ANA Holdings Inc. is Japan’s largest airline group by passenger volume, the anchor Star Alliance carrier in Asia, and the company that came out of the pandemic with the cleanest balance sheet of any major full-service flag carrier — without state-led restructuring, foreign capital injection, or shareholder reset. Two decades of slot dominance at Tokyo Haneda, a full-service mainline supplemented by the Peach low-cost carrier, an outsized cargo franchise that proved indispensable during COVID, and launch-customer status on the Boeing 787 have combined to give ANA a structurally different operating model from Japan Airlines — the rival that did go through bankruptcy in 2010 and is still managed accordingly. For corporate-travel buyers, freight forwarders, and aerospace suppliers, understanding what makes ANA tick is increasingly a precondition to doing business in or through Japan.

From helicopter operator to flag carrier in seventy years

The company that became ANA Holdings began in December 1952 as Japan Helicopter and Aeroplane Transports, a small post-war operator running a pair of Bell helicopters. A 1957 merger with Far East Airlines produced All Nippon Airways. For its first four decades it grew quietly inside Japan’s tightly regulated domestic market, alongside the state-supported Japan Airlines that monopolised international routes until liberalisation in the mid-1980s. ANA was the second carrier — the challenger without the diplomatic flag and the lifetime employees of the former national champion.

Two events reshaped the company. The first was joining Star Alliance in 1999, which gave ANA a global codeshare and frequent-flyer network without the capital expense of building one alone. The second was Japan Airlines’ bankruptcy and government-led restructuring in 2010, which left ANA facing a competitor cleansed of legacy pension liabilities, pruned of unprofitable routes, and recapitalised by the state-backed Enterprise Turnaround Initiative Corporation. ANA spent the 2010s responding to that asymmetry by expanding international capacity, locking in Haneda slots as they were progressively re-internationalised, and building Peach into Japan’s only credible domestic LCC platform.

In 2013 the group was restructured into a holding company — ANA Holdings — with All Nippon Airways becoming a subsidiary alongside Peach Aviation, ANA Cargo, ANA Components Service, and a long list of ground-handling, catering, IT, and travel-related units. Headquarters sit in the Shiodome district of Tokyo. Koji Shibata, a career ANA executive who ran the mainline carrier through the back end of the pandemic, took over as president and chief executive officer of ANA Holdings in April 2023.

The Haneda thesis

The single most important structural fact about ANA is its slot position at Tokyo International Airport — Haneda — the airport closer to central Tokyo than Narita and the one preferred by both business travellers and the Japanese government. For domestic operations, Haneda has effectively been ANA’s home base since the carrier began jet service. For international operations, slots have been opened in waves, with each round expanding the carrier’s global network out of the most commercially valuable airport in East Asia.

Haneda’s appeal is not a matter of taste. It is roughly thirty minutes from central Tokyo by rail or car versus sixty to ninety for Narita; it is the default for Japanese government and major corporate travel; and the volume of high-yield business passengers it captures per landing is substantially higher than at any other Japanese airport. Holding the largest share of slots at Haneda is closer to holding a beachfront property portfolio than to holding gate space — the supply is fixed by physical runways, environmental constraints, and noise abatement, and demand grows with Tokyo itself.

ANA holds a share of Haneda domestic slots roughly on par with Japan Airlines, and an outsized share of the international slots progressively reallocated since the 2010 fourth-runway expansion and the 2020 daytime-slot increase. That position is the foundation of the corporate-travel franchise, the cargo network, and — by extension — the resilience that became visible during the pandemic.

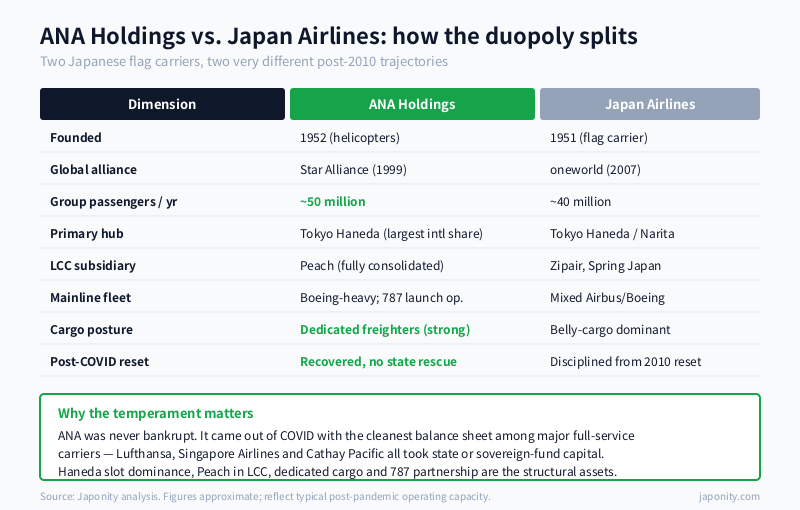

What ANA and JAL actually look like, side by side

The two carriers are often described as a duopoly, which is broadly correct but obscures meaningful structural differences. The table below sketches the comparison.

| Dimension | ANA Holdings | Japan Airlines |

|---|---|---|

| Founded | 1952 (as helicopter operator) | 1951 (as national flag carrier) |

| Holding company since | 2013 | 2010 (post-bankruptcy reset) |

| Global alliance | Star Alliance (since 1999) | oneworld (since 2007) |

| LCC unit | Peach Aviation (fully consolidated) | Zipair Tokyo, Spring Japan |

| Passengers per year (approx.) | ~50 million group total | ~40 million group total |

| Mainline fleet leaning | Boeing-heavy, 787 launch operator | Mixed Airbus/Boeing post-bankruptcy |

| Cargo posture | Dedicated freighters, strong franchise | Belly-cargo dominant, lighter freighter fleet |

| Balance-sheet posture post-COVID | Recovered without state rescue | Continued discipline from 2010 reset |

Both carriers compete on most of the same routes and serve the same Japanese corporate accounts. But the strategic temperament is different. JAL after 2010 became a disciplined, financially conservative carrier under what is sometimes called the Inamori reset — a Kyocera-founder-led cultural rebuild that emphasised unit economics, cost transparency, and per-employee profit metrics. ANA, never having been bankrupt, retained more of the operating culture of an ambitious challenger, with a higher tolerance for capacity additions and lower-yield network growth.

The Peach experiment, and why it worked

Peach Aviation, headquartered in Osaka at Kansai International Airport, launched commercial flights in March 2012 as Japan’s first true low-cost carrier. The capital structure at founding was tripartite: ANA Holdings (then roughly thirty-three percent), the Innovation Network Corporation of Japan (a public-private investment vehicle), and First Eastern Investment Group from Hong Kong. The architecture was deliberate. ANA wanted exposure to the LCC segment without contaminating the mainline cost structure, brand, or labour agreements; outside capital provided the cultural distance required to actually run an LCC differently.

The experiment worked. By 2017 ANA had moved to majority ownership, lifting its stake to approximately seventy-seven point nine percent, and by 2020 Peach was effectively a consolidated subsidiary of the group. The competing AirAsia Japan venture, which had been re-established as a separate joint venture in 2014 after an earlier dissolution, was absorbed into Peach in 2018-2020 and the brand wound down — leaving Peach as the only meaningful domestic LCC anchored to a Japanese parent.

The strategic significance of Peach is not its standalone profitability, which has been modest and volatile. It is two things. First, Peach lets ANA participate in the price-sensitive segment of the domestic market — leisure, visiting-friends-and-relatives, inbound budget tourists — without forcing the mainline to compete on price against pure-play LCCs. Second, it provides a tested low-cost operating template the group can scale internationally as Asian LCC traffic grows. The competing JAL group has had to assemble equivalent positioning more recently through Zipair (long-haul low-cost) and Spring Japan (short-haul), with less time on the runway.

The Boeing 787 partnership

ANA was the launch operator for the Boeing 787 Dreamliner. The carrier placed its first order in 2004, took delivery of the first commercial aircraft in September 2011, and operated the type’s inaugural commercial flight from Tokyo Narita to Hong Kong in October 2011. By any measure, ANA was the closest airline partner Boeing had on the program, including through the early-life battery incidents that grounded the global fleet for several months in 2013.

The 787 fit ANA’s network thinking precisely. The aircraft’s range and economics opened secondary city pairs — Tokyo to Seattle, Tokyo to San Jose, Tokyo to Düsseldorf, Tokyo to Brussels — that did not work on the larger 777-300ER and were marginal on the 767-300ER it replaced. For a carrier with disproportionate access to Haneda but limited room to grow at the mega-hub, the 787 allowed network expansion through frequency and city-pair diversity rather than through aircraft size.

The relationship has continued into the 777X order book and the operation of the 777-300ER fleet alongside the Airbus A380 — the latter operated in three Flying Honu liveries on the Tokyo-Honolulu route, a niche but commercially important franchise. ANA’s overall fleet remains Boeing-leaning, with measured Airbus exposure through the A320 family operated by Peach and the A321 in the mainline.

Cargo: the franchise nobody saw coming until they did

Air cargo had been a steady, unsexy contributor to ANA’s economics for years. Then the pandemic happened. With passenger belly capacity collapsing globally and consumer e-commerce exploding, dedicated freighter operators and combination carriers with credible freighter fleets became indispensable to the global supply chain. ANA Cargo, the group’s dedicated freight subsidiary, was unusually well positioned: a fleet of Boeing 767-300F freighters operating out of Narita and Okinawa’s Naha hub, a long-standing relationship with major Japanese forwarders, and a network that connected Asian manufacturing centres to U.S. and European consumption markets via overnight wide-body capacity.

In the trough quarters of the pandemic, cargo revenue at times became one of the largest individual line items in the group’s revenue mix, materially offsetting the loss of premium-cabin passenger yield. Even as passenger demand recovered through 2023 and 2024, the cargo business has remained a structurally larger contributor than it was pre-pandemic. The Naha hub in particular, which positions ANA’s freighters within four hours of most major Asian cities, has proven to be one of the most underrated strategic assets in the group. For freight forwarders, ANA Cargo is now a more substantial counterparty in Asian air-freight than its pre-pandemic profile suggested.

The post-pandemic financial reset

Japanese aviation came out of the pandemic without the dramatic state interventions seen in Europe and parts of North America. ANA accessed standard liquidity instruments — bank credit lines, subordinated debt instruments, and a roughly three hundred and twenty billion yen public equity offering in November 2020 — but did not undergo a government-led capital restructuring. The combination of pre-pandemic balance-sheet conservatism, the cargo offset, aggressive cost actions including voluntary leave programs, and a methodical capacity restoration meant that by fiscal 2023 the group had returned to profitability and by fiscal 2024 was operating at or above pre-pandemic margins on most key metrics.

That outcome is not trivial. Lufthansa required a roughly nine billion euro German government rescue. Singapore Airlines raised more than twenty billion Singapore dollars from Temasek and subsequent rights issues. Even Cathay Pacific accessed Hong Kong government recapitalisation. Among the major full-service carriers, ANA’s post-pandemic recovery is genuinely distinctive — and is now visible in fleet renewal, hiring, and the resumption of cancelled aircraft orders.

What ANA Components Service quietly does

One of the less-discussed pieces of the group is ANA Components Service, the subsidiary handling aircraft maintenance, repair, and component overhaul for the mainline fleet and increasingly for third-party customers. Aircraft MRO is a niche but capital-light business with long contract cycles and high switching costs. ANA’s MRO infrastructure — concentrated at Haneda, Narita, and Itami — supports its own carriers and foreign airlines that prefer to handle component overhauls regionally rather than ship parts to Europe or North America.

For overseas aerospace suppliers — avionics, landing gear, cabin systems, engine components, composite repair — ANA Components Service is a meaningful customer and a route into broader Japanese aviation MRO. The qualification cycle is slow and the quality-discipline expectations are high, but the relationships, once established, are durable.

Strategic priorities under Shibata

Koji Shibata’s tenure since April 2023 has been organised around three priorities that the company has communicated publicly. The first is sustaining the network recovery, particularly on China and other Asian routes that recovered later than transpacific and transatlantic. The second is fleet renewal, with continued Boeing 787 deliveries, the introduction of the 777X when it enters service, and a deliberately measured Airbus exposure. The third is sustainability and operational decarbonisation, anchored by sustainable aviation fuel offtake agreements, fleet efficiency improvements, and operational measures around routing and fuel burn.

Underneath those sit several less-publicised priorities: integrating Peach more deeply without erasing its low-cost identity, building out cargo as a permanent rather than cyclical contributor, and capturing the inbound travel boom of 2024-2025, driven partly by a weak yen and partly by sustained interest in Japan as a destination — conditions the group is using to lock in long-term corporate contracts and tour-operator relationships.

Why ANA matters to non-Japanese counterparties

For corporate-travel buyers managing global programs that include Japan, ANA is the default Star Alliance option and the carrier with the largest Haneda footprint. For freight forwarders, ANA Cargo is now a more substantial counterparty than its pre-pandemic profile suggested, particularly out of Naha and Narita. For aerospace and MRO suppliers, ANA Components Service is a credible entry point into Japanese aviation supply chains. For inbound investors and partners in Japanese tourism, hospitality, and travel-tech, ANA’s distribution reach into the domestic market — through both the mainline and Peach — is one of the few mass-market consumer channels in the country with both scale and a willingness to partner with foreign firms.

What makes ANA different from JAL is not the route map. It is the temperament. ANA has been the challenger for most of its history, the operator that built into competition rather than being built around it, and the company that emerged from the pandemic without an outside hand on the balance sheet. Those things compound — and they show up in everything from how the airline approaches Boeing to how it manages Peach to how it staffs a new transpacific city pair.

FAQ

Who owns ANA Holdings?

ANA Holdings is a publicly listed company on the Tokyo Stock Exchange (ticker 9202). Ownership is broadly distributed across Japanese trust banks acting on behalf of institutional investors, global asset managers, and individual shareholders. There is no controlling shareholder, no founding family block, and no state ownership stake. A November 2020 public equity offering of approximately three hundred and twenty billion yen modestly diluted existing shareholders but did not introduce a new strategic owner. Cross-shareholdings with selected partners exist but are modest compared with traditional keiretsu structures.

How does ANA compare with Japan Airlines in size?

ANA Holdings is the larger of the two by passengers carried, with approximately fifty million passengers per year across the group at full operating capacity, versus approximately forty million for the JAL group. On revenue, the two are closer, reflecting JAL’s slightly higher international yield mix post-bankruptcy. Both carriers hold roughly comparable shares of Tokyo Haneda domestic slots; ANA holds a larger share of Haneda international slots awarded in the post-2010 expansion rounds. ANA is a Star Alliance member; JAL is in oneworld.

What is the relationship between ANA and Peach Aviation?

Peach Aviation is ANA Holdings’ fully consolidated low-cost carrier subsidiary, headquartered in Osaka at Kansai International Airport. ANA started with approximately a thirty-three percent stake at Peach’s founding in 2011, increased it to approximately seventy-seven point nine percent in 2017, and absorbed the formerly competing AirAsia Japan venture into the Peach platform between 2018 and 2020. Peach now operates an Airbus A320-family fleet on domestic and selected international routes. It is run with operational autonomy from the mainline but is fully part of the group commercially and financially.

Why was ANA the Boeing 787 launch customer?

ANA placed its first Boeing 787 order in 2004 and worked closely with Boeing through the aircraft’s development program. The carrier took delivery of the first 787 in September 2011 and operated the type’s inaugural commercial flight from Tokyo Narita to Hong Kong in October 2011. The aircraft fit ANA’s network strategy of opening secondary international city pairs from Tokyo that did not justify a larger widebody. ANA continued to operate one of the largest 787 fleets in the world and remains a strategically important Boeing customer.

How well did ANA come through the pandemic compared with global peers?

ANA accessed standard liquidity instruments and conducted a roughly three hundred and twenty billion yen equity offering in November 2020 but did not undergo a state-led capital restructuring. By fiscal 2023 the group had returned to profitability, and by fiscal 2024 it was operating at or above pre-pandemic margins on most key metrics. Compared with Lufthansa, Singapore Airlines, Cathay Pacific, and other major full-service carriers that required substantial state or sovereign-fund recapitalisation, ANA’s post-pandemic recovery is genuinely distinctive — supported by the cargo offset, balance-sheet conservatism, and a methodical capacity restoration.

Working with ANA Holdings

For corporate-travel buyers, the practical entry point to ANA is through the airline’s corporate sales organisation and its Star Alliance corporate program, with negotiated fares, on-site account management, and integration into global travel management company workflows. For freight forwarders, ANA Cargo offers direct contracting, scheduled freighter capacity out of Narita and Naha, and specialised handling for pharmaceutical, automotive, and high-tech shipments. For aerospace, MRO, and component suppliers, ANA Components Service and the group’s procurement organisation handle qualification, typically through a multi-stage engineering review and a long-tail relationship cycle.

Beyond the airline itself, the broader ANA group ecosystem — ground handling, catering, IT services, travel agencies, and the ANA Trading subsidiary — represents a substantial set of additional commercial relationships that foreign suppliers can pursue independently of the mainline carrier.

If your company provides corporate travel services, freight or logistics solutions, aerospace components, MRO services, sustainable aviation fuel, in-flight technology, or hospitality and tourism partnerships relevant to ANA — or if you are evaluating Japan inbound travel and cargo capacity as part of a regional strategy — Japonity’s business matching service can help structure a credible first conversation with the right counterparty inside the ANA group.

Related from Japonity — Japan’s airlines

- Japan Airlines — The bankrupt flagship reborn under Inamori’s Amoeba Management

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →