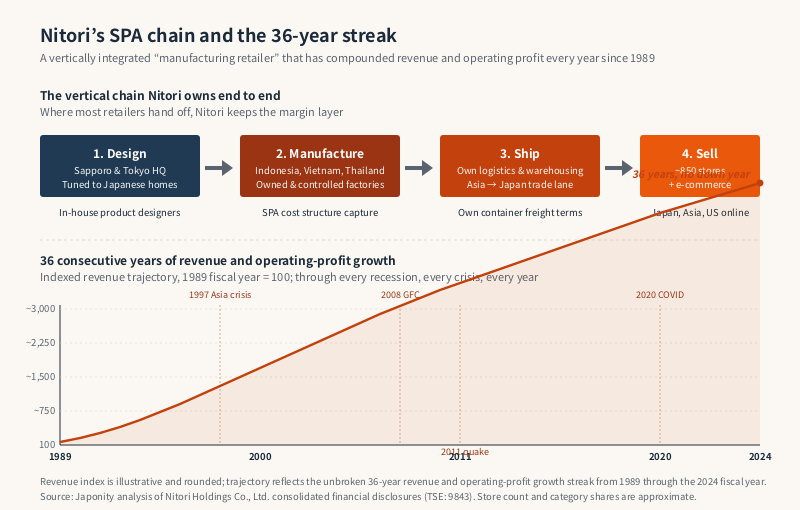

For thirty-six consecutive financial years, Nitori Holdings Co., Ltd. has booked higher revenue and higher operating profit than the year before. No other company on the Tokyo Stock Exchange has matched that unbroken streak. Through Japan’s banking crisis, the 1997 Asian currency rout, the 2008 global financial collapse, the 2011 earthquake and the pandemic, a Sapporo-based furniture and home-goods retailer founded in 1967 by Akio Nitori has gone on quietly compounding earnings while department stores, electronics chains and apparel groups cycled through crisis. The Nitori network now spans approximately 850 stores across Japan, China, Taiwan, the rest of Asia and a growing online-led presence in the United States, all stocked with merchandise the company itself designs in Japan, manufactures in Asian factories under its own management, ships through its own logistics and sells at price points anchoring the lower end of Japanese middle-class spending. The Western analogy is usually IKEA. The deeper truth is that Nitori, alone among Japanese retailers, has built a vertically integrated SPA model that works — and has quietly become the most successful Japanese retail export of the post-war era.

From one furniture shop in Sapporo to the SPA pioneer

Akio Nitori opened his first furniture store, Nitori Furniture, in Sapporo in 1967, at twenty-three years old, with a single salesroom selling locally made tansu and bedding. The early business almost failed; Hokkaido in the late 1960s was not a forgiving retail market for an under-capitalised newcomer. The turning point, by his own account, was a 1972 visit to the United States, where suburban furniture chains operating at scale, with deep assortments and aggressive price points, presented a model that simply did not exist in Japan. He returned with two convictions that would define the company for the next half-century: that Japanese consumers were paying too much for furniture relative to what they got, and that the only way to fix that was to control the entire chain from design to retail.

Through the 1980s and 1990s Nitori rolled out larger suburban stores across Hokkaido and then the mainland, while progressively bringing manufacturing in-house and offshore. The company established its own factories in Indonesia in the 1990s, later expanding to Vietnam and Thailand, and built up a logistics arm capable of moving containers from those factories to Japanese ports and onward to its own distribution centres. By the early 2000s Nitori had become an unmistakeable SPA — the specialty-retailer-of-private-label model Inditex and Uniqlo had popularised in apparel — but applied to furniture and home goods, a category most retailers had assumed was too bulky, too slow-turning and too design-fragmented to industrialise that way. Akio Nitori formally handed the CEO role to Toshiyuki Shirai in 2022 while remaining chairman. The thirty-six-year profit-growth streak survived the transition.

The “manufacturing retailer” model, decoded

Nitori describes itself as a seizo kouri-gyo — a “manufacturing retailer” — and the phrase is more than corporate marketing. It describes a value chain that the company controls end to end in a way few of its global peers can match.

Design happens in Japan, primarily at the Sapporo head office, at product-development centres tuned to the dimensions, materials and storage habits of Japanese housing. That orientation matters: Japanese homes are smaller, ceilings lower, hallways narrower and wardrobes shallower than the Western norm, and a sofa that does not fit Japanese spatial conventions will not sell regardless of price. Nitori’s designers iterate against those constraints in a way IKEA, designing for Northern European homes, never has needed to. Sourcing and manufacturing happen across an Asian network anchored in Indonesia, Vietnam and Thailand, with Nitori owning a meaningful share of production capacity through wholly owned factories or long-term contract relationships where it specifies design, materials, quality and pricing. The proportion under direct Nitori control is substantially higher than at most Japanese retailers, and is one structural reason the company sustains margins across cycles.

Logistics is the third leg. Nitori operates its own distribution centres in Japan and runs container shipping volumes large enough to negotiate competitive freight terms on the Asia-Japan trade lane — a quiet but decisive cost advantage in a country where most furniture retailers depend on wholesalers and third-party logistics providers. Retail is the final integration: large-format suburban stores, urban formats such as Nitori Decohome, the EXPRESS small-format city stores and an e-commerce channel that integrates with the same inventory pool. The result is a value chain in which a sofa designed in Sapporo can be specified for an Indonesian factory, shipped on a Nitori-controlled container, distributed through a Nitori warehouse and sold through a Nitori store at a price point competitors using a traditional wholesale model find structurally difficult to match.

The 36-year streak in context

The unbroken thirty-six-year run from the 1989 through the 2024 fiscal year deserves to be examined rather than simply repeated. Other Japanese growth companies have posted long streaks, but the combination of duration, consistency across categories and survival through multiple recessionary cycles is unique. The 1997-1998 Asian crisis, the 2008-2009 global financial crisis, the 2011 earthquake and post-disaster consumer freeze, and the 2020-2022 pandemic each produced annual contractions for most large Japanese retailers. Nitori did not contract in any of them.

Several structural drivers explain that consistency. The first is the SPA cost structure: by owning design, sourcing, manufacturing, logistics and retail, Nitori captures margin layers competitors hand off to third parties and can compress prices without compressing operating profitability. The second is yen-cost arbitrage; production in Indonesia, Vietnam and Thailand denominates much of cost of goods sold in currencies that have, over decades, moved favourably relative to the yen. The third is category breadth — bedding, textiles, kitchenware, decoration and lifestyle goods provide higher-turnover, smaller-ticket categories that smooth quarterly performance. The fourth is geographic diversification, late but accelerating, into China, Taiwan, Southeast Asia and now the United States. The fifth is store-productivity discipline: conservative on the pace of openings relative to demand signals, aggressive on closing or repositioning underperformers.

Format mix and category breadth

The popular image of Nitori is the large suburban store with a parking lot, anchored by furniture showrooms. The reality of the assortment is broader, and the format mix has diversified deliberately over the last decade as the company has pushed into urban Japanese markets where suburban-scale boxes are not viable.

| Category | What it sells | Typical share of sales | Strategic role |

|---|---|---|---|

| Furniture | Sofas, beds, dining sets, storage, desks, chairs | Approximately one-third | Anchor category, drives footfall, structural margin |

| Bedding and textiles | Mattresses, futons, sheets, curtains, rugs | Approximately one-fifth | High-frequency repeat purchase, seasonal refresh |

| Decoration and lifestyle | Tableware, kitchen tools, storage boxes, decor | Approximately one-quarter | Smaller-ticket impulse, urban-format core |

| Home appliances and outdoor | Small appliances, garden, outdoor furniture | Low double-digit percentage | Seasonal and lifestyle expansion |

| Other and overseas | Cosmetics niches, international operations | Remainder | Growth optionality, brand extension |

The large-format suburban stores remain the network anchor and primary driver of furniture revenue. Nitori Decohome, a smaller urban concept focused on decoration, lifestyle and gift goods, has expanded rapidly in shopping malls and station-area locations where a full furniture showroom is impractical. Nitori EXPRESS, an even smaller format, targets dense urban catchments. The e-commerce channel integrates with the physical network for delivery, returns and assembly. Adjacent-category niche acquisitions — the Etat Pure cosmetics line in France being the most discussed — round out the portfolio.

Nitori, IKEA and Muji compared

Westerners reaching for an analogy almost always say “Japan’s IKEA,” and the comparison is useful as a starting point. Both run large suburban stores, private-label assortments and value-for-money positioning, and both are vertically integrated relative to their categories. The differences, however, reveal why Nitori has succeeded inside Japan in a way IKEA never quite has.

| Dimension | Nitori | IKEA | MUJI (Ryohin Keikaku) |

|---|---|---|---|

| Founded | 1967, Sapporo | 1943, Sweden | 1980, Tokyo |

| Approximate store count | ~850 stores globally | ~470 stores globally | ~1,200 stores globally |

| Category | Furniture, bedding, lifestyle | Furniture, lifestyle, kitchen | Lifestyle, apparel, food, furniture |

| Manufacturing model | Direct ownership and tight control of Asian factories | Long-term supplier network, limited direct ownership | Branded sourcing from contract manufacturers |

| Design centre | Sapporo and Tokyo, tuned to Japanese homes | Sweden, global design standard | Tokyo, minimalist global aesthetic |

| Format mix | Suburban large-format plus urban Decohome / EXPRESS | Suburban large-format dominant | Urban small and mid-format dominant |

| Profit-growth track record | 36 consecutive years of revenue and operating-profit growth | Private; long history of revenue growth, profit volatility | Long growth history with periodic resets |

IKEA entered Japan in earnest in 2006 after an earlier failed attempt in the 1970s and has built a presence of around a dozen stores, but it has never threatened Nitori’s domestic position the way it has displaced incumbents elsewhere. The reasons are structural: IKEA’s Swedish design language, flat-pack self-assembly assumption and parking-required suburban siting all run against the grain of Japanese consumer expectations on dimension, finish and service. Nitori, by designing for Japanese homes from the start and offering paid assembly and delivery as standard, occupies precisely the space IKEA cannot. MUJI, by contrast, operates further upmarket on lifestyle aesthetics and further downmarket on furniture ticket size, and is more a complement than a direct competitor.

Asia first, then America

Nitori’s international story is more recent and faster-moving than the domestic narrative suggests. The company opened its first overseas store in Taiwan in 2007 and has since built a Taiwanese network that, by per-capita store density, rivals the domestic Japanese footprint. China followed in 2014, with stores in Shanghai and other major cities. Singapore, Malaysia and Hong Kong rounded out the Asian footprint through the late 2010s and early 2020s. The combined overseas Asian network now spans more than one hundred stores. Production-side, the Indonesia, Vietnam and Thailand factory network is the manufacturing backbone of the entire group, progressively deepened with new plants and expanded capacity.

The United States is the more recent frontier. Nitori entered in 2022 through an online channel oriented to West Coast consumers, with a deliberately measured rollout that contrasts with the all-at-once physical-store push other Japanese retailers have sometimes attempted. E-commerce lets Nitori test product-market fit, delivery economics and brand awareness with limited capital exposure; a future physical-store rollout, when it comes, can be calibrated to demonstrated demand corridors rather than speculative real-estate bets. The medium-term ambition is to build the United States into a meaningful contributor to group revenue, though the company has been characteristically conservative about timelines.

The Shimachu acquisition and the home-improvement bridge

The largest single transaction in Nitori’s recent history was the 2020 acquisition of Shimachu Co., Ltd., a listed home-furnishing and home-improvement retailer with stores concentrated in eastern Japan. The deal was valued at approximately one hundred and seventy billion yen and brought a complementary footprint with stronger DIY and home-improvement positioning. Shimachu gave Nitori three things at once: incremental store locations in catchments where the core brand was under-represented, a foothold in the home-improvement-plus-furnishing format category, and an additional channel for the Nitori private-label assortment. Integration has proceeded as Nitori integrations typically do — patient, operationally focused and biased toward preserving the acquired brand rather than absorbing it wholesale.

Beyond Shimachu, Nitori has made selective adjacent investments — including the Etat Pure cosmetics brand in France and various lifestyle and wellness positions — that round out the portfolio without distracting from the core SPA economics. The pattern is the opposite of the format-zoo conglomeration approach pursued by some Japanese peers: bounded, related-category and integration-light additions designed to extend the SPA capability rather than dilute it.

Governance, succession and what comes next

Akio Nitori, now in his eighties, remains chairman and the dominant strategic voice within the group, but the operational handover to Toshiyuki Shirai as president and CEO in 2022 marked a meaningful generational transition. Shirai came up through merchandising and operations, and his appointment signalled continuity rather than rupture — exactly the message a thirty-six-year compounding machine wants to send to shareholders. The Tokyo Stock Exchange listing, under code 9843, attracts meaningful foreign institutional ownership, and Nitori has been more communicative than many Japanese mid-cap retailers about long-term strategy, capital allocation and overseas plans.

The medium-term strategy rests on three pillars. First, domestic store-network optimisation, with urban-format expansion offsetting slower growth of the suburban network and private-label penetration deepening across categories. Second, overseas growth, with the United States as the headline priority and patient build-out continuing in China, Taiwan and Southeast Asia. Third, operational deepening — logistics automation, e-commerce integration, factory modernisation across the Asian production network and adjacent-lifestyle category expansion — designed to extend the SPA margin advantage.

None of those moves is revolutionary. Nitori’s competitive advantage has never been a single product or store concept; it is the cumulative compounding of small operational improvements across a vertically integrated chain competitors have largely failed to replicate. The thirty-six-year streak is the visible artefact. The deeper truth is the boring one: an SPA model executed with extraordinary patience, applied to a category most retailers found too hard to industrialise, by a founder who started with one shop in Sapporo and refused to outsource the parts that mattered. The next test is whether the formula travels intact to Los Angeles and Shanghai. The early evidence, modest but consistent, suggests it does.

FAQ

What does Nitori’s “36 consecutive years of profit growth” actually mean?

From the 1989 fiscal year through the 2024 fiscal year, Nitori Holdings has reported higher consolidated revenue and higher consolidated operating profit than the prior year in every single annual period — a thirty-six-year unbroken streak. No other company listed on the Tokyo Stock Exchange has matched that record over the same time frame. The streak has survived the 1997 Asian financial crisis, the 2008 global financial crisis, the 2011 Tohoku earthquake and the 2020-2022 pandemic, all of which caused most large Japanese retailers to report at least one year of contraction.

How is Nitori different from IKEA?

Both Nitori and IKEA operate vertically integrated furniture-and-lifestyle retail businesses anchored by large suburban stores and private-label assortments. The differences are that Nitori designs its products specifically for Japanese homes (smaller dimensions, different storage habits, different finish expectations), owns or tightly controls more of its Asian factory base than IKEA does of its suppliers, and offers paid delivery and assembly as standard rather than treating self-assembly as the default. Inside Japan, Nitori has thoroughly outcompeted IKEA, which entered the market in 2006 and has built only a small network of stores. The two compete more directly outside Japan.

What is the SPA model in Nitori’s context?

SPA stands for “specialty store retailer of private label apparel,” a model originally developed in the apparel industry by companies such as Inditex (Zara) and Uniqlo, in which a single company designs, manufactures, distributes and retails its own branded products end to end. Nitori applies the SPA model to furniture and home goods — a category most retailers had assumed was too capital-intensive and slow-turning to integrate that way. Nitori designs in Japan, manufactures primarily in its own and contract factories in Indonesia, Vietnam and Thailand, ships through its own logistics network and sells through its own stores. The integrated chain is the source of Nitori’s structural cost advantage.

What was the Shimachu acquisition?

In 2020 Nitori acquired Shimachu Co., Ltd., a listed Japanese home-furnishing and home-improvement retailer, in a transaction valued at approximately one hundred and seventy billion yen. Shimachu gave Nitori a complementary network of stores concentrated in eastern Japan, a stronger position in the DIY and home-improvement category, and an additional channel for its private-label assortment. The integration has proceeded in the patient, brand-preserving style characteristic of Nitori’s M&A approach.

Is Nitori expanding into the United States?

Yes. Nitori entered the US market in 2022, initially through an online channel oriented to West Coast consumers, and has communicated medium-term ambition to build a meaningful US business as part of its broader international expansion. The approach has been deliberately measured — e-commerce first, physical store rollout calibrated to demonstrated demand — which contrasts with the all-at-once physical-store entries other Japanese retailers have sometimes attempted abroad. The United States is the headline international growth priority alongside continued build-out in China, Taiwan and Southeast Asia.

Working with Nitori

For overseas suppliers, factory partners, real-estate landlords, logistics providers and capital partners, Nitori offers an unusually disciplined and long-horizon counterparty. Private-label manufacturing relationships, especially in Indonesia, Vietnam and Thailand, anchor the supply side; mall and shopping-centre tenancy relationships drive the store-network growth in Asia and increasingly the United States; and adjacent-category brand investments — cosmetics, wellness and lifestyle — provide selective M&A entry points. Japonity introduces qualified overseas companies to Japanese retailers, manufacturers, real-estate developers and capital allocators through its business matching service. If you are exploring a private-label opportunity, a factory partnership, a real-estate relationship or a capital tie-up with one of Japan’s most consistent compounding businesses, get in touch to start a conversation.

Related from Japonity — Japan’s mass retail & discount giants

- Aeon Group — Japan’s biggest retailer by sales — and ASEAN’s largest mall network

- Pan Pacific International Holdings — Don Quijote and DON DON DONKI — the only Japanese mass-retailer to crack overseas Asia

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →