Sixteen years after Nomura Holdings bought Lehman Brothers’ Asia-Pacific and European operations over a frantic September 2008 weekend for approximately $225 million, the deal still defines what Nomura is — and what it is not. The Archegos collapse in March 2021 cost the firm approximately $2-3 billion in a single quarter and forced a hard reassessment of its US prime brokerage ambitions. The slow, public retreat from US cash equities trading and parts of EMEA equities followed. Yet for all of that mess, Nomura remains the only Japanese-headquartered investment bank with a serious global footprint, the only one that foreign acquirers and fund sponsors can credibly treat as a peer rather than a domestic distribution channel, and the only one whose Tokyo trading floor and London origination desk speak in the same compensation grammar as Goldman or Morgan Stanley.

An Osaka brokerage that became Japan’s bank to the world

Nomura Securities was founded in Osaka in 1925 by Tokushichi Nomura II, the son of a money changer who had already built a thriving securities business inside Osaka Nomura Bank. The new firm was, from the start, a securities house in the Anglo-American sense rather than a universal bank in the German sense — a deliberate choice that shaped the next century. By the late 1930s Nomura was already managing investment trusts; by the 1960s it was the dominant force in Japan’s retail brokerage market; by the late 1980s, at the peak of the bubble, it was, by some measures, the most profitable financial institution in the world.

The structure that exists today — Nomura Holdings, Inc., listed on the Tokyo and New York Stock Exchanges, with Nomura Securities Co., Ltd. as its principal Japanese operating subsidiary — was formalised in 2001 with the move to a holding company model. The headquarters at Otemachi, Tokyo, sits in the financial district alongside the megabanks and the central bank. The firm employs roughly 25,000 to 27,000 people globally across more than thirty countries. Its three reportable business segments — Retail, Investment Management, and Wholesale — capture three very different businesses pretending to be one company, and the tension between them is the story of modern Nomura.

The Lehman weekend, and what Nomura actually bought

The mechanics of the September 2008 transaction are worth recalling, because they explain why Nomura’s global identity has been so difficult to either consolidate or abandon. When Lehman Brothers filed for Chapter 11 on 15 September 2008, the firm’s North American operations were swept up by Barclays in a separate deal. Nomura, moving with unusual speed for a Japanese institution, signed term sheets within days for Lehman’s Asia-Pacific franchise (approximately 3,000 staff, including Lehman’s strong India and Hong Kong M&A teams) and, shortly after, for Lehman’s European and Middle Eastern equities and investment banking businesses (a further roughly 2,500 staff).

The headline cash price was modest — public reporting placed it at approximately $225 million in total — but the real cost was the retention package Nomura committed to in order to keep the Lehman talent in place. Two-year guaranteed bonuses, in some cases pegged to 2007 Lehman compensation levels, ran into the billions of dollars and embedded a compensation culture inside Nomura that the firm had never operated before. The strategic logic was clear: Nomura had spent two decades trying to build a global investment bank organically and had not succeeded. Buying Lehman’s non-US franchise at distress prices was the only realistic shortcut. The execution risk was equally clear: a Japanese house with a deeply Japanese management culture had just acquired several thousand of the most expensive bankers in the world, with no integration playbook.

The segment mix, sixteen years later

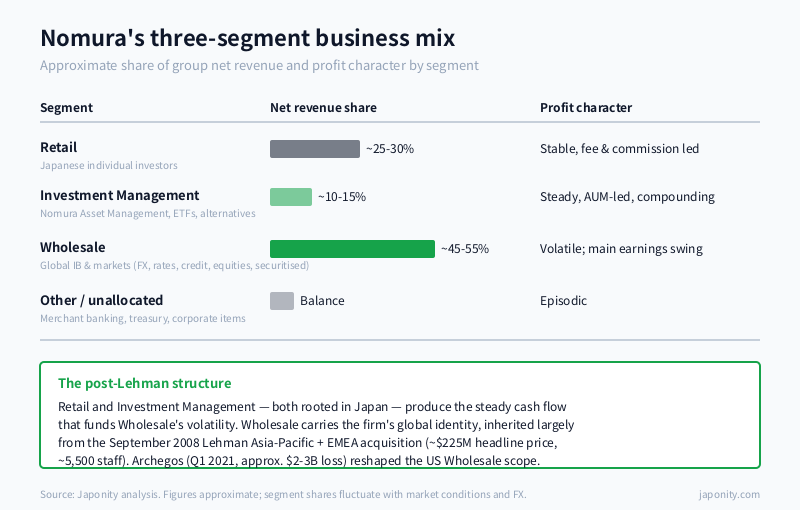

The Lehman deal is now visible in Nomura’s segment structure mostly through the Wholesale division — investment banking and global markets — which is where the firm competes, or chooses not to compete, with the bulge bracket. Retail and Investment Management, by contrast, are essentially domestic Japanese businesses with overseas extensions. The rough shape of the consolidated business looks like this:

| Segment | What it does | Approx. share of group net revenue | Profit character |

|---|---|---|---|

| Retail | Japanese individual investors, branch-based brokerage and wealth advice | ~25-30% | Reasonably stable, fee and commission led |

| Investment Management | Nomura Asset Management and adjacent businesses, public and private funds | ~10-15% | Steady, scale-sensitive, AUM-led |

| Wholesale | Global investment banking, global markets (FX, rates, credit, equities, securitised products) | ~45-55% | Volatile; the main earnings swing factor |

| Other / unallocated | Merchant banking, treasury, corporate items | Balance | Episodic |

Segment economics fluctuate sharply with market conditions, the yen, and one-off items, but the structural pattern has been consistent for most of the post-Lehman era: Retail and Investment Management produce the steady cash flow that funds Wholesale’s volatility, and Wholesale produces the bulk of the upside in good years and the bulk of the disappointments in bad ones. The Archegos loss in early 2021 was the most dramatic illustration, but it was not the first quarterly write-down nor the last.

Retail: the part of Nomura that is unambiguously Japanese

Nomura’s domestic retail business is the largest of its kind in Japan, with several hundred branches and a sales force whose tenure averages substantially longer than at any of its global competitors. The customer base skews older and wealthier than the Japanese average, reflecting both the firm’s brand premium and the fact that Japan’s household financial assets — approximately 2,100 trillion yen in aggregate — sit disproportionately with households over the age of sixty.

The unit economics here are very different from Wholesale. Average ticket sizes are larger than at the online brokers (Rakuten Securities, SBI Securities, Monex) but the customer is paying for advice and access to primary issuance, including IPO allocations and structured products distributed under Nomura’s underwriting franchise. Margins are reasonable but the growth story is constrained: Japan’s NISA (tax-advantaged retail investment) regime expanded materially in 2024, which is a tailwind, but the demographic backdrop remains a structural headwind. Retail is the segment that anchors the firm’s domestic reputation and provides the captive distribution channel that makes Nomura’s equity capital markets franchise viable for Japanese corporates. It is also the segment that overseas investors most often underweight in their mental model of the firm.

Investment Management: the franchise that quietly compounds

Nomura Asset Management is one of Japan’s largest asset managers by AUM, with significant ETF presence (the NEXT FUNDS series is a fixture of the Tokyo Stock Exchange ETF market) and a growing alternatives and private markets capability. The Investment Management segment also houses Nomura’s stakes in adjacent vehicles, including investments in American Century Investments (the US asset manager in which Nomura took a strategic minority position in 2016) and selective private equity exposures.

This segment is the firm’s most underrated. It is small relative to Wholesale in revenue terms but contributes a disproportionate share of stable, fee-based earnings. The strategic question for overseas counterparties is whether Nomura can use Investment Management as the lever to deepen its non-Japanese institutional client relationships in ways that Wholesale, with its lumpier deal-by-deal economics, cannot. The 2024-2025 expansion of private markets and alternatives capacity — including the Q1 2024 acquisition of Australia’s NB Capital business and selective hires in private credit — suggests the firm has been working on this thesis.

Wholesale: where the global identity is contested

Nomura’s Wholesale division is what most readers of the financial press picture when they think about the firm: trading floors in Tokyo, London, Hong Kong, Singapore, and New York; M&A bankers in Mumbai and Frankfurt; rates and FX desks competing against the bulge bracket on flow. This is the part of Nomura that absorbed the Lehman acquisition, and it is also the part of the business that has been most extensively reshaped in the last five years.

The most consequential changes have come in the US. After the Archegos loss in March 2021, Nomura America re-scoped its prime brokerage and equities trading ambitions, exited substantial parts of US cash equities execution, and refocused on fixed income, securitised products, and selective investment banking. The securitised products desk — which Nomura had quietly rebuilt into one of the strongest non-bulge-bracket franchises in the US — became, in effect, the spine of the US operation. Meanwhile, Japanese equities, Asian credit, EMEA rates, and global FX continued to operate at competitive scale.

The honest characterisation is that Nomura is no longer trying to be a full-service global investment bank in the bulge-bracket sense. It is trying to be a globally credible Japanese investment bank with deep, defensible positions in specific products and geographies. That is a narrower ambition than the post-Lehman strategy of 2009-2015, but it is also a more honest one, and the financial results since 2022 have been materially better than the noisy decade that preceded it.

The Okuda restructuring and what it changed

Kentaro Okuda became President and Group CEO in April 2020, succeeding Koji Nagai. Okuda’s background is investment banking — he ran the Wholesale division and held senior roles in the US business — and his restructuring agenda has been correspondingly weighted toward Wholesale rationalisation. The post-Archegos cuts to US equities, the renewed focus on private markets and alternatives, the strengthening of cross-border M&A advisory (where Nomura has retained a strong franchise inherited partly from the Lehman Asia business), and the gradual pivot of Investment Management toward non-Japanese AUM growth are all Okuda-era moves.

What Okuda has not done is abandon the global model. There has been speculation in the financial press, at various points since 2012, that Nomura should retreat to a regional Asia-Pacific identity and exit EMEA and the Americas entirely. That has not happened, and under Okuda the signal has been that it will not happen. Nomura’s identity as the only global Japanese investment bank — useful to Japanese corporates doing outbound M&A, useful to overseas investors accessing Japanese equity and credit markets, useful to global allocators benchmarking against bulge-bracket research — is something the firm regards as a strategic asset worth defending, even at the cost of accepting lower group ROE than a domestic-only model would deliver.

Nomura versus Daiwa, and why the gap matters

Nomura’s closest domestic peer is Daiwa Securities Group, the other surviving member of what was once Japan’s “Big Four” securities houses (Nomura, Daiwa, Nikko, and Yamaichi; Yamaichi collapsed in 1997, and Nikko was absorbed into the SMBC group as SMBC Nikko Securities). Daiwa runs a serious investment banking and asset management franchise and competes hard with Nomura in Japanese ECM and DCM league tables. But Daiwa’s overseas footprint is meaningfully thinner than Nomura’s, and the firm has never made an acquisition on the scale of the Lehman deal.

SMBC Nikko Securities, embedded inside the SMBC megabank group, is structurally a different business: it leverages the parent bank’s corporate relationships for deal flow but does not pursue independent global investment banking ambitions in the way Nomura does. Mizuho Securities and MUFG Morgan Stanley Securities — the latter a joint venture born from the 2008 capital injection into Morgan Stanley — fill similar bank-affiliated roles in their respective groups.

The result is that, in 2026, Nomura is the only Japanese securities house with a global investment banking franchise that is structurally independent of a megabank parent. For overseas counterparties, this matters: a deal mandate at Nomura is not implicitly tied to a lending commitment from a parent bank, and the firm’s research, trading, and advisory businesses do not carry the conflict-of-interest overhead that affects bank-affiliated competitors.

Where Nomura stands in 2026

Two things overseas firms tend to underestimate. The first is the depth of Nomura’s domestic distribution: the firm is the most credible underwriting partner in Japan for foreign issuers seeking institutional or retail demand, whether through equity offerings, Samurai bonds, or structured products, and the retail branch network frequently dismissed in the international press as a legacy cost is in fact a moat that no foreign firm can replicate. The second is the cross-border M&A franchise: the investment banking division, with Lehman-era European and Asian teams now fully integrated, runs one of the strongest non-bulge-bracket cross-border M&A practices, particularly on Japan-outbound and Asia-Europe transactions, and remains selective about mandates in favour of strategically significant deals.

The cleanest way to read Nomura today is to refuse two opposite caricatures. It is not a Japanese securities house with overpriced ambitions in markets it cannot win. It is also not a credible bulge-bracket competitor in US equities. It is, instead, a hybrid: a globally credible Japanese investment bank with a Tokyo retail and asset management base that funds selective Wholesale exposures in product categories where it can compete — Japanese equities, Asian credit, US securitised products, cross-border M&A, global FX and rates — and a willingness to step back from categories where it cannot. Whether that identity is durable depends on whether Investment Management can grow non-Japanese AUM faster than Retail’s demographic headwind shrinks the domestic base, and whether the next CEO transition preserves the global commitment without repeating the post-Lehman integration cost overruns. Each question is open. None has an obvious negative answer.

FAQ

Who owns Nomura Holdings?

Nomura Holdings, Inc. is a publicly listed company on the Tokyo Stock Exchange (ticker 8604) and the New York Stock Exchange (NMR). There is no controlling shareholder. The largest holders are typically Japanese trust banks acting on behalf of institutional clients, alongside global asset managers and a base of long-tenured Japanese retail investors. The founding Nomura family exited its equity position decades ago and is no longer involved in governance.

How much did Nomura actually pay for Lehman’s non-US operations?

Public reporting placed the headline cash price at approximately $225 million for the combined Asia-Pacific and European/Middle Eastern Lehman operations in September 2008. The real cost was substantially higher once two-year guaranteed retention packages for Lehman bankers were included; total compensation commitments in the immediate post-deal period ran into the billions of dollars. The deal added roughly 5,500 staff across the two transactions.

What happened with Archegos, and how exposed is Nomura today?

In March 2021, the collapse of Archegos Capital Management, a family office that had built large and highly leveraged equity positions through total return swaps with multiple prime brokers, caused Nomura to record a loss of approximately $2-3 billion in the first quarter of fiscal 2021. The firm subsequently rescoped its US prime brokerage and cash equities businesses, exited substantial parts of US equities execution, and tightened risk controls. Nomura’s current US Wholesale business is materially smaller and more focused on fixed income and securitised products than it was pre-Archegos.

How does Nomura differ from Daiwa and SMBC Nikko?

Daiwa Securities Group is Nomura’s closest domestic peer in retail brokerage and Japanese investment banking, but Daiwa’s overseas presence is meaningfully thinner. SMBC Nikko Securities operates as the securities arm of the SMBC megabank group; its business model relies on the parent bank’s corporate relationships and it does not pursue independent global investment banking. Mizuho Securities and MUFG Morgan Stanley Securities are similarly bank-affiliated. Nomura is the only Japanese securities house that operates a structurally independent global investment bank without a megabank parent.

Is Nomura a credible counterparty for cross-border M&A?

Yes, particularly for transactions involving Japanese parties on either side. Nomura’s investment banking division retained much of the Lehman-era European and Asian advisory talent and has built one of the strongest non-bulge-bracket cross-border M&A franchises, especially on Japan-outbound deals into the US, Europe, and Asia. The firm is selective about mandates and prefers strategically significant transactions over volume, but for mid-market and large-cap deals with Japanese counterparty involvement it is frequently the most knowledgeable advisor available.

Working with Nomura

For overseas corporates, financial sponsors, and asset managers, the practical entry points to Nomura are diverse: cross-border M&A advisory, Japanese equity and debt capital markets access, Samurai bond underwriting, Japanese institutional and retail distribution for offshore funds, securitised product structuring in the US, and Asian credit and equity research access. Each of these is a distinct franchise inside the firm, with its own senior contacts, and a credible first conversation typically starts with the right product specialist rather than with corporate development.

Beyond Nomura itself, the broader ecosystem of Japanese securities houses — Daiwa, SMBC Nikko, Mizuho Securities, MUFG Morgan Stanley Securities, and a long tail of regional and specialised brokers — is a substantial market for foreign data, technology, research, and execution providers. Many of these firms operate outside the Anglophone industry press and are not easy to reach cold.

If your firm is exploring a cross-border M&A mandate involving a Japanese counterparty, a Samurai or Pro-Bond issuance, a Japanese distribution partnership for an offshore fund, or a technology, data, or research relationship with a Japanese securities house — Japonity’s business matching service can help structure a credible first conversation with the right team in Tokyo.

Related from Japonity — Japan’s megabanks & securities

- MUFG — Japan’s #1 megabank and its Morgan Stanley stake

- Sumitomo Mitsui FG (SMFG) — Japan’s #2 megabank and the Jefferies alliance

- Mizuho Financial Group — Japan’s #3 megabank — Greenhill + Rakuten Securities second act

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →