Walk down Ginza’s Chuo-dori on a Saturday afternoon, or push through the rush-hour crowds at Shinjuku’s east exit, and the brightest object on the street is almost certainly the same one: a vivid yellow and blue storefront with the letters MatsuKiyo stamped across it. To Tokyoites the colour is unremarkable urban furniture. To the tens of millions of foreign tourists who pass through Japan each year, it is something closer to a landmark. Matsumoto Kiyoshi — founded as a single pharmacy in 1932 in Matsudo, Chiba, by a young pharmacist named Kiyoshi Matsumoto — has become the most internationally recognisable name in Japan’s roughly ¥9 trillion drugstore market, the tourist-channel anchor of a sector otherwise dominated by suburban dispensing pharmacies. In October 2021, after a two-year process, Matsumoto Kiyoshi completed a full integration with Cocokara Fine, a younger but similarly cosmetics-skewed rival, forming Matsukiyo Cocokara & Co. The combined group — approximately 3,300 stores, ¥0.96 trillion in revenue and a Tokyo Stock Exchange listing under code 3088 — was briefly the largest Japanese drugstore by sales. The throne did not last long. The 2024-announced Welcia–Tsuruha integration, both Aeon Group subsidiaries, is on track to overtake it by 2027. What remains, however, is a uniquely positioned franchise: not the largest, but the one foreign visitors actually walk into.

From a Matsudo pharmacy to the yellow signage of Ginza

Matsumoto Kiyoshi’s founding story is unusually clean for a Japanese listed company. In 1932, in the small commuter town of Matsudo in Chiba Prefecture across the Edo River from Tokyo, a 22-year-old pharmacist named Kiyoshi Matsumoto opened Matsumoto Yakkyoku, a single-counter neighbourhood pharmacy. The business was small, family-run and locally focused — there were thousands of such pharmacies across pre-war Japan, and few of them survived the war and the post-war reorganisation of the country’s medical and retail systems. Matsumoto Yakkyoku did, partly because its founder doubled as Matsudo’s mayor in the 1960s and 1970s and partly because the next generation of the family, led by Kazuo Matsumoto, made the leap from a single pharmacy to a chain in the 1970s and 1980s.

The strategic break came in the 1990s. While most Japanese pharmacy chains were chasing dispensing-pharmacy volume — driven by the Ministry of Health’s separation-of-dispensing-and-prescribing reform — Matsumoto Kiyoshi made the opposite bet. It would lean heavily into cosmetics, beauty, hair care, health food and over-the-counter medicine, and it would do so in dense urban locations rather than suburban roadside lots. In 1994 the company rolled out what would become its signature visual identity: bright yellow shopfronts with a blue MatsuKiyo logo, designed to be loud, cheap to fabricate and impossible to miss from a hundred metres away. By the late 1990s a generation of young Japanese women had begun to use “MatsuKiyo” the way Americans used “the drugstore” — as a generic noun for affordable beauty. The Tokyo Stock Exchange listing followed in 1996, and through the 2000s Matsumoto Kiyoshi grew into the most profitable Japanese drugstore by operating margin, with the highest-traffic urban stores in the country. By 2019, on the eve of the merger, visitors from Greater China and South-East Asia were already accounting for a meaningful share of revenue at flagship urban stores — a structural exposure no other major Japanese drugstore came close to matching.

Cocokara Fine and the 2021 merger

The other half of Matsukiyo Cocokara & Co. has a more complicated lineage. Cocokara Fine itself was created in 2008 through the merger of two listed drugstore operators — Seijo (the operator of the Seijo and Segami chains in eastern Japan) and Sapporo Drug Store — and was later joined by Iwasaki Industries’ Drug Iwasaki business and Higuchi Industries’ Higuchi drugstore network. The corporate logic was straightforward: none of the constituent chains was large enough on its own to compete with the top tier of Welcia, Tsuruha, Sundrug or Matsumoto Kiyoshi, but together they could form a credible fifth or sixth chain with national footprint. By the late 2010s, Cocokara Fine operated roughly 1,300 stores under several banners, with particular density in western Japan and a similar cosmetics-and-urban skew to Matsumoto Kiyoshi.

The integration with Matsumoto Kiyoshi was announced in August 2019 as a basic agreement, then put through a two-year process of regulatory clearance and governance design. The formal business combination was completed in October 2021 under a new holding-company structure named Matsukiyo Cocokara & Co., with the existing Matsumoto Kiyoshi Tokyo Stock Exchange listing (code 3088) carried forward. Head office is in Shinjuku, Tokyo. The two operating brands — Matsumoto Kiyoshi and Cocokara Fine — were retained at the store level, partly because the Cocokara banner has strong recognition in western Japan and partly because the cost of a single-brand consolidation across 3,000-plus outlets would have been significant. At the moment of merger, the combined group reported approximately 3,300 stores, ¥0.96 trillion in revenue, and roughly 36,000 employees. By revenue, it was briefly number one. The achievement did not last.

The drugstore top tier, before and after the Welcia–Tsuruha merger

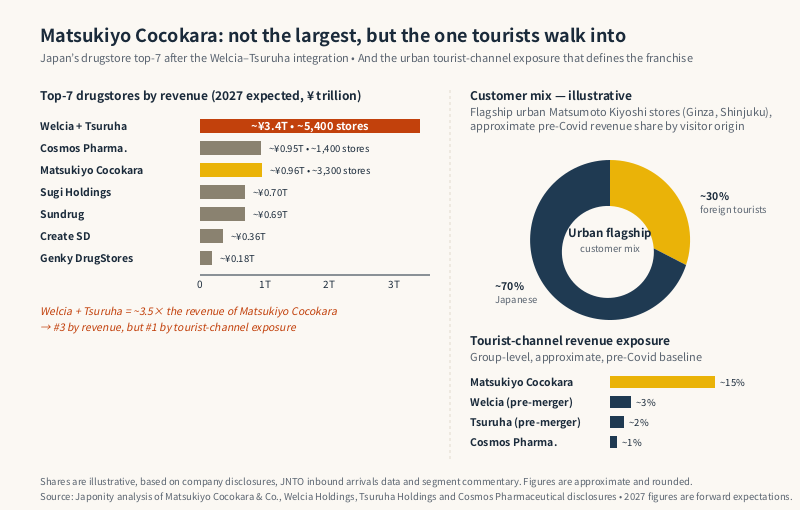

Japan’s drugstore industry contains a peculiar fact: seven national chains, none with more than roughly 15% market share, and a long tail of regional operators. The top tier — Welcia, Tsuruha, Matsukiyo Cocokara, Cosmos, Sugi, Sundrug, Create SD — has been racing on store openings and dispensing-pharmacy economics for two decades. The 2021 Matsumoto Kiyoshi–Cocokara Fine merger reset the field by creating the first chain with more than ¥0.9 trillion in revenue. The 2024 Welcia–Tsuruha announcement will reset it again — this time by a much larger margin.

| Position (2027 expected) | Chain | Approx. stores | Approx. revenue (¥ trillion) | Defining strategy |

|---|---|---|---|---|

| 1 | Welcia + Tsuruha (merged) | ~5,400 | ~3.4 | Suburban dispensing-pharmacy, Aeon-anchored |

| 2 | Cosmos Pharmaceutical | ~1,400 | ~0.95 | Kyushu base, food-discounter model |

| 3 | Matsukiyo Cocokara & Co. | ~3,300 | ~0.96 | Urban cosmetics + tourist channel |

| 4 | Sugi Holdings | ~1,700 | ~0.70 | Tokai region, dispensing-pharmacy heavy |

| 5 | Sundrug | ~1,400 | ~0.69 | Tokyo and Kansai urban density |

| 6 | Create SD Holdings | ~750 | ~0.36 | Kanagawa and Shizuoka |

| 7 | Genky DrugStores | ~500 | ~0.18 | Hokuriku, food-led roadside |

Two points are worth pulling out from the table. The first is that by store count Matsukiyo Cocokara is and will remain the largest, with roughly 3,300 stores across the two banners. By revenue, however, the Welcia–Tsuruha combination will be more than three times larger by 2027, and Cosmos Pharmaceutical — a Kyushu-headquartered chain that has invested heavily in a low-price, food-heavy roadside model — is likely to creep ahead in some years on top-line. The second is that of the top three, only Matsukiyo Cocokara has a strategy structurally tied to the inbound-tourist economy. Welcia–Tsuruha sells dispensing volume to the suburban over-65 cohort. Cosmos sells discount food and household goods to price-conscious local shoppers. Matsukiyo Cocokara sells cosmetics, sunscreen, prestige skincare and souvenirs to a customer base that is roughly a third foreign in its flagship urban stores.

Why the tourist channel is a moat, not a vulnerability

It is easy to mistake exposure to foreign tourists as a structural weakness — a beta exposure to a volatile, sentiment-driven flow. The pandemic appeared to confirm that view. Between 2020 and 2022, inbound tourist arrivals to Japan collapsed by more than 95%, and Matsukiyo Cocokara’s urban flagship stores took a disproportionate hit. The merger had been completed in October 2021, in the middle of that downturn, and analysts at the time questioned whether the strategic logic still held.

By 2024 the answer was unambiguous: yes, and more so. Inbound tourism rebounded faster than almost any forecaster had predicted, helped by yen weakness, post-pandemic pent-up demand and the loosening of visa rules for Chinese, South-East Asian and Indian visitors. Japan was receiving more than 30 million foreign visitors a year, on track for the government’s 60 million target by 2030. These visitors come with shopping lists. Japanese cosmetics and skincare — the Shiseido, DHC, Hada Labo, Curél, Anessa, Biore and Senka categories that fill Matsukiyo Cocokara’s beauty aisles — have become a structural export channel in their own right, executed entirely through inbound retail.

What makes this moat durable is not the absolute volume of tourist spending, which can fluctuate, but the structural distribution of those tourists. Roughly two-thirds of foreign visitors to Japan pass through one of three locations — central Tokyo, Osaka–Kyoto and Fukuoka — and within those locations the highest-density retail corridors are dominated by Matsumoto Kiyoshi outlets, often within fifty metres of major rail interchanges. Tax-free counters, multilingual signage, Chinese and Korean-speaking staff, dedicated souvenir corners — all of these are operating-model assets that took the company more than a decade to build. The Welcia–Tsuruha combination, even at three times the revenue, will have a fraction of this tourist-channel exposure simply because its store network is suburban.

The private-label engine: MK Customer Co and Cocokara MS

Tourist exposure alone would not justify the valuation. The second pillar of Matsukiyo Cocokara’s profitability is its private-label programme — built first under the MK Customer Co (MKC) brand at Matsumoto Kiyoshi, and now extended through Cocokara MS at the legacy Cocokara stores. Private-label penetration is high by Japanese drugstore standards, with hundreds of SKUs across cosmetics, skincare, oral care, hair care, basic OTC, supplements and household categories. The economics are straightforward: private-label products, manufactured under contract by the same factories that supply national brands, retain a much larger share of the retail price for the retailer. Penetration of even 20% private label in beauty and personal care can shift a drugstore’s blended gross margin by hundreds of basis points, and the MKC and Cocokara MS programmes are a key reason the chain’s operating margin sits comfortably above the Japanese drugstore average.

The private-label proposition has also become a tourist-marketing asset. Visitors arriving with Chinese-language shopping lists curated on Xiaohongshu, RED or Douyin increasingly know the MKC brand by name, and certain hero SKUs — sheet masks, eye-care patches, Q10 serums, hair-treatment products — circulate as recommended items inside cross-border social-commerce communities. Matsumoto Kiyoshi has begun selling selected MKC products directly into China, Taiwan and South-East Asia through cross-border e-commerce partnerships, turning a domestic retail brand into a thin export channel without giving up the in-store discovery loop that drives most of the volume.

How Matsukiyo Cocokara differs from the Welcia-Tsuruha model

The simplest way to understand Matsukiyo Cocokara is to put it directly alongside the Welcia–Tsuruha integration that is now consolidating beneath the Aeon umbrella. Both businesses are technically drugstores. They share regulatory frameworks, supplier relationships, dispensing reimbursement codes and the same broad Japanese consumer base. But the underlying strategies are almost mirror opposites.

The Welcia–Tsuruha model is rural and suburban in its centre of gravity. Stores are 1,500 to 2,000 square metres, sit on roadside lots with their own parking, anchor or co-anchor Aeon-affiliated shopping zones, and run an unusually high ratio of in-store dispensing pharmacies — roughly half at Welcia, somewhat lower at Tsuruha. The customer base skews older, more price-sensitive on food and household goods, and almost entirely Japanese. Aeon Group, as majority shareholder, provides loyalty integration through WAON and supply-chain support through Topvalu private-label products. The bet is on Japan’s structural aging.

The Matsukiyo Cocokara model is urban and tourist-anchored. Stores are typically 400 to 800 square metres, on prime high-street frontage in Ginza, Shinjuku, Shibuya, Umeda, Namba and Dotonbori. Dispensing-pharmacy penetration is much lower — roughly a quarter of stores carry a prescription counter — because the floor space is too expensive to allocate to a slow-turn, regulated category. Cosmetics, fragrance, skincare and prestige hair care take pride of place. The customer mix tilts heavily young, female, and during peak inbound years foreign. The bet is on Japan’s cultural pull on the rest of Asia.

Neither bet is wrong. They are different bets, on different demographic flows. For overseas brands evaluating Japan-market entry, the choice between approaching Matsukiyo Cocokara and approaching Welcia–Tsuruha is therefore not a question of scale but of audience. A premium Korean cosmetics brand, a European indie skincare line, a souvenir-suitable confectionery or a high-margin supplement targeting Asian-tourist demand belongs on Matsukiyo Cocokara’s shelves. A daily-essential household brand, a generic OTC line or a dispensing-pharmacy adjacency belongs in the Welcia–Tsuruha network.

Governance, leadership and capital markets

Matsukiyo Cocokara is listed on the Prime Market of the Tokyo Stock Exchange under code 3088, the legacy Matsumoto Kiyoshi listing carried into the merged structure. The company is professionally managed, with the Matsumoto family retaining a meaningful minority stake and historical influence through the founding lineage. Yukihiro Iwabuchi has been identified in recent disclosures as group president, though management roles have evolved as the integration matured. From a capital-markets perspective, Matsukiyo Cocokara has long been one of the most foreign-investor-followed names in the Japanese drugstore segment, partly because its cosmetics and inbound-tourist exposure are easy to model in Western analyst frameworks. Trading multiples have at various points reflected a premium to suburban-drugstore peers, with valuation tracking inbound-tourism arrivals and yen exchange rates as much as same-store sales numbers. The 2027 reset of the league table, with Welcia–Tsuruha overtaking on revenue, is well-flagged to the market and is unlikely on its own to compress the multiple. What matters more, for the share price, is whether tourist arrivals continue their post-Covid expansion and whether private-label penetration keeps climbing.

FAQ

Is Matsukiyo Cocokara the largest Japanese drugstore?

By store count, yes — Matsukiyo Cocokara operates roughly 3,300 stores across the Matsumoto Kiyoshi and Cocokara Fine banners, more than any other domestic chain. By revenue, at approximately ¥0.96 trillion it was briefly number one immediately after the 2021 merger but currently sits roughly in third place behind Welcia and Tsuruha, and once those two complete their announced integration around 2027 the combined Welcia–Tsuruha entity will be more than three times larger on revenue, pushing Matsukiyo Cocokara to a clear third position. By tourist-channel exposure, however, Matsukiyo Cocokara remains the segment leader by a wide margin.

What is the difference between Matsumoto Kiyoshi and Cocokara Fine stores?

Both are operating brands of Matsukiyo Cocokara & Co. after the 2021 merger. Matsumoto Kiyoshi, identified by its yellow-and-blue signage, is the older and larger brand with particular strength in eastern Japan and the central Tokyo tourist corridors. Cocokara Fine is the surviving consumer-facing identity of the 2008 Cocokara Fine merger that combined the Seijo, Segami and several other chains, with stronger density in western Japan. The two banners are kept distinct partly because of regional brand recognition and partly because consolidating signage and store layouts across more than 3,000 outlets would carry significant cost and disruption. Behind the scenes, supply chain, private label and back office have been progressively integrated.

Why is Matsukiyo Cocokara so visible to foreign tourists?

The chain pursued an urban high-street strategy from the 1990s onward, opening flagship locations in Ginza, Shinjuku, Shibuya, Umeda and Dotonbori at a time when most Japanese drugstores were chasing suburban roadside footprint. The bright yellow signage, designed in 1994, was deliberately loud and easy to spot from a distance. As inbound tourism scaled up in the 2010s — driven by visa relaxation, low-cost airlines and yen weakness — those urban stores happened to be sitting directly on the highest-traffic tourist walking corridors, and the chain invested heavily in tax-free counters, multilingual staffing and tourist-curated assortments. The result is that Matsumoto Kiyoshi is, for many foreign visitors, the first and most recognisable Japanese retail brand they encounter.

How does Matsukiyo Cocokara compete with Welcia and Tsuruha?

It does not, in the most important sense. The three groups serve different customer bases through different formats. Welcia and Tsuruha — both now consolidating under Aeon Group’s umbrella — run suburban, dispensing-pharmacy-heavy stores aimed at Japan’s aging population and daily-essentials shoppers. Matsukiyo Cocokara runs urban, cosmetics-led, tourist-exposed stores aimed at younger Japanese consumers and inbound foreign visitors. There is overlap, particularly in mid-sized cities where both formats compete for the same daily-goods purchases, but the strategic centre of gravity is different. The Welcia–Tsuruha merger increases pressure on Matsukiyo Cocokara on national-scale buying and back-office efficiency, but does not directly attack its urban-tourist franchise.

How can an overseas brand get its products onto Matsukiyo Cocokara shelves?

The most common entry routes are through an established Japanese cosmetics distributor, through a category-specific buying agent, or — for larger brands — through a direct master-distributor agreement negotiated with the Matsukiyo Cocokara head office in Shinjuku. The chain’s beauty, skincare and supplement categories actively scout international brands, particularly from Korea, Greater China, France and increasingly South-East Asia, and there is a structural appetite for products that resonate with both Japanese consumers and inbound foreign shoppers. For private-label opportunities, Matsukiyo Cocokara works with a relatively small pool of contract manufacturers across Japan, Korea and parts of South-East Asia, with relationships generally introduced via long-standing trading-company intermediaries.

Working with Matsukiyo Cocokara

For overseas cosmetics brands, skincare innovators, supplement manufacturers, contract producers and tourism-economy partners, Matsukiyo Cocokara & Co. offers a route into Japan that no other retailer can replicate: an urban, tourist-anchored, cosmetics-led store network with structural exposure to the same inbound consumer demand that is reshaping Japanese hospitality, retail and consumer-goods export. Japonity introduces qualified overseas companies to Japanese drugstore chains, urban-retail operators and cosmetics distributors through its business matching service. If you are evaluating a Japan-market entry, a tourist-channel brand launch, a private-label production partnership or a cross-border e-commerce arrangement targeting Asian visitors to Japan, get in touch to start a conversation.

Related from Japonity — Japan’s drugstore chains

- Welcia Holdings — Japan’s biggest drugstore chain — and the impending Tsuruha merger

- Tsuruha Holdings — Japan’s #2 drugstore — the Oasis activist campaign and the Welcia merger

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →