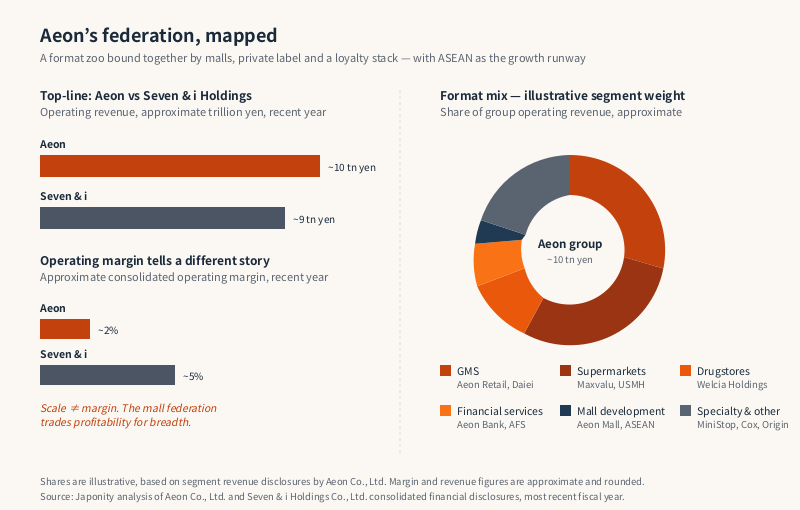

By revenue, Aeon Co., Ltd. is the largest retailer in Japan. The company books approximately ten trillion yen in consolidated operating revenue in a typical recent year, edging past Seven & i Holdings, the operator of 7-Eleven Japan. Yet anyone who has driven past an Aeon Mall ringed by a parking lot of two thousand cars on the outskirts of Sendai, Fukuoka or Phnom Penh, then walked through its food court past a Mister Donut, a MiniStop, an Origin Toshu boxed-lunch counter, a Welcia drugstore and a row of Aeon Bank ATMs, will understand why scale has never automatically translated into either margin or mystique. Aeon is not a category killer. It is something stranger — a federation of formats, financial services and real-estate vehicles that together mirror, more accurately than any other Japanese corporation, the spending habits of the suburban middle class. Headquartered in Makuhari on Tokyo Bay and tracing its lineage to a kimono shop founded in 1758 in Mie Prefecture, the group now operates across roughly twenty markets and runs the largest network of shopping malls in Vietnam, Cambodia and Malaysia. Its story is also the story of why scale alone, in retail, is not enough.

From a Mie kimono shop to a Makuhari conglomerate

Aeon’s official founding year is 1758, when Sojiro Shinohara opened Shinohara-ya, a small kimono and dry-goods shop in Yokkaichi, a port town in what is now Mie Prefecture. The Shinohara family business survived the Meiji Restoration, two world wars and the post-war collapse of Japan’s textile economy, eventually re-emerging as Okadaya, a mid-sized regional retailer. In 1969, Okadaya merged with two other family-run regional chains — Futagi from Hyogo and Shiro from Mie — to form Jusco Co., Ltd., a name assembled from “Japan United Stores Company.” Jusco’s stated ambition, unusual for a Japanese retailer of the time, was nationwide scale through corporate combination rather than organic store opening.

The Jusco era, from 1969 through 1989, laid the foundations of today’s group. The chain rolled up regional supermarkets across western and central Japan, then began experimenting with what Japan called the sogo super — a multi-floor box selling apparel, household goods, electronics and food under one roof. In 1989, the group rebranded as Aeon, a Latin-rooted word chosen for its connotations of eternity. Listing followed, and through the 1990s and 2000s the company acquired Mycal, Daiei (completed in 2015) and a long list of smaller regional supermarkets, until almost every prefecture in Japan had an Aeon-branded store.

Headquarters today sit in Makuhari, a planned waterfront business district on Tokyo Bay in Chiba Prefecture, deliberately distant from Tokyo’s traditional corporate clusters. The geography is not incidental. Aeon’s centre of gravity has always been the suburb, the prefectural capital and the bedroom-community satellite town. Its competitors fight for footfall in Shinjuku and Ginza. Aeon owns the parking lot.

The format zoo

What makes Aeon difficult to compare with any single Western retailer is not its size but its format mix. Walmart is a discount big-box. Costco is a membership warehouse. Tesco is a supermarket-plus-convenience hybrid. Aeon is all of these and several other businesses besides, often within the same shopping mall. The group reports through several listed subsidiaries and a long list of unlisted operating companies, and the simplification below understates the complexity.

| Segment | Representative operating company | What it sells | Approximate footprint |

|---|---|---|---|

| General merchandise stores (GMS) | Aeon Retail, Aeon Kyushu, Aeon Hokkaido | Apparel, household, electronics, food under one roof | Several hundred stores nationwide |

| Supermarkets | Maxvalu chains, United Super Markets, Daiei | Daily food and household goods | Roughly two thousand stores domestically |

| Discount stores | The Big, Acolle | Hard-discount food and apparel | A few hundred stores |

| Drugstores / health & wellness | Welcia Holdings | Pharmacy, cosmetics, daily goods | Largest Japanese drugstore by store count |

| Convenience stores | MiniStop | Convenience, fresh food, soft-serve ice cream | Approximately two thousand stores in Japan plus ASEAN |

| Specialty stores | Cox apparel, Talbots, Claire’s Japan, Mega Sports | Apparel, accessories, sporting goods | Hundreds of stores |

| Food service / prepared foods | Origin Toshu, Mister Donut (licensee) | Boxed lunches, doughnuts | Hundreds of outlets |

| Financial services | Aeon Financial Service, Aeon Bank | Credit cards, retail banking, consumer loans | Tens of millions of cardholders |

| Real estate development | Aeon Mall Co., Ltd. | Suburban regional mall development and operation | Approximately 160-plus malls across Japan and Asia |

| Services and digital | Aeon Delight, Aeon Fantasy | Facility management, indoor amusement | Mall-anchored services |

The crucial point is that these are not standalone businesses pretending to share a brand. They feed each other. Aeon Mall builds a regional shopping centre. The anchor tenant is an Aeon GMS or supermarket. Sub-tenants include a Welcia drugstore, a MiniStop, an Origin Toshu, an Aeon Bank branch and a Cox apparel store. Shoppers pay with an Aeon Card, accumulating WAON points redeemable across every tenant. Aeon Delight cleans the floors. Aeon Fantasy runs the children’s play area. Topvalu private-label products fill roughly a fifth of the supermarket shelf space. The mall is not just a property asset; it is a customer-acquisition machine for every other group business.

Why Aeon outsells Seven & i but earns less per yen

Aeon and Seven & i Holdings are the two giants of Japanese retail, and on a top-line basis Aeon has been larger for most of the last decade. Yet on operating margin and on per-store productivity, Seven & i has historically run rings around Aeon, and the gap reveals something important about the limits of conglomerate retail in Japan.

Seven & i’s economic engine is 7-Eleven, a high-rotation convenience chain with extraordinary store-level productivity, a category-defining private-label programme (Seven Premium) and a global footprint extended through the Seven-Eleven, Inc. acquisition in the United States. The format is narrow, the execution is uniform, and the corporate structure has been progressively pruned — Sogo & Seibu was divested in 2023, Ito-Yokado has been under restructuring pressure, and activist investors have argued for years that Seven & i should focus on 7-Eleven globally and shed everything else.

Aeon has resisted that focus. Its mall-anchored model depends on a wide assortment of co-located formats; pulling any one out weakens the others. The domestic GMS business has been only intermittently profitable, dragged by the same structural decline that hollowed out American big-box retail. Drugstores, convenience stores and financial services subsidise the GMS legacy. Aeon Mall generates the most reliably attractive returns within the group, partly because it operates at one remove from the price-competitive retail floor. The result is a conglomerate that delivers consistent revenue scale, defensible market share and modest group margins. Investors who want pure-play convenience retail buy Seven & i. Investors who want a diversified bet on Asian middle-class consumption buy Aeon.

Topvalu, WAON and the loyalty stack

Two strategic assets cut horizontally across the group and explain why the federation hangs together. The first is Topvalu, the private-label brand introduced in 1974 and now spanning food, beverages, apparel, household goods, electronics and pet products. Topvalu accounts for a meaningful share of supermarket and GMS sales — well into double digits in many categories — and is sold across virtually every group format. Sub-brands include Topvalu Best Price (entry-level value), Topvalu Gurinai (organic and health-conscious) and Topvalu Select (premium). The programme is one of the most extensive private-label operations in Asia, and its scale gives Aeon negotiating leverage with manufacturers and, increasingly, with overseas suppliers whose products are reformulated for Topvalu labels.

The second asset is the loyalty and payment stack: Aeon Card, WAON electronic money and the broader Aeon Financial Service ecosystem. WAON, launched in 2007, is one of Japan’s most widely held prepaid e-money services, with tens of millions of cards in circulation. The Aeon Card credit programme adds another layer of cardholders. Together they generate a stream of transaction data and interchange income, deepen customer stickiness across formats, and underpin Aeon Bank, the group’s internet-and-mall-branch retail bank chartered in 2007. Aeon Financial Service, the listed holding company, also operates consumer-finance and credit-card businesses across Hong Kong, Thailand, Malaysia, Vietnam, Indonesia and several other Asian markets, often well ahead of the group’s retail footprint in those countries.

Aeon Mall and the ASEAN expansion

If one Aeon subsidiary symbolises the group’s strategic ambition outside Japan, it is Aeon Mall Co., Ltd., the listed real-estate-and-mall-development arm. Aeon Mall operates more than 160 shopping centres, with the overseas portfolio concentrated across Vietnam, Cambodia, China, Indonesia and Malaysia. The ASEAN expansion has been deliberate, patient and visible: in cities where modern shopping malls were rare a decade ago, an Aeon Mall arrival is a civic event.

Vietnam is the headline market. Aeon entered with its first mall in Ho Chi Minh City in 2014 and has since opened large suburban centres in Ho Chi Minh, Hanoi, Hai Phong, Binh Duong and other growth corridors, often as anchors for new mixed-use neighbourhoods. Aeon Vietnam, the retail-operating subsidiary, runs the GMS and supermarket businesses inside those malls and supplies a growing share of imported Japanese and Topvalu products. Cambodia is smaller but symbolically important: Aeon Mall Phnom Penh, opened in 2014, was the first modern shopping mall in the country. Aeon Mall Sen Sok City followed in 2018, with further malls since. In Malaysia the group operates through Aeon Co. (M) Bhd., a Bursa-listed subsidiary running department stores, supermarkets and malls across Peninsular Malaysia. Indonesia has Aeon Mall Jakarta Garden City and BSD City; China remains the largest overseas market by store count, though competitive intensity there has prompted strategic adjustments.

The strategic logic is not complicated. Domestic Japanese retail is structurally declining, weighed down by population shrinkage and a price-conscious aging consumer. ASEAN, by contrast, offers two-decade horizons of middle-class growth, urbanisation and modern-trade penetration that mirror Japan’s own retail history in the 1970s and 1980s. Aeon arrives in those markets with one structural advantage few competitors can match: it knows, from sixty years of Japanese suburb-building, how a regional mall ecosystem actually works.

Welcia and the drugstore consolidation

The Aeon group also includes the largest Japanese drugstore chain by store count, Welcia Holdings. Welcia was originally an independent operator that came under Aeon influence through a series of capital tie-ups starting in the mid-2000s and was consolidated as an Aeon subsidiary in 2014. The chain now operates several thousand stores across Japan and has been a serial consolidator in the highly fragmented drugstore segment, absorbing smaller regional chains. In recent years Welcia has announced merger plans with Tsuruha Holdings, another large Japanese drugstore group, in a transaction that would reshape the competitive landscape of the segment if completed as planned and would make the combined entity one of the largest drugstore operators in Asia.

The drugstore strategy matters because Japanese drugstores have become hybrid daily-essentials channels that compete directly with supermarkets and convenience stores on food, beverages and household goods, in addition to pharmacy and cosmetics. For Aeon, owning Welcia means owning the format that has been quietly eating share from its own GMS business — a hedge that turns disruption into internal cannibalisation rather than external loss.

Governance and family legacy

For most of the modern era Aeon’s strategic direction was set by the Okada family, descendants of one of the merger partners that formed Jusco in 1969. Takuya Okada, the group’s long-serving honorary chairman, was the architect of the Jusco-to-Aeon expansion and a familiar figure in Japanese retail circles. Motoya Okada served as president and group chief executive across a generation of corporate development, leading the Daiei acquisition, the ASEAN push and the Welcia consolidation. In recent years the group has gone through governance reorganisation: Akio Yoshida, a long-time executive within the group, took over as president of the holding company, and Motoya Okada moved into the chairmanship before further restructuring shifted senior roles again. The pattern resembles other large Japanese founding-family conglomerates — gradual professionalisation of the management team while the family name retains symbolic weight.

That governance arc matters for outsiders evaluating the group. Aeon has moved at a Japanese pace on board independence, capital-efficiency disclosure and segment-level profitability transparency. Activist pressure of the kind that reshaped Seven & i has been notably absent. The implicit bet is that patience and federation, not radical focus, will deliver returns over the long ASEAN runway.

What comes next

Aeon’s medium-term strategy, articulated across recent investor communications, leans on three vectors. First, lifting margins in the domestic GMS and supermarket businesses through digital ordering, store-format rationalisation and stronger Topvalu private-label penetration. Second, accelerating the ASEAN mall and retail rollout, with Vietnam as the anchor and Cambodia, Indonesia and the Philippines as expanding satellites. Third, deepening the financial-services and digital-payment stack so that loyalty income, transaction data and consumer-finance margins offset the structural pressure on physical retail.

None of these moves resemble a category-killer playbook. Aeon is not betting that any single format will win. It is betting that a federated portfolio, anchored in suburban real estate and bound together by a private label and a loyalty programme, will continue to mirror the middle-class consumer better than any specialist competitor. That is a deeply Japanese bet — and the one most likely to keep Aeon at the top of the Japanese retail revenue league even as the structural ground beneath the industry shifts.

FAQ

Is Aeon really larger than Seven & i Holdings?

On consolidated operating revenue, yes — Aeon has been the largest Japanese retailer for several years, typically reporting around ten trillion yen against Seven & i in a similar range or lower depending on accounting treatment of franchised stores. The gap is narrow and the rankings can flip year to year, but Aeon’s broader format footprint and mall-development revenue keep it consistently at or near the top. On operating profit and per-employee productivity, however, Seven & i has historically been stronger, driven by 7-Eleven’s high-margin convenience economics.

What is Aeon Mall and how is it related to the rest of the group?

Aeon Mall Co., Ltd. is the listed real-estate development and mall-operation subsidiary of the Aeon group. It develops and operates more than 160 large suburban shopping centres across Japan, Vietnam, Cambodia, China, Indonesia and Malaysia. Aeon Mall is the property developer; the anchor and sub-tenants are typically other Aeon group operating companies such as Aeon Retail, Welcia, MiniStop, Aeon Bank and Cox apparel. The mall and the retail businesses inside it are commercially separate but strategically interdependent.

What is Topvalu and why does it matter?

Topvalu is Aeon’s group-wide private-label brand, launched in 1974, covering food, beverages, apparel, household goods, electronics and pet products. It is sold across nearly every Aeon retail format and accounts for a substantial share of sales in many categories. Topvalu gives Aeon negotiating leverage with manufacturers, supports gross margin in a price-competitive market, and enables product differentiation that pure distribution scale alone cannot deliver. For overseas suppliers, securing a Topvalu contract is one of the most reliable routes into Japanese mass distribution.

How big is Aeon’s ASEAN business?

Aeon operates large mall portfolios across Vietnam, Cambodia, Indonesia and Malaysia, as well as a long-established business in China. Vietnam is the anchor market, where Aeon has opened multiple regional malls since 2014 and continues to expand. In Cambodia, Aeon was the first operator to bring modern shopping malls to the country. Aeon Malaysia operates as Aeon Co. (M) Bhd., a Bursa-listed subsidiary. Across ASEAN the group runs malls, supermarkets, GMS stores and a growing financial-services footprint through Aeon Financial Service subsidiaries.

Who owns Welcia and how does it fit into the group?

Welcia Holdings is a listed drugstore-chain operator and Aeon group subsidiary, consolidated as an Aeon subsidiary in 2014 after a series of earlier capital tie-ups. It is the largest Japanese drugstore chain by store count and has announced merger plans with Tsuruha Holdings that, if completed as currently described, would create one of Asia’s largest drugstore operators. Welcia gives the Aeon group a strong position in the fast-growing drugstore-as-daily-essentials channel that has been taking share from supermarkets and convenience stores.

Working with Aeon

For overseas brands, food exporters, private-label manufacturers, mall co-tenants and capital partners, Aeon’s federated structure offers an unusually wide set of entry points — from Topvalu private-label contracts to Aeon Mall tenancy in Japan and ASEAN, from Welcia drugstore distribution to Aeon Financial Service co-branded card programmes. Japonity introduces qualified overseas companies to Japanese retailers, mall developers and consumer-brand operators through its business matching service. If you are exploring a Japan-market entry, a private-label opportunity, a mall partnership or an ASEAN co-investment, get in touch to start a conversation.

Related from Japonity — Japan’s retail & convenience-store giants

- Seven & i Holdings — The convenience-store empire targeted by Couche-Tard

- Lawson — The konbini now jointly owned by Mitsubishi Corp and KDDI

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →