When Warren Buffett disclosed in 2020 that Berkshire Hathaway had quietly accumulated roughly 5% stakes in each of Japan’s five major sogo shosha — and then steadily increased them through 2024 — Mitsui & Co., Ltd. was the most natural fit for his thesis. The company that traces its lineage to the Mitsui Echigoya dry goods house of 1673 had spent a century and a half doing precisely what Buffett admires: buying durable assets, holding them across cycles, and compounding cash flows from things the modern economy cannot do without. Iron ore. Liquefied natural gas. Copper. Hospital beds. Today Mitsui & Co. operates one of the world’s most geographically distributed LNG portfolios — equity interests stretching from Sakhalin-2 in the Russian Far East to Cameron LNG in Louisiana to the stalled but vast Mozambique LNG project — alongside an iron ore franchise built on partnerships with Vale in Brazil and BHP in Australia, and a fast-growing healthcare arm anchored by an approximately 33% stake in Kuala Lumpur-listed IHH Healthcare. It is, in short, the sogo shosha most directly exposed to the energy transition’s central contradictions: the world needs less carbon, but also more reliable molecules and metals to get there. How Mitsui & Co. navigates that tension over the next decade will matter to LNG buyers in Europe, mining customers in China, and hospital operators across South-East Asia.

From Echigoya kimono shop to global trader

Mitsui & Co.’s origin story is older and more deliberate than that of any other Japanese trading house. The Mitsui family established the Echigoya dry goods store in Edo (now Tokyo) in 1673, pioneering cash-on-delivery retail at fixed prices — a radical departure from the credit-based commerce of the era. From that merchant base the family built one of Japan’s earliest financial institutions, and in 1876, four years after the Meiji government opened the country to foreign commerce, founded Mitsui Bussan as a dedicated trading company. It is the oldest of the modern shosha by any reasonable accounting.

The first 70 years tracked the arc of imperial Japan: cotton, coal, machinery, sugar, and increasingly the supply chain of empire. After Japan’s defeat in 1945, the Allied occupation dissolved the major zaibatsu, and in 1947 Mitsui Bussan was broken into more than 200 successor firms. Reassembly began almost immediately. By 1959 the principal fragments had recombined into the present-day Mitsui & Co., Ltd., and the company rejoined the front rank of Japanese commerce just as the post-war economic miracle hit its stride. The dissolution-and-reconstitution episode left a cultural imprint that persists: a preference for syndicate-style co-investment, deep equity positions held for decades, and an institutional memory that distrusts ideological orthodoxy of any kind.

What a sogo shosha actually does

Foreign observers often misread the shosha as either traders or conglomerates. Both descriptions miss the point. Mitsui & Co. is best understood as a permanent-capital investment platform with a global commercial nervous system attached. Roughly two-thirds of its profit comes from equity-method affiliates and consolidated subsidiaries — businesses Mitsui owns wholly or in partnership — rather than from trading margins on the cargoes that move through its books. The trading flows remain enormous, but they are increasingly the connective tissue around the asset base, not the main event.

The headline numbers convey the scale. Mitsui & Co. reported approximately ¥1.06 trillion in net profit attributable to shareholders for the fiscal year ended March 2024, on revenue of about ¥13.3 trillion, against shareholders’ equity of approximately ¥7.6 trillion. Roughly 47,000 employees work across more than 60 countries. The Otemachi headquarters in central Tokyo sits in a tower designed in part to be the company’s twenty-first-century stage; the building’s atrium is intentionally large enough to host industry events for the partners and customers Mitsui needs to keep close.

The business segment map

Mitsui & Co. organizes itself into seven reporting segments. Reading them in order tells you where the cash is, where the strategy is moving, and where the friction lies.

| Segment | What it does | Signature assets / partners | Strategic role |

|---|---|---|---|

| Mineral & Metal Resources | Iron ore, copper, coal, aluminum equity production and trading | Vale (Brazil iron ore), BHP (Robe River, Western Australia), Anglo American copper | Cash engine; cyclical core |

| Energy | LNG, oil & gas equity production, power assets | Sakhalin-2, Cameron LNG (Louisiana), Mozambique LNG, Browse, Tangguh, Qatar, Oman, Abu Dhabi, Brunei | Largest LNG portfolio among shosha |

| Machinery & Infrastructure | Power generation, ships, mobility, automotive | IPP/IWPP across Middle East and Asia, Penske Automotive (US), VLCC fleets | Long-duration infrastructure cash flows |

| Chemicals | Basic chemicals, fertilizers, methanol, ammonia, plastics | Methanol JVs in Trinidad; ammonia and low-carbon fuels under development | Transition fuels bridge |

| Iron & Steel Products | Steel distribution, oil-country tubular goods, automotive steel | Game Changer Detroit, Steel Technologies (US), regional service centers | Downstream margin and customer access |

| Lifestyle | Food & agribusiness, healthcare, retail, fashion | IHH Healthcare (~33%), Mitsui Sugar, Multigrain (grain origination in Brazil) | Defensive growth pillar |

| Innovation & Corporate Development | Finance, real estate, IT services, ventures | Mitsui Knowledge Industry, MBK Real Estate, Moov AI & data ventures | Digital and capital-allocation flexibility |

The LNG portfolio: scale, scars and strategic options

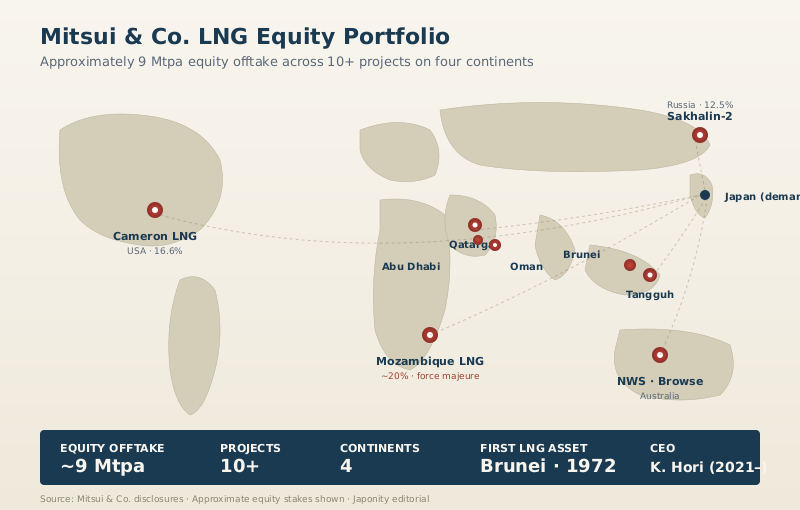

If one business defines modern Mitsui & Co., it is liquefied natural gas. The company has been an equity participant in LNG projects since the Brunei LNG facility came online in 1972 — the world’s second commercial LNG project after Algeria’s Camel — and has compounded those positions for half a century. Today Mitsui holds equity in projects across Brunei, Abu Dhabi (Das Island), Oman, Qatargas, Indonesia’s Tangguh, Australia’s North West Shelf and Browse, Sakhalin-2 in Russia, Cameron LNG in the United States, and Mozambique LNG on Africa’s Indian Ocean coast. The total equity-share LNG offtake runs to approximately 9 million tonnes per annum, making Mitsui one of the most diversified non-IOC LNG portfolios in the world.

Two assets bracket the strategic challenge. Sakhalin-2, in which Mitsui retains a 12.5% stake alongside Mitsubishi (10%) and Russian operator Sakhalin Energy, became politically radioactive after Russia’s 2022 invasion of Ukraine. Tokyo’s official position has been that Japanese energy security justifies continued participation; the equity has been preserved through a forced restructuring into a Russian-incorporated successor entity. The asset still produces, still delivers cargoes into Japan, and still generates cash — but the optionality around it has narrowed considerably.

Mozambique LNG is the other bookend. Mitsui holds an approximately 20% stake in the project, operated by TotalEnergies, which has been under force majeure since insurgent attacks in Cabo Delgado in 2021 forced an evacuation of the site. The project remains paused as of 2026; restart timing is the single largest swing factor in Mitsui’s energy segment outlook. Between these two extremes sits Cameron LNG, a 16.6%-owned export facility in Louisiana that has functioned as Mitsui’s flagship American molecule and as a hedge against Asian supply concentration.

What LNG buyers should take away

For European utilities and Asian power companies sourcing LNG, Mitsui is unusual in that it can offer optionality across geographic basins, currency exposures, and contract structures (oil-indexed, Henry Hub-indexed, JKM-indexed) from a single counterparty. The trade-off is that any given cargo carries Mitsui’s portfolio risk premium — a discipline that historically has not been about being cheapest, but about being reliable across decades.

Iron ore: the quiet compounder

Mitsui & Co.’s mineral resources segment is, in plain financial terms, the engine room. The company holds long-standing equity interests in Vale’s iron ore operations in Brazil — through the Valepar holding structure and direct stakes in specific mines — alongside its position in BHP’s Robe River and other Pilbara assets in Western Australia, a stake originally taken in 1971 that has paid for itself many times over. Mineral & Metal Resources has in most recent years contributed the single largest share of segment profit.

The narrative around iron ore has shifted. China’s property-driven demand peak appears to have passed, and the long-run growth story is now about India, South-East Asia and the gradual greening of steelmaking through direct-reduced iron and electric arc furnaces. Mitsui has been deliberate about investing in higher-grade ore — Carajás material from Brazil in particular — that commands a premium in a low-carbon steel future. Customers in Japan, Korea, China and increasingly India can expect Mitsui to be present in any conversation about iron ore supply security through 2040.

Healthcare: the third pillar nobody quite expected

The most consequential strategic move of the past decade has been Mitsui’s build-out of a healthcare franchise centered on IHH Healthcare Berhad. Listed in Kuala Lumpur and Singapore, IHH operates roughly 80 hospitals across Singapore, Malaysia, Turkey, India, China and Central Europe under brands including Mount Elizabeth, Gleneagles, Acibadem and Fortis. Mitsui became IHH’s largest shareholder in 2018, taking a stake from Khazanah Nasional, and has since increased its holding to approximately 33%.

The logic is demographic. Asia’s middle class is aging, urbanizing and demanding higher-quality care precisely as public health systems strain. IHH is positioned across the income spectrum and across the region’s most populous markets. For Mitsui the platform delivers something the resources businesses cannot: secular volume growth largely uncorrelated with commodity cycles. The segment has been complemented by smaller bets in nutrition (a stake in Belgian nutrition group Nutreco’s affiliates), animal protein, and pharmaceutical distribution.

For hospital operators and medical device suppliers in Japan considering ASEAN expansion, Mitsui’s IHH platform is the most direct path into a credentialed, multi-market hospital chain. The company’s commercial logistics arm can move equipment, the financing arm can structure deals, and the Lifestyle segment in Tokyo provides decision-making proximity.

The energy transition: opportunity and contradiction

Mitsui’s official medium-term plan, refreshed under President and CEO Kenichi Hori since April 2021, sets out three pillars: Industrial Business Solutions, Global Energy Transition, and Wellness Ecosystem Creation. The Energy Transition pillar is where the contradictions live. Mitsui is simultaneously expanding LNG capacity (still a fossil fuel), investing in clean ammonia and hydrogen value chains (the next decade’s potential winners), participating in offshore wind in Europe and Asia, and exploring carbon capture, utilization and storage (CCUS) opportunities.

The company’s position is that Japan’s energy security cannot be reorganized on idealistic timelines, that LNG is a 30-year asset class, and that the credible path to decarbonization runs through bridge molecules — not around them. That stance is congruent with how Tokyo policymakers see the world. It also exposes Mitsui to two kinds of risk: the carbon intensity of its portfolio drawing pressure from European institutional investors and rating agencies, and the chance that ammonia or hydrogen technologies arrive faster (or slower) than the asset base assumes.

Governance, capital allocation and the Buffett seal

Berkshire Hathaway’s accumulated stake in Mitsui & Co. (now approximately 8–10% across the five shosha investments combined) has had a real second-order effect on Tokyo corporate governance. Mitsui has been progressively raising shareholder returns — share buybacks now run routinely into the hundreds of billions of yen per fiscal year, and the dividend has been raised consistently. Return on equity has stabilized in the mid-teens. The pivot from book-building empire to capital-disciplined compounder is well underway, and Buffett’s continued endorsement (he confirmed in his 2024 annual letter that the positions are intended to be held long-term) gives Hori political cover to keep pushing.

Capital allocation now leans visibly toward bolt-on healthcare and digital acquisitions, selective LNG expansion (Cameron train expansion and Ruwais LNG in Abu Dhabi being recent commitments), and divestment of non-core legacy positions. The cultural shift inside the building — from “deal-doer” to “owner-operator” — is real and ongoing.

Who should be paying attention

Four constituencies should understand Mitsui & Co. with some precision. European and Asian LNG buyers negotiating long-term supply contracts will find Mitsui’s portfolio uniquely diversified and its credit profile among the strongest in the merchant LNG world. Hospital operators, medtech companies and pharma distributors looking at ASEAN should treat the IHH platform as a serious channel option rather than a curiosity. Mining customers and steelmakers negotiating Pilbara or Brazilian ore have Mitsui at the table whether they realize it or not. And technology firms and venture investors — particularly in industrial AI, climate tech and digital health — should know that Mitsui’s Innovation & Corporate Development segment is actively writing checks, and that a Mitsui partnership is one of the more efficient routes into the broader Japanese industrial customer base.

The sogo shosha model has been declared obsolete several times over the past 40 years. Each time, Mitsui & Co. has reorganized itself around the next era’s scarcity — energy in the 1970s, metals in the 1990s and 2000s, healthcare and energy transition in the 2020s — and emerged larger. The next decade will test whether that pattern holds when scarcity is defined as much by carbon constraints as by molecules and metals. Three and a half centuries in, the bet on Mitsui’s adaptability is still being placed.

FAQ

Q1. How does Mitsui & Co. differ from Mitsubishi Corporation and Itochu?

Mitsui & Co. is the most heavily weighted toward natural resources and energy among the top shosha, with iron ore and LNG forming its profit core. Mitsubishi Corporation has a more balanced portfolio with significant exposure to integrated infrastructure and consumer businesses, while Itochu skews toward consumer-facing assets like food retail and apparel. All three are diversified, but their center of gravity differs noticeably.

Q2. What is Mitsui & Co.’s exposure to Russia after Sakhalin-2?

Mitsui retains its approximately 12.5% equity in the restructured Sakhalin-2 entity, in line with Japanese government policy on energy security. The asset continues to deliver LNG cargoes to Japanese utilities. Beyond Sakhalin-2, Mitsui’s direct Russian exposure is limited and has been progressively reduced since 2022.

Q3. Why did Mitsui invest so heavily in IHH Healthcare?

Healthcare offers secular demand growth largely uncorrelated with commodity cycles, and IHH provides a single credentialed platform across Singapore, Malaysia, Turkey, India and Central Europe. The investment is the cornerstone of Mitsui’s Wellness Ecosystem Creation strategy and a deliberate counterweight to cyclical resources earnings.

Q4. Is Mozambique LNG ever going to restart?

TotalEnergies, the operator, has signaled readiness to lift force majeure as security conditions stabilize, but a definitive restart date remains uncommitted as of 2026. For Mitsui, the project is a deferred call option — a large one — rather than an active asset. Restart timing is the single biggest swing factor in the company’s energy segment trajectory.

Q5. How do foreign companies typically engage with Mitsui & Co.?

Engagement usually starts with the relevant segment headquarters in Otemachi (Tokyo) or the major overseas office (London, Houston, Singapore, Sydney). For LNG, contact the Energy Business Unit; for hospital partnerships, the Wellness & Nutrition Business Unit; for industrial technology, Innovation & Corporate Development. Initial conversations typically explore strategic fit before commercial terms — a feature, not a delay, of the Mitsui process.

Working with Mitsui & Co

Whether you are a global LNG buyer, an ASEAN healthcare operator, a mining customer, or a technology company seeking a Japanese partner with a global commercial footprint, Mitsui & Co. is one of the most consequential counterparties in your category. Japonity can support introductions and partnership development across Japan’s leading sogo shosha and their portfolio companies.

Learn more about partnership and business-matching opportunities at Japonity Business Matching.

Related from Japonity — Japan’s sogo shosha (trading houses)

- Itochu Corporation — The consumer-oriented sogo shosha Buffett bet on

- Mitsubishi Corporation — The biggest sogo shosha — Lawson take-private and consumer pivot

- Sumitomo Corporation — The conservative shosha — steel distribution and J:COM

- Marubeni Corporation — The textile-to-electrons shosha — power IPP, Helena, Gavilon

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →