For most of the last six years, the global top of YouTube Super Chat earnings — money sent by viewers during livestreams — has been dominated by Japanese VTubers, not Korean streamers or American gaming celebrities. The two companies behind most of that wave, ANYCOLOR Inc. (operator of Nijisanji) and COVER Corp. (operator of Hololive Production), are both listed on the Tokyo Stock Exchange, have posted multi-billion-yen operating profits, and have built repeatable agency businesses that resemble a fusion of music label, talent agency and game studio more than anything in the Western influencer economy. This is the B2B brief overseas marketers, advertisers, investors and talent agencies should be reading. For background, see Japonity’s previous coverage of ANYCOLOR.

Two listed champions: ANYCOLOR and Cover

The VTuber industry is plural — there are dozens of agencies in Japan, ranging from one-person production units to mid-sized labels — but the public-market story is a duopoly.

ANYCOLOR Inc. (TSE Growth: 5032), founded in 2017 as Ichikara Inc., rebranded in 2021 and listed on TSE Growth in June 2022, operates Nijisanji, launched in 2018 with a then-novel proposition: lower the technical bar for entry by issuing 2D Live models rather than custom 3D rigs, and scale the talent roster aggressively. Its roster across Japan and overseas branches has at various points exceeded 150 active talents — a scale no other operator has matched — and the company’s revenue is reported in the tens of billions of yen annually, with operating margins consistently above 25 per cent.

COVER Corp. (TSE Growth: 5253), founded in 2016 and listed on TSE Growth in March 2023, operates Hololive Production. Cover’s positioning has been the opposite of Nijisanji’s: a smaller, more curated roster (typically 80 to 100 active talents across regions), heavier investment in proprietary 3D motion-capture stages, original music and large-scale live events. Annual revenue ranges in the tens of billions of yen, and the company has been profitable since its IPO, with merchandise and live-event revenue carrying disproportionate weight in the mix.

Between them, ANYCOLOR and Cover account for the overwhelming majority of the institutional VTuber economy. VShojo, Brave Group, Noripro, 774 inc. and Riot Music form the long tail with niche audiences and different revenue mixes.

The revenue mix: where the money actually comes from

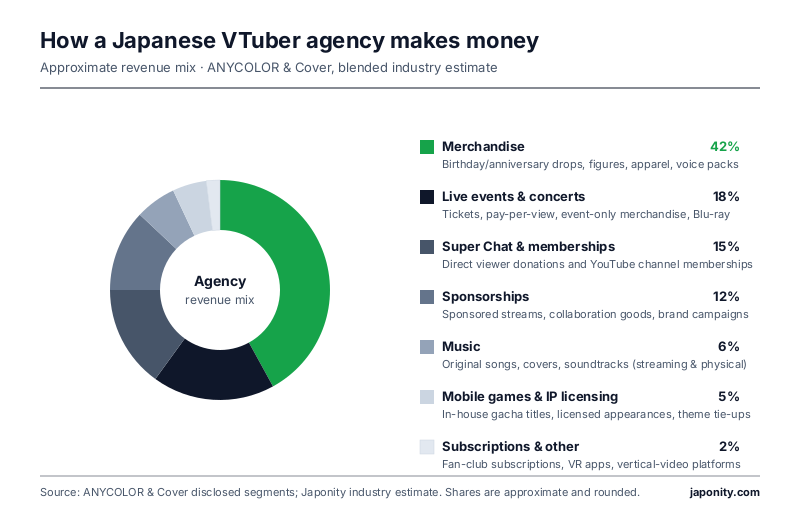

Western marketers approaching VTuber agencies for the first time tend to assume the business is YouTube ad revenue plus brand deals — the influencer-economy default. It is not. Disclosed segment data from ANYCOLOR’s and Cover’s filings, with industry estimates from Oricon and Anime Industry Report sub-trackers, paints a different picture.

| Revenue stream | Approx. share of agency revenue | Notes |

|---|---|---|

| Merchandise (physical & digital) | ~38–45% | Limited-edition birthday/anniversary “voice packs”, figures, acrylic stands, apparel, drop-shipped via Geekjack and BOOTH |

| Live events & ticketed concerts | ~15–20% | Solo concerts, group lives, arena events; ticketing + live-stream pay-per-view + merchandise tail |

| YouTube Super Chat & memberships | ~12–18% | Direct viewer payments during livestreams; channel memberships; YouTube takes ~30% |

| Sponsorships & brand collaborations | ~10–15% | Brand sponsorships, product placement streams, collaboration goods with consumer brands |

| Music (streaming, downloads, physical) | ~5–8% | Original songs, covers, soundtracks; Spotify, Apple Music, physical CD sales in Japan |

| Mobile games & IP licensing | ~5–8% | In-house and licensed mobile games, character licensing to third-party titles, gacha mechanics |

| Subscription apps & other | ~2–5% | Fan-club subscriptions, VR apps, vertical-video platforms |

Three observations matter for outside buyers. First, merchandise is the engine, not livestream donations. A single popular VTuber’s birthday merch drop can gross several hundred million yen in 72 hours — limited print run, high margin, near-zero unsold inventory because demand is pre-aggregated through fan signal. This is closer to the K-pop “comeback album” economy than to Twitch streamer merch.

Second, live events are increasingly the highest-leverage product. A Hololive solo concert at Pacifico Yokohama or a Nijisanji group live at Saitama Super Arena combines ticket revenue (¥8,000–¥15,000), pay-per-view streaming (¥4,000–¥7,000), event-only merchandise (¥3,000–¥30,000 per attendee) and post-event Blu-ray sales. Margins are higher than on equivalent K-pop concerts because the venue and motion-capture stage are amortised across dozens of events. Third, Super Chat is a marketing lighthouse, not a profit centre. After YouTube’s ~30 per cent platform cut and the agency-talent split, the agency keeps roughly a third of the gross. The headline rankings drive coverage, but they are rarely the largest line on the P&L.

Talent economics: the split, the debut, the graduation

The agency-talent revenue split varies, is private, and is the single most negotiated term in the industry. Practitioners describe a typical structure in bands. On Super Chat and memberships, the split favours the talent — frequently 60/40 or 70/30 in the talent’s favour, after YouTube’s platform fee. On merchandise produced and warehoused by the agency, the split is closer to 50/50 or weighted toward the agency because production capital and inventory risk sit with the company. On sponsorships, talents typically receive a fixed appearance fee and the agency books the deal margin. On music and live events, the agency captures the majority because rights, recording, choreography and 3D stage infrastructure are agency-owned.

The debut process is structurally similar to the K-pop trainee pipeline, compressed in time. Agencies receive thousands of auditions per generation; candidates are screened on voice, personality, streaming aptitude and the ability to sustain a daily-streaming schedule under a managed character identity. Successful candidates receive a custom 2D Live model (commissioned art plus rigging, typically ¥3–¥8 million per model at top-tier agencies), voice training, a streaming setup, and a managed debut over four to six weeks. The economics work because a single successful talent generates revenue at a multiple of their model production cost within months.

“Graduation” is the industry’s term for talent retirement, and one of its most distinctive features. Unlike Western influencer agencies, which expect creators to continue indefinitely, VTuber agencies operate under the explicit assumption that talents will eventually exit. The graduation event is itself a monetisable product: farewell streams routinely generate Super Chat in the tens of millions of yen, and graduation-edition merchandise is among the highest-margin drops an agency produces. The model is, counter-intuitively, healthier for fan retention than a forced-continuity model.

The agency moat: why DIY does not scale

An obvious investor question is: why don’t talents simply go independent? The talent owns the audience, after all. The answer is that the agency-scale model has accumulated three durable barriers to entry.

The first is 3D infrastructure. A Hololive or Nijisanji solo concert requires a custom 3D model, an Xsens or OptiTrack motion-capture stage with operators, real-time rendering and a stage director. Cover’s investment in proprietary capture studios runs into the billions of yen. An independent VTuber cannot replicate that, and audiences are unforgiving of lower-fidelity alternatives.

The second is IP development capacity. Original music, mobile games, collaboration goods and outside licensing require a full production stack: songwriters, composers, animators, game developers, licensing lawyers. ANYCOLOR and Cover both ship multiple music releases per month and at least one collaboration drop per week. That cadence is not replicable by an individual or a five-person studio.

The third is cross-promotion network effects. A new debut into Hololive or Nijisanji is introduced to an audience numbering in the millions via co-streams, group videos and event appearances. An independent must build that audience from a cold start. The cost of acquiring the first 100,000 subscribers is the largest hidden line item in independent VTubing — and the one the agency model effectively socialises.

The international expansion playbook — and its failure modes

Both ANYCOLOR and Cover have run multi-year international expansion programmes — Nijisanji EN, Nijisanji KR (later consolidated), Nijisanji ID (later wound down), hololive English, hololive Indonesia. Collectively, more than 100 non-Japanese-language talents have been debuted. The playbook is consistent: localise the agency-quality production stack, recruit near-native English/Indonesian/Spanish-speaking talents, give them access to the cross-promotion network, and route their revenue share through the parent’s compliance structure.

It has worked unevenly. Hololive English has produced individual talents whose subscriber counts rival the top Japanese names. Nijisanji EN has had commercial success but also experienced public talent disputes that in 2024 materially affected ANYCOLOR’s share price. The model exports cleanly where there is an existing anime audience, English-fluent voice performers comfortable with daily long-form streaming, and labour law that accommodates the agency-talent contract. It exports poorly where local markets expect creator-led ownership of channels and IP, where platform economics differ materially (China’s separate ecosystem), or where cultural norms around character roleplay diverge from Japan. For foreign investors, the second wave of expansion will be slower and more selective than the first.

The brand-collaboration opportunity for foreign sponsors

This is where inbound interest is rising fastest. A foreign brand can sponsor a Japanese VTuber stream, commission a collaboration video, license character likeness, or co-develop limited-edition merchandise. The mechanics in rough outline:

- Sponsored stream: A two-to-three-hour stream playing the brand’s game, reviewing the product or running a campaign format. Fees range from low seven figures to mid-eight figures of yen depending on talent tier. Lead time: 4–8 weeks.

- Collaboration merchandise: Joint-branded goods (apparel, beverages, snacks, cosmetics). Typically a 6–9 month development cycle. Margin-share negotiated case by case. Lawson, FamilyMart, Bushiroad and McDonald’s Japan collaborations are the visible references; foreign brands are increasingly admitted to the same workflow.

- Original character commission: The brand commissions an agency to develop a VTuber persona under licence. Rare, expensive, typically pursued only by very large rights-holders such as global gaming publishers.

- Event sponsorship: Title sponsorship of an arena live or pay-per-view event. Nine-figure yen budgets, but with the broadest reach and the strongest media tail.

The agency-side gatekeeping is meaningful. Both ANYCOLOR and Cover have business-development teams that filter inbound enquiries against brand-safety and talent-fit constraints. Foreign brands without a Japanese counsel and a local marketing agency rarely advance past initial enquiry. A credible Japanese partner is, in practice, a precondition.

Risks: what could break this

The bull case is straightforward — overseas audiences, merchandise scaling, expanding live events, growing brand-sponsor budgets. Four risks are worth pricing in.

Talent churn. The 2024 disputes inside Nijisanji EN are not idiosyncratic. The contract structure, while well-suited to scaling rosters, creates recurring friction around revenue splits and channel ownership. Both companies have revised contracts and added HR investment, but the issue is structural.

Platform dependency. Roughly 80–90 per cent of agency video and Super Chat revenue routes through YouTube. A material change in YouTube’s monetisation policy or revenue-share terms would propagate directly to agency P&L. Diversification toward in-house apps and proprietary fan platforms is real but slow.

Demographic ceiling. The core VTuber audience in Japan skews to men aged 15–34, a shrinking cohort. International expansion partially offsets this, but both companies’ Japan-only audiences will be smaller in absolute terms by 2030 than today.

China’s separate ecosystem. Bilibili hosts a large, parallel Chinese VTuber economy without Japanese agency participation. Cover and ANYCOLOR exited active China operations in 2020–2021. China is neither upside surprise nor downside risk in the way it is for the broader anime industry; it is simply absent from the model.

2026–2030 outlook

The base case is continued mid-teens revenue growth at both listed operators, rising merchandise and live-event share of the mix, gradual maturation of international branches, and steady foreign brand-collaboration spend. The bull case adds a meaningful second platform (a vertical-video channel, a proprietary subscription product, or a successful mobile-game franchise) and improved overseas live-event economics. The bear case is talent churn that compresses roster size, or a YouTube policy change that resets unit economics. None of the three cases ends with VTubing returning to a hobbyist niche. The infrastructure is too built out, and the audience too large, for that reversion to happen quickly.

Frequently asked questions

How big is Japan’s VTuber industry by market size?

Industry estimates put the Japanese VTuber market — agency revenue plus related goods, events, mobile games and brand-collaboration spend — at roughly ¥80–120 billion annually as of 2024, with double-digit growth. ANYCOLOR and Cover account for the majority of the institutional segment. Including independents, regional agencies and brand spend captured by adjacent platforms, the total footprint is meaningfully larger.

What is the VTuber business model, briefly?

A talent agency that develops branded virtual personas (2D and 3D animated avatars), debuts them on YouTube and other streaming platforms, and monetises across multiple revenue lines — merchandise, live events, Super Chat and memberships, sponsorships, music and mobile games. Merchandise and live events together typically account for more than half of agency revenue, with Super Chat a high-visibility but secondary line.

How do ANYCOLOR (Nijisanji) and Cover (Hololive) compare?

ANYCOLOR (TSE: 5032) operates Nijisanji, a larger roster with lower per-talent production cost and heavier emphasis on streaming volume. Cover (TSE: 5253) operates Hololive Production, a smaller, more curated roster with heavier investment in 3D infrastructure, original music and live events. Both are TSE Growth-listed and consistently profitable. Cover skews more toward merchandise and live events; Nijisanji captures more streaming volume and Super Chat share — but the overall model is the same.

How can a foreign brand collaborate with a VTuber?

The four common formats are sponsored streams (low seven figures to mid-eight figures of yen), collaboration merchandise (6–9 month development cycle), original character commissions (rare, expensive) and event sponsorships (nine-figure budgets). The agency-side business development team gates all inbound enquiries, and a credible Japanese counsel or production partner is in practice a precondition for advancing past initial contact. Lead times for top-tier talents are 4–8 weeks for sponsored streams and substantially longer for merchandise and events.

Why does the Western influencer economy not look like this?

Three structural reasons. Western platforms emphasise creator-owned channels and direct creator-to-brand deals, limiting the agency role. Western audiences are less accustomed to digital tipping or premium personality merchandise, compressing the per-fan base. And Western live-event production is not structured around motion-capture concerts; the infrastructure investment is absent. The Japanese model is best understood as the K-pop talent agency model applied to virtual avatars on YouTube, with merchandise and live events as the durable economic engines.

If your firm is evaluating a VTuber sponsorship, a collaboration merchandise programme, an event title-sponsorship, or an investment in a Japanese VTuber agency or supplier, Japonity’s editorial and business-matching teams introduce qualified overseas partners to vetted Japanese rights holders and agencies. Contact our business-matching desk to begin.

More from Japonity’s Japan Anime Business series

This article is part of a 10-piece editorial cluster on the business of Japanese anime. Read the rest:

- Inside Japan’s Anime Production Committee — How the money and rights really flow inside the joint-venture structure that funds almost every Japanese TV anime.

- Japan’s Anime Export Boom — Why overseas anime sales topped ¥1.7 trillion and overtook domestic for the first time in 2023.

- The 10 Anime Studios Behind 80% of Output — A ranked, opinionated business map of the studios that dominate foreign-licensed Japanese animation.

- Licensing Anime IP: A 2026 Foreign Buyer’s Guide — Why Western licensing instincts produce wrong answers in Japan, and the eight-stage flow that actually closes deals.

- The New Geography of Anime Streaming — Crunchyroll, Bilibili, Netflix, Disney+ and others split the world by region, rights and business model.

- Why Akihabara Still Matters — Behind the neon, Tokyo’s Akihabara is a working B2B test market for anime IP — a foreign buyer’s walking tour.

- The Anime Merchandise Pipeline — From Tokyo factories to Comic-Con booths — how an anime figure actually travels to a foreign retail shelf.

- Japan’s Trillion-Yen Manga Industry — Inside a publishing business larger than anime — and the four Tokyo houses every foreign publisher should know.

- A Day in the Life of an Anime Animator — Inside the working day of a rank-and-file animator, and the structural reasons wages stay low across the industry.

Sourcing beyond anime? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores that already stock them, with HS codes, certifications and supplier MOQs ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →