In March 2015, the most famous video game director in Japan was reportedly barred from collecting his own lifetime-achievement award. Hideo Kojima, creator of Metal Gear and the public face of Konami for nearly three decades, had just been quietly stripped of his title on the company’s marketing materials. By the end of the year he was gone — taking his studio, his colleagues, and his next blockbuster (Death Stranding) into independence under Sony’s patronage. Almost a decade later, in October 2024, Konami shipped Silent Hill 2 Remake — a reverent reconstruction of a 2001 cult classic that the company itself had let lie dormant for over a decade. It became one of the most warmly received Japanese games of the year. In the same window, Metal Gear Solid Δ: Snake Eater — a remake of Kojima’s 2004 masterpiece, built without him — moved into final production. And quietly, in the background, the Yu-Gi-Oh! Trading Card Game crossed an estimated 35 billion cards sold globally, the best-selling TCG in human history by Guinness’s reckoning. This is the paradox of Konami Group Corporation (TSE: 9766): a publisher whose relationships with its star creators are the most fractious in Japanese gaming, whose flagship football franchise lost the FIFA license and stumbled into a calamitous 2021 relaunch, and which nevertheless sits on an IP vault, a pachislot cash engine, and a fitness-club portfolio that together produce among the steadiest operating margins in the sector. The question, in 2026, is no longer whether Konami can survive without its auteurs. It is whether the company’s system — IP factory plus diversified cash flows — is in fact the more durable model.

From Osaka jukebox rental to Tokyo IP conglomerate

Konami’s origin story is one of the strangest in Japanese entertainment. The company was founded in March 1969 in Osaka by Kagemasa Kozuki as a jukebox rental and repair business — the name a portmanteau of the founders’ surnames. Within four years it had pivoted into arcade-game manufacturing, and by the early 1980s it was producing some of the era’s defining coin-op hits, including Frogger (1981) and Track & Field (1983). The Famicom and arcade booms of the late 1980s and early 1990s transformed Konami into one of Japan’s “big four” third-party game publishers alongside Capcom, Namco, and Square. It listed on the Tokyo Stock Exchange in 1988, relocated its headquarters to Tokyo’s Roppongi district, and by 2000 was the architect of franchises — Metal Gear, Silent Hill, Castlevania, Pro Evolution Soccer, Powerful Pro Yakyu, Yu-Gi-Oh!, the BEMANI music-game family — that would define an entire generation of console and arcade play.

What sets Konami apart from its peers is what happened next. Where Capcom doubled down on developer-led franchise resuscitation (Resident Evil, Monster Hunter), where Bandai Namco built an anime-IP licensing machine, and where Sega Sammy fused console publishing with pachislot manufacturing, Konami chose a third path: diversification into adjacent leisure businesses — fitness clubs, casino gaming systems, and pachislot — that buffered the volatility of its software pipeline. The company was renamed Konami Group Corporation in 2022 (from Konami Holdings), a rebrand intended to signal the conglomerate’s evolution beyond games. Today, founder Kagemasa Kozuki remains chairman; his son Takuya Kozuki sits on the board, and the day-to-day leadership has passed to a professional management cadre. The Kozuki family retains a substantial founding stake.

The IP vault: a portfolio that rivals any publisher in the world

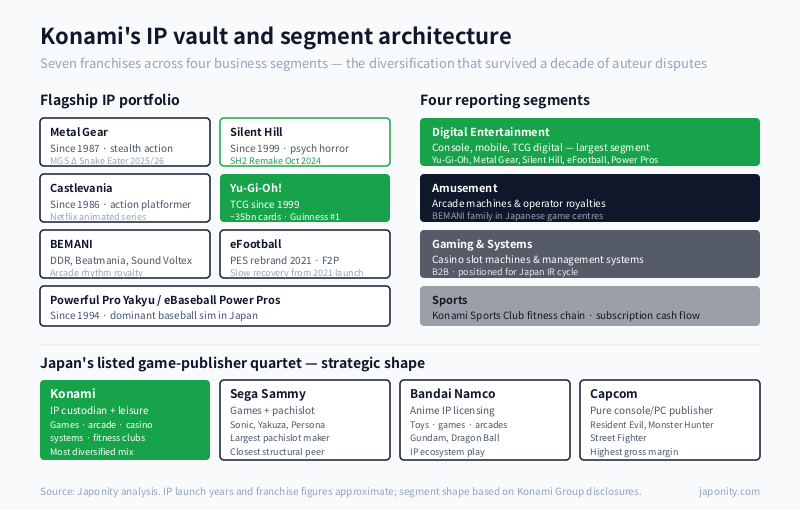

To understand why Konami’s chaotic creator relationships have not destroyed the company, look at the catalogue. Metal Gear, launched in 1987 and reborn as a 3D stealth franchise with Metal Gear Solid in 1998, is among the most critically lauded series in gaming history. Silent Hill, debuting in 1999, defined the psychological-horror genre. Castlevania, running since 1986, produced one of the genre-defining “Metroidvania” titles in Symphony of the Night (1997) and later inspired a successful Netflix animated series. The Bemani family — Dance Dance Revolution, Beatmania, Pop’n Music, Sound Voltex — created the modern rhythm-game category. Powerful Pro Yakyu (“Power Pros”) has been the dominant baseball simulation in Japan for three decades. And Pro Evolution Soccer, rebranded as eFootball in 2021, was for years FIFA’s only credible challenger on console.

Then there is Yu-Gi-Oh!. Launched as a Trading Card Game in 1999 in Japan and 2002 globally, it has sold an estimated 35 billion cards worldwide — recognised by Guinness World Records as the best-selling TCG ever. Unlike the boom-bust cycle of console releases, the TCG generates recurring annual revenue through booster pack sales, organised play, and digital adaptations (Yu-Gi-Oh! Master Duel, launched 2022, has been downloaded approximately 80 million times). The card business alone, bundled inside Konami’s Digital Entertainment segment, is widely understood to be one of the company’s most profitable lines.

The breadth matters because it insulates against any single franchise stumbling. When eFootball launched disastrously in September 2021 — patches needed, reviews scathing, ratings near historic lows for a AAA release — the share price wobbled but did not crater, because Yu-Gi-Oh!, Bemani arcade royalties, Power Pros, and the broader leisure businesses absorbed the shock.

The Kojima split and what it really meant

The defining episode of modern Konami is the 2015 rupture with Hideo Kojima. The public account is by now well established: production of Metal Gear Solid V: The Phantom Pain ran heavily over budget and over schedule; Kojima’s name was removed from the box art; the studio Kojima Productions was reportedly partitioned off from the rest of the company; and in December 2015 Kojima departed to set up an independent Kojima Productions, signing with Sony for Death Stranding (released 2019).

Konami’s official position has always been more restrained than the fan narrative — the company has consistently said it remains open to working with external talent and that it did not “ban” Kojima from receiving his award. But the substantive fact is undeniable: Konami parted with the most celebrated game designer in the country, and then spent nearly a decade with no major Metal Gear title in development. The 2018 zombie spin-off Metal Gear Survive underperformed and was widely seen as confirmation that the franchise had lost its directing intelligence.

The Kojima split was not the only fracture. Castlevania‘s creative lead Koji Igarashi departed in 2014 and successfully Kickstarter-funded the spiritual successor Bloodstained. Silent Hill‘s ambitious next entry Silent Hills — being developed by Kojima with film director Guillermo del Toro and actor Norman Reedus, with a celebrated “P.T.” playable teaser — was cancelled in 2015 in the wake of the Kojima rupture. For roughly a decade, Konami was a publisher with one of the strongest IP libraries in the industry and almost no flagship development to show for it.

What Konami did instead was pivot to a model that gaming analysts now sometimes call the “IP custodian” approach: license and outsource development of legacy franchises to trusted external studios, while the in-house teams concentrate on the live-service and recurring-revenue lines (Yu-Gi-Oh, Bemani, Power Pros, eFootball).

The 2024-2026 revival: outsourced, reverent, methodical

The pivot bore fruit in October 2024 with Silent Hill 2 Remake, developed by Polish studio Bloober Team under Konami’s supervision. The release was a critical and commercial success, restoring the franchise’s reputation after more than a decade of dormancy. Around it Konami announced an entire Silent Hill revival programme: a new mainline entry Silent Hill f, a film adaptation directed by Christophe Gans, and additional projects from external partners.

Metal Gear Solid Δ: Snake Eater — a from-the-ground-up remake of Metal Gear Solid 3 (2004), generally regarded as Kojima’s finest entry in the series — entered final development for release in 2025/2026 across PlayStation 5, Xbox Series X|S, and PC. Critically, Konami is shipping it without Kojima’s involvement; the remake is being built by an in-house team alongside external partners, in a deliberate test of whether the company can stand on the IP’s foundations alone. A Metal Gear Solid: Master Collection bundling the older entries was released in 2023.

Behind these flagship returns, Yu-Gi-Oh! Master Duel continues to compound. The eFootball recovery has been slow but tangible — successive patches, free-to-play model refinement, mobile growth — though FIFA’s departure (now EA Sports FC) has not been recovered as a license. And Powerful Pro Yakyu and its sister title eBaseball Powerful Pro Baseball remain dominant in Japan.

Segments: how the conglomerate actually makes money

Konami reports across four primary business segments. The breakdown reflects the diversification thesis: console and mobile games are large but volatile; the gaming-and-systems (casino), amusement (arcade), and sports (fitness clubs) businesses provide the ballast.

| Segment | What it includes | Strategic role |

|---|---|---|

| Digital Entertainment | Console and mobile games: Yu-Gi-Oh, Metal Gear, Silent Hill, Castlevania, eFootball, Power Pros, Master Duel | Largest revenue contributor; highest-volatility line; long-tail IP licensing |

| Amusement | Arcade machines and revenue-share: Bemani family (DDR, Beatmania, Sound Voltex, Pop’n Music), arcade card games | Steady recurring revenue from operator royalties; cultural moat in Japanese game centres |

| Gaming & Systems | Casino slot machines and casino-management systems (international markets, particularly North America and Asia-Pacific) | B2B revenue with long contract cycles; expanding ahead of Japanese integrated-resort openings |

| Sports | Konami Sports Club fitness chain across Japan; sports-related services | Subscription cash flow; counter-cyclical to game-release cadence |

The Digital Entertainment segment is by far the largest by revenue, but the others are the reason Konami’s operating margin has remained comfortably positive even in years of weak software releases. The pachislot business — operated through a subsidiary — generates substantial cash that is often re-invested into IP development. In aggregate, Konami’s operating margin has typically run in the mid-to-high teens, a figure that compares favourably with most international games publishers.

The competitive frame: Konami versus the other Japanese majors

Konami occupies an unusual position among Japanese listed entertainment groups. Its closest analogues — each operating a different blend of console publishing, arcade and amusement, and adjacent leisure — illustrate the divergent strategies the sector has pursued.

Capcom is the purest console-and-PC publisher, leaner in headcount, with a tighter franchise portfolio (Resident Evil, Monster Hunter, Street Fighter) and the highest gross margin in the sector. Bandai Namco is an IP-licensing colossus, leveraging anime, toys, and games into an integrated entertainment ecosystem. Sega Sammy combines console games (Sonic, Yakuza/Like a Dragon, Persona via Atlus) with a much larger pachislot and amusement business — closer in structural shape to Konami than to Capcom.

The instructive comparison is not who has the best year, but who has the most defensible cash flow over a decade. By that measure, Konami’s deliberate de-risking through fitness clubs, gaming systems, and TCG annuity revenue is closer to Sega Sammy’s pachislot-and-games hybrid than to Capcom’s pure-play software model. The trade-off: lower upside from a console blockbuster cycle, but lower drawdowns when one falters.

What 2026 tells us about the strategy

Three signals from the current cycle are worth tracking. First, the Silent Hill and Metal Gear revivals are both being executed through a hybrid in-house / external-studio model. If Metal Gear Solid Δ succeeds critically and commercially without Kojima, it will be the strongest validation yet of the IP-custodian thesis — the idea that, with sufficient reverence and craft from a partner studio, Konami’s IP value is not dependent on the original auteurs. If it underperforms, the case for a more developer-centric model gets a fresh hearing.

Second, the Japanese integrated-resort (IR) opening — most prominently in Osaka, targeted for 2030 — is a multi-decade tailwind for the Gaming & Systems segment. Konami is one of a small number of global suppliers of casino slot machines and casino-management systems with the engineering depth and regulatory track record to win serious IR contracts. The investment cycle for those contracts begins well before opening day.

Third, the Yu-Gi-Oh! ecosystem continues to defy expectations. A 27-year-old card franchise that grew through paper, then digital, then esports, then short-form video on TikTok and YouTube, is a rare example of an IP that has compounded across every consumer-technology transition. Konami’s stewardship of the property — measured global event calendar, careful card-power balance, ongoing digital reinvestment — is a quieter story than the Kojima split, but is arguably the more important one for the company’s long-term value.

The verdict: a company that learned to live without auteurs

The dominant story about Konami for a decade was the auteur question — could a games publisher that loses or alienates its most creative directors really thrive? The 2024-2026 cycle is delivering a tentative answer: yes, provided the IP vault is deep enough and the surrounding businesses provide enough ballast to fund a careful, outsourced revival. Konami is not the most beloved games publisher in Japan, and inside the developer community its reputation remains contested. But by the metrics that matter to a listed conglomerate — diversified revenue, durable margin, IP value compounding through digital adaptations and global card sales — it has constructed one of the more resilient business models in the sector. The IP factory has learned to fight even with its own developers, and to keep shipping anyway.

FAQ

Why did Hideo Kojima leave Konami?

The departure followed production tensions during Metal Gear Solid V: The Phantom Pain (2015), which ran significantly over budget and schedule. Kojima’s name was removed from marketing materials, his studio was reportedly reorganised, and he formally left at the end of 2015 to establish an independent Kojima Productions backed by Sony. Konami has consistently said it remains open to working with external creative partners.

Is the Silent Hill franchise being revived?

Yes. Silent Hill 2 Remake, developed by Polish studio Bloober Team, was released in October 2024 to strong critical and commercial reception. Konami has additionally announced a new mainline entry (Silent Hill f), a film adaptation, and further projects with external partners. The franchise had been largely dormant from approximately 2012 until the 2024 revival.

How big is the Yu-Gi-Oh! Trading Card Game?

Approximately 35 billion cards have been sold globally since launch, making it the best-selling Trading Card Game in history according to Guinness World Records. The digital companion Yu-Gi-Oh! Master Duel, released in 2022, has been downloaded approximately 80 million times. Together they represent one of Konami’s most profitable franchise lines.

What happened to Pro Evolution Soccer and the FIFA license?

Pro Evolution Soccer was relaunched as the free-to-play eFootball in September 2021 and suffered a difficult launch with widespread quality criticism. Separately, EA Sports lost the FIFA naming license and rebranded as EA Sports FC from 2023. eFootball has recovered gradually through successive patches and continues as Konami’s flagship football title.

Why does Konami operate fitness clubs and casino-machine businesses?

The diversification provides counter-cyclical cash flow against the volatility of game-release cycles. Konami Sports Club generates subscription revenue largely independent of software launches, while the Gaming & Systems segment (casino slot machines and management systems) carries long B2B contract cycles. Together they help stabilise the consolidated operating margin and fund IP-development investment during slower release years.

Working with Konami

For licensing partners, casino-system integrators, esports organisers, retail and TCG distribution partners, and brand-collaboration teams looking to engage with Konami Group Corporation or its operating subsidiaries, Japonity’s business-matching team can help structure introductions and outline practical next steps. Visit /business-matching/ to begin.

Related from Japonity — Japan’s gaming, theme parks & entertainment

- Sega Sammy Holdings — Pachinko cash funding Sonic, Persona and Like a Dragon

- Oriental Land — Tokyo Disney’s quasi-Disney and the best licensee deal in entertainment

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →