In July 2017, three fierce competitors did the unthinkable. Nippon Yusen Kabushiki Kaisha (NYK Line), Mitsui O.S.K. Lines (MOL) and Kawasaki Kisen Kaisha (K Line) — the trio that had defined Japanese shipping for over a century — folded their container divisions into a single joint venture, Ocean Network Express (ONE). It was an admission, after years of bleeding losses in the commodified box-shipping market, that none of them could survive that business alone. Yet the merger left the rest of NYK — the world’s oldest shipping group still in operation, founded in 1885 — not weaker but sharper. Stripped of its loss-making container arm, NYK doubled down on what it does best: pure car carriers (PCC) hauling Toyotas, Hondas and Nissans across the Pacific; dry-bulk vessels feeding Japanese steel mills with Australian iron ore; and LNG carriers serving Asia’s energy transition. When the pandemic shipping super-cycle of 2021-2022 sent freight rates to record highs, ONE delivered NYK its largest profits in history. This is the story of how a Mitsubishi-founded shipping company became the quiet anchor of Japan’s three-way maritime oligopoly — and the world’s largest auto-carrier operator.

From Mitsubishi to Mitsubishi: a 141-year arc

NYK’s origin story is inseparable from the Mitsubishi zaibatsu. In September 1885, two Japanese shipping operators — Mitsubishi Shipping Company (run by Yataro Iwasaki, founder of Mitsubishi) and the government-backed rival Kyodo Unyu Kaisha — merged under government pressure to form Nippon Yusen Kabushiki Kaisha. Tokyo wanted a national flag carrier strong enough to challenge Western powers on the seas; merging the two largest domestic operators was the answer.

The newly formed NYK was not just a shipping company but an instrument of Japan’s modernization. By 1893 it had opened a regular service to Bombay (Mumbai); by 1896, lines to Europe, North America and Australia. The famous “Three Lines of the Pacific” — Yokohama-Seattle, Yokohama-San Francisco, Yokohama-Hong Kong — turned NYK into a recognizable global brand decades before most Japanese manufacturers had even begun exporting.

Two world wars devastated the fleet. NYK lost roughly 185 vessels in World War II, including most of its crews. The postwar reconstruction, supported by Japan’s industrial policy, rebuilt the company around two pillars that still define it: bulk shipping for the iron and steel industry, and liner shipping for the country’s export-driven manufacturers. By the 1970s NYK was a core member of the Mitsubishi keiretsu — quietly tied to Mitsubishi UFJ Bank, Mitsubishi Corporation and the broader trading-house ecosystem that still characterizes its customer book today.

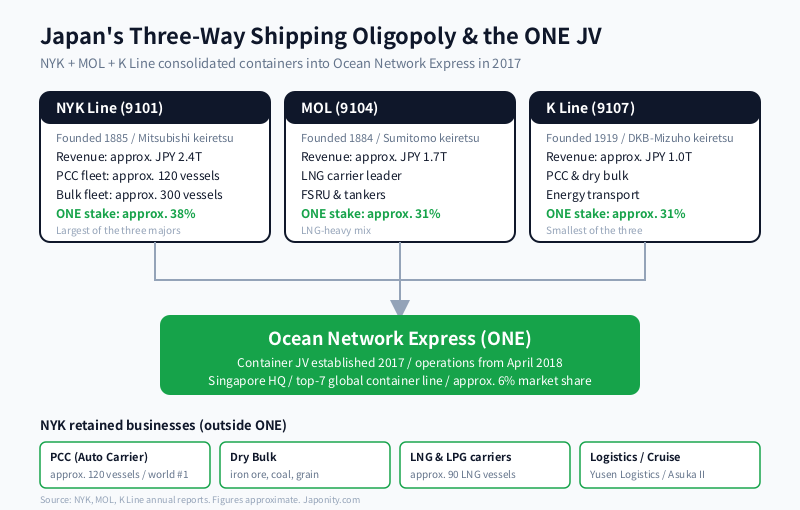

The 2017 reset: why three rivals built ONE

For most of the 2000s and 2010s, the world’s container shipping market was a slow-motion catastrophe. After the global financial crisis, fleet capacity grew faster than trade volumes for nearly a decade. Freight rates fell below cash-operating costs. South Korea’s Hanjin Shipping, once a top-ten carrier, collapsed in 2016 — a warning shot heard loudly in Tokyo.

Japan’s three big carriers — NYK, MOL and K Line — were each individually too small to compete with Maersk (Denmark), MSC (Switzerland) and CMA CGM (France), the European giants that had been consolidating aggressively. In October 2016 the three Japanese rivals announced the unthinkable: they would merge their container businesses into a single joint venture. Ocean Network Express (ONE) began operations in April 2018 from a Singapore headquarters, with NYK holding approximately 38%, MOL 31% and K Line 31%.

The merger was painful — the first year produced a roughly USD 600 million loss as IT systems clashed and customers defected — but by 2020 ONE had stabilised as a top-seven global container line with around six percent market share. Then the pandemic arrived. Port congestion, container shortages and a consumer-goods boom sent freight rates up by a factor of ten. ONE recorded over USD 16 billion in net profit in fiscal 2021, of which NYK’s share alone exceeded the company’s combined profits of the previous decade.

The auto-carrier kingdom: PCC as the crown jewel

Containers grab the headlines, but NYK’s most enduring competitive moat sits in a less glamorous corner of shipping: the Pure Car Carrier, or PCC. These ships — looking from outside like floating warehouses with ramps — are specifically designed to move finished automobiles. Each can carry approximately 6,000 to 7,000 vehicles. NYK operates a fleet of roughly 120 such vessels, the largest in the world.

The PCC business is structurally attractive in ways container shipping is not. Customers are concentrated — Toyota, Honda, Nissan, Mazda, Subaru, plus growing volumes from Korean and European brands — and they sign long-term contracts rather than spot rates. Switching costs are high: a Toyota plant in Aichi cannot simply put its Camrys on a competitor’s ship next quarter. And the fleet is hard to replicate. Building a new PCC takes about two years and roughly USD 100 million per vessel, and only a handful of yards in Japan, Korea and China can build them well.

The result is an oligopolistic market dominated by NYK, MOL and K Line (the same three Japanese houses), plus Norway’s Wallenius Wilhelmsen and Korea’s Hyundai Glovis. Japan’s automakers prefer to ship on Japanese keels for the same reason German automakers prefer European yards — relationships, financing flexibility, and an industrial-policy logic that runs back decades.

Bulk, LNG, and offshore: the unsung businesses

Dry bulk — the carriage of iron ore, coal, grain and other commodities in unpackaged form — is NYK’s other historic stronghold. Japan is the world’s third-largest steel producer; nearly all its iron ore comes from Australia and Brazil. NYK’s Capesize and Panamax bulker fleet (approximately 300 vessels including chartered tonnage) feeds Nippon Steel, JFE Steel and Kobe Steel under long-term contracts of affreightment. This is unsexy business — average freight rates have been low for years — but the contracts are sticky and dollar-denominated, providing a steady hedge against yen weakness.

LNG and LPG carriers form a third leg. With Japan having shut most of its nuclear capacity after Fukushima in 2011, the country became the world’s largest LNG importer for a decade. NYK operates approximately 90 LNG carriers, often through joint ventures with Mitsubishi Corporation and the major energy utilities (JERA, Tokyo Gas, Osaka Gas). Each carrier is effectively a floating, insulated thermos worth USD 250 million; the contracts behind them often run 15 to 20 years.

Offshore — supply vessels, floating production storage units, and shuttle tankers — was an aggressive growth bet through the 2010s and is now being rationalised after the oil-price crash and the energy transition. NYK is repositioning the offshore unit toward offshore wind support vessels, an area where Japan’s domestic market is finally beginning to scale.

The three-way Japanese shipping landscape

| Company | Ticker (TSE) | FY24 Revenue (approx.) | Container JV stake (ONE) | Signature business |

|---|---|---|---|---|

| NYK Line (Nippon Yusen) | 9101 | JPY 2.4 trillion | ~38% | PCC (auto carrier), Dry bulk, LNG |

| MOL (Mitsui O.S.K. Lines) | 9104 | JPY 1.7 trillion | ~31% | LNG carriers, Dry bulk, FSRU |

| K Line (Kawasaki Kisen) | 9107 | JPY 1.0 trillion | ~31% | PCC, Dry bulk, Energy transportation |

The three companies, often grouped as Japan’s “shipping majors”, are roughly comparable in vessel count but differ in business mix. NYK is the largest and most diversified; MOL skews heavily toward LNG and tanker work; K Line is the smallest and most cyclical. All three are members of separate keiretsu (NYK-Mitsubishi, MOL-Sumitomo, K Line-DKB/Mizuho), which historically prevented any merger of the three companies themselves — only their container arms could be combined.

Cruise, logistics and the air cargo exit

NYK’s brand recognition outside shipping circles comes largely from one ship: Asuka II, the flagship of Japan’s premium domestic cruise market. Operated by subsidiary NYK Cruises, Asuka II is a 50,000-ton, 872-passenger vessel built in 1991, scheduled to be replaced in 2025 by a new Asuka III. The cruise business is small in revenue terms (under one percent of group sales) but disproportionately important for brand and recruitment.

Logistics — third-party warehousing, freight forwarding, customs brokerage — is run through the listed subsidiary Yusen Logistics (TSE: 9370), which NYK took private and then partially relisted. With approximately 600 offices in 45 countries, Yusen Logistics is Japan’s largest forwarder by international air cargo handling volume. It increasingly competes with DHL, Kuehne+Nagel and DSV — and like them is investing heavily in digital booking platforms.

Air cargo, by contrast, has been exited. In 2024 NYK completed the sale of subsidiary Nippon Cargo Airlines (NCA) to ANA Holdings’ cargo arm, ANA Cargo, for an undisclosed sum. The sale ended NYK’s 46-year direct presence in the air cargo business and reflected a strategic decision to focus capital on maritime decarbonisation rather than maintain an undersized freighter operation.

Decarbonisation: the next twenty years

Shipping accounts for approximately three percent of global CO2 emissions, and the International Maritime Organization (IMO) has agreed to reach net-zero by around 2050. For an industry where vessels are typically depreciated over 25 years, this means every ship ordered today must already have a credible path to carbon-neutral fuels.

NYK’s strategy, articulated under its 2023 medium-term plan and current president Yutaka Higurashi (appointed 2023), bets on a portfolio of alternative fuels: ammonia for deep-sea, LNG and methanol as transition fuels, and battery-electric for short-sea and tugs. The company is a founding investor in ammonia-fuelled vessel projects with Nihon Shipyard and IHI Power Systems, and announced its first ammonia-fuelled PCC in 2024.

Capital expenditure has stepped up sharply. NYK’s medium-term plan envisions roughly JPY 1.2 trillion of capex over five years to 2027, of which a third is allocated to green-fuel vessels. The financing assumes that the post-pandemic profit windfall — over JPY 2 trillion in cumulative net income in fiscal 2021-2022 — provides the balance-sheet cushion to invest through what is otherwise a structurally low-margin industry.

What it means for foreign companies and investors

For overseas exporters into Japan, NYK is rarely the front-line counterparty — that role usually falls to ONE on containers or to Yusen Logistics on door-to-door freight. But understanding NYK matters for three reasons. First, in automotive, NYK and its peers control roughly half the world’s deep-sea PCC capacity; pricing and slot availability are determined in long-term negotiations between three Japanese shipowners and a handful of automakers. Second, in LNG, NYK is structurally embedded in the procurement of Japan’s energy utilities — any new project shipping LNG to Japan is likely to involve an NYK vessel or its JV. Third, as an investment thesis, NYK trades on the Tokyo Stock Exchange (9101) at a price-to-book ratio that has historically swung between 0.4x in container troughs and 1.5x at cyclical peaks — making it a high-beta proxy for global trade volumes and a vehicle for foreign investors taking a view on Japan’s industrial economy.

For Japanese policy watchers, NYK also matters as a national-security asset. In any future Indo-Pacific contingency, the question of who controls the merchant fleet feeding Japan’s energy and food imports is no longer abstract. NYK, MOL and K Line — together with the Japan Maritime Self-Defense Force — quietly form the backbone of what Tokyo calls its “sea lane security” framework.

FAQ

When was NYK Line founded?

NYK was founded in September 1885 through the merger of Mitsubishi Shipping Company (controlled by the Iwasaki family of Mitsubishi) and the government-backed Kyodo Unyu Kaisha. It is the oldest shipping company in Japan still in operation and one of the oldest in the world. Headquarters are in Otemachi, Tokyo.

What is ONE (Ocean Network Express) and how does it relate to NYK?

ONE is the container-shipping joint venture established in July 2017 (operations commenced April 2018) by NYK, MOL and K Line — Japan’s three largest shipping companies. NYK holds approximately 38% of ONE, the largest stake. ONE consolidates the three companies’ container operations into a single global carrier headquartered in Singapore, currently the seventh-largest container line worldwide.

How large is NYK’s pure car carrier (PCC) fleet?

NYK operates approximately 120 pure car carriers, the largest such fleet in the world. Each PCC can carry roughly 6,000-7,000 finished vehicles. The fleet serves long-term contracts with Toyota, Honda, Nissan, Mazda, Subaru and other automakers, moving cars from Japan and Korea to the Americas, Europe, the Middle East and Oceania.

Is NYK part of the Mitsubishi group?

Yes. NYK is a core member of the Mitsubishi keiretsu, tracing its lineage to Mitsubishi Shipping Company founded by Yataro Iwasaki in the 1870s. It maintains close ties with Mitsubishi UFJ Bank, Mitsubishi Corporation, and other Mitsubishi-group companies through cross-shareholdings and shared business relationships, though it operates independently as a listed company on the Tokyo Stock Exchange (ticker 9101).

Did NYK sell its air cargo business?

Yes. In 2024 NYK completed the sale of its wholly owned subsidiary Nippon Cargo Airlines (NCA) to ANA Holdings’ cargo arm, ANA Cargo. The transaction ended NYK’s 46-year direct presence in air cargo and reflected a strategic decision to concentrate investment on maritime decarbonisation, particularly ammonia and methanol-fuelled vessels.

Working with NYK

Whether you are a manufacturer seeking long-term ocean logistics, an LNG project sponsor looking for vessel partners, or an investor evaluating Japan’s shipping cycle, understanding the NYK-MOL-K Line oligopoly and the role of ONE is essential. Japonity’s business-matching service introduces foreign companies to Japan’s maritime, logistics and trading-house ecosystem — including the three shipping majors and their listed subsidiaries (Yusen Logistics, MOL Logistics, K Line Logistics).

→ Explore Japonity Business Matching

Related from Japonity — Japan’s deep-sea shipping

- Mitsui O.S.K. Lines (MOL) — Japan’s #2 shipping company and the world’s largest LNG carrier fleet

- Kawasaki Kisen (K Line) — Japan’s #3 shipping company and the leverage-restructuring story

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →