From the 52nd floor of the Shinjuku Sumitomo Building — the triangular glass monolith that pierced Tokyo’s western skyline in 1974 and remained, for nearly half a century, one of the city’s most distinctive silhouettes — the geography of Japanese real estate looks deceptively simple. To the east, in Marunouchi, sits Mitsubishi Estate’s empire of grey-suited tenants. To the south, in Nihonbashi and Hibiya, Mitsui Fudosan’s mixed-use complexes hum with shoppers and salarymen. And here, in Shinjuku, sits Sumitomo Realty & Development — the third of the so-called “big three” property companies that, between them, own a disproportionate slice of central Tokyo’s most valuable square metres. But the three are not interchangeable. Mitsubishi Estate is the landlord-aristocrat. Mitsui Fudosan is the urban placemaker. Sumitomo Realty is something else entirely: the leveraged developer — the one that builds the most buildings, sells the most condominiums, and carries the most debt to do so. For foreign tenants weighing a Tokyo office, foreign lenders weighing exposure to Japanese property, or foreign investors weighing the J-REIT-adjacent equity story, understanding that distinction matters more than the surface-level similarity of three blue-chip names.

The Sumitomo zaibatsu’s quietest survivor

Sumitomo Realty & Development Co., Ltd. (住友不動産株式会社, Sumitomo Fudōsan) was incorporated in 1949, but its institutional roots reach back nearly four centuries to the Sumitomo family’s copper-trading and banking operations in Osaka and Kyoto. When the postwar Allied occupation dissolved Japan’s zaibatsu conglomerates, the property assets of the old Sumitomo group were reconstituted into an independent listed entity — initially small, regionally focused, and overshadowed by the better-located Mitsubishi and Mitsui holdings in central Tokyo.

What followed was, in retrospect, one of postwar Japan’s most patient compounding stories. Sumitomo Realty did not inherit Marunouchi. It did not inherit Nihonbashi. It had to buy its way into central Tokyo, parcel by parcel, decade by decade — and it did so with a balance sheet willing to carry leverage that its rivals would not. By the early 1970s it had assembled enough Shinjuku land to commission what became, on completion in 1974, one of the district’s first three super-high-rise office towers: the 210-metre Shinjuku Sumitomo Building, immediately recognisable for its triangular floor plate and the hollow atrium that runs almost the full height of the structure. The building was a statement — that Tokyo’s office market had a western pole, not just an eastern one, and that Sumitomo Realty intended to anchor it.

Five decades on, the company is headquartered in that same Shinjuku tower, listed on the Tokyo Stock Exchange Prime Market under code 8830, and ranked the third-largest of the country’s property developers by market capitalisation — behind Mitsubishi Estate and Mitsui Fudosan, but ahead of every other listed peer. Junichi Kuranari, who became chairman and CEO in 2024 after a long internal career, presides over roughly six segments of revenue and a development pipeline that, on any reasonable cyclically-adjusted measure, is among the largest in the country.

The three-way oligopoly: how Sumitomo Realty differs

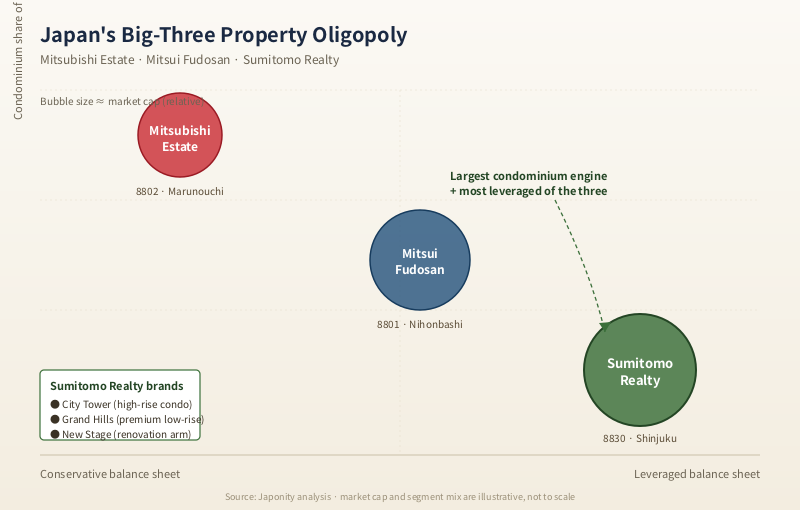

The temptation, particularly for foreign analysts new to the sector, is to treat Mitsubishi Estate, Mitsui Fudosan and Sumitomo Realty as essentially the same company in three different liveries. That is wrong. The three differ on three dimensions that matter — geography, segment mix, and balance-sheet posture — and Sumitomo Realty sits at the corner of all three.

| Dimension | Mitsubishi Estate (8802) | Mitsui Fudosan (8801) | Sumitomo Realty (8830) |

|---|---|---|---|

| Core district | Marunouchi, Otemachi | Nihonbashi, Hibiya, Toyosu | Shinjuku, Shintora-dori, Roppongi |

| Revenue weighting | Office leasing dominant | Mixed-use (office + retail + logistics + hotels) | Office leasing + heavy condominium sales |

| Condominium presence | Modest, premium-only | Substantial, “Park” brands | Largest of the three; “City Tower” / “Grand Hills” |

| Balance-sheet posture | Conservative | Moderate | Most leveraged of the three |

| Renovation arm | Limited | Reform business via group | Sumitomo Realty New Stage (large) |

| Overseas exposure | Meaningful (London, US) | Meaningful (US, ASEAN) | Historically domestic |

Read across that table and Sumitomo Realty’s distinctive profile emerges. It is the most exposed of the three to the residential cycle, because condominium sales — under the “City Tower” tower-condominium brand and the lower-rise “Grand Hills” line — make up a far larger share of revenue than at either rival. It is the most balance-sheet-aggressive, willing to carry net debt at multiples of equity that Mitsubishi Estate’s CFO would find uncomfortable. And it is the most domestically concentrated, with overseas development a marginal line rather than a stated strategic pillar.

None of those choices are accidents. They reflect a company that, lacking an inherited prime district, chose to build volume and turnover rather than rely on the gentle compounding of Marunouchi-style ground rents.

The Shinjuku tower portfolio

Shinjuku is to Sumitomo Realty what Marunouchi is to Mitsubishi Estate: not merely an address but a thesis. The company’s anchor tenancy in the district begins with the 1974 Shinjuku Sumitomo Building — recently renovated, with its base re-engineered into the covered “Sankaku Hiroba” event atrium — and extends through a series of subsequent towers built or acquired over the following four decades.

The neighbouring Shinjuku NS Building, completed in 1982, gave the company a second high-rise anchor with a distinctive hollow-core atrium and a tenant mix tilted towards technology and back-office functions. Shinjuku Front Tower, completed in 2011 on the north side of the station, added Grade-A office space at a moment when supply elsewhere in central Tokyo was tightening. Shinjuku Garden Tower, completed in 2017 in the Higashi-Shinjuku district, extended the cluster eastward and combined office floors with a hotel and serviced-apartment block.

The strategic point is not that Sumitomo Realty owns Shinjuku — it does not; JR East, Odakyu, Keio, Takashimaya and a host of smaller landlords also matter — but that within the western office sub-market, Sumitomo Realty’s footprint is large enough to function as a price-setter for the kind of mid-cycle Grade-A floors that multinational tenants typically lease. For a foreign company relocating its Japan headquarters out of the saturated Marunouchi cluster, Shinjuku is now a credible alternative principally because Sumitomo Realty made it one.

Shintora-dori and the Toranomon push

If Shinjuku is the legacy bet, the Shintora-dori (新虎通り) corridor — the broad boulevard cut through the Toranomon-Shimbashi district as part of pre-2020 Olympic redevelopment — is the next-generation one. Sumitomo Realty has positioned itself as one of the most active developers along the corridor, with the Tokyo Toranomon Tower complex and a sequence of mid-rise office and residential buildings that together knit the district into a continuous business address running from Kasumigaseki down to the Hamamatsucho waterfront.

This matters strategically because Toranomon-Shimbashi is, in effect, central Tokyo’s last large-scale greenfield opportunity. Mori Building has the southern end with Toranomon Hills. Mitsui Fudosan has its own Toranomon projects. Sumitomo Realty is the third major developer in the corridor — and for foreign tenants who want a central Tokyo address without the queueing premium of Marunouchi, the Shintora-dori cluster has become the realistic shortlist.

Condominium sales: the “City Tower” engine

What truly distinguishes Sumitomo Realty from its rivals is the scale of its for-sale residential business. The company is, by units sold, consistently among the largest condominium developers in Japan, and its two flagship brands — “City Tower” for high-rise tower condominiums and “Grand Hills” for lower-rise premium projects — have come to define a generation of Tokyo upper-middle-class housing.

The condominium model is fundamentally different from office leasing in cash-flow terms. Office leasing produces decades of stable, low-yielding rents against very long-lived assets. Condominium development produces a lumpy sale on completion, recycles capital quickly, and exposes the developer to the precise moment of buyer sentiment when each project reaches occupancy. Sumitomo Realty has chosen to carry that exposure at scale — which is the proximate reason its leverage runs higher than its rivals. The implicit bet is that Japan’s metropolitan housing market, particularly the supply-constrained tower-condominium segment in central Tokyo, Yokohama and a handful of other gateway cities, will continue to clear at premium prices for the foreseeable cycle.

For foreign observers, this matters in two ways. First, the company’s reported earnings are more cyclical than a pure office REIT-style story would suggest. Second, the “City Tower” brand is one of the most visible touch-points through which expatriate executives encounter Japanese property at all — many of the central Tokyo tower condominiums marketed to international buyers and serviced-apartment operators are Sumitomo Realty assets.

Sumitomo Real Estate New Stage and the renovation flywheel

The third leg of the stool — and the one most easily missed by foreign analysts focused on the headline office and condominium businesses — is the residential renovation arm, Sumitomo Real Estate New Stage Co., Ltd. (住友不動産ニューステージ). The reform business takes existing single-family homes and condominium units across Japan and re-engineers them, often with significant structural work, into modernised stock that can be re-sold or re-occupied.

The renovation arm is interesting for two reasons. Operationally, it gives Sumitomo Realty exposure to Japan’s vast stock of ageing post-1980s housing — a market that demography all but guarantees will grow as households inherit and dispose of family homes. Strategically, it provides a counter-cyclical buffer: when new-build condominium sales slow, renovation demand tends not to slow in the same way, because it serves a different customer (often older households rationalising existing assets rather than first-time buyers).

The leveraged balance sheet: what foreign lenders should know

The phrase “most leveraged of the big three” is a relative statement, not an absolute warning. Sumitomo Realty’s balance sheet is, by the standards of leveraged property companies globally, prudently managed. Japanese property’s structural tailwinds — extremely low domestic interest rates, dense central-city land scarcity, and a lender base of long-relationship megabanks — make leverage cheaper to carry in Tokyo than in almost any other major property market.

That said, the relativity matters for foreign credit analysts. Sumitomo Realty’s debt-to-equity ratio runs meaningfully above Mitsubishi Estate’s and above Mitsui Fudosan’s, and the company’s interest-rate sensitivity is correspondingly higher. The Bank of Japan’s gradual exit from yield-curve control over 2024-25 has shifted the underlying funding curve upwards in ways that will, over the medium term, compress margins more visibly at Sumitomo Realty than at its less-leveraged peers. None of this is news to the company’s CFO; the response has been a measured deleveraging programme funded partly through asset disposals and partly through the natural cash recycling of condominium completions. But foreign lenders weighing exposure to the company — whether through senior loans, syndicated facilities or J-REIT-adjacent equity — should price the rate sensitivity explicitly rather than assume it mirrors Mitsubishi Estate’s.

Sustainability and the net-zero pivot

Sumitomo Realty has committed to net-zero greenhouse-gas emissions across its portfolio by 2050, in line with the broader Japanese corporate consensus, with interim milestones for both new construction and existing-asset retrofits. The challenge is concentrated in the legacy 1970s and 1980s towers — Shinjuku Sumitomo Building and NS Building among them — where the embodied energy of the structure means meaningful emissions reductions depend on operational decarbonisation rather than rebuilding. The renovation arm’s institutional capability becomes relevant here too: the same teams that re-engineer single-family homes also serve as in-house expertise for retrofitting office tower interiors at scale.

What foreign counterparties should understand

For three categories of foreign reader, the practical takeaways from Sumitomo Realty’s profile differ.

Foreign tenants evaluating a Tokyo office should treat Sumitomo Realty’s Shinjuku and Shintora-dori portfolios as a genuinely competitive alternative to Marunouchi and Nihonbashi — particularly for occupiers who value floor-plate efficiency over postcode prestige, and for whom proximity to Shinjuku Station’s transport interchange is a logistics advantage. The leasing relationship will be transactional in a way that Mitsubishi Estate’s most premium Marunouchi addresses sometimes are not.

Foreign lenders should read the leverage profile carefully and not assume the three big-three names are equally rate-insensitive. The medium-term BOJ normalisation path matters more here than at Mitsubishi Estate. That said, the underlying collateral quality — central-Tokyo Grade-A offices and tower condominiums — is among the highest in the listed-property universe globally.

Foreign equity investors should understand they are buying a hybrid: part long-duration office landlord, part cyclical condominium developer, part renovation services business. The valuation multiple the market applies to Sumitomo Realty has historically traded at a discount to Mitsubishi Estate precisely because of that hybrid character. Whether the discount is too wide is a judgement call about Japanese housing demand, BOJ rates, and the durability of the Shinjuku office cluster — none of which the company controls, but all of which it has positioned itself to benefit from if they move favourably.

FAQ

Is Sumitomo Realty part of the same group as Sumitomo Corporation or SMFG?

They share the historical Sumitomo name and family lineage but are independent listed companies with separate management, boards and shareholder bases. Sumitomo Corporation (8053) is the trading house; SMFG / Sumitomo Mitsui Financial Group is the banking group; Sumitomo Mitsui Trust is the trust bank; Sumitomo Chemical, Sumitomo Electric and Sumitomo Heavy are separately listed industrial companies. Sumitomo Realty (8830) is the property arm. Cross-shareholdings exist but are not strategic control stakes.

How does Sumitomo Realty compare in size to Mitsubishi Estate and Mitsui Fudosan?

By market capitalisation, Sumitomo Realty is the third-largest of Japan’s listed property developers, behind Mitsubishi Estate and Mitsui Fudosan but ahead of every other listed peer. By unit volume of condominium sales, however, it is consistently among the very largest in the country.

What are the City Tower and Grand Hills brands?

“City Tower” (シティタワー) is Sumitomo Realty’s flagship high-rise tower-condominium brand, deployed across central Tokyo, Yokohama, Osaka and other gateway markets. “Grand Hills” (グランドヒルズ) is the lower-rise premium-residential line, typically deployed in established residential districts where tower zoning is unavailable.

Where is the company headquartered?

At the Shinjuku Sumitomo Building (新宿住友ビル) in Nishi-Shinjuku, the company’s flagship 210-metre tower completed in 1974 and renovated in recent years to add the Sankaku Hiroba covered event atrium at its base.

What is Sumitomo Real Estate New Stage?

It is the group’s housing-renovation arm — taking existing single-family homes and condominium units across Japan and re-engineering them, often with structural-level reform, into modernised stock. The business serves Japan’s large existing-housing inventory and provides counter-cyclical revenue against the more volatile new-build condominium cycle.

Working with Sumitomo Realty

For foreign tenants considering a Shinjuku or Shintora-dori office, foreign investors evaluating the Japanese listed property complex, or foreign service providers seeking to engage with Sumitomo Realty’s procurement and operations teams, Japonity’s business matching service can facilitate introductions to the appropriate counterparty within the group. We also profile other anchors of Japan’s property and infrastructure landscape across the Tech, Companies and Insights categories — read alongside our coverage of Mitsubishi Estate, Mitsui Fudosan and the broader Japanese real-estate oligopoly.

Related from Japonity — Japan’s real estate giants

- Mitsubishi Estate — The Marunouchi landlord — ~30 buildings in Tokyo’s prime district

- Mitsui Fudosan — The aggressive developer — Mid-Town, LaLaport, 50 Hudson Yards

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →