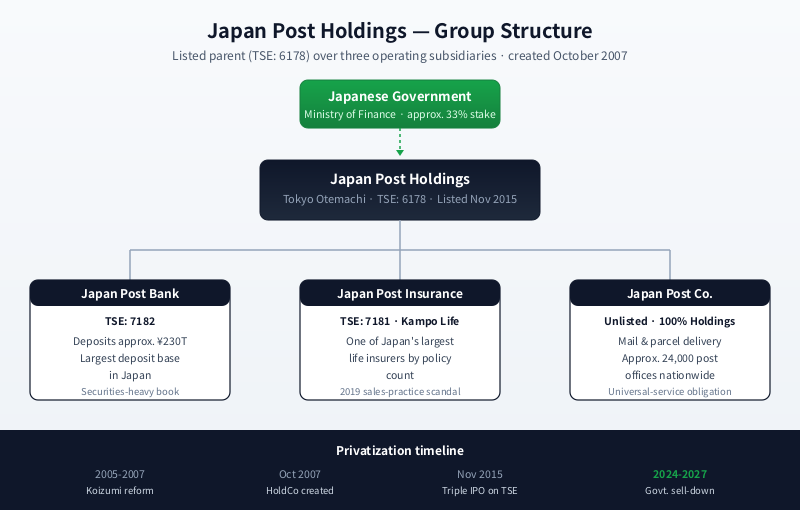

In October 2007, after nearly two decades of political fights, a single piece of administrative geometry was redrawn. Japan Post Public Corporation — the postwar postal monopoly that for more than a century had sat inside Japan’s central government, run by what is now the Ministry of Internal Affairs and Communications — was broken into four separate joint-stock companies and placed under a holding company in Tokyo’s Otemachi district. The reform was the centerpiece of former prime minister Junichiro Koizumi’s 2005-2007 privatization drive, the issue on which he had called and won a snap general election. From that day, Japan Post Holdings (TSE: 6178) became the parent of three operating subsidiaries that, taken together, made it one of the most unusual financial conglomerates in the world: Japan Post Bank, with deposits of approximately ¥230 trillion making it Japan’s largest deposit-taking institution; Japan Post Insurance, marketed as Kampo Life and historically the country’s largest life insurer by policy count; and Japan Post, the mail and parcel delivery business whose approximately 24,000 post offices form a network larger than 7-Eleven Japan’s store count. Nearly two decades after privatization, the Japanese government — through the Ministry of Finance — still holds roughly one-third of the parent company’s shares. Between 2024 and 2027, that residual stake is being unwound in a sequence of secondary offerings that will hand foreign and domestic institutional investors their largest single piece of postal-financial paper in a generation.

From postwar monopoly to listed holding company

The institution that Japan Post Holdings inherited was old. The Meiji-era postal system dates to 1871, and from its earliest years it carried not only letters but savings deposits — the postal savings system, established in 1875, became one of the largest pools of household capital in the country and, for much of the twentieth century, an off-balance-sheet funding source for government-directed lending through the Fiscal Investment and Loan Program. Postal life insurance, marketed under the Kampo name, was added in 1916 and grew into Japan’s largest life insurer by number of policies in force. By the postwar period, the postal monopoly was simultaneously a postman, a savings bank, and a life-insurance company — all run inside a government ministry, with no separate balance sheets and no external shareholders.

The political case for breaking that structure apart had two strands. The first was efficiency: critics argued that the postal monopoly was overstaffed, sheltered from competition, and a drag on Japan’s productivity. The second was capital allocation: the roughly ¥330 trillion of postal savings and insurance assets in the early 2000s sat largely in Japanese government bonds and FILP loans, and proponents of privatization argued that a listed, profit-seeking financial institution would deploy that capital more productively. Koizumi’s signature legislative push between 2005 and 2007 — including the dramatic 2005 snap election he called after the upper house initially rejected his bill — produced the October 2007 reorganization. Japan Post Holdings became the parent. The three operating subsidiaries were spun out as separate joint-stock companies. The privatization timetable, originally projected to end government ownership entirely by 2017, was repeatedly slowed by subsequent administrations.

The 2015 triple IPO and what came next

The first listing wave came in November 2015, when Japan Post Holdings, Japan Post Bank, and Japan Post Insurance simultaneously listed on the Tokyo Stock Exchange — a coordinated triple IPO that, by some measures, was the largest in Japan since NTT’s privatization in the late 1980s. The structure was deliberate. Japan Post Holdings, the parent, sold a minority of its shares to public investors while the Ministry of Finance retained a controlling stake. The two listed subsidiaries — Bank and Insurance — sold smaller free floats, with Holdings continuing to own the majority of each. Japan Post itself, the mail-delivery business, was not listed and remains a wholly owned subsidiary of Holdings.

The 2015 triple IPO accomplished several things at once. It established market valuations for entities whose balance sheets had previously been opaque inside the government accounts. It gave the operating subsidiaries listed-currency optionality for future acquisitions — a card that Japan Post Holdings tried to play, with limited success, in its 2015 acquisition of Australian logistics company Toll Holdings. And it set a precedent for the gradual sell-down of government ownership that has continued, with pauses, ever since.

The group today: holding company over three operating pillars

For foreign investors, lenders, reinsurers, logistics partners, and policy researchers trying to understand the group, the cleanest mental model is to treat Japan Post Holdings as a parent that owns three operating subsidiaries with very different business models, capital intensities, and regulatory regimes.

| Entity | Business | Scale | Role within group |

|---|---|---|---|

| Japan Post Holdings (TSE: 6178) | Listed holding company | Govt. (MoF) ~33% stake | Parent over three operating subsidiaries; HQ Otemachi, Tokyo |

| Japan Post Bank (TSE: 7182) | Deposit-taking bank, asset management | Approx. ¥230T deposits | Largest savings bank in Japan by deposits |

| Japan Post Insurance / Kampo (TSE: 7181) | Life insurance | Tens of millions of policies in force | One of Japan’s largest life insurers by policy count |

| Japan Post Co. | Mail, parcel and post office network | Approx. 24,000 post offices nationwide | Unlisted; wholly owned by Holdings |

Two features of this structure shape almost every strategic conversation about the group. First, Japan Post Holdings is a financial holding company in economic substance — the bank and the insurer dwarf the mail-delivery business by assets, revenues, and pretax profit, and the group’s reported earnings move with interest rates and investment returns more than with parcel volumes. Second, the three operating subsidiaries are tied together by the post office network: most retail customers of Japan Post Bank and Kampo Life buy their products at a counter inside a Japan Post Co. branch, and the unwinding of any pillar would unsettle the economics of the others.

Japan Post Bank: ~¥230 trillion of deposits and a yield problem

Japan Post Bank is, by deposit base, the largest bank in Japan. The roughly ¥230 trillion of deposits it carries on its balance sheet is more than any of the three megabanks — Mitsubishi UFJ, Sumitomo Mitsui, Mizuho — hold individually in their domestic operations. The deposit base is overwhelmingly retail, gathered through the Japan Post counter network, and it is sticky in a way that wholesale funding never is. That stickiness is the bank’s structural advantage and, simultaneously, its structural problem.

Unlike the megabanks, Japan Post Bank does not have a meaningful corporate lending book. Historically, postal savings funds were channelled into Japanese government bonds and Fiscal Investment and Loan Program lending; even after privatization, the bank’s loan book is small relative to its assets. Most of the balance sheet sits in securities — JGBs, foreign bonds, structured credit, equity funds, and increasingly alternative assets including private equity and infrastructure mandates. In a low-rate environment, that mix produced a structural yield gap: the bank pays close to zero on deposits but earns single-digit basis points on its safest assets, forcing a steady reach into riskier, higher-duration positions. The Bank of Japan’s gradual exit from negative rates and yield-curve control in 2024 has improved the math, but the basic capital-allocation problem — what to do with the world’s largest pool of retail Japanese yen savings — is one of the most consequential investment questions in Asian finance.

Japan Post Insurance and the 2019 Kampo scandal

Japan Post Insurance, marketed as Kampo Life (かんぽ生命), is one of Japan’s largest life insurers measured by number of policies in force. Its business model is built on the same network: products are sold predominantly through Japan Post counters, distributed by post-office staff, and concentrated in older, less affluent rural customers. That distribution model — high-touch, deeply embedded in local communities, with sales staff whose performance is measured by new-policy targets — produced the worst reputational crisis in the group’s post-privatization history.

Beginning in mid-2019, Japanese media reported widespread improper sales practices at Kampo and Japan Post Co., including cases in which elderly customers had been persuaded to surrender existing policies and buy new ones — a “churn” that generated commission income for sales staff but left customers in worse contractual positions, sometimes without coverage during a transition window. Internal investigations identified hundreds of thousands of potentially problematic contracts. Senior executives at Japan Post Holdings, Japan Post Insurance and Japan Post Co. resigned. The Financial Services Agency imposed business improvement orders. Sales of Kampo products were temporarily suspended at post office counters while remediation programs were rolled out. The scandal forced the group to overhaul commission structures, sales training, and elderly-customer safeguards — changes that have since been formally embedded in the group’s compliance and customer-protection framework.

Japan Post Co. and the world’s largest post office network

The unlisted leg of the group — Japan Post Co. — is the least financially dramatic but the most operationally distinctive. Its approximately 24,000 post offices nationwide constitute one of the densest retail networks in the developed world, larger than 7-Eleven Japan’s convenience-store footprint. The network is the physical substrate for the bank and the insurer; without it, the deposit-gathering and policy-distribution economics of the financial subsidiaries would not work.

The mail and parcel business itself is structurally challenged. First-class letter volumes in Japan, as in every advanced economy, have been falling for two decades, and the universal-service obligation embedded in the postal law requires Japan Post to deliver to every address in the country at uniform rates. Parcels, driven by e-commerce, have grown, but the segment is competitive — Yamato Holdings (TA-Q-BIN) and SG Holdings (Sagawa Express) are aggressive, well-capitalized rivals. Strategic responses have included partnerships with Yamato on certain delivery categories, postal-network monetization through tie-ups with retailers and convenience-store chains, and consolidation of post office back-office functions. Hiroya Masuda, the former Iwate prefectural governor and minister, has served as president and representative executive officer of Japan Post Holdings since 2020.

The 2024-2027 government sell-down

The privatization that began in 2007 has never quite finished. After the 2015 triple IPO and a follow-on secondary offering in 2017, the Ministry of Finance still owned roughly one-third of Japan Post Holdings — a stake the postal privatization law authorizes the government to reduce further, with proceeds earmarked in part to fund Tohoku earthquake reconstruction.

Between 2024 and 2027, the Ministry of Finance has been executing a sequence of secondary offerings designed to bring government ownership below the one-third floor that triggers special-resolution voting rights under Japanese company law. For foreign institutional investors, these offerings are among the largest free-float events in the Japanese equity market in the period: the parent’s market capitalization, combined with the size of the government stake being unwound, has produced placements that institutional desks in Tokyo, London, and New York have priced as benchmark events. Japan Post Holdings itself has used buybacks to support the price during the sell-down and to absorb part of the supply that would otherwise hit the market.

The downstream questions for investors are unresolved. A reduced government stake should, in theory, allow Japan Post Holdings to pursue more aggressive capital deployment — buybacks, dividends, M&A — without political constraints. In practice, the universal-service obligation and the embedded role of the post office network in rural Japan mean that the group will continue to operate under a regulatory and political envelope that purely private financial conglomerates do not face. Whether the post-privatization equilibrium settles closer to a Western European postal-bank model, a Japanese megabank model, or something distinctively its own is the question that will define the next decade.

FAQ

When was Japan Post Holdings created and why?

Japan Post Holdings was established in October 2007 as the parent company created when Japan Post Public Corporation, the postwar government postal monopoly, was reorganized under the Koizumi-era privatization. The reform split the old monopoly into four separate joint-stock companies — Japan Post Holdings as parent, plus Japan Post Bank, Japan Post Insurance (Kampo) and Japan Post — and placed them on a path toward eventual listing.

Who owns Japan Post Holdings today?

The Japanese government, through the Ministry of Finance, holds approximately one-third of the parent company’s shares as of the mid-2020s. The remainder is held by domestic and foreign institutional investors and retail shareholders. Between 2024 and 2027, the Ministry of Finance is conducting a sequence of secondary offerings that will further reduce government ownership.

How large is Japan Post Bank compared to other Japanese banks?

Japan Post Bank holds approximately ¥230 trillion in deposits, making it the largest deposit-taking institution in Japan — larger by deposit base than any single domestic operation at Mitsubishi UFJ, Sumitomo Mitsui or Mizuho. Its balance sheet is concentrated in securities rather than corporate loans, reflecting its postal-savings origins.

What was the 2019 Kampo Life scandal?

Beginning in 2019, investigations revealed widespread improper sales practices at Japan Post Insurance (Kampo Life) and Japan Post Co., including cases in which elderly customers were persuaded to switch from existing policies to new ones in ways that disadvantaged the customer but generated sales commissions. Senior executives at three group companies resigned, the Financial Services Agency issued business improvement orders, and sales of Kampo products were temporarily suspended at post office counters.

How big is the post office network?

Japan Post Co. operates approximately 24,000 post offices nationwide — a retail network larger than the store count of 7-Eleven Japan. The network is the distribution channel through which Japan Post Bank and Kampo Life products reach most of their retail customers, and is one of the densest postal networks in any advanced economy.

Working with Japan Post Holdings

For overseas banks, asset managers, reinsurers, logistics operators, and policy researchers interested in engaging with Japan Post Holdings or its operating subsidiaries — Japan Post Bank, Japan Post Insurance (Kampo Life), or Japan Post Co. — Japonity supports introductions and structured analysis around the group, its privatization path, and the 2024-2027 government share offerings. Visit /business-matching/ to start a conversation.

Related from Japonity — Japan Post Group

- Japan Post Bank — Japan’s largest savings bank — Asia’s biggest deposit-funded allocator

- Japan Post Insurance — The post-office life insurer rebuilding after the 2019 scandal

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →