Sharp Corporation (TSE: 6753) is the Osaka-based consumer-electronics and display-technology company that, since August 2016, has been approximately 66% owned by Taiwan’s Hon Hai Precision Industry — better known by its trade name Foxconn. Founded in 1912 by Tokuji Hayakawa, headquartered in Sakai, and famous for the AQUOS television brand, Sharp is now the most-studied case in modern Japanese business of what a foreign acquirer can — and cannot — do to a wounded national champion.

The company in one paragraph

Sharp makes televisions, smartphones, white goods, business displays, multifunction printers, advanced sensors, and the LCD and OLED panels that go into all of them. Its consumer brand, AQUOS, remains one of the best-known household names in Japan and across parts of Southeast Asia. Its industrial brand sits behind the scenes — in 8K studio cameras, in the digital signage that lines train platforms from Tokyo to Bangkok, and in display modules embedded inside other companies’ products. Around 50,000 people work for Sharp worldwide. Roughly two-thirds of the equity sits with Hon Hai and its affiliates. Operationally, the company has spent the past eight years rebuilding around a smaller, more focused identity than the sprawling electronics conglomerate it was in the 2000s.

From Ever-Sharp pencil to global electronics

The founding story is by now a piece of Japanese industrial folklore. In 1912, a 19-year-old metalworker named Tokuji Hayakawa opened a small workshop in Tokyo. In 1915 he patented the Ever-Sharp mechanical pencil — a propelling-pencil mechanism that gave the company its eventual name. After losing his workshop and his family in the 1923 Great Kanto earthquake, Hayakawa moved to Osaka and rebuilt. The new business pivoted into radios in the 1920s, calculators in the 1960s (Sharp produced one of the world’s first commercial transistor calculators in 1964), liquid crystal displays in the 1970s, and televisions through the 1980s and 1990s.

By the late 1990s, Sharp had bet decisively on liquid crystal display technology, branding its televisions AQUOS in 2001 and pouring capital into massive LCD fabrication plants at Kameyama in Mie Prefecture and later at Sakai in Osaka Prefecture. The Sakai plant, opened in 2009, was at the time the most advanced tenth-generation LCD facility in the world. For a brief moment, Sharp looked like the company that would own the future of the flat-panel television.

The crisis years: 2008-2015

The plan unraveled almost as soon as the Sakai plant came online. The 2008 global financial crisis crushed television demand. Korean rivals Samsung Display and LG Display, backed by patient chaebol capital, scaled faster and cut prices harder. Chinese manufacturers entered the panel market with state-supported balance sheets. By 2012, Sharp was posting losses measured in the hundreds of billions of yen, and the Kameyama and Sakai fabs — engineering triumphs only a few years earlier — had become a strategic liability rather than an asset.

An initial rescue plan was negotiated in March 2012 with Terry Gou’s Hon Hai Precision Industry, under which the Taiwanese contract manufacturer would acquire roughly a 9.9% stake in Sharp for approximately ¥67 billion. The deal collapsed within months as Sharp’s share price fell below the agreed strike price and the two sides could not renegotiate. Sharp limped through three more years of restructuring, asset sales, and emergency credit lines from its main banks — Mizuho and the Bank of Tokyo-Mitsubishi UFJ — before the situation became untenable.

The 2016 acquisition

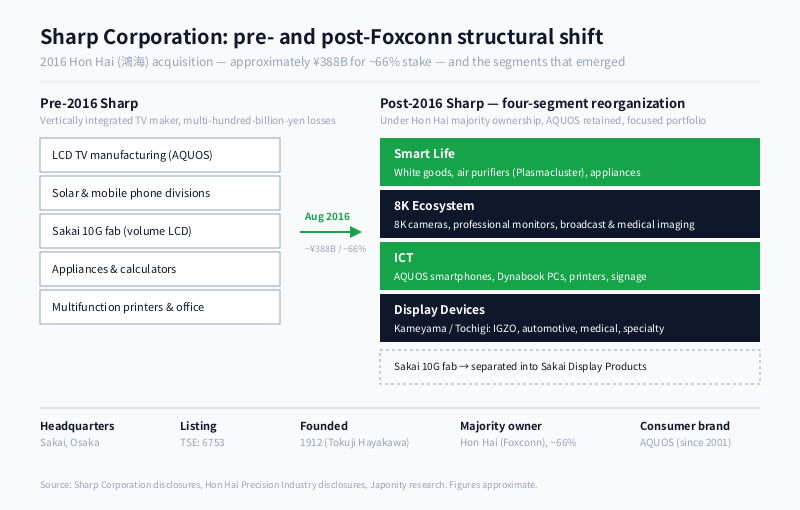

The takeover, when it finally came, was the largest foreign acquisition of a major Japanese electronics maker in history. Negotiations between Hon Hai and Sharp’s board ran from early 2015 through the spring of 2016. The deal nearly fell apart twice — once over disclosure of approximately ¥350 billion in previously unbooked contingent liabilities, and once over voting structure — before being finalized in August 2016. Hon Hai and its affiliates paid approximately ¥388 billion for roughly a 66% stake, with Terry Gou personally taking a position alongside the corporate buyer.

What made the deal historically significant was less the price than the precedent. For decades, the unwritten rule of Japanese corporate distress had been that troubled national champions were rescued by domestic capital — by their main bank, by the Innovation Network Corporation of Japan (a state-backed turnaround vehicle that had bid against Hon Hai for Sharp), by a rival keiretsu, or by a managed merger with another Japanese firm. The Sharp transaction broke that pattern. A foreign acquirer outbid the state-backed vehicle, took majority control of a household-name Japanese electronics brand, and was permitted by regulators and creditors to do so.

Pre-Foxconn versus post-Foxconn: the structural shift

| Dimension | Pre-2016 Sharp | Post-2016 Sharp |

|---|---|---|

| Ownership | Public float, main-bank ties | Approximately 66% Hon Hai & affiliates |

| Strategy | Vertically integrated TV maker | Display-tech licensor + consumer brand |

| LCD posture | Compete head-to-head with Korea | Specialty & 8K niches, exit volume TV panels |

| Capital discipline | Multi-hundred-billion-yen losses | Restored to profitability in most years post-2017 |

| Senior leadership | Career Sharp executives | Robert Wu / Robert Wang and other foreign-installed leaders through the late 2010s |

| Plants | Kameyama, Tochigi, Sakai (under Sharp) | Sakai under Sakai Display Products (separately structured), Kameyama and Tochigi retained |

| Foxconn relationship | Supplier of contract assembly | Parent & co-manufacturer for Sharp-brand products |

The four-segment company today

Sharp under Hon Hai has been reorganized around four operating segments, each with a distinct competitive identity.

Smart Life

This is the consumer white-goods business — refrigerators, washing machines, air purifiers, air conditioners, kitchen appliances, and small home electronics. Smart Life is the part of Sharp most visible to the Japanese household, and it has been the steadiest contributor to group operating profit since 2017. The plasmacluster ion air-purification technology, developed in-house, has been licensed to automotive OEMs and used as a differentiator in the post-pandemic premium-appliance segment.

8K Ecosystem

This segment houses Sharp’s bet that ultra-high-definition video, beyond the now-mainstream 4K, will become a meaningful market in broadcasting, medical imaging, industrial inspection, and surveillance. Sharp manufactures 8K cameras, professional 8K monitors, encoder hardware, and the software stack that ties them together. The market is small and slow-building, but margins are high and competition is thin. NHK’s experimental 8K broadcasting program and Sharp’s 8K studio camera business sit at the center of this segment.

ICT (Information & Communications Technology)

The ICT segment covers smartphones (sold mainly in Japan under the AQUOS brand and in Southeast Asia), tablets, PCs (through the NEC Personal Computers and Dynabook businesses, the latter acquired from Toshiba in 2018), business projectors, multifunction printers, and digital signage. ICT is the segment where the Hon Hai parentage shows most clearly in the operating model: many devices are co-engineered with Foxconn, share Foxconn-managed component supply chains, and are assembled in Foxconn-affiliated factories.

Display Devices

This is the LCD and OLED panel business — the segment that nearly destroyed Sharp in the early 2010s and that has been most aggressively restructured since 2016. The large-format LCD operation at Sakai was separated into Sakai Display Products, a vehicle in which Hon Hai and Terry Gou personally took ownership stakes structurally distinct from Sharp itself. The Kameyama plant produces small and mid-size LCD and IGZO panels, including some volumes that flow into Apple’s iPhone supply chain through Foxconn. The Tochigi plant houses additional display and module operations. Sharp’s strategy here is no longer to win volume but to hold defensible niches — automotive displays, medical displays, 8K professional displays, and ruggedized industrial panels — where its IGZO oxide-semiconductor technology and reliability engineering still command a price premium.

Plants, geography, and the question of Made-in-Japan

Sharp’s manufacturing footprint inside Japan today comprises three principal sites: Kameyama in Mie Prefecture (small and mid-size displays, IGZO panels), Tochigi (display modules and selected electronics), and Sakai in Osaka Prefecture (large-format LCDs under the separately structured Sakai Display Products). A fourth important node is the historic Yao site in Osaka, which houses parts of the appliance and air-conditioner business.

One of the most-debated questions inside Sharp during the post-acquisition years has been how much of its manufacturing should remain physically in Japan versus shifting to Hon Hai’s enormous Chinese and Southeast Asian factory network. The consensus that emerged by the early 2020s — visible in capital allocation rather than in press releases — was that Japan would retain the high-mix, low-volume, high-IP work (8K, automotive panels, premium appliances), while volume consumer products would increasingly be assembled in Foxconn-operated facilities outside Japan. This is the bargain that Hon Hai struck and that Sharp’s management has accepted: keep the brand, keep the R&D, keep the technically demanding manufacturing, and let the rest follow global cost curves.

Governance: what Foxconn changed, and what it did not

After the 2016 closing, Hon Hai installed a slate of senior leaders — Robert Wu and Robert Wang the most visible among them — into board and executive roles at Sharp, with Tai Jeng-wu serving as president through the late 2010s. This was the most aggressive foreign installation of senior leadership at a major Japanese listed company in living memory. By the early 2020s, Japanese executives — including Robert Wu’s successors as CEO, who have been alternately Japanese and Taiwanese — had reclaimed many day-to-day operational roles, but capital allocation, strategic M&A, and the relationship with Foxconn’s contract-manufacturing business continued to be decided in close consultation with Hon Hai’s Taipei leadership.

The governance lesson that other Japanese boards have drawn from the Sharp case is mixed. On one hand, foreign ownership did not destroy the brand — AQUOS televisions, AQUOS smartphones, and Sharp white goods continue to be sold under the same names, in the same retail channels, with broadly the same product positioning. On the other hand, the Sharp of 2026 is materially smaller and more focused than the Sharp of 2010. The vertical integration ambition is gone. The fight for global television market share is gone. The dream of beating Samsung Display on its own ground is gone. What remains is a profitable, focused, mid-sized electronics company — which is, in the end, exactly what Hon Hai paid for.

Why the Sharp case still matters in 2026

Eight years on, the Sharp acquisition continues to be the reference point in every senior-level conversation in Japan about foreign capital and corporate rescue. When Toshiba was broken up. When Hitachi divested its consumer businesses. When the Innovation Network Corporation of Japan and its successor JIC have considered bids for distressed semiconductor or display assets. When private-equity firms — domestic and foreign — circle Japanese listed companies trading below book value. In every one of these conversations, Sharp under Hon Hai is the case study that both sides cite. The bulls cite it as proof that foreign ownership can be productive and disciplined. The bears cite it as proof that the rescued company ends up smaller and less ambitious than it once was. Both are correct, and that is precisely why the case is studied.

For foreign investors, distributors, technology partners, and OEMs considering business with Sharp today, the practical takeaway is straightforward. Sharp is no longer the sprawling, somewhat unpredictable electronics conglomerate of the 2000s. It is a more disciplined, more focused, more capital-aware operation, with deep technological roots in display, sensor, and appliance engineering, and with a parent — Hon Hai — that brings global manufacturing scale most Japanese competitors cannot match. For the right counterparty, that combination is unusually powerful.

FAQ

When did Foxconn acquire Sharp, and how much of the company does it own?

Hon Hai Precision Industry (Foxconn) and its affiliates acquired approximately a 66% stake in Sharp in August 2016 for approximately ¥388 billion, after an earlier 2012 agreement for a smaller minority stake had collapsed. Hon Hai remains the majority shareholder as of 2026.

Is Sharp still a Japanese company?

Sharp remains headquartered in Sakai, Osaka, is listed on the Tokyo Stock Exchange under code 6753, employs the majority of its R&D and senior engineering staff in Japan, and operates its principal display and appliance plants in Mie, Tochigi, and Osaka prefectures. Its majority shareholder is Taiwan-based, but the operating company and the brand are Japanese.

What is the AQUOS brand and is it still active?

AQUOS is Sharp’s flagship consumer electronics brand, launched in 2001 for liquid crystal display televisions. The brand has since extended to smartphones, tablets, and selected appliances, particularly in Japan and Southeast Asia. AQUOS remains Sharp’s most recognizable consumer-facing name.

What does Sharp actually make today?

Sharp’s business is organized into four segments: Smart Life (white goods, air purifiers, kitchen appliances), 8K Ecosystem (ultra-high-definition cameras and monitors for broadcast, medical, and industrial uses), ICT (smartphones, tablets, PCs through Dynabook, multifunction printers, business displays), and Display Devices (LCD and IGZO panels for automotive, medical, and specialty applications).

How can a foreign company partner with or distribute Sharp products?

Sharp operates regional sales subsidiaries across Asia, Europe, and the Americas, and works extensively with distribution and OEM partners. For display panels, business displays, and 8K equipment, partnership is typically handled through its B2B sales organization. For consumer products and appliances, regional distributors are the primary route. Initial introductions for editorial or business-matching purposes can be made through the Japonity platform.

Working with Sharp

Sharp Corporation is one of the most-studied case studies in modern Japanese corporate history, and one of its most operationally interesting consumer-electronics and display-technology companies to engage with. For foreign distributors, technology partners, broadcasters, and industrial buyers exploring Sharp’s display, appliance, 8K, or ICT product lines, Japonity can facilitate editorial coverage and introductions to the right counterparties. Visit our business matching page to begin a conversation.

Related from Japonity — Japan’s electronics & IT services

- Panasonic Holdings — Tesla batteries, airline IFE and consumer appliances under one holdco

- Fujitsu — The PC giant that bet its future on services — Fugaku to Uvance

- NEC Corporation — Defence, biometrics, undersea cable — Japan’s under-appreciated tech infra

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →