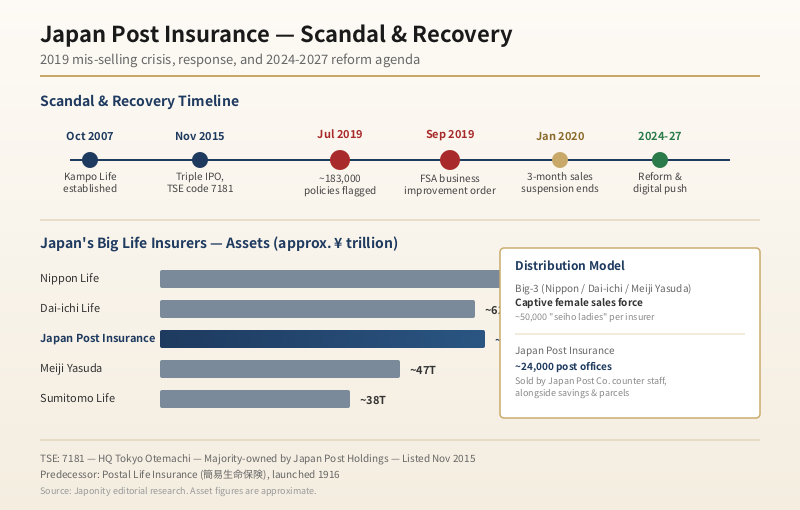

In the summer of 2019, Japan’s Financial Services Agency delivered a verdict that few in Tokyo’s insurance industry had thought possible: the country’s most ubiquitous life insurer — the one with a counter inside almost every post office from Hokkaido to Okinawa — had been systematically mis-selling policies to elderly customers. Japan Post Insurance Co., Ltd. (株式会社かんぽ生命保険), known to most Japanese simply as Kampo, was ordered to halt new sales for three months, executives resigned, and approximately 183,000 contracts were flagged for investigation. With assets of roughly ¥60-70 trillion, Kampo is Japan’s fourth-largest life insurer by assets and a uniquely physical creature in a sector increasingly going digital — its distribution still runs through approximately 24,000 post offices nationwide. This is the story of how a postwar institution became a listed financial group, stumbled badly, and is now rebuilding under a 2024-2027 reform agenda that is quietly rewiring how insurance is sold in rural Japan.

From postwar safety net to listed insurer

The legal entity called Kampo Life was created in October 2007, but its institutional DNA stretches back almost a century. Its predecessor, the Postal Life Insurance system (簡易生命保険, kan’i seimei hoken, abbreviated to “kanpo”), was launched in 1916 as a small-policy life insurance scheme run by the state postal monopoly. The premise was deliberately modest: small premiums, no medical examination, a policy available at every village post office. For most of the twentieth century, it was the only form of life insurance that ordinary Japanese — farmers, small shopkeepers, elderly women in mountain hamlets — could realistically access.

By the time Prime Minister Junichiro Koizumi pushed through his signature privatization of Japan Post in 2005-2007, the postal insurance system held an asset base larger than many sovereign wealth funds. The Postal Service Privatization Law split the monolith into four operating companies under a holding company. Kampo Life inherited the new business — policies sold from October 2007 onward — while the legacy pre-privatization policies were transferred to a separate state-backed administrator. From day one, Kampo carried a paradox in its structure: a private joint-stock insurer on paper, but with a distribution channel of post offices, a customer base built over decades of public trust, and an implicit association with the Japanese state.

The next milestone came in November 2015, when Japan Post Insurance was floated on the Tokyo Stock Exchange (code: 7181) as part of what bankers dubbed the “triple IPO” — the simultaneous listing of Japan Post Holdings, Japan Post Bank, and Japan Post Insurance. It was the largest IPO in Japan since NTT’s 1987 flotation. The state retained majority control through Japan Post Holdings, which itself remained partly government-owned. Kampo Life entered the public markets as the most peculiar of Japan’s listed insurers: simultaneously a private company answerable to shareholders, and a quasi-public institution whose distribution depended on the postal network the state still indirectly controlled.

What Kampo actually sells

To understand the 2019 scandal, one must first understand the product. Kampo’s lineup looks ordinary by global standards but has a distinct Japanese character: small face values, long durations, and a strong savings component embedded inside what are nominally protection products. The company’s headquarters, located in Tokyo’s Otemachi financial district, oversees a portfolio dominated by individual policies rather than the group contracts that anchor competitors such as Dai-ichi Life or Nippon Life.

| Segment | Typical face value | Customer profile | Distinguishing feature |

|---|---|---|---|

| Individual Whole Life (終身保険) | ¥3-10 million | Mid-aged to elderly, often rural | Lifetime cover with savings build-up; the historical mainstay |

| Term Life (定期保険) | ¥5-20 million | Family breadwinners, 30s-50s | Pure protection, lower premium, shorter duration |

| Educational Endowment (学資保険) | ¥2-5 million | Parents saving for university | Maturity-linked payouts at age 18 or 22; quintessentially Japanese |

| Individual Annuity (個人年金) | ¥5-15 million | Pre-retirees, 50s-60s | Deferred annuity with fixed payouts; competes with bank deposits |

| Medical / Hospital (医療特約) | Riders on base policy | All ages | Hospital-day benefits; cancer riders added 2010s |

Three structural features deserve highlighting. First, policies are capped by law at relatively modest face values compared with the multimillion-dollar contracts written by private insurers — a deliberate carry-over from the postal-era mandate to serve small savers. Second, the customer base skews dramatically older and more rural than that of the Big Three private competitors; Kampo’s countertop is, for many in their seventies and eighties, the only financial counter they have ever visited. Third, the educational endowment policy — a Japanese cultural artefact tying insurance to university entry — was for decades sold almost exclusively through post offices and remains a brand pillar.

The 2019 scandal: how it happened

The mechanism that broke Kampo’s reputation was technically a “policy conversion” (乗り換え, norikae) — the practice of cancelling an existing policy and replacing it with a new one. In theory, conversion can be appropriate when a customer’s needs change. In practice, from roughly 2014 through 2019, salespeople at Japan Post Co. — the post office operating company — and at Kampo Life itself converted policies in ways that left customers worse off. Elderly customers, many of whom had paid premiums into a single policy for decades, found their accumulated credits effectively reset. Some held two overlapping policies simultaneously and paid double premiums for months. Others were converted into new contracts at older entry ages, raising premiums for inferior coverage.

The improprieties were not isolated. In July 2019, an internal review identified approximately 183,000 contracts requiring re-examination, and subsequent investigations found systemic incentive misalignment: the postal sales force had been measured on new contract counts rather than on net customer benefit, and managers had pushed conversions to hit quarterly targets. On 27 September 2019, the Financial Services Agency issued a business improvement order to Japan Post Insurance, Japan Post Co., and Japan Post Holdings. Japan Post Co. — the postal salesforce — was instructed to suspend solicitation of insurance products for three months. The presidents of all three companies, including Japan Post Holdings, resigned by the end of the year.

The damage was both quantitative and qualitative. New policy sales collapsed: in fiscal years following the scandal, individual insurance new business fell sharply, and rebuilding it has taken years. Reputationally, the affair punctured a public trust that had been built over a century. The post office counter, long understood as a safer, more honest financial channel than commercial bank branches, was suddenly tarred with the same brush as the worst of pre-2008 Western retail banking.

The Big Four — and where Kampo fits

Japan’s life insurance market is one of the largest in the world by premium income, behind only the United States and trailing closely with mainland China. Four insurers dominate. Three are private mutual or stock companies with histories stretching to the late nineteenth or early twentieth century. The fourth, Kampo, is the postal newcomer with the oldest distribution footprint.

| Insurer | Founded | Approx. total assets | Distribution model | Customer skew |

|---|---|---|---|---|

| Nippon Life (日本生命) | 1889 | ¥80-90 trillion | Captive female sales force (~50,000) | Urban & suburban, all ages |

| Dai-ichi Life (第一生命) | 1902 | ¥60-65 trillion | Captive sales force + bancassurance + overseas (Protective Life US) | Diversified domestic + offshore |

| Meiji Yasuda (明治安田) | 1881 / merged 2004 | ¥45-50 trillion | Captive sales force, corporate channel | Group / corporate-heavy |

| Japan Post Insurance (かんぽ生命) | 2007 (predecessor 1916) | ¥60-70 trillion | ~24,000 post offices | Rural, elderly, small policies |

| Sumitomo Life (住友生命) | 1907 | ¥35-40 trillion | Captive sales force, digital push (Vitality) | Mid-market, health-focus |

What distinguishes Kampo from the other majors is not asset size — at roughly ¥60-70 trillion it sits in the same weight class as Dai-ichi — but channel architecture. The private Big Three rely on captive sales forces of insurance ladies (生保レディー, seiho lady), a postwar Japanese institution in which mostly female agents cultivate long-term relationships with workplace clients. Kampo, by contrast, has no such force. Its products reach customers via Japan Post Co.’s postal employees, who sell insurance as one of several over-the-counter financial services alongside savings deposits, money transfers, and parcel delivery. This makes Kampo simultaneously the most physically distributed insurer in Japan and the one most dependent on a sister company it does not control.

Asset management: the bond portfolio that ate the budget

Behind the consumer story sits an equally important institutional one. Like its peers, Kampo runs an enormous bond-dominated investment portfolio funded by long-dated policy liabilities. Historically, this portfolio leaned overwhelmingly on Japanese Government Bonds (JGBs). When the Bank of Japan pinned ten-year yields close to zero from 2016 onward under yield curve control, life insurers’ net investment income compressed sharply. Kampo responded, as did its competitors, by shifting incremental allocation into foreign bonds (often hedged), foreign equities, and alternative assets — private credit, infrastructure, real estate.

The BoJ’s 2024 exit from negative interest rates, and the subsequent gradual rise in JGB yields, has begun to reverse this squeeze. For Kampo, whose liability duration is among the longest in the industry given its whole-life-heavy book, the slow normalization of Japanese yields is a structural positive — though it also creates mark-to-market pain on legacy bond holdings. The 2024-2027 medium-term plan published by the company outlines a continued cautious diversification, with selective increases in credit risk and overseas allocations, alongside a tighter focus on asset-liability management discipline.

The 2024-2027 reform agenda

Six years after the scandal, the rebuilding work continues — visibly in compliance, less visibly in distribution economics. Three threads matter for understanding where Kampo is heading.

First, sales force restructuring. Japan Post Co.’s salespeople still account for the dominant share of new business, but the commission and incentive structure has been rebuilt to reward customer retention and suitability rather than gross new contract counts. Independent compliance monitoring, alien to the post-office culture before 2019, is now embedded in the sales process. The trade-off is productivity: sales per branch have not returned to pre-scandal levels, and Kampo’s management is openly debating whether the postal channel alone can support its growth ambitions.

Second, digital and direct channels. Kampo has begun building online application flows for simpler products — initially educational endowments and entry-level whole life — alongside a smartphone application for existing policyholders. The strategic ambition is modest by global standards: digital is positioned as a complement to the post office, not a replacement. But it is a meaningful departure for an insurer whose entire identity, until very recently, was synonymous with the physical counter.

Third, capital and ownership. Japan Post Holdings has gradually reduced its stake in Kampo through secondary offerings, partly to fund its broader strategic investments and partly under government pressure to complete privatization. Each reduction loosens the institutional linkage between Kampo and the postal network, raising — quietly but persistently — the question of whether the two should one day separate altogether. For now, the integrated structure remains, but the direction of travel is clear.

What Kampo means for foreign partners

For non-Japanese asset managers, technology vendors, reinsurers, and corporate buyers, Kampo is one of the most distinctive — and underexplored — counterparties in Japanese finance. Three angles bear watching.

For asset managers, the ¥60-70 trillion portfolio is a meaningful allocator into foreign credit, foreign equities, and alternatives. Mandates tend to be large, long-dated, and awarded after careful institutional due diligence. Global firms with strong ESG, infrastructure, or private credit platforms have been the principal beneficiaries.

For insurtech and compliance technology vendors, the post-scandal rebuilding has created unusual openness to outside ideas. Tools for sales suitability monitoring, policyholder communication, and digital onboarding have all moved up the procurement priority list in ways that would have been unthinkable a decade ago.

For reinsurers, Kampo’s policy book — heavily individual, long-dated, with relatively predictable mortality — is in principle an attractive cedent, although reinsurance penetration in Japanese life remains low by global standards. Negotiations tend to be slow, relationship-driven, and undertaken with the long view.

The thread tying these threads together is institutional patience. Kampo does not move fast. Decisions take time, hierarchies are deep, and the cultural memory of 2019 remains fresh enough that compliance considerations dominate every new partnership conversation. For partners willing to invest in the relationship, however, the rewards can be considerable — both in asset scale and in the symbolic credibility that comes from doing business with one of Japan’s most recognizable institutions.

FAQ

When was Japan Post Insurance founded?

The current entity, Japan Post Insurance Co., Ltd. (株式会社かんぽ生命保険), was established in October 2007 as part of the Japan Post privatization. Its institutional predecessor, the Postal Life Insurance system, dates to 1916.

What was the 2019 mis-selling scandal?

Between approximately 2014 and 2019, Japan Post Co. and Japan Post Insurance salespeople systematically converted existing customer policies — often held by elderly customers — into new contracts in ways that disadvantaged the customer. The Financial Services Agency issued a business improvement order in late September 2019, Japan Post Co. suspended insurance sales activity for three months, and the presidents of all three Japan Post group companies resigned.

How large is Japan Post Insurance compared with other Japanese life insurers?

Kampo is Japan’s fourth-largest life insurer by total assets, with approximately ¥60-70 trillion under management. Nippon Life remains the largest, followed by Dai-ichi Life and Meiji Yasuda.

How does Kampo distribute its products?

Kampo sells primarily through approximately 24,000 post offices nationwide, operated by sister company Japan Post Co. This is unique among Japan’s major life insurers, all of which rely on captive sales forces rather than a post-office network.

Is Japan Post Insurance publicly listed?

Yes. Kampo was listed on the Tokyo Stock Exchange in November 2015 as part of the “triple IPO” of Japan Post Holdings, Japan Post Bank, and Japan Post Insurance. Its ticker is 7181. Japan Post Holdings retains majority ownership, although the stake has been progressively reduced through secondary offerings.

Working with Japan Post Insurance

Japonity connects international asset managers, insurtech providers, reinsurers, and corporate partners with Japan’s most strategically significant financial institutions. If you are evaluating a partnership, investment mandate, or vendor relationship with Japan Post Insurance — or with any of its peers among Japan’s life insurance majors — our editorial and matching team can help you map the right entry point, understand the institutional culture, and structure a credible first conversation. Visit /business-matching/ to start the discussion.

Related from Japonity — Japan Post Group

- Japan Post Holdings — The half-privatized postal-banking-insurance empire

- Japan Post Bank — Japan’s largest savings bank — Asia’s biggest deposit-funded allocator

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →