Nippon Life Insurance Company — Nissay to almost everyone who deals with it — has been a mutual since the day it was founded in Osaka in 1889 as Japan’s first life insurance company, and it has resisted, for more than a century, the demutualisation wave that pulled Dai-ichi Life onto the Tokyo Stock Exchange in 2010 and reshaped almost every other large global life insurer. The result is a company that manages approximately seventy trillion yen of policyholder assets, that paid roughly two and a half billion US dollars in 2016 to take MassMutual Life Insurance of Japan into its group as Mitsui Life Insurance (later rebranded Taiyo Life — no, that is a different firm; Mitsui Life retained the Mitsui Life name as a Nippon Life subsidiary), and that has quietly become one of the most active Japanese institutional cheque-writers for US private credit, US equity stakes, and Asian growth-equity managers — and yet remains entirely unlisted, with no ticker, no quarterly equity-analyst calls, and no shareholders other than its policyholders.

A mutual that predates the modern Japanese state’s insurance regulator

Nippon Life Insurance Company was founded in Osaka in July 1889 by Sukesaburo Hirose, a former Mitsui Bank executive, as Japan’s first life insurance company. The Insurance Business Law that governs the industry today did not exist; the modern Financial Services Agency would not be created until more than a century later. Nissay’s founding mutual structure — policyholders as economic owners, premium surpluses returned as policyholder dividends rather than distributed to outside shareholders — was a deliberate choice copied from European mutuals of the period, and one that the firm has held onto with unusual stubbornness even as its largest domestic peers chose otherwise.

The company today operates from twin headquarters in Osaka (the historic head office in Chuo-ku) and Tokyo (Marunouchi), with approximately seventy thousand sales representatives — the “seimei reji” channel of mostly female, branch-affiliated agents who remain the dominant distribution force in Japanese life insurance — supported by a corporate-channel and bancassurance footprint that is large by international standards but secondary to the in-person sales force. Total assets under management for the consolidated group sit at approximately seventy trillion yen, making Nissay the largest life insurer in Japan and one of the very largest in the world by general account assets.

What “mutual” actually means in 2026, and why it still matters

A mutual life insurer — sogo kaisha in Japanese, literally “mutual aid company” — has no equity shareholders. Policyholders are simultaneously customers and the residual claimants on surplus. In a stock life insurer, surplus above what is needed for reserves and solvency flows to equity holders as dividends or retained earnings. In a mutual, surplus flows back to policyholders as policyholder dividends, or is retained as foundation funds (kikin) and surplus reserves that strengthen the balance sheet for future generations of policyholders.

The consequences for governance are substantial. Nissay has no quarterly earnings call. Its accounts are public, audited, and detailed, but the operating tempo is set by the firm’s own board and by the Financial Services Agency, not by sell-side analysts. Senior management does not own equity in the firm, because there is no equity to own. Strategic decisions — including the 2016 Mitsui Life acquisition, the gradual build-out of US and European asset-management subsidiaries, and the willingness to commit policyholder capital to long-dated illiquid assets such as private credit and infrastructure — are made on horizons that listed competitors find difficult to match. The disadvantage, equally substantial, is that mutuals cannot raise external equity capital. Growth must be funded from retained surplus or from subordinated debt (kikin chotatsu), and large M&A is correspondingly rare and carefully chosen.

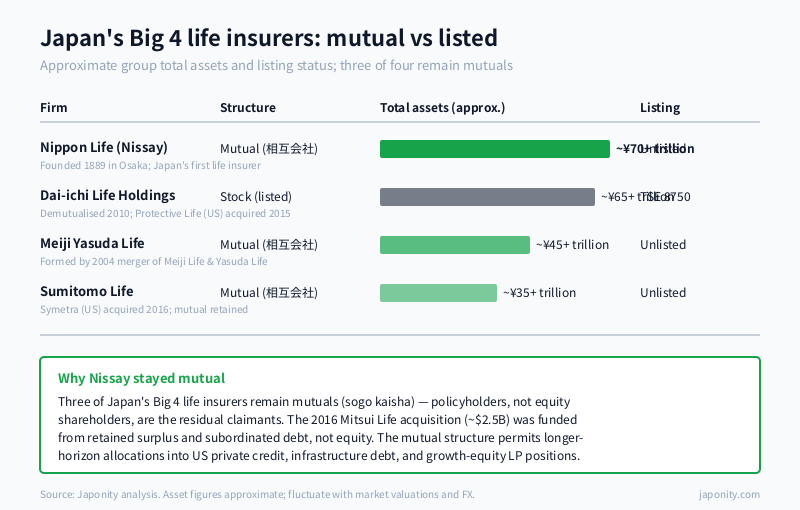

The “Big 4” of Japanese life insurance, and where Nissay sits

Japan’s domestic life insurance market is dominated by four firms whose combined assets account for the majority of the industry: Nippon Life, Dai-ichi Life Holdings, Meiji Yasuda Life, and Sumitomo Life. The four were once structurally similar — all mutuals, all built on a vast in-person sales force, all heavily exposed to Japanese government bonds. Today only two of them are still mutuals. The split is worth seeing clearly:

| Firm | Structure | Approx. total assets | Listing status | Demutualised? |

|---|---|---|---|---|

| Nippon Life Insurance | Mutual (相互会社) | ~¥70+ trillion | Unlisted; no ticker | No — never demutualised |

| Dai-ichi Life Holdings | Stock holding company | ~¥65+ trillion | Tokyo Stock Exchange (8750) | Yes — demutualised 2010 |

| Meiji Yasuda Life | Mutual (相互会社) | ~¥45+ trillion | Unlisted; no ticker | No — formed by 2004 merger |

| Sumitomo Life | Mutual (相互会社) | ~¥35+ trillion | Unlisted; no ticker | No — partial Symetra (US) stake |

The 2010 Dai-ichi Life demutualisation was the most consequential governance event in Japanese life insurance in the post-war period. It produced a listed peer that could raise equity capital, pursue overseas M&A on listed-company timetables, and offer equity incentives to senior managers — advantages that Dai-ichi visibly used in its 2015 acquisition of Protective Life in the US and its subsequent buildup of TAL Dai-ichi in Australia. Nissay watched closely, and chose not to follow. The argument inside the firm, articulated repeatedly by successive presidents, has been that the mutual structure is itself a competitive advantage: it permits longer-horizon asset allocation, it aligns management with policyholders rather than with quarterly equity-market sentiment, and it preserves a brand premium in Japan where trust in long-dated savings products is unusually valuable.

The 2016 Mitsui Life acquisition and the mid-tier consolidation play

In 2015-2016 Nissay completed the acquisition of Mitsui Life Insurance Company from its predecessor parent group for approximately two hundred and fifty billion yen, or roughly two and a half billion US dollars at then-prevailing exchange rates. Mitsui Life had been a mid-tier life insurer with strong corporate-channel relationships through the Mitsui keiretsu, a complementary product mix weighted slightly more toward whole-life and corporate-owned policies than Nissay’s traditional retail base, and a balance sheet of roughly seven to eight trillion yen — material in absolute terms, modest as a percentage of Nissay’s pre-deal book, and exactly the right size to be a strategically meaningful tuck-in without straining the group’s capital position.

The deal had two strategic logics. The first was distribution: Mitsui Life’s corporate-channel presence inside Mitsui-affiliated companies gave Nissay an upgraded route into a segment where it had been competitive but not dominant. The second was capital efficiency: by retaining Mitsui Life as a wholly-owned subsidiary with its own brand rather than fully merging the operating companies, Nissay preserved Mitsui Life’s existing customer relationships, agent network, and corporate-channel goodwill while consolidating asset management, IT infrastructure, and shared services at the group level. Mitsui Life today continues to operate under its own brand as a Nippon Life subsidiary; it is not the same firm as Taiyo Life Insurance (a separate company within the T&D Holdings group). The deal was funded from retained surplus and subordinated debt — not from external equity, which Nissay as a mutual cannot issue — and was the largest piece of mid-tier consolidation in Japanese life insurance in the decade after the Dai-ichi demutualisation.

The asset-allocation revolution: from JGBs to US private credit

For most of the post-war period a Japanese life insurer’s investment portfolio looked like a yield-curve replica: long-dated Japanese government bonds matched to long-dated insurance liabilities, supplemented by domestic equities, real estate, and a thin slice of foreign bonds. The Bank of Japan’s zero-and-negative interest-rate regime, in place in various forms from the late 1990s through the gradual normalisation of 2024-2025, made that allocation increasingly unworkable. Nissay’s response — broadly shared by the rest of the Big 4 but executed earlier and at greater scale at Nippon Life — was to extend duration cautiously, to add foreign credit (initially US Treasuries and US investment-grade corporates with currency hedges), and then, from roughly the mid-2010s onward, to add genuinely illiquid alternatives: US private credit, US and European private equity stakes, infrastructure debt, and selective real-asset positions.

The US private credit allocation has been particularly visible. Through Trino Capital, a US-based investment vehicle, and through direct fund commitments to managers such as Apollo, Ares, and Blackstone, Nissay has become one of the largest single Japanese institutional sources of capital into US senior secured private credit. The firm has also taken minority equity stakes in US and Asian asset managers — pieces in the global build-out of a Nippon Life Asset Management franchise that complements the domestic Nissay Asset Management Corporation — and has been an active limited partner in growth-equity funds across India, Southeast Asia, and Australia. None of this looks like the JGB-heavy portfolio of 2005. Almost none of it would have been possible without the long-horizon flexibility that the mutual structure provides.

The seimei reji distribution machine

The most distinctively Japanese feature of Nissay — and of the Japanese life insurance industry generally — is the sales channel. Approximately seventy thousand sales representatives, the vast majority of them women, work out of branch offices nationwide on a hybrid employment model that combines a modest base salary with substantial commission. They are recruited locally, trained intensively in product knowledge and customer-relationship management, and assigned territories that often correspond to specific corporate workplaces — they sell, in many cases, inside the cafeterias and lobbies of the companies their customers work for. The tenure pattern is bimodal: many representatives leave within the first two years, and those who survive the early period frequently stay for decades, building up books of customers that may include three generations of the same family.

The economics of this channel are not the economics of broker distribution in the US or independent financial adviser distribution in the UK. The Japanese sales representative is closer to a bank branch officer than to a US insurance agent: institutionally embedded, brand-loyal, and supported by a customer-relationship management infrastructure that runs to the largest such databases in Japan outside the megabanks. The channel’s productivity has declined modestly with demographic change and the rise of online direct insurance challengers such as Lifenet Insurance, but it remains the dominant distribution mode for whole-life, endowment, and medical insurance products, and it is one of the principal reasons Nissay’s underwriting margins are structurally higher than its global peers’ on equivalent products.

Hiroshi Shimizu, the Tsutsui legacy, and the governance question

Hiroshi Shimizu became president of Nippon Life Insurance in 2018, succeeding Yoshinobu Tsutsui, who moved to the chairman’s role. Tsutsui’s tenure as president, which had begun in 2011, was defined by the Mitsui Life acquisition, by the early expansion of the alternative-asset allocation, and by the gradual professionalisation of the firm’s overseas investment teams. Shimizu has continued these trends, with additional emphasis on digital transformation of the sales channel, climate-related investment policy (Nissay was an early Japanese signatory to the Net-Zero Asset Owner Alliance), and selective build-out of overseas insurance subsidiaries in Australia, Southeast Asia, and the US.

The governance question that follows Nissay around the international institutional-investor community is straightforward and almost always asked privately: will the firm, at some point, demutualise? The answer, repeatedly and consistently from the current management team, has been no. The argument is that the mutual structure is not a legacy anachronism but a competitive moat — one that aligns the firm with policyholders over multi-decade horizons in a way that a listed life insurer, even one as well-managed as Dai-ichi, cannot. Whether that argument survives the next president, or a future stress event that requires external capital, is one of the open strategic questions of Japanese finance.

What overseas counterparties actually need to know

For foreign reinsurance buyers, asset-management firms, private credit managers, and growth-equity sponsors, Nissay is one of the most consequential institutional counterparties in Japan, and one of the least understood. Three points are worth absorbing before any first meeting.

First, the decision-making cadence is slower and more consensus-driven than at a listed peer, but the resulting commitments are correspondingly larger and longer. A first fund commitment from Nissay typically follows nine to eighteen months of relationship building and operational due diligence, but a successful first commitment routinely leads to a multi-year, multi-fund relationship. Foreign managers who treat Nissay as a transactional one-off tend to leave a great deal of capital on the table.

Second, the mutual structure shapes everything. Senior officers at Nissay are not paid in equity, are not measured against quarterly equity-market metrics, and are accountable, in the final analysis, to a policyholder representative meeting (sodaikai) rather than to a shareholder meeting. Pitches that emphasise short-horizon returns or quarterly mark-to-market volatility tend to land poorly. Pitches that emphasise long-dated risk-adjusted income and alignment with policyholder liabilities tend to land well.

Third, the firm operates with a clear preference for joint ventures, minority equity stakes, and limited-partner relationships rather than full acquisitions, which is partly a function of mutual-company capital constraints and partly a function of governance philosophy. Foreign asset managers seeking distribution into the Japanese institutional market through Nissay should think in terms of strategic minority partnerships and long-dated mandates rather than in terms of one-off transactions.

FAQ

Is Nippon Life Insurance listed on any stock exchange?

No. Nippon Life Insurance Company is a mutual company (相互会社, sogo kaisha) organised under Japan’s Insurance Business Law. It has no equity shareholders and is owned, in economic terms, by its policyholders. There is no Tokyo Stock Exchange listing, no overseas listing, and no ticker symbol. The firm’s financial accounts are publicly disclosed and audited, but it does not hold quarterly equity-analyst earnings calls in the way that Dai-ichi Life Holdings, its demutualised peer, does.

How large is Nippon Life compared to Dai-ichi Life and Meiji Yasuda Life?

Nippon Life is the largest of Japan’s “Big 4” life insurers by total assets, with approximately seventy trillion yen on a consolidated basis. Dai-ichi Life Holdings follows at approximately sixty-five trillion yen, Meiji Yasuda Life at approximately forty-five trillion yen, and Sumitomo Life at approximately thirty-five trillion yen. All figures are approximate and fluctuate with market valuations and exchange-rate movements; rankings between Nippon Life and Dai-ichi Life by some sub-metrics are close, but Nissay has remained number one by group general-account assets for the entire post-war period.

What did Nippon Life pay for Mitsui Life Insurance, and is the deal still in place?

Nippon Life acquired Mitsui Life Insurance Company in 2015-2016 for approximately two hundred and fifty billion yen, or roughly two and a half billion US dollars at then-prevailing exchange rates. The transaction was the largest piece of mid-tier consolidation in Japanese life insurance during the 2010s. Mitsui Life today continues to operate under its own brand as a wholly-owned Nippon Life subsidiary, with its own sales channel and corporate-customer relationships preserved, while back-office, IT, and asset-management functions have been progressively consolidated at the Nippon Life group level. Mitsui Life is not the same company as Taiyo Life Insurance, which sits within the separate T&D Holdings group.

How does Nippon Life’s investment portfolio differ from its listed peers?

Nippon Life’s general account portfolio remains anchored in long-dated Japanese government bonds and domestic corporate credit, but the firm has been one of the most active large Japanese institutional buyers of US private credit, US and European private equity, infrastructure debt, and minority stakes in US and Asian asset managers. The firm operates Trino Capital as a US investment vehicle and is an active limited partner in multiple US and European private-markets fund families. The mutual structure permits longer-horizon, more illiquid allocations than a listed life insurer would typically run; portfolio illiquid-asset shares at Nissay are at the higher end among Japanese Big 4 peers.

Why does Nippon Life still rely so heavily on in-person sales representatives?

Approximately seventy thousand sales representatives — the seimei reji channel, mostly female, branch-affiliated — remain the dominant distribution mode for whole-life, endowment, and medical insurance products in Japan. The channel is unusually productive by international standards because it is institutionally embedded inside Japanese corporate workplaces, supported by long-tenure customer relationships, and complemented by a customer-relationship management infrastructure that is among the largest in Japan outside the megabanks. Online direct insurance has grown but remains a small share of the overall market for the long-dated, advice-led products that anchor Nissay’s underwriting margins.

Working with Nippon Life

For overseas reinsurance buyers, asset managers, private credit and private equity sponsors, infrastructure-debt platforms, and growth-equity firms, the practical entry points to Nippon Life are distinct: institutional asset-management mandates run through Nissay Asset Management Corporation and its overseas affiliates; private-markets and US private credit relationships are typically intermediated through the group’s overseas investment teams and Trino Capital; reinsurance relationships sit inside the insurance operating company; and strategic minority equity partnerships into asset managers are negotiated at the group corporate-development level. Each of these is a separate first conversation, with its own senior contacts and its own decision tempo.

Beyond Nissay itself, the broader ecosystem of Japanese life insurers — Dai-ichi Life Holdings, Meiji Yasuda Life, Sumitomo Life, T&D Holdings, and a long tail of mid-tier and bancassurance-affiliated firms — together represents one of the largest pools of institutional capital in the world, and remains structurally under-served by foreign managers who do not have a Tokyo or Osaka presence. The mutual-company subset of that ecosystem, in particular, is rarely covered in the English-language financial press and is not reachable through standard institutional-investor sales channels.

If your firm is exploring a Japanese institutional mandate, a US private-credit or private-equity limited-partner relationship with a Japanese life insurer, a reinsurance treaty with a Big 4 Japanese life carrier, or a strategic minority partnership into a Japanese asset manager — Japonity’s business matching service can help structure a credible first conversation with the right team in Osaka or Tokyo.

Related from Japonity — Japan’s life insurers

- Dai-ichi Life Holdings — Japan’s largest listed life insurer — Protective Life US, TAL Australia

- Meiji Yasuda Life — Japan’s #3 life insurer — mutual holdout, StanCorp US

- Sumitomo Life Insurance — Japan’s #4 life insurer — the third mutual holdout + Symetra US

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →