In Japan’s roughly $80 billion drugstore market, one chain has quietly become the largest by store count, the most profitable in its segment, and the unlikely darling of an aging society’s healthcare strategy. Welcia Holdings — about 2,800 stores under the Welcia, Hac Drug, Inageya Welcia and Marudai banners — sits at the top of the league table, controls a dispensing-pharmacy footprint that few competitors can match, and is majority-owned by Aeon Group. In February 2024, Welcia and the country’s #2 chain Tsuruha Holdings announced an integration plan: a combined entity targeting roughly ¥3.4 trillion ($22 billion) in revenue, vaulting past Asia’s existing drugstore leaders and reshaping what the industry calls Japan’s “fourth retail format.” This is the story of how a single pharmacy in Ibaraki became the prototype for a uniquely Japanese hybrid — half clinic, half convenience store — and why the rest of the sector is now consolidating to keep up.

From a single Ibaraki pharmacy to the national league table

Welcia traces its roots to 1980, when Junichi Suzuki founded Suzuki Yakkyoku in the city of Ushiku, Ibaraki Prefecture, north of Tokyo. The original was a single dispensing pharmacy attached to a local clinic ecosystem — a model that, in 1980s Japan, was the rule rather than the exception. Pharmacies were small, neighborhood, prescription-led, and ran on thin margins.

What changed Suzuki’s trajectory — and the industry’s — was the 1990s push by Japan’s Ministry of Health, Labour and Welfare to separate dispensing from prescribing (医薬分業, iyaku-bungyō). The reform forced doctors to write external prescriptions rather than dispense in-house, creating sudden demand for independent retail pharmacies near hospitals and clinics. Suzuki Yakkyoku expanded aggressively into this gap, gradually shifting from a pure prescription business to a hybrid store mixing dispensing, over-the-counter (OTC) medicine, cosmetics, daily goods and eventually food. By 2000, the chain had been renamed Welcia Kanto, and by 2008 it had become Welcia Holdings — a listed entity on the Tokyo Stock Exchange (3141) with roughly 700 stores.

The decisive turn came that same year. Aeon Group, Japan’s largest retail conglomerate, acquired a majority stake in Welcia Holdings, folding it into a portfolio that already included supermarkets, malls, convenience stores and financial services. The deal gave Welcia access to Aeon’s private-label supply chain, its loyalty program (WAON), and — crucially — its mall real estate. What had been a regional Kanto chain became a national platform almost overnight. Today Welcia operates around 2,800 stores, generates more than ¥1.1 trillion in revenue, and is the #1 drugstore in Japan by both store count and sales.

The “fourth retail format” Japan invented

To understand Welcia’s importance, you have to understand what a Japanese drugstore actually is — because it bears almost no resemblance to a Walgreens, Boots or Watsons. In Western markets, drugstores are essentially pharmacies with a cosmetics aisle bolted on. In Japan, they are something stranger: a 1,000–2,000 square-metre big-box format that sells prescription drugs, OTC medicines, vitamins, cosmetics, baby goods, diapers, household cleaners, snacks, beverages, frozen food, rice and increasingly fresh produce — all at price points that undercut both supermarkets and convenience stores on packaged goods.

Industry analysts call this the “fourth retail format,” sitting alongside supermarkets, convenience stores and general merchandise stores (GMS). Drugstores grew by stealing share from all three: from supermarkets on toiletries and snacks, from convenience stores on packaged food and beverages, and from GMS on cosmetics and baby goods. The format works because Japan’s tax code zero-rates a basket of medical and hygiene categories, because pharmacy regulations create high entry barriers, and because the dispensing-pharmacy revenue stream — insurance-reimbursed, low-volatility — cross-subsidises the front-of-store retail.

Welcia has pushed this hybrid further than anyone. Roughly half of its stores include a dispensing pharmacy counter — the highest ratio among the top chains — which generates around a third of group revenue but disproportionate margin and customer stickiness. The remaining footprint mixes OTC, cosmetics and food in proportions tuned to each neighborhood: urban Tokyo stores skew heavily to cosmetics and bento; suburban Aeon-mall stores carry deeper food and baby aisles; rural Welcia outlets in Ibaraki and Tochigi function as miniature general stores. The chain’s 24-hour pharmacy concept — a small but growing subset — addresses an aging-society problem that competitors have largely ignored.

The Aeon umbilical cord

It is impossible to discuss Welcia without discussing Aeon. Aeon Group holds roughly half of Welcia Holdings — enough to consolidate it as a subsidiary, enough to direct strategy, and enough to make Welcia’s destiny inseparable from Aeon’s broader retail vision. That vision has, for the last decade, treated drugstores as a strategic adjacency to the supermarket and mall businesses: a higher-margin, demographically defensible format that can be planted inside Aeon malls, near Aeon supermarkets, or in standalone locations where Aeon has no presence.

The benefits flow both ways. Welcia gets WAON loyalty integration, Aeon Topvalu private-label products on its shelves, financing from Aeon Financial Service, and preferential mall slotting. Aeon gets a healthcare beachhead it could not build organically — and a chain that, unlike Aeon’s own supermarkets, generates above-segment operating margins. Welcia’s operating margin sits in the mid-single digits, healthy for Japanese retail, and well above the Aeon supermarket business’s roughly 2% range.

The structural arrangement also explains why Welcia’s growth has not come primarily from greenfield store openings, but from M&A. Welcia absorbed Takasaki Pharmacy in 2014, CFS Corporation — the parent of Hac Drug, dominant in Kanagawa — in 2015, Marudai Welcia Yakkyoku in Niigata in 2018, and Inageya Welcia, a joint venture with Aeon-affiliated supermarket Inageya, over multiple stages. Each tuck-in added regional density without dilution of the operating model. By 2023, Welcia had become a federation of regional banners coordinated under one holding company — closer to Aeon’s own conglomerate structure than to a traditional single-banner retailer.

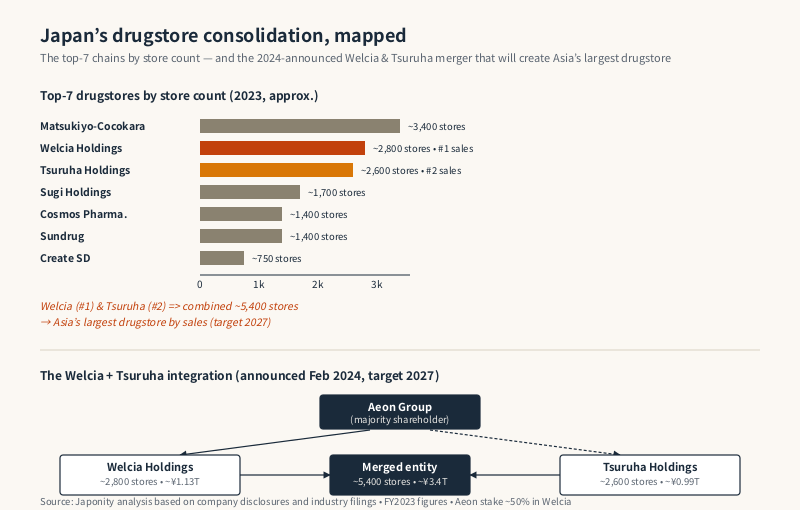

The drugstore league, and why consolidation became inevitable

Japan’s drugstore industry contains a peculiar fact: by 2023 it had roughly seven national chains, none with more than 15% market share, and a long tail of regional operators. The top tier — Welcia, Tsuruha, Cosmos, Sundrug, Matsumotokiyoshi-Cocokara, Sugi, Create SD — had been racing each other on store openings and SG&A scale for two decades. Margins were healthy but no one had a structural moat. The math of dispensing-pharmacy economics rewards scale — purchasing power, IT systems, pharmacist deployment, insurance-claim back office — at exactly the level no single chain had yet reached.

| Rank (2023) | Chain | Stores | Revenue (¥ trillion) | Notes |

|---|---|---|---|---|

| 1 | Welcia Holdings | ~2,800 | ~1.13 | Aeon majority; #1 by stores |

| 2 | Tsuruha Holdings | ~2,600 | ~0.99 | Hokkaido roots; Oasis Management activist |

| 3 | Matsumotokiyoshi-Cocokara | ~3,400 | ~0.96 | 2021 merger; cosmetics-led, inbound focus |

| 4 | Cosmos Pharmaceutical | ~1,400 | ~0.92 | Kyushu base; food-heavy “discounter” model |

| 5 | Sugi Holdings | ~1,700 | ~0.70 | Tokai region; dispensing-pharmacy heavy |

| 6 | Sundrug | ~1,400 | ~0.69 | Tokyo / Kansai urban density |

| 7 | Create SD Holdings | ~750 | ~0.36 | Kanagawa / Shizuoka |

The first major consolidation came in 2021, when Matsumotokiyoshi and Cocokara Fine merged to form Matsumotokiyoshi-Cocokara Holdings, instantly the largest by store count and a cosmetics-led leader in urban Japan and the inbound tourist channel. That merger reset the field. The remaining top chains were forced to consider whether to merge themselves or be permanently locked into smaller scale.

For Welcia and Tsuruha, the answer arrived in February 2024. The two companies — historically rivals, with Welcia strong in Kanto and Tsuruha strong in Hokkaido and western Japan — announced a basic agreement to integrate by the end of 2027, under a new holding company likely to be majority-controlled by Aeon Group. The combined entity would operate roughly 5,400 stores, generate approximately ¥3.4 trillion ($22 billion) in revenue, and become Asia’s largest drugstore chain by sales — leapfrogging not only Matsumotokiyoshi-Cocokara but also Hong Kong’s A.S. Watson and South Korea’s Olive Young.

The deal is not without complications. Tsuruha’s largest minority shareholder, the Hong Kong-based activist fund Oasis Management, had spent the prior two years pushing for governance changes and had opposed earlier Aeon-led integration talks. The 2024 announcement reflects a negotiated compromise — including board independence concessions and a multi-year integration timeline — but the final structure remains subject to shareholder approval and regulatory clearance.

The dispensing-pharmacy edge

What sets Welcia apart from Cosmos, which has chosen a food-discounter model, or Matsumotokiyoshi, which has chosen a cosmetics-and-inbound model, is its commitment to the dispensing pharmacy. Roughly half of Welcia stores include a prescription counter staffed by licensed pharmacists, compared with industry averages closer to 25%. The decision is expensive — pharmacists are scarce and command higher wages than retail staff, and the regulatory overhead is significant — but it has produced a defensible niche.

Japan’s aging population — 29% over 65, projected to reach 35% by 2040 — is driving structural growth in prescription volumes. National Health Insurance reimbursement for dispensing is stable, with periodic downward revisions but no risk of collapse. And the dispensing footprint creates a flywheel: customers who fill prescriptions also buy OTC medicines, vitamins, hygiene products and increasingly food, generating a basket size meaningfully larger than the drugstore sector average. Welcia’s same-store sales growth has consistently outpaced the industry, and its dispensing-pharmacy revenue line grows at high single digits annually.

The Tsuruha merger amplifies this. Tsuruha has a smaller dispensing footprint as a share of revenue, but a larger absolute store base in Hokkaido and western Japan — geographies where Welcia is thin. The combined entity would unify Welcia’s pharmacy operating model across Tsuruha’s network, while gaining Tsuruha’s regional density in markets Welcia has historically struggled to enter.

The next-generation drugstore: clinic-adjacent, AI-assisted, food-led

Welcia’s leadership, currently under president Mishio Mizuno, has been explicit about where the format is going. Three vectors stand out. The first is clinic adjacency: Welcia has been opening pharmacies inside or next to medical clinics, hospitals and senior-care facilities, often under multi-year exclusive agreements. The model imports the dispensing economics into a much higher prescription-volume environment than a standalone retail store could ever match.

The second vector is food. Welcia has been quietly expanding its fresh and frozen food assortment, narrowing the gap with supermarkets and convenience stores. In rural Japan, where supermarket density is falling as the population ages, the Welcia store often becomes the de facto grocery option. The Aeon Topvalu private-label range gives Welcia a cost advantage that pure-play drugstores struggle to match.

The third is technology. Welcia has invested in pharmacist workflow automation, telehealth-linked dispensing, and AI-assisted inventory and replenishment systems shared with Aeon. The chain has piloted “smart pharmacies” with semi-automated dispensing robots, and is among the larger users of digital prescription infrastructure introduced by the Ministry of Health in 2023. These investments will be easier to amortise across a combined Welcia-Tsuruha footprint than they would have been across either company alone — a point the merger announcement explicitly cited.

The strategic question

The merger, if completed on schedule by 2027, will produce a drugstore chain unlike anything else in Asia: a 5,000-plus-store hybrid retail-and-healthcare network with anchored dispensing economics, a private-label supply chain through Aeon, and the deepest pharmacist roster in Japan. Whether that translates into sustained margin expansion or simply into more bargaining power against suppliers and insurers is the open question. Japanese retail has a long history of scale that fails to translate into profitability — Aeon Group itself is the canonical example.

What is harder to dispute is the strategic logic. Japan’s demographic curve guarantees rising demand for pharmacy and healthcare services. The regulatory moat — pharmacist licensing, dispensing rules, insurance-claim systems — keeps foreign and pure-tech entrants out. And the fourth-format hybrid has proven resilient in a way that pure supermarkets and pure convenience stores have not. For overseas operators looking at Japan, Welcia is now both the gatekeeper of the drugstore channel and, after 2027, the single most important retail counterparty in the healthcare-adjacent consumer market.

FAQ

How many stores does Welcia Holdings operate?

Approximately 2,800 stores across Japan as of 2024, making Welcia the #1 drugstore chain in Japan by store count. The footprint includes the core Welcia and Welcia Yakkyoku banners, Hac Drug in Kanagawa, Marudai in Niigata and Inageya Welcia in greater Tokyo.

What is Welcia’s relationship with Aeon Group?

Aeon Group has held a majority stake — roughly 50% — in Welcia Holdings since 2008. Welcia is consolidated as an Aeon subsidiary and integrates with Aeon’s private-label, loyalty program (WAON) and mall real estate, while operating as a separately listed entity on the Tokyo Stock Exchange (ticker 3141).

What is the Welcia-Tsuruha merger?

In February 2024, Welcia Holdings and Tsuruha Holdings — Japan’s #1 and #2 drugstore chains — announced a basic agreement to integrate under a new holding company by the end of 2027. The combined entity would operate roughly 5,400 stores and generate approximately ¥3.4 trillion ($22 billion) in revenue, becoming Asia’s largest drugstore chain by sales.

What makes Japanese drugstores different from Western ones?

Japanese drugstores are a much broader retail format than Western pharmacies. They typically sell prescription drugs, OTC medicines, cosmetics, baby goods, household items, snacks, beverages and increasingly fresh and frozen food — often at lower prices than supermarkets or convenience stores. Industry analysts call this the “fourth retail format” alongside supermarkets, convenience stores and general merchandise stores.

How does Welcia compete with Matsumotokiyoshi-Cocokara?

Welcia and Matsumotokiyoshi-Cocokara represent two different drugstore strategies. Matsumotokiyoshi-Cocokara leads in cosmetics and inbound-tourism retail, with strong urban Tokyo and Osaka density. Welcia leads in dispensing pharmacy — roughly half of its stores include a prescription counter — and skews more toward suburban and rural geography with broader food and daily-goods assortment. The Tsuruha merger would significantly widen Welcia’s lead in total scale.

Working with Welcia

For overseas brands in cosmetics, health and wellness, OTC medicine, baby goods, food and beverage, or supplements, Welcia is a primary gatekeeper to the Japanese drugstore channel — and after the Tsuruha integration, the single largest distribution partner in Asia’s drugstore market. Japonity’s business matching service helps overseas companies navigate Welcia’s category buyer structure, prepare submission materials aligned with Aeon Group procurement standards, and identify the right distributor partners for first-stage market entry. Get in touch to discuss how your product fits Japan’s drugstore opportunity.

Related from Japonity — Japan’s drugstore chains

- Tsuruha Holdings — Japan’s #2 drugstore — the Oasis activist campaign and the Welcia merger

- Matsukiyo Cocokara — The tourist-favourite drugstore — Japan’s #3 after Welcia-Tsuruha

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →