When Warren Buffett disclosed in August 2020 that Berkshire Hathaway had bought into Japan’s five general trading houses, Mitsubishi Corporation stood at the head of the list — the largest by assets, the deepest in upstream resources, and the most exposed to the cyclical swings of liquefied natural gas, copper, iron ore and oil that have historically defined what a sogo shosha is. Four years later Mitsubishi Corp surfaced again in a way that surprised observers: it joined KDDI, the telecoms group, to take Lawson convenience stores private in a 2024 deal valuing the chain at roughly 1 trillion yen and splitting ownership approximately fifty-fifty. Around the same time the company briefly crossed a market-cap threshold that made it Japan’s largest non-bank private-sector company by equity value. The pairing of those facts — the largest resource-heavy trading house and the buyer of the country’s third-largest convenience-store chain — is the story Mitsubishi Corp is now telling investors. The first half of its century-and-a-half history was about scale through commodities. The second act, every executive at the Marunouchi headquarters will say, is about consumer, digital and food.

Iwasaki, the Mitsubishi keiretsu and the trading-company question

Mitsubishi Corporation’s lineage runs back further than the company itself. In 1870 a samurai-turned-shipping-entrepreneur named Iwasaki Yataro founded a maritime business in Tosa, on the southern island of Shikoku, that within a decade became the dominant shipping line linking Tokyo, Osaka and the western ports. He named it Mitsubishi — three diamonds — and the three-leaf crest survives, with minor modifications, on every Mitsubishi-affiliated firm today. Iwasaki’s company diversified rapidly into shipbuilding, mining, banking, insurance and trading, and by the late Meiji period the Iwasaki family controlled one of the four great zaibatsu — Mitsubishi, Mitsui, Sumitomo and Yasuda — that organised industrial Japan.

The trading arm was formally incorporated as Mitsubishi Shoji Kaisha in 1918, growing into one of the world’s largest trading firms by volume in the inter-war period. In 1947 the Occupation authorities, suspicious of zaibatsu concentration, ordered its dissolution into more than a hundred successor firms. The fragmentation lasted seven years. In 1954, after the Occupation ended, the constituent pieces were recombined under the present name Mitsubishi Corporation. The recombination set the template by which the trading house would operate as connective tissue of the broader Mitsubishi group — Mitsubishi Heavy Industries, Mitsubishi Electric, Mitsubishi UFJ Financial Group, Mitsubishi Estate, Mitsubishi Chemical and dozens of others — without formal cross-shareholding bonds that would later face investor pressure.

What a sogo shosha actually is

The phrase sogo shosha translates literally as “general trading company,” but the description undersells what these institutions do. A modern sogo shosha is part commodity trader, part private-equity firm, part project-finance arranger and part logistics operator. The five largest — Mitsubishi, Mitsui, Itochu, Sumitomo and Marubeni — touch every link of the supply chains that feed, fuel, clothe and house Japan, and increasingly the rest of Asia.

The business model has cycled through phases. In the 1960s and 1970s the houses were middlemen on thin margins. Disintermediation by manufacturer clients squeezed those margins through the 1980s and 1990s, and the firms pivoted toward investment. By the 2010s the dominant model was equity stakes in producing assets — iron ore mines, LNG fields, copper smelters — supplemented by the trading flow they generated. The 2020s have brought a further shift toward consumer, digital and decarbonisation plays. Among the five, Mitsubishi Corp has historically sat furthest along the resource-heavy axis — a position that generated extraordinary profits at commodity-cycle peaks (the company posted a then-record net profit of roughly 1.18 trillion yen in fiscal 2022) and equally extraordinary swings when prices retreated. The challenge of the current decade is to keep the resource franchise running for cash while building a second engine with steadier returns.

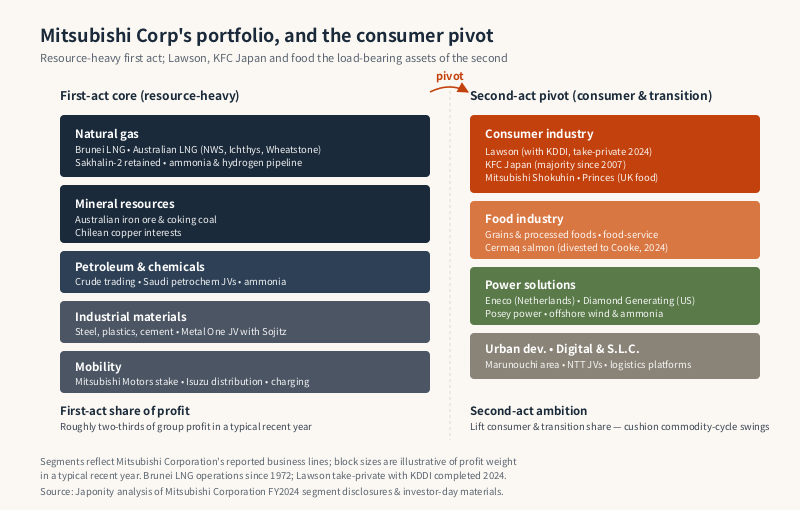

The segment portfolio, sketched

Mitsubishi Corp reports its earnings across roughly ten business segments. The table below sketches the landscape and where the profit centre of gravity has historically sat; weights are approximate and reflect a typical recent year.

| Segment | What it covers | Profit weight | Signature asset or franchise |

|---|---|---|---|

| Natural gas | LNG projects, gas trading, midstream | Very high | Brunei LNG, Australian LNG, Sakhalin-2 retained interest |

| Mineral resources | Iron ore, coking coal, copper | Very high | Australian iron ore and coal, Chilean copper interests |

| Petroleum & chemicals | Crude trading, petrochemicals, ammonia | Medium | Saudi petrochemical JVs, ammonia decarbonisation pipeline |

| Industrial materials | Steel, plastics, cement, automotive materials | Medium | Metal One steel joint venture with Sojitz |

| Food industry | Salmon, grains, processed foods, food-service | Medium-high | Cermaq integrated salmon (divested 2024), grain elevators |

| Consumer industry | Retail, lifestyle brands, fashion distribution | Medium-high | Lawson (with KDDI, since 2024), KFC Japan |

| Power solutions | Generation, transmission, renewables | Medium | Eneco (Netherlands), Diamond Generating in the US |

| Mobility | Auto distribution, mobility services | Medium | Mitsubishi Motors stake, Isuzu distribution networks |

| Urban development & infrastructure | Real estate, water, transport infra | Lower | Marunouchi area redevelopment exposure |

| Digital, S.L.C., others | Software, supply-chain logistics, finance | Lower | NTT joint ventures, digital-platform investments |

The structural fact is that the top two segments, natural gas and mineral resources, have for most of the last fifteen years generated the majority of group profit. That concentration is what gives Mitsubishi Corp the highest earnings volatility among the five sogo shosha, and it is what management is trying to dilute.

The LNG franchise, still the load-bearing wall

Mitsubishi’s natural-gas business runs back nearly half a century. In the early 1970s the company partnered with Shell and the Brunei government to develop Brunei LNG, one of the world’s first commercial liquefied natural gas projects, beginning exports to Japan in 1972. The Brunei template — long-term off-take contracts with Japanese utilities, equity in upstream production and liquefaction infrastructure, and a trading arm capturing both equity dividends and commercial margins — was replicated over following decades in Australia (North West Shelf, Ichthys, Wheatstone), Malaysia, Russia and elsewhere.

The Russian piece deserves attention. Mitsubishi holds approximately 10 percent of Sakhalin-2, the Russian Far East LNG project operated until 2022 by Gazprom and Shell. When Russia invaded Ukraine in February 2022, Shell announced its withdrawal. Mitsubishi and Mitsui, the other Japanese partner, chose differently. After consultation with the Japanese government, which considers Sakhalin-2 strategically critical — the project supplies roughly nine percent of Japan’s LNG imports — Mitsubishi retained its position. The decision is one of the cleanest examples of how sogo shosha investment behaviour is shaped not just by commercial logic but by an implicit mandate to underwrite Japanese energy security. Looking forward, the company has pushed into adjacent low-carbon fuels — ammonia, hydrogen, e-methane — with pilots in the Middle East and Australia aiming to ship low-carbon ammonia to Japanese power plants by the late 2020s.

Lawson, KFC Japan and the consumer pivot

If the LNG franchise is the load-bearing wall of Mitsubishi Corp’s first century, the Lawson take-private with KDDI in 2024 is the signature move of its second. Lawson is Japan’s third-largest convenience-store chain, with roughly 14,000 stores domestically and several thousand more in China, Indonesia, the Philippines and Thailand. Mitsubishi Corp had held a controlling stake since the early 2000s, after taking over Daiei’s ownership position, and had operated the chain through long-tenure leadership including Takeshi Niinami, later Suntory boss.

The 2024 transaction brought in KDDI, the second-largest Japanese mobile carrier, as an equal partner, with each ending at roughly fifty percent and Lawson delisting from the Tokyo Stock Exchange. The rationale united two complementary capability sets. Mitsubishi brings the supply chain — food manufacturing, fresh-produce sourcing, integrated logistics — while KDDI brings the digital layer: payment rails through Ponta and au Pay, location-based services, and a customer-data graph spanning tens of millions of mobile subscribers. The aspiration is to recast the convenience store from a transactional retail format into a “real-tech retail” platform combining physical store density with mobile-native commerce.

Lawson is the headline, but the consumer pivot extends further. Mitsubishi Corp owns a majority position in KFC Japan, the master franchisee of the American fried-chicken chain, after acquiring control from Mitsubishi Trust in 2007; the menu has been aggressively localised and the chain continues to add stores while many quick-service rivals contract. Beyond KFC the Consumer Industry segment touches Mitsubishi Shokuhin, Japan’s largest food wholesaler, stakes in Princes Limited in the UK, and various apparel-distribution joint ventures.

Salmon, food security and the Cermaq chapter

The food segment offers an instructive case study of how Mitsubishi makes and unmakes long-horizon bets. In 2014 the company paid approximately 1.4 billion dollars to acquire Cermaq, the Norwegian-listed integrated salmon-farming company with operations in Norway, Chile and Canada. The acquisition was framed as a food-security investment: protein demand would rise structurally with Asian middle-class growth, aquaculture would take share from wild-catch fisheries, and integrated control of farming, processing and distribution would generate margins closer to consumer-branded food than to commodity protein. Within a few years Cermaq had become one of the world’s largest farmed-salmon producers, and Mitsubishi had built sales channels into Japanese supermarkets and food-service.

A decade later, in 2024, the company sold Cermaq to Cooke Aquaculture, the Canadian seafood group, for a reportedly multi-billion-dollar sum. Integrated farming had proved capital-intensive and exposed to environmental and biological risk, and Consumer Industry offered better risk-adjusted opportunities. The Cermaq cycle — acquire at the high water mark of the food-security thesis, build operationally, exit when better uses for the capital appear — is evidence in the ongoing debate about whether sogo shosha portfolio management is closer to private equity than to a traditional industrial conglomerate.

The Mitsubishi Motors question

The most-watched single relationship in the Mobility segment is the equity position in Mitsubishi Motors. The trading company has held the stake for decades, weathering the carmaker’s 2016 fuel-economy data scandal, its rescue by the Nissan-Renault alliance, and the realignment of that alliance after the 2018 arrest of Carlos Ghosn. Mitsubishi Corp has used the position to support the carmaker’s regional strength in Southeast Asia, where the trading-house distribution network dovetails with the carmaker’s manufacturing footprint. The segment has begun a measured rotation toward charging infrastructure and battery supply.

Power, Posey and the energy transition

Mitsubishi Corp’s Power Solutions segment is among the better-positioned within the five sogo shosha for the energy transition. The franchise is built around three platforms: Diamond Generating, a US independent power producer with thermal and renewable assets; Eneco, a Dutch utility acquired in 2020 with strong wind exposure across north-west Europe; and a network of project-specific joint ventures including the Posey power assets in North America, offshore-wind partnerships in Asia, and a growing pipeline of hydrogen and ammonia projects feeding the natural-gas segment’s decarbonisation strategy. The financial logic is steady-cash, long-duration assets backed by regulated or contracted revenue, providing a counterweight to commodity-cycle volatility — and management’s recent medium-term plan has lifted the segment’s share of new investment accordingly.

Governance, scale and the Buffett endorsement

Among the five sogo shosha, Mitsubishi Corp operates with the most pronounced sense of institutional weight. Headquartered in Marunouchi, central Tokyo, adjacent to Mitsubishi Estate’s flagship developments, the company employs roughly 80,000 people across consolidated subsidiaries and over 5,000 at the parent. Internal promotion is the dominant career track. Chief executives typically serve six to eight years and are succeeded by long-tenure insiders. Katsuya Nakanishi has served as president and chief executive since April 2022, succeeding Takehiko Kakiuchi in the established generational pattern.

The Buffett investment, disclosed in 2020 and progressively raised through 2023 and beyond, gave the entire sogo shosha sector a credentialed Western endorsement. Buffett funded the position in part by issuing yen-denominated debt — an elegant carry trade pairing cheap Japanese liabilities with equity stakes in firms paying meaningful dividends. In his 2023 annual letter he praised the trading houses for capital discipline and willingness to buy back shares. Mitsubishi Corp, as the largest of the five, benefitted disproportionately when valuations and trading volumes pushed up; the market capitalisation crossed several symbolic thresholds in 2023 and 2024, briefly putting Mitsubishi Corp ahead of all banks and most industrials by equity value.

Whether the endorsement endures depends on whether the company can execute the consumer and decarbonisation pivot well enough to dampen historical earnings volatility. The Lawson-KDDI deal is the most visible signal of intent. The Cermaq exit shows the firm will recycle assets that no longer fit. The LNG and metals franchises continue to generate the cash that funds the rotation.

What comes next

Mitsubishi Corp’s medium-term plan sketches a portfolio rotation rather than a revolution. Resources will be run for cash, with disciplined replacement capex rather than aggressive growth. Consumer, food and digital businesses will absorb an outsized share of new investment, with Lawson as the lead vehicle. Power and decarbonisation will scale through Eneco, Diamond Generating and the LNG-adjacent low-carbon pipeline. The execution risk is real — sogo shosha pivots have a long record of moving slower than promised — but Mitsubishi has scale advantages smaller houses cannot match: the financial firepower of peak-cycle resource earnings, and the keiretsu network giving every initiative access to capability across the broader Mitsubishi group. Whether those advantages translate into the consumer-focused second act every sogo shosha is now trying to write will be the defining question of the next decade.

FAQ

Why did Warren Buffett invest in Mitsubishi Corporation and the other Japanese trading houses?

Berkshire Hathaway disclosed approximately 5 percent stakes in each of the five sogo shosha — Mitsubishi, Mitsui, Itochu, Sumitomo and Marubeni — in August 2020, subsequently raising each position beyond 9 percent through 2023 and 2024. Buffett cited the trading houses’ diversified earnings, disciplined capital allocation, low valuations relative to free cash flow and willingness to return capital to shareholders. Mitsubishi Corporation, as the largest of the five by assets and market capitalisation, has benefitted disproportionately from the resulting investor attention, though its earnings remain the most cyclical of the group because of its resource concentration.

Why did Mitsubishi Corp take Lawson private with KDDI in 2024?

Mitsubishi Corp had been the controlling shareholder of Lawson, Japan’s third-largest convenience-store chain, since the early 2000s. The 2024 transaction brought in KDDI, the major telecoms group, as a roughly equal partner — each ending with approximately 50 percent — and delisted Lawson from the Tokyo Stock Exchange in a deal valuing the chain at approximately 1 trillion yen. The strategic logic combines Mitsubishi’s supply-chain and food-manufacturing capabilities with KDDI’s digital, payments and customer-data infrastructure, positioning Lawson as a “real-tech retail” platform spanning physical stores and mobile-native commerce.

What is Mitsubishi Corporation’s relationship to the broader Mitsubishi group and Mitsubishi Motors?

Mitsubishi Corporation is the trading-house arm of the broader Mitsubishi group that traces back to Iwasaki Yataro’s 1870 shipping venture. The group dissolved under Occupation antitrust action in 1947 and recombined in 1954, with the constituent companies linked by historical ties, the three-diamond brand, and overlapping but no longer mandatory cross-shareholdings. Mitsubishi Corp holds an equity stake in Mitsubishi Motors as part of its Mobility segment, distinct from Mitsubishi Heavy Industries (the engineering arm) and Mitsubishi UFJ Financial Group (the banking arm), each of which is a separately listed and independently managed entity.

How does Mitsubishi Corp differ from Itochu and the other sogo shosha?

All five major sogo shosha overlap heavily in scope, but their centres of gravity differ. Mitsubishi Corp and Mitsui are weighted toward upstream resources — LNG, iron ore, copper, energy infrastructure — which makes their earnings the most cyclical of the five and gives Mitsubishi Corp the highest profit volatility through commodity cycles. Itochu derives roughly two-thirds of profit from non-resource segments including textiles, food, distribution, ICT and financial services. Sumitomo blends metals with media and real estate; Marubeni is heavy in power generation and agri-inputs. Mitsubishi Corp’s current strategic priority is to dilute the resource concentration through consumer, food and digital expansion, with Lawson and KFC Japan as the lead platforms.

Why did Mitsubishi Corporation sell Cermaq in 2024?

Mitsubishi Corp acquired Cermaq, the Norwegian integrated salmon-farming company with operations in Norway, Chile and Canada, in 2014 for approximately 1.4 billion dollars as part of a long-horizon food-security thesis. Over the following decade Cermaq grew into one of the world’s largest farmed-salmon producers, but the integrated-aquaculture business proved capital-intensive and exposed to environmental and biological risk. In 2024 Mitsubishi sold Cermaq to Cooke Aquaculture, the Canadian seafood group, reallocating the proceeds toward consumer-industry and decarbonisation investments where management saw better risk-adjusted returns. The cycle is widely cited as an example of sogo shosha portfolio rotation in action.

Working with Mitsubishi Corporation

For overseas brands, exporters, energy developers and capital partners seeking distribution into Japan or co-investment across Asia, the sogo shosha remain unmatched as relationship-led gateways — and Mitsubishi Corporation, with its scale, energy-infrastructure depth and growing consumer-platform footprint through Lawson and KFC Japan, is often the most natural fit for energy, food, mobility and large-scale infrastructure businesses. Japonity introduces qualified overseas companies to Japanese trading houses, brand operators and distributors through its business matching service. If you are exploring a Japan-market entry, an LNG or decarbonisation partnership, a consumer-brand distribution deal or a co-investment with a sogo shosha, get in touch to start a conversation.

Related from Japonity — Japan’s sogo shosha (trading houses)

- Itochu Corporation — The consumer-oriented sogo shosha Buffett bet on

- Mitsui & Co. — The trading house most exposed to the energy transition

- Sumitomo Corporation — The conservative shosha — steel distribution and J:COM

- Marubeni Corporation — The textile-to-electrons shosha — power IPP, Helena, Gavilon

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →