manufacturing system. The Lasertec series — laser texturing, additive deposition, and powder-bed additive — sits on a separate sub-brand and represents DMG Mori’s bet on the convergence between subtractive and additive metal manufacturing. The fact that one supplier can ship a powder-bed 3D printer and a 5-axis finishing machine that share a control philosophy is itself a differentiator.

The Industry 4.0 stack: where DMG Mori stops being just a machine builder

For most of the twentieth century, machine-tool makers competed on mechanical accuracy, thermal stability, spindle rigidity, and the quality of their controls. Those still matter. But the differentiator in the 2020s is increasingly the software layer that sits above the iron — and this is where DMG Mori has invested most aggressively, partly to defend against FANUC’s grip on controls and partly to build a recurring-revenue stream that machine-tool builders have historically lacked.

Celos is the company’s machine-side operating environment, a touch-based interface that runs on top of either Siemens Sinumerik or FANUC controls and standardises the operator experience across the entire DMG Mori line. The DMG Mori IIoT cloud — built on Microsoft Azure — collects machine telemetry for condition monitoring, OEE analysis, and predictive maintenance. Adamos, originally a joint venture with Software AG, ASM PT, Dürr, Zeiss, and others, provides the open Industrial IoT platform layer that allows DMG Mori machines to interoperate with other vendors’ equipment on the same factory floor — a deliberate counter-move against vertically integrated closed ecosystems.

For a customer running a multi-vendor shop floor — and most aerospace and medical-device manufacturers do — this matters. A Pfronten 5-axis milling centre, an Iga mill-turn, and a Lasertec additive cell can be commissioned, monitored, and optimised through a common software layer, with telemetry feeding into the customer’s MES or ERP without bespoke integration. Few competitors offer this end-to-end stack. Mazak has SmartBox and iSmart Factory; Trumpf has TruConnect; Okuma has Connect Plan. None of them combines the depth of Adamos with the geographic spread of DMG Mori’s service network.

The customer base: who actually buys these machines

Approximately 40% of revenue comes from outside Japan, with Europe historically the largest non-Japan region (a Gildemeister legacy), followed by North America and a growing China segment. The customer base concentrates in three industries: automotive (including EV powertrain and battery housing work), aerospace, and medical devices, with electronics, semiconductor equipment, and general industrial filling the remainder.

Automotive customers — both legacy ICE OEMs and EV-native firms — buy DMG Mori predominantly for powertrain and chassis component work, with growing volumes for battery cell tray machining and motor housing milling. The EV transition has not been the existential threat to machine-tool demand that some forecasters predicted in 2020; it has shifted the workpiece mix toward aluminium and copper, increased demand for high-throughput milling, and reduced demand in some legacy gear-cutting and crankshaft-grinding niches. DMG Mori’s exposure has rebalanced accordingly.

Aerospace customers — Boeing, Airbus, the engine OEMs Pratt & Whitney, Rolls-Royce, and Safran, and their tier-one suppliers — drive demand for 5-axis titanium milling, blisk machining, and the largest mill-turns. This segment is structurally tied to commercial aviation production rates, which finally recovered in 2023-2024 from the COVID-era trough and are constrained today more by supply chain than by demand. Medical-device customers — implant manufacturers, surgical-tool makers, and the growing dental sector — buy small-envelope precision machines, with biocompatible titanium and stainless-steel work driving model-mix choices.

The footprint: Japan-Germany dual core, US and China as production centres

DMG Mori operates production on four continents. In Japan, the Iga campus (Mie Prefecture) and the historic Yamatokoriyama works (Nara) cover turning, mill-turn, and selected milling families. In Germany, Pfronten (Bavaria) is the global centre for 5-axis milling and the large duoBLOCK machines, while Bielefeld (North Rhine-Westphalia) is the long-standing Gildemeister base for turning and assembly. In the United States, Davis, California houses milling production and serves North American customers, and Hoffman Estates, Illinois is the Americas headquarters and training centre. In China, the Pinghu plant near Shanghai produces machines for the Chinese and broader Asian markets.

This dual-cored, four-continent structure has practical implications for foreign customers. Spare parts are stocked locally on each continent. Service engineers are trained on common platforms, which means a 5-axis milling centre installed in Munich can be supported by a service engineer trained in Nagoya without major translation friction. Lead times, which spiked across the industry in 2021-2022, have largely normalised, though the most heavily configured multi-axis mill-turns still carry six to twelve months of backlog.

Leadership and governance

Masahiko Mori, the grandson of the founder Tsuneo Mori, has been the chief architect of the German integration and remains president of DMG Mori. His decade-and-a-half tenure overlapping the merger process gave the integration a continuity of vision that most cross-border mergers lack — the same person who designed the alliance in 2009 saw it through the renaming, the equity consolidation, and the post-2018 squeeze-out of remaining minority shareholders in Germany. Christian Thönes, the long-time German CEO of the AG, served alongside Mori through the critical integration years before stepping down in 2022. The current top management is dual-locus by design: Japan-based and Germany-based executives share supervisory functions, and the supervisory board includes representatives from both heritage organisations.

The company is listed on the Tokyo Stock Exchange (ticker 6141, Prime Market). The shareholder base is mostly Japanese institutional, with notable foreign holdings. Cross-shareholdings are limited compared to other Japanese industrial conglomerates — a deliberate choice that has given the company room to make integration decisions without consensus-building inside a tight keiretsu.

The risks worth pricing

Three structural risks frame the medium-term view. First, Chinese domestic machine-tool builders — Shenyang Machine Tool, DMTG, and a cluster of newer entrants — have closed much of the technology gap in standard 3-axis milling and conventional turning, and are competing aggressively in the lower and middle tiers of the global market. DMG Mori’s defensive position depends on holding the high end (5-axis, mill-turn, additive, software-integrated) where Chinese competitors are still behind.

Second, the FANUC dependency. DMG Mori’s machines run predominantly on either Siemens Sinumerik or FANUC controls; Celos sits above these but does not replace them. If FANUC ever chose to favour its own ROBODRILL line or restrict access to advanced control features, the dynamics could shift. To date FANUC has behaved as a neutral supplier to the industry, but the structural risk is real.

Third, machine-tool demand is procyclical. The 2008-2009 collapse, the 2015-2016 slowdown, and the 2020 COVID trough each cut industry orders sharply. DMG Mori’s larger service and spare-parts revenue base — now a meaningfully larger share of total revenue than at the pre-merger Mori Seiki — provides some buffer, but the company remains exposed to global capex cycles in a way that, say, FANUC’s controls business is not.

What this means for foreign manufacturers and suppliers

For aerospace, automotive, and medical-device manufacturers outside Japan that are buying or specifying capital equipment, DMG Mori warrants direct evaluation against Mazak, Trumpf, and Okuma rather than being treated as a generic Japanese alternative. The Japan-Germany dual heritage means that a customer in, say, Toulouse can specify a Pfronten-built 5-axis machine with the same software stack, service contract, and spare-parts logistics as a customer in Nagoya specifying an Iga-built mill-turn. The Industry 4.0 layer — Celos, the IIoT cloud, Adamos — is the most credible attempt by any machine-tool maker to compete as a software-and-iron company rather than a pure metal-cutting builder.

For component suppliers — spindle bearings, linear guideways, ballscrews, tool-holders, coolant systems, automation cells — DMG Mori sources from a global supplier base that includes both Japanese (NSK, THK, NTN, Big Daishowa) and German (Schaeffler, Bosch Rexroth, HSK, Schunk) firms, with the historical pattern of Japan-built machines pulling more from Japanese suppliers and German-built machines pulling from European suppliers slowly giving way to convergence. The procurement decision points are split: Iga and Yamatokoriyama for Japanese-built models, Pfronten and Bielefeld for European models, with corporate-level frame agreements increasingly applied across both.

FAQ

Is DMG Mori a Japanese or a German company?

Both, structurally. The listed parent is Japanese (Tokyo Stock Exchange code 6141) and the original founder family — the Mori family of Nara — remains the controlling influence at the top. The product lines, however, are split roughly half-and-half between Japanese-origin designs (mostly turning and mill-turn) and German-origin designs (mostly 5-axis milling and additive), produced respectively in Iga/Yamatokoriyama and Pfronten/Bielefeld. The company brands itself as global rather than nationally rooted, and customers in North America and Europe rarely distinguish between the two heritages.

How did DMG Mori become the world’s number two machine-tool maker?

Through the 2009-2016 merger between Mori Seiki and Gildemeister AG. Before the merger, Mori Seiki was a strong but mid-sized Japanese player and Gildemeister was Europe’s largest machine-tool group. Combining them produced a company with roughly double the revenue base of either standalone and with complementary product and geographic footprints. The ranking behind Mazak reflects the broader CNC turning, milling, and mill-turn portfolio combined with a global service network few competitors match.

What is the difference between DMG Mori and FANUC?

FANUC primarily makes CNC controls, industrial robots, and the ROBODRILL line of compact machining centres. DMG Mori primarily makes the machine tools themselves — turning centres, milling centres, mill-turns, and additive systems — many of which run on FANUC’s controls. The two companies are partners in many configurations and competitors at the margins where their product ranges touch (ROBODRILL versus DMG Mori’s smaller mills, for instance). They serve overlapping customers but are not direct substitutes for most procurement decisions.

How does DMG Mori’s Industry 4.0 stack compare to competitors?

DMG Mori has invested more publicly in software than most peers, with three named layers: Celos (machine operator interface), the DMG Mori IIoT cloud (telemetry and predictive maintenance on Microsoft Azure), and Adamos (open IIoT platform originally jointly developed with Software AG, ASM PT, Dürr, Zeiss and others). Mazak, Trumpf, and Okuma each have their own platforms, but the breadth and openness of Adamos in particular is unusual in the industry. Whether this software lead translates into a defensible recurring-revenue business over the next decade is one of the open strategic questions for the company.

How do foreign suppliers qualify into DMG Mori’s supply chain?

Procurement is split by manufacturing site: spindle bearings, guideways, ballscrews, coolant systems, electrical and automation components for Japanese-built models go primarily through Iga and Yamatokoriyama purchasing, while European-built models are sourced through Pfronten and Bielefeld. Corporate frame agreements cover an increasing share of common components. Suppliers with differentiated technology in high-stiffness bearings, advanced linear motors, precision sensors, tool-changer automation, or coolant/chip management have viable paths to qualify, typically beginning through application engineering at the nearest manufacturing site rather than through Nara headquarters.

Working with DMG Mori

For overseas aerospace, automotive, and medical-device manufacturers specifying or buying capital equipment, DMG Mori warrants direct comparison with Mazak, Trumpf, Okuma, and Makino rather than being treated as a generic alternative. The Japan-Germany dual heritage gives the company a service footprint and a product breadth — turning, milling, multi-axis, mill-turn, additive, and the software layer above — that few competitors match end-to-end. The procurement entry points differ by region: North American customers typically engage through Hoffman Estates and Davis, European customers through Pfronten and Bielefeld, and Asian customers through Iga, Yamatokoriyama, and Pinghu.

For component suppliers — bearings, guideways, ballscrews, tool-holders, automation, sensors, coolant and chip management, software — DMG Mori sources from a global supplier base across Japan, Germany, and increasingly other geographies. Qualification typically begins through application engineering at the nearest manufacturing site, with corporate frame agreements applied across sites for strategic components.

If your company makes capital equipment specification decisions in aerospace, automotive, or medical-device manufacturing, supplies precision components or industrial software relevant to DMG Mori’s product line, or is looking to license Japanese or German machine-tool technology into your home market, Japonity’s business matching service can help structure a credible first conversation with the right counterparty inside the company.

Related from Japonity — Japan’s industrial conglomerates & machine tools

- Mitsubishi Heavy Industries — Japan’s defence renaissance has a prime contractor

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →