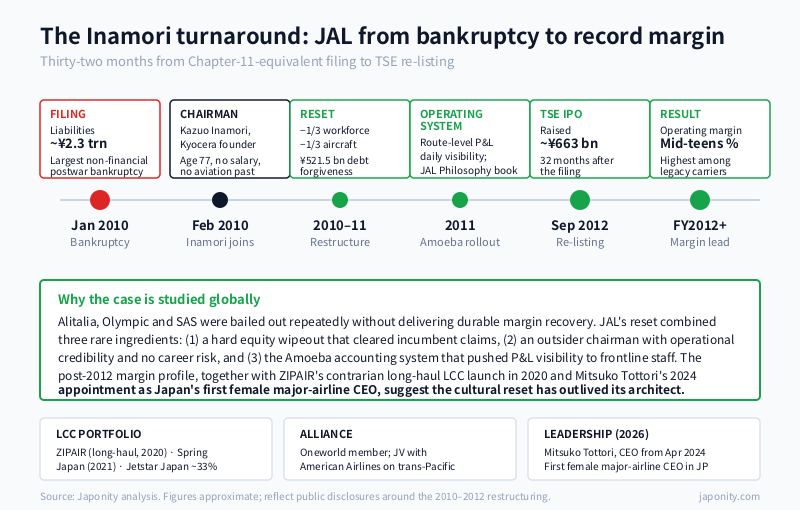

In January 2010, Japan Airlines filed for bankruptcy with liabilities of approximately ¥2.3 trillion — the largest corporate failure in postwar Japan outside the financial sector. The flag carrier, once a symbol of the country’s high-growth era, was effectively delisted, its shareholders wiped out and its workforce reduced by roughly a third. Fifteen years later, JAL is widely cited in business schools as one of the most successful corporate turnarounds in modern history: the company that emerged from court protection in 2012 has since posted operating margins that are, in good years, the highest among the world’s full-service legacy carriers — a profile closer to a disciplined manufacturer than a typical national airline.

From flag carrier to insolvency: how JAL ran out of altitude

Japan Airlines was founded in 1951 as the country’s designated flag carrier in the immediate postwar period, charged with reconnecting an isolated economy to the rest of the world. For four decades it operated under an implicit social contract — guaranteed long-haul routes, government-influenced fares, a privileged relationship with aerospace suppliers, and an unspoken role as the airline of choice for Japanese officialdom. The model worked beautifully when Japan’s GDP was compounding at single-digit rates and outbound business travel was a near-monopoly market.

By the mid-2000s, however, the contract had become a liability. Three structural shifts converged. First, deregulation eroded the duopoly with All Nippon Airways (ANA), allowing low-cost carriers and second-tier players to compete on domestic trunk routes. Second, the global financial crisis of 2008–09 collapsed premium long-haul demand at exactly the moment JAL had over-invested in widebody capacity, especially the four-engine Boeing 747-400 fleet. Third, JAL’s cost structure — generous pension obligations, unionized cabin and ground staff agreements, and a sprawling route network kept alive for political rather than commercial reasons — left no margin for error. Operating losses widened, debt ballooned, and by late 2009 the company was negotiating emergency credit lines with its main banks.

On 19 January 2010, JAL filed for protection under Japan’s Corporate Rehabilitation Law. The case was handed to the Enterprise Turnaround Initiative Corporation of Japan (ETIC), a state-backed restructuring vehicle. The terms were severe: full equity wipeout, ¥521.5 billion of debt forgiveness from creditors, and a mandate to cut roughly one-third of the workforce and a similar share of aircraft capacity. What attracted international attention, though, was the choice of chairman.

The Inamori intervention: amoeba management in the cockpit

Kazuo Inamori, the founder of Kyocera and KDDI, was 77 years old, had no aviation experience, and accepted the chairmanship for no salary. Inamori was already famous in Japan for two reasons: a half-century track record building two Fortune 500 companies from scratch, and a philosophical management framework — codified in his bestselling books and the Seiwajuku executive school — built around the question “as a human being, what is the right thing to do?”. His operational toolkit, known as Amoeba Management, broke the company into small accounting units, each treated as a profit centre with daily P&L visibility and clear ownership.

Applied to JAL, the approach produced three structural changes that legacy carriers elsewhere had failed to deliver. Route-level profitability was made transparent to operating staff, not just headquarters analysts — every flight, every day, became a unit accountable for its own contribution. Loss-making routes were closed without sentiment, including iconic but unprofitable services. And a cultural rewrite, the so-called “JAL Philosophy” handbook distributed to every employee, redefined the company’s purpose around staff well-being and customer service rather than national prestige.

The financial results were striking. JAL re-listed on the Tokyo Stock Exchange in September 2012, just thirty-two months after filing, raising approximately ¥663 billion in one of the largest IPOs of the year. By fiscal 2012, operating margin had reached the mid-teens — a level that European and American flag carriers, even in good cycles, rarely sustain. Inamori stepped back from day-to-day involvement in 2013 and passed away in 2022, but the management cadence he installed has outlived him.

Post-bankruptcy economics: why the margin gap persists

More than a decade after re-listing, JAL still earns operating margins that are unusual for a full-service legacy carrier. In strong years the figure has reached the mid-teens; even through the pandemic and the subsequent fuel-price spike, JAL recovered to profitability faster than most peers of comparable size. Three drivers explain the gap.

The first is route discipline. JAL flies fewer city pairs than ANA and far fewer than the European majors, but the network is curated for yield rather than coverage. The second is fleet rationalisation. The carrier was an early adopter of the Boeing 787 Dreamliner — in fact, it was the launch customer for the type in commercial service — and used the bankruptcy as cover to retire the fuel-thirsty 747-400 fleet years before competitors. The third is the Amoeba accounting system itself, which keeps unit costs visible at a granularity that few peers attempt.

The discipline is not without trade-offs. JAL’s domestic market share trails ANA, and the carrier has been more cautious than its rival in committing to greenfield capacity. Critics argue that the bankruptcy left a residual conservatism — a reluctance to take the kind of expansionary bets that ANA has made on international long-haul and freight. The counter-argument, increasingly heard from investors, is that capital discipline is precisely what global aviation needs and that JAL’s restraint is a feature, not a bug.

JAL versus ANA: two playbooks for the same market

The rivalry between Japan’s two full-service carriers is one of the most instructive duopolies in global aviation. Both serve a roughly identical home market, operate similar widebody fleets, and command comparable brand premiums. The strategic divergence — driven in large part by the bankruptcy and its aftermath — has become a clean natural experiment in airline strategy.

| Dimension | Japan Airlines (JAL) | All Nippon Airways (ANA) |

|---|---|---|

| Global alliance | Oneworld (since 2007) | Star Alliance (since 1999) |

| Tokyo primary hub | Haneda & Narita, balanced | Haneda-led, Narita secondary |

| Strategic posture (post-2012) | Capital discipline, yield focus | Network expansion, scale |

| LCC strategy | Multi-brand (ZIPAIR, Spring Japan, Jetstar Japan stake) | Single brand (Peach Aviation) |

| Widebody flagship | Boeing 787 (launch customer) | Boeing 787 (largest operator) |

| Operating margin profile | Mid-teens in strong years | High single digits typically |

| Cargo focus | Belly capacity, modest dedicated fleet | Substantial dedicated freighter operation |

| Leadership (2026) | Mitsuko Tottori, first female major-airline CEO in Japan | Shinichi Inoue |

The alliance choice is more consequential than it first appears. Oneworld, anchored by American Airlines, British Airways and Cathay Pacific, gives JAL deep trans-Pacific and trans-Atlantic feed, particularly the joint business agreement with American Airlines that effectively unifies the two carriers’ Japan–US economics. Star Alliance gives ANA broader European reach via Lufthansa and a stronger position in intra-Asia connectivity. Neither is strictly better; they reflect different bets on where premium long-haul demand will concentrate over the next two decades.

The LCC portfolio: ZIPAIR, Spring Japan, Jetstar

The most distinctive element of JAL’s strategy is its multi-brand approach to low-cost flying. Where ANA consolidated its budget operations under a single brand, Peach, JAL operates a portfolio of three vehicles aimed at different segments of the cost-conscious traveller.

ZIPAIR Tokyo, launched in 2020, is the most strategically interesting. It is a long-haul international low-cost carrier — a difficult model historically — using Boeing 787s in a high-density layout, branded with deliberate distance from the JAL parent. ZIPAIR flies routes such as Tokyo to Los Angeles, San Francisco, Singapore and Bangkok, targeting price-sensitive leisure travellers and the long tail of Asian outbound demand that the mainline carrier cannot serve profitably. The fact that JAL launched a long-haul LCC during the pandemic was widely questioned at the time and is now broadly credited as a contrarian success.

Spring Japan, originally a joint venture with China’s Spring Airlines, became a wholly-owned JAL subsidiary in 2021. Its role is short-haul international service to mainland China and other parts of North Asia, with a cost structure JAL mainline cannot match on those routes. Jetstar Japan, in which JAL holds approximately one-third — alongside the Qantas Group and Mitsubishi Corporation — covers domestic and short-haul international leisure flying, leveraging Jetstar’s global LCC platform.

The three-brand architecture allows JAL to compete in segments — leisure long-haul, China point-to-point, domestic budget — without diluting the mainline premium. It is operationally more complex than ANA’s single-brand Peach approach, but it provides a hedge against any one segment underperforming, and it preserves the JAL brand for the yield-paying customer.

Engineering, ground services and the value chain

Beneath the commercial brand, JAL operates one of the most respected maintenance, repair and overhaul (MRO) operations in Asia. JAL Engineering, originally JAL Maintenance & Engineering, provides line and heavy maintenance for the group’s own fleet and selectively for third-party carriers. The MRO business is rarely glamorous but is structurally important — it captures margin that would otherwise leak to overseas providers, and it gives JAL leverage in fleet decisions through deep technical relationships with Boeing, Airbus and the engine OEMs.

The group also encompasses cargo, catering, ground handling and a sprawling loyalty programme, JAL Mileage Bank, which functions as a high-margin financial business with credit-card partnerships that contribute meaningfully to group earnings. As at major US carriers, the loyalty programme is often the most valuable single asset on a sum-of-the-parts basis, although JAL does not break it out separately in disclosure.

Tottori and the next chapter

In April 2024, Mitsuko Tottori was appointed president and CEO — the first woman to lead a major Japanese airline. The succession itself was a quiet statement. Tottori joined JAL as a cabin attendant in 1985 and rose through the customer experience and operations side of the business rather than the finance or planning track that typically produces airline chief executives. Her appointment, following the tenures of Yuji Akasaka and Yukio Nakamura, signalled a continuation of the post-Inamori cultural emphasis on frontline employees as the company’s primary stakeholders.

Her early agenda has emphasised safety, sustainability and the integration of the LCC portfolio. The January 2024 Haneda runway collision, in which a JAL Airbus A350 was destroyed but all 379 passengers and crew evacuated successfully, was held up internationally as a textbook demonstration of cabin crew training and aircraft design — and is, in retrospect, a vindication of the Inamori-era investment in frontline competence. Looking forward, JAL faces the familiar questions confronting every legacy carrier: how fast to transition to sustainable aviation fuel, how to price premium leisure as it grows relative to business travel, and how to manage labour costs in an inflationary environment after two decades of Japanese deflation.

What JAL means for foreign partners

For overseas businesses looking at Japan, JAL matters in three distinct ways. As a route partner, the joint business agreement with American Airlines makes JAL the most efficient way to move people and time-sensitive cargo across the Pacific. As a procurement partner, JAL’s fleet, MRO and ground-services demand is significant — Boeing, GE Aerospace, Rolls-Royce and a long list of tier-one suppliers count the carrier as a strategic customer. And as a brand-licensing and loyalty partner, JAL’s mileage programme reaches a demographic — affluent Japanese travellers and the Asian diaspora — that is difficult to access through any other single channel.

The deeper lesson, though, is governance. JAL’s bankruptcy and recovery are studied at business schools precisely because the company executed a turnaround that most legacy carriers — Alitalia, Olympic, SAS — failed to deliver despite repeated state bailouts. The combination of a hard reset, a disciplined operating system, and a charismatic but selfless interim leader is rare. It is also, increasingly, the template that other restructuring practitioners point to when explaining what a successful Chapter 11 equivalent can look like outside the United States.

FAQ

Why did JAL go bankrupt in 2010?

JAL filed under Japan’s Corporate Rehabilitation Law in January 2010 after a combination of pension liabilities, an oversized widebody fleet (particularly the Boeing 747-400), the collapse in premium demand after the 2008 financial crisis, and decades of route decisions made for political rather than commercial reasons. Liabilities were approximately ¥2.3 trillion — the largest non-financial corporate bankruptcy in postwar Japan.

Who is Kazuo Inamori and what was his role?

Inamori was the founder of Kyocera and KDDI, two Fortune 500 companies he built from scratch. He was appointed JAL chairman in 2010 at age 77 without a salary, brought no aviation experience, and applied his Amoeba Management system — small accounting units with daily P&L visibility — alongside a cultural rewrite codified in the “JAL Philosophy” handbook. He is widely credited as the architect of the turnaround.

How does JAL compare to ANA today?

JAL sits in Oneworld; ANA in Star Alliance. JAL has historically run with tighter capital discipline and higher operating margins, while ANA has pursued more aggressive network expansion and operates substantially more dedicated cargo capacity. JAL uses a multi-brand LCC strategy (ZIPAIR, Spring Japan, Jetstar Japan stake); ANA consolidates around Peach.

What is ZIPAIR Tokyo?

ZIPAIR is JAL’s long-haul international low-cost carrier, launched in 2020. It operates Boeing 787s in a high-density configuration on routes such as Tokyo to Los Angeles, San Francisco, Singapore and Bangkok. It is one of the few long-haul LCCs globally to have reached scale, and was launched contrarian-style during the pandemic.

Who currently leads JAL?

Mitsuko Tottori became president and CEO in April 2024, the first woman to lead a major Japanese airline. She joined JAL as a cabin attendant in 1985 and rose through the customer experience and operations track, succeeding Yukio Nakamura and Yuji Akasaka.

Working with JAL

If your organisation is exploring partnerships with Japan Airlines — whether as a supplier, codeshare partner, corporate travel account, loyalty programme integration, or MRO customer — Japonity can support the introduction and translation work. Visit our business matching service to start the conversation. We work with global companies across aviation, aerospace, travel technology and adjacent sectors to build long-term commercial relationships with leading Japanese firms.

Related from Japonity — Japan’s airlines

- ANA Holdings — Japan’s #1 airline emerging from the pandemic with the cleanest balance sheet

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →