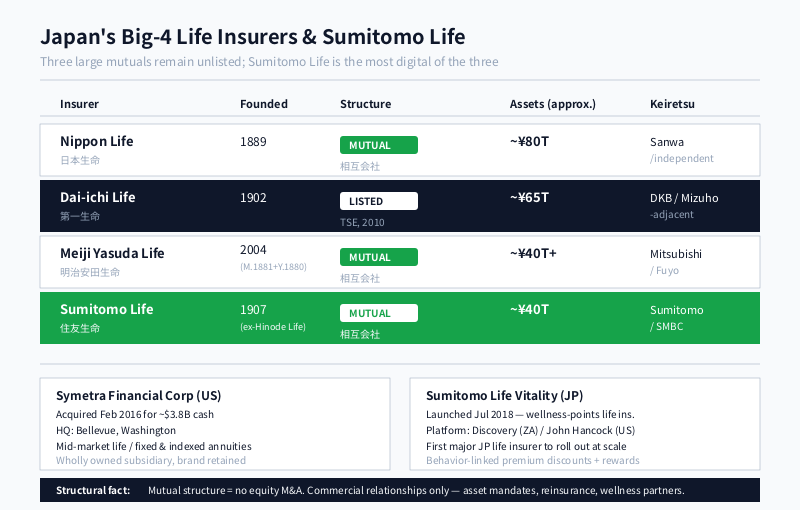

In February 2016, Sumitomo Life Insurance Company paid approximately 3.8 billion US dollars in cash for Symetra Financial Corporation, a mid-market US life insurer and annuities provider based in Bellevue, Washington. The deal — modest by global insurance-M&A standards but transformational for the buyer — gave Japan’s fourth-largest life insurer its first material US insurance footprint. Eight years on, Sumitomo Life holds approximately forty trillion yen in total assets, remains a mutual company (相互会社) alongside Nippon Life and Meiji Yasuda Life, and has emerged as the most visibly digital of Japan’s three large mutual holdouts — most prominently through its 2018 launch of Vitality, the wellness-points insurance program originally developed by Discovery Health of South Africa and distributed in North America by John Hancock. The combination of mutual structure, mid-cap US subsidiary, and behavior-linked underwriting makes Sumitomo Life the most distinctive of Japan’s “Big Four” life insurers, and the one whose strategic choices most clearly preview where the mutual life sector is heading.

From Sumitomo zaibatsu sideline to “Big Four” mutual

Sumitomo Life Insurance Company traces its origin to 1907, when it was founded in Osaka as Hinode Life Insurance (日之出生命保険) under the broader umbrella of the Sumitomo zaibatsu — the centuries-old merchant house whose copper, banking, and industrial businesses had, by the late Meiji period, become one of Japan’s four great prewar conglomerates. The firm was renamed Sumitomo Life Insurance in 1925, formally aligning its branding with the family name, and grew through the prewar period as the insurance arm of one of Japan’s most diversified industrial groups.

The postwar SCAP-era zaibatsu dissolution scattered the Sumitomo combine into independent companies, but the Sumitomo brand — and the dense web of cross-shareholdings and main-bank relationships among the successor firms — survived as one of Japan’s “Big Six” postwar keiretsu. Sumitomo Life sat inside that grouping alongside what is now Sumitomo Mitsui Banking Corporation (SMBC), Sumitomo Corporation, Sumitomo Chemical, NEC, Sumitomo Metal Industries (now part of Nippon Steel), and others. Through the high-growth period, Sumitomo Life’s distribution rode the expansion of the Sumitomo industrial base — corporate group life policies sold into Sumitomo group companies, individual life sold through a captive sales-representative channel that today numbers roughly forty thousand staff.

By the 2000s, the operating environment had narrowed sharply. Japan’s life-insurance industry had passed through several mid-sized firm failures in the late 1990s; demographics had turned against domestic premium growth; and ultra-low JGB yields were compressing the margin between credited rates and investment returns. Sumitomo Life entered the 2010s as the fourth-largest life insurer in Japan — behind Nippon Life, Dai-ichi Life, and the merged Meiji Yasuda Life — and the one with the smallest overseas presence relative to balance sheet size.

The “Big Four” and the three mutual holdouts

Japan’s life insurance sector is unusual among large developed markets in that its biggest carriers are not joint-stock corporations but mutual companies — legally owned, in principle, by their policyholders. Of the four largest, three remain mutuals; only Dai-ichi Life broke ranks, demutualizing and listing on the Tokyo Stock Exchange in 2010.

| Insurer | Founded | Structure | Approx. total assets | Keiretsu / lineage |

|---|---|---|---|---|

| Nippon Life | 1889 | Mutual (相互会社) | ~¥80T | Sanwa / independent |

| Dai-ichi Life | 1902 | Joint-stock (TSE-listed, 2010) | ~¥65T | DKB / Mizuho-adjacent |

| Meiji Yasuda Life | 2004 (Meiji 1881 + Yasuda 1880) | Mutual (相互会社) | ~¥40T+ | Mitsubishi / Fuyo |

| Sumitomo Life | 1907 | Mutual (相互会社) | ~¥40T | Sumitomo / SMBC |

For foreign counterparties evaluating any of the three remaining mutuals — Nippon Life, Meiji Yasuda, or Sumitomo Life — the mutual-versus-listed distinction is the single most consequential structural fact in the conversation. Listed insurers operate under continuous public-market discipline: quarterly earnings calls, equity-financed M&A, total-shareholder-return-linked executive compensation, and the perpetual possibility of activist intervention. Mutuals operate under none of these constraints. Capital is raised through retained surplus, subordinated debt, and — in Japan’s mutual case — a specific form of kikin (基金) funding from institutional partners. “Shareholders” are policyholders, who vote indirectly through a representative assembly (総代会). The planning horizon is measured in decades rather than quarters.

What this means for any foreign counterparty approaching Sumitomo Life is straightforward: equity-level transactions with the holding entity are not on the menu, and will not be in any reasonable planning horizon. Commercial relationships — sub-advisory mandates, reinsurance treaties, distribution partnerships, technology contracts — are. Overseas capital deploys through wholly owned subsidiaries, not minority equity positions.

Symetra: the 2016 US foothold

The clearest expression of that pattern is the Symetra Financial Corporation acquisition, completed on 1 February 2016. Sumitomo Life paid approximately 3.8 billion US dollars in cash for Symetra, a mid-cap US insurance holding company based in Bellevue, Washington, whose primary business sits across mid-market individual life insurance, retirement annuities (fixed and indexed), and a smaller group benefits book sold to US employers. Symetra had been a publicly traded company on the New York Stock Exchange; the deal took it private under Sumitomo Life ownership and de-listed the shares.

The strategic logic mirrors the template visible across the three large mutuals’ overseas moves. Symetra was not a turnaround target. It was a stable mid-cap US carrier with a mid-market product mix that complemented — rather than overlapped with — Sumitomo Life’s domestic Japanese book. Three things the Japanese parent could not generate at home came with the deal: a US dollar–denominated regulated insurance balance sheet, access to the depth of the US fixed-income market for asset-liability matching against the acquired annuity liabilities, and a beachhead in indexed annuities — a product category virtually absent from Japan’s individual life market. The Symetra brand, management team, and Bellevue operations were retained intact.

For Sumitomo Life, the Symetra acquisition was structurally similar in shape to its mutual peers’ overseas deals (Meiji Yasuda’s StanCorp purchase, Nippon Life’s MLC Australia investment): wholly owned, specialist-complementary, brand-preserved. A decade on, Symetra continues to operate from Bellevue under its own name with an expanded indexed-annuity product line, and remains Sumitomo Life’s largest overseas business by a wide margin.

Vitality: the wellness-points pivot

If Symetra defines the geographic shape of Sumitomo Life’s overseas strategy, Vitality defines the more interesting question of where its domestic product is heading. In July 2018, Sumitomo Life launched “Sumitomo Life Vitality” in Japan — a behavior-linked life insurance program built on the Vitality platform originally developed by Discovery Health of South Africa in the 1990s and licensed internationally to John Hancock in the United States, Manulife in Canada, Generali in Europe, and AIA across Asia.

The model is straightforward in concept and operationally complex in execution. Policyholders enroll in a wellness program attached to their life insurance contract. They earn points for measurable healthy behaviors — verified gym visits, step counts logged through wearable devices, annual health checkups, smoking cessation, and similar. Points accumulate into status tiers (Bronze through Platinum), which translate into premium discounts, gift-card rewards, and partner-merchant benefits. The insurer, in theory, receives a healthier book of policyholders whose lower mortality and morbidity over time more than offsets the cost of the rewards. The policyholder receives ongoing financial reinforcement for behaviors that would have benefited them anyway. The wearable and gym-chain partners receive verified, premium-segment customers.

Sumitomo Life was the first major Japanese life insurer to roll out a full wellness-points program at scale, and the launch was structured as a partnership with Discovery (which provides the underlying Vitality platform and analytics) rather than a wholly owned proposition. By the early 2020s, Vitality had become Sumitomo Life’s flagship individual product line, with millions of enrolled members and a steadily expanding partner ecosystem covering fitness chains, drugstores, and health-data platforms. The firm has subsequently added Medibloc Network and other medical-data alliances, positioning itself — among the three Japanese mutual holdouts — as the most digitally forward.

For foreign partners, Vitality matters in two ways. First, it has established Sumitomo Life as the natural counterparty in Japan for any global health-data, wearables, or wellness-rewards platform looking for a Japanese life-insurance integration partner. Second, it signals where the broader mutual life sector is likely to follow: from passive risk-pooling to active behavior modification, with the insurer’s data infrastructure and partner ecosystem becoming as strategically important as the actuarial book itself.

The investment portfolio: matching ~¥40T of liabilities

Approximately forty trillion yen in total assets sits behind Sumitomo Life’s policyholder liabilities — a general-account portfolio whose composition broadly mirrors its mutual peers. The dominant allocation is to Japanese government bonds for duration-matching against long-dated life liabilities, followed by foreign bonds (predominantly US treasuries and high-grade US dollar credit, with hedge ratios that vary with the USD-JPY interest-rate differential), domestic and foreign equities, and a growing tail in alternatives — private equity, private credit, infrastructure, and real estate.

For foreign asset managers, this is the most commercially accessible point of engagement with Sumitomo Life. Japanese mutual life insurers are among the most coveted limited-partner relationships in global private markets: long-dated capital, low redemption pressure, and ticket sizes that meaningfully move a fund’s close. Competition for those mandates is intense, gatekeeper bars are high (multi-cycle audited track records, ESG documentation, Japanese-language reporting where the relationship demands it), and the relationship arc is measured in years. But unlike the holding entity, which cannot be invested in, the general account is open for business to managers who clear the diligence threshold.

The yen-hedging cost on the foreign-bond book has been the dominant tactical variable for Japanese life insurer general accounts since the 2022 monetary-policy divergence widened the USD-JPY rate gap. Elevated hedge costs push allocations toward unhedged foreign bonds, domestic credit, and alternatives; compressed hedge costs reverse the flow. Foreign managers pitching Sumitomo Life — like Nippon Life and Meiji Yasuda — should expect any conversation to include a granular view on hedge-regime resilience, not just headline returns.

Distribution, group business, and the SMBC connection

Domestically, Sumitomo Life distributes through two overlapping channels. The first is its own captive sales-representative force — the “life planner” model common to all four Big Four insurers, with roughly forty thousand sales staff (営業職員) selling individual life, medical, and savings-type policies on a household-by-household basis. The second is bancassurance: insurance products sold through retail bank branches, an arrangement liberalized in Japan in stages between 2001 and 2007.

The Sumitomo lineage gives the firm a privileged shelf position with SMBC Group — Sumitomo Mitsui Banking Corporation, SMBC Trust, and the broader SMBC retail and private-banking architecture. The shelf is not exclusive, but the keiretsu adjacency remains a structural advantage, and the Sumitomo Life / SMBC relationship is one of the most institutionally embedded distribution arrangements in Japanese financial services.

Beyond individual life, Sumitomo Life operates a significant group life and group pension business sold to Japanese corporate employers — particularly within the Sumitomo group’s industrial perimeter — making it one of the larger institutional channels into Japan’s defined-benefit and defined-contribution corporate retirement market.

Leadership and governance

Sumitomo Life is led by President Yasuhiro Takagi, who succeeded Yukio Sakamoto (now chairman) as the firm’s chief executive in recent years. Governance follows the standard Japanese mutual template: a representative assembly of policyholders (総代会) elects directors, who in turn appoint the executive team. The board includes outside directors in line with the corporate-governance code applied to large mutual insurers, and Sumitomo Life has progressively expanded outside-director representation and committee independence over the past decade.

The resulting governance system is, by design, slower-moving and more consensus-oriented than at a listed insurer — but also more insulated from quarterly market noise. Multi-year capital-deployment commitments (Symetra; the Vitality build-out) can be sustained through cycles that would draw activist attention at a listed peer. Foreign counterparties should plan for relationship-led, multi-year engagement.

What it means for foreign partners

For a foreign reinsurer, asset manager, distribution partner, wearable / health-data platform, or technology vendor evaluating Sumitomo Life Insurance Company, three structural realities frame everything that follows.

First, the firm is a mutual and will remain so for the foreseeable future. Equity-level transactions — minority stakes, joint-venture equity in the holding entity, public-market financing — are not on the menu. Commercial relationships are.

Second, overseas capital deployment runs through wholly owned subsidiaries, with Symetra as the cornerstone template and any subsequent move likely to follow the same shape: specialist-complementary, brand-preserved, mid-cap rather than mega-cap, fully integrated under Tokyo-Osaka capital governance but operationally autonomous. A foreign insurer hoping to be acquired by Sumitomo Life is in a different conversation from one hoping to reinsure its business or co-invest alongside it.

Third, the firm’s Vitality position makes it the natural — and in some respects only — Japanese life-insurance counterparty for global wellness platforms, wearable manufacturers, and health-data infrastructure providers. The product roadmap implied by Vitality runs further into behavior-linked underwriting, data-platform partnerships, and corporate wellness distribution than any of its mutual peers have yet committed to. Foreign technology partners with a relevant capability should expect Sumitomo Life to be the most receptive of Japan’s three mutual holdouts.

Within those constraints, Sumitomo Life is one of the most consequential institutional capital pools in Japan, with a demonstrated cross-border execution track record (Symetra), a distinctive domestic product franchise (Vitality), and a long planning horizon that rewards partners willing to invest in the relationship.

FAQ

When was Sumitomo Life founded and what is its keiretsu lineage?

Sumitomo Life Insurance Company was founded in 1907 in Osaka as Hinode Life Insurance (日之出生命保険) under the broader Sumitomo zaibatsu, and renamed Sumitomo Life Insurance in 1925. It sits inside the postwar Sumitomo keiretsu alongside SMBC (Sumitomo Mitsui Banking Corporation), Sumitomo Corporation, Sumitomo Chemical, and the other Sumitomo-affiliated firms, and is one of Japan’s “Big Four” life insurers by total assets.

Is Sumitomo Life publicly listed?

No. Sumitomo Life remains a mutual company (相互会社), legally owned by its policyholders rather than by shareholders, and is not listed on the Tokyo Stock Exchange or any other exchange. It is one of three large Japanese life insurers — alongside Nippon Life and Meiji Yasuda Life — that have declined to demutualize. Dai-ichi Life is the only one of Japan’s “Big Four” to have listed (in 2010).

What is the Symetra Financial Corporation acquisition?

In February 2016, Sumitomo Life completed the acquisition of Symetra Financial Corporation, a Bellevue, Washington–based US insurance holding company, for approximately 3.8 billion US dollars in cash. Symetra’s primary businesses are mid-market individual life insurance, retirement annuities (fixed and indexed), and group benefits sold to US employers. Symetra continues to operate under its own brand from Bellevue as a wholly owned subsidiary, and remains Sumitomo Life’s largest overseas business.

What is Sumitomo Life Vitality?

Sumitomo Life Vitality is a behavior-linked life insurance program launched in Japan in July 2018, built on the Vitality wellness platform originally developed by Discovery Health of South Africa and licensed globally to partners including John Hancock (US), Manulife (Canada), Generali (Europe), and AIA (Asia). Policyholders earn points for verified healthy behaviors — gym visits, step counts, health checkups, smoking cessation — which translate into premium discounts and partner-merchant rewards. Sumitomo Life was the first major Japanese life insurer to roll out a full wellness-points program at scale.

How can a foreign company partner with Sumitomo Life?

The most accessible commercial channels for foreign counterparties are asset-management mandates (sub-advisory and direct allocations from the general account), reinsurance and retrocession on the individual and group life books, wellness and health-data partnerships into the Vitality platform, and technology / service provision to the firm’s insurance operations. Equity-level transactions with the holding entity itself are not available given Sumitomo Life’s mutual structure; relationships are commercial and typically multi-year in nature.

Working with Sumitomo Life

Japonity helps foreign reinsurers, asset managers, wellness and health-data platforms, and capital-markets counterparties navigate Japan’s three remaining large mutual life insurers — Sumitomo Life among them — where keiretsu lineage, mutual-company structure, and multi-year relationship cycles shape every commercial conversation. If your firm is evaluating a Japanese institutional relationship or a Vitality-adjacent wellness partnership, visit our business matching page to be introduced to the right counterparties.

Related from Japonity — Japan’s life insurers

- Dai-ichi Life Holdings — Japan’s largest listed life insurer — Protective Life US, TAL Australia

- Nippon Life Insurance — Japan’s largest life insurer — the unlisted mutual giant

- Meiji Yasuda Life — Japan’s #3 life insurer — mutual holdout, StanCorp US

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →