Sega Sammy Holdings is the most architecturally unusual entertainment conglomerate in Japan, and possibly anywhere. The company that publishes Sonic the Hedgehog, the Persona role-playing series, the Like a Dragon (formerly Yakuza) crime saga, Total War, Football Manager, and Phantasy Star Online is also, in cash-flow terms, a pachinko and pachislot business. Roughly half of consolidated operating profit in most years has come from the Japanese gambling-machine arm inherited from Sammy Corporation, and a meaningful share of the cash thrown off by selling pachislot cabinets to parlour operators flows into the budgets of console and PC game studios in Tokyo, Horsham, and London. Formed in October 2004 by the merger of arcade-and-console publisher Sega Corporation with pachislot-machine maker Sammy Corporation, the group has spent two decades quietly redirecting yen from a structurally declining Japanese gambling industry into globally branded game intellectual property — most visibly the Hollywood Sonic films, the breakout success of Like a Dragon: Infinite Wealth, and the Persona series’ transition from cult JRPG to a multi-billion-yen franchise.

An improbable merger: how arcade Sega met pachislot Sammy

In 2004, neither half of the merger was obviously a winner. Sega Corporation, founded in 1960 in Tokyo as Service Games of Japan by an American expatriate-led group and merged in 1965 with Rosen Enterprises (run by David Rosen), had spent the 1990s losing the console wars. The Mega Drive (Genesis) was a credible challenger to Nintendo in early-1990s North America, but the Saturn was outsold by Sony’s PlayStation, and the Dreamcast (1998-1999) was discontinued in early 2001 after Sony’s PlayStation 2 captured the next-generation market. In January 2001 Sega formally exited the home-console hardware business and reorganised as a software publisher and arcade operator.

Sammy Corporation, founded in 1975 by Hajime Satomi, had taken the opposite trajectory — a small Tokyo workshop building pachislot machines that rode the 1990s and early 2000s boom to become a dominant manufacturer of the cabinets filling the country’s thousands of parlours. By the early 2000s Sammy was sitting on a large cash pile and looking to diversify. Satomi invested in Sega in 2003, and in October 2004 the two companies combined under a new holding company, with Satomi becoming chairman and the largest individual shareholder.

The strategic logic on paper was straightforward: Sammy had cash; Sega had global IP and development talent. In practice it was more delicate. Pachinko and pachislot are politically and demographically sensitive industries in Japan; many international investors will not hold stocks with meaningful gambling exposure, and many Western media partners will not co-brand with them. Sega Sammy has spent twenty years managing that arrangement, segmenting the group so the games business can present itself to international audiences without dragging the gambling-machine logo through every Sonic trailer.

The segment structure: pachislot pays, games grow

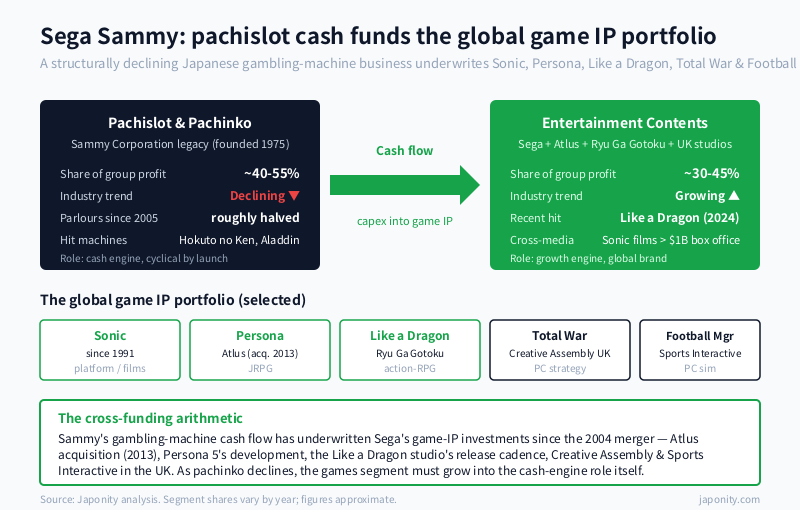

Sega Sammy reports under four main segments. The structural pattern — gambling machines as the cash engine, games as the growth and brand engine, resort as a long bet, the rest as residual — has been remarkably persistent in the two decades since the merger.

| Segment | Approx. share of group profit | Strategic role | Key assets |

|---|---|---|---|

| Pachislot & Pachinko | ~40-55% (variable) | Cash engine; cyclical by machine launch | Sammy-branded pachislot and pachinko machines, parlour operator relationships |

| Entertainment Contents (games) | ~30-45% | Growth engine; global brand vehicle | Sega, Atlus, Creative Assembly, Sports Interactive, Ryu Ga Gotoku Studio |

| Resort | low single digits, loss-making in some years | Long bet on integrated resorts | Paradise City (Incheon, Korea, JV with Paradise Group) |

| Other / Eliminations | residual | Real estate, music, ancillary | Tokyo Joypolis (until 2017), Sega Toys (until 2017 spin-off) |

The numbers move year to year. In strong pachislot launch years, gambling-machine profit can dominate the group P&L, occasionally well over half of operating profit. In quieter years or years with a major game-IP release schedule, the games segment closes the gap or briefly overtakes it. What does not change is direction: pachislot has been the net cash provider for the consolidated group for most of the post-merger period, and games has been the net cash consumer in terms of upfront development spend, even when its operating profit is positive.

Sonic: the franchise that survived the console exit

Sonic the Hedgehog launched in June 1991 as Sega’s mascot character, designed by Naoto Ohshima and a team led by Yuji Naka to be the company’s answer to Nintendo’s Mario. For most of the 1990s, Sonic was one of the two or three most valuable platform-game franchises in the world. The 2000s were harder — a series of three-dimensional Sonic titles received mixed reviews, and the franchise’s cultural cachet slipped against newer competitors.

The Sonic resurgence of the 2020s is one of the more interesting franchise-management stories in Japanese entertainment. The Paramount Pictures Sonic films (2020, 2022, 2024) collectively crossed well over a billion U.S. dollars in worldwide box office, with the third in particular becoming the highest-grossing video-game-based film in history at the time of its release. The films succeeded partly because of Paramount’s redesign of the title character following 2019 fan backlash to the initial trailer, and partly because Sonic had retained genuine multi-generational recognition outside Japan in a way few Japanese game brands besides Mario, Pokemon, and Zelda had managed. Sonic is now closer to a multi-channel media franchise than a pure game brand, and the films have re-energised demand for the underlying games.

The Atlus acquisition and the Persona franchise

In September 2013 Sega acquired Atlus, the Tokyo-based developer of the Persona and Shin Megami Tensei role-playing series, from the bankrupt Index Corporation for a reported figure in the tens of billions of yen. The deal was treated at the time as defensive — Atlus was a respected mid-size studio with a cult following, and Sega was thought to be picking it up largely to keep it out of competitors’ hands.

What followed was one of the highest-return acquisitions in modern Japanese gaming. Persona 5, released in 2016 in Japan and 2017 in the West, became a global hit far beyond the franchise’s previous scale, with the enhanced re-release Persona 5 Royal continuing to sell strongly through the early 2020s. The series has expanded onto every major platform — Xbox, PlayStation, Switch, and PC via Steam — and the brand has spawned spin-off rhythm games, anime adaptations, and a stage musical run. Atlus also delivered Shin Megami Tensei V in 2021, with an enhanced Vengeance edition in 2024. By most reasonable estimates the deal has returned a multiple of its purchase price in cumulative software revenue and licensing, and it gave Sega a global JRPG franchise at a moment of renewed international demand.

Like a Dragon, Total War, Football Manager: the studio portfolio

Sega Sammy’s games operation is not a single studio but a portfolio of development houses, each with distinct IP and audience. The Ryu Ga Gotoku Studio, based in Tokyo and headed for many years by Toshihiro Nagoshi (departed 2021) and now by Masayoshi Yokoyama, produces the Yakuza series — rebranded Like a Dragon for international markets from 2020. Like a Dragon: Infinite Wealth (January 2024) was the franchise’s strongest commercial performance to date and confirmed its transition from a Japan-centric cult franchise to a globally branded action-RPG line. The studio’s output cadence — roughly one mainline entry plus a spin-off each year — is unusually fast for AAA Japanese development.

Creative Assembly, based in Horsham, West Sussex, was acquired by Sega in 2005 and develops the Total War historical strategy series — Rome, Medieval, Empire, Shogun, Attila, Three Kingdoms, Pharaoh, plus the long-running Warhammer trilogy under Games Workshop licence. The studio also developed Alien: Isolation (2014), widely regarded as one of the best Alien-franchise games. Sports Interactive, based in London and acquired in 2006, develops Football Manager — the dominant football-management simulation in the world, with a multi-million-unit annual sales base and an exceptionally loyal community. The studio retains significant operational autonomy and has been one of Sega’s most reliable revenue contributors year after year. Phantasy Star Online 2 and its NGS expansion continue as a long-running online RPG service, with a global launch in 2020.

The pachinko decline and the cash-flow question

The structural problem is that the cash engine is shrinking. The Japanese pachinko and pachislot industry has been in long-run decline since its mid-2000s peak, when total industry gross gaming revenue ran into the tens of trillions of yen annually. By the mid-2020s, industry revenue had roughly halved from peak, the active player population had aged and shrunk, the number of parlours had roughly halved over two decades, and younger Japanese demographics were largely uninterested. Regulatory tightening on machine payout volatility from 2018 onward accelerated the contraction.

Sega Sammy has responded by trying to make each remaining pachislot launch count more. Hit machines built around well-known anime or Sega-owned IP — including Hokuto no Ken (Fist of the North Star) and Aladdin — drive a disproportionate share of segment profit when they land. The segment is therefore increasingly cyclical: investors and management both know the multi-decade direction of the gambling-machine cash flow is downward.

The strategic implication has been a deliberate reweighting of the consolidated group toward the games segment. Capital expenditure has shifted disproportionately to game development, the resort business has been pruned (Sega Sammy exited the Phoenix Seagaia Resort in 2017 by selling it to a Chinese investor group), and recent corporate communications have emphasised the entertainment-contents arm as the future growth engine. The cash the pachinko business throws off while it still can is, increasingly explicitly, being routed into game IP that can compound over decades.

Resort: the integrated-resort bet that did not quite happen

Sega Sammy’s resort segment is the smallest and the slowest to deliver. The flagship asset is the Paradise City integrated resort at Incheon International Airport, a joint venture with Korean operator Paradise Group that opened in 2017. It combines a casino (for foreign passport holders only, per Korean law), hotels, a convention centre, and entertainment facilities, positioned to capture travellers transiting through one of north-east Asia’s largest airports.

The wider ambition behind the segment had been Japan’s domestic integrated-resort regime, enabled by 2018 legislation allowing up to three IR licences. Sega Sammy was widely expected to be a credible bidder. In practice the Japanese IR process has moved far more slowly than envisaged — only one of the three permitted licences (in Osaka, awarded to a consortium not led by Sega Sammy) has advanced materially. The resort segment therefore remains a long bet rather than a near-term growth driver.

Governance: the Satomi family and the founder’s son

Sega Sammy is unusual among Tokyo Stock Exchange Prime-listed companies in being a still-family-influenced holding. Hajime Satomi, the Sammy founder who engineered the 2004 merger, served as chairman and group CEO for most of the post-merger period. His son, Haruki Satomi, was named president of the holding company in 2017 and has progressively taken on operational leadership, with a particular focus on the entertainment-contents segment.

The governance posture under Haruki Satomi has been more visibly oriented toward the global games business than under his father. English-language investor communications have improved, the Like a Dragon and Sonic global push has been actively championed at the holding-company level, and recent corporate-strategy documents have placed the entertainment-contents segment at the centre of medium-term planning. The group is listed on the Tokyo Stock Exchange under code 6460 and remains headquartered in Tokyo’s Shinagawa district.

Why the unusual shape matters

The temptation, looking at Sega Sammy from outside Japan, is to wish away the pachinko half — to imagine a spin-off in which the global games arm trades on its own at a Western multiple. That spin-off is not impossible, but it is not what management has chosen to do, and the reason is genuine: the pachinko cash flow, declining as it is, has been an enormously useful funding source for game-IP investments that would otherwise have had to compete with quarterly earnings pressure on a stand-alone basis. Persona 5’s development cycle, Ryu Ga Gotoku Studio’s release cadence, the Total War: Warhammer trilogy, Football Manager’s continued investment, and the Hollywood Sonic negotiations all benefited from sitting inside a group with a separate, structurally cash-positive segment.

The medium-term question is what happens when the pachinko cash flow contracts further. Sega Sammy is implicitly betting that the games segment will have grown enough by then — through Sonic’s cross-media economics, Persona’s platform expansion, Like a Dragon’s globalisation, and the UK studio portfolio — to sustain itself, and the consolidated group, on its own profit base. That bet is more credible than it was a decade ago. Whether it is credible enough is the open question.

For foreign companies and investors, Sega Sammy is one of the most accessible large Japanese entertainment groups to partner with on global-IP licensing, cross-media development, and Western-studio collaboration. The global games arm operates with notable institutional autonomy from the Tokyo gambling-machine business, the UK studios have been Western-counterpart-friendly for two decades, and the holding-company leadership has been increasingly explicit about wanting to grow the games segment internationally. The structural awkwardness of the parent group is real; the operational accessibility of the games arm is also real.

FAQ

What does Sega Sammy actually do?

Sega Sammy Holdings is a Japanese entertainment conglomerate formed by the October 2004 merger of Sega Corporation and Sammy Corporation. It operates in four main segments: pachislot and pachinko gambling machines (the historical cash engine), entertainment contents (video games published by Sega and its subsidiary studios), resort operations (notably Paradise City in Incheon, Korea), and other ancillary businesses. It is listed on the Tokyo Stock Exchange under the code 6460.

What games does Sega publish?

Sega publishes the Sonic the Hedgehog franchise (since 1991), the Persona role-playing-game series (through subsidiary Atlus, acquired 2013), the Like a Dragon series formerly known as Yakuza (through Ryu Ga Gotoku Studio in Tokyo), the Total War historical strategy series (through Creative Assembly in the UK), Football Manager (through Sports Interactive in London), Phantasy Star Online 2, and a wider catalogue of mobile and arcade titles.

How does pachinko money relate to Sega games?

Profit generated by Sammy’s pachislot and pachinko-machine business has historically funded a meaningful share of the group’s capital expenditure on game development and intellectual-property investments. The gambling-machine segment has accounted for a large share — often around half — of consolidated operating profit in many post-merger years, and that cash flow has supported the games arm’s development cycles, studio acquisitions, and Western expansion.

Is the pachinko industry really shrinking?

Yes. The Japanese pachinko and pachislot industry has been in long-run decline since its mid-2000s peak, with total gross gaming revenue roughly halving over two decades, the number of parlours roughly halving, and younger Japanese demographics largely uninterested in the format. Regulatory tightening from 2018 onward accelerated the contraction. Sega Sammy has responded by trying to maximise the value of each remaining machine launch and by reweighting the group toward the games segment.

Who runs Sega Sammy?

Hajime Satomi, the founder of Sammy Corporation, engineered the 2004 merger and served as chairman and group CEO for most of the post-merger period. His son, Haruki Satomi, is now president of the holding company and has progressively taken on operational leadership, with a particular focus on growing the global games business. The Satomi family remains a significant shareholder.

Working with Sega Sammy

Japonity helps foreign companies, investors, studios, and intellectual-property holders identify and approach the right counterparts inside Sega Sammy — across game publishing, IP licensing, cross-media collaboration, Western-studio partnerships, and arcade or location-based-entertainment ventures. The operating teams and decision-makers differ substantially between the Tokyo-based Sega and Atlus divisions, the Ryu Ga Gotoku Studio, the UK studios at Creative Assembly and Sports Interactive, and the gambling-machine arm. If you would like a structured introduction, please visit our business matching service.

Related from Japonity — Japan’s gaming, theme parks & entertainment

- Konami Group — The IP factory behind Metal Gear, Silent Hill, Yu-Gi-Oh and eFootball

- Oriental Land — Tokyo Disney’s quasi-Disney and the best licensee deal in entertainment

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →