In the early hours of October 13, 2008, as Morgan Stanley’s share price was in free-fall and the U.S. Treasury was bracing for a second Lehman, a $9 billion wire transfer landed from Tokyo. The buyer was Mitsubishi UFJ Financial Group, Japan’s largest bank — and the cheque, famously cut as a literal physical instrument because the U.S. interbank system was closed for Columbus Day, bought a roughly 21% stake in Morgan Stanley at the bottom of the financial crisis. Eighteen years later, that stake is worth a multiple of the original investment, has thrown off billions in dividends, and underwrites one of the most consequential corporate alliances in global finance. The deal is also the lens through which to understand modern MUFG: a roughly ¥400 trillion balance sheet, the largest U.S. dollar-funded Japanese institution, and the default counterparty for foreign capital entering — or exiting — Japan.

The bank that absorbed Japan

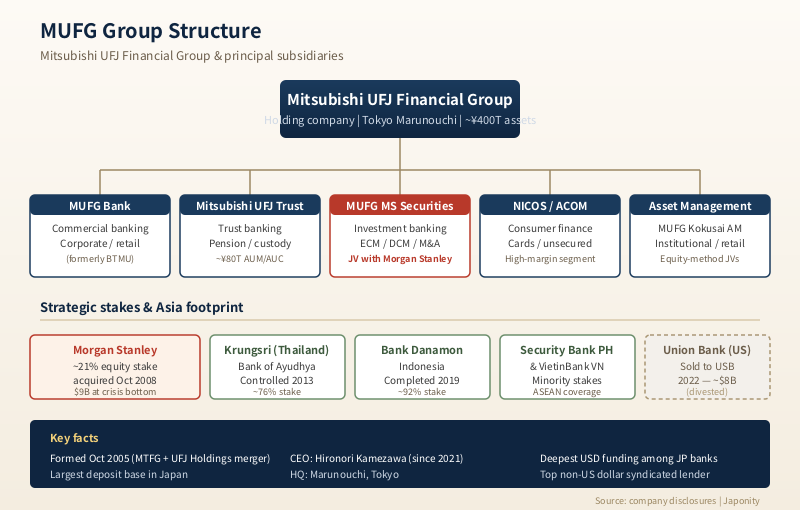

Mitsubishi UFJ Financial Group, known universally as MUFG, was formed in October 2005 from the merger of Mitsubishi Tokyo Financial Group and UFJ Holdings. At the time it created the world’s largest bank by deposits, and the deal capped a decade of forced consolidation following Japan’s banking crisis of the late 1990s. What had been roughly a dozen city banks, trust banks and long-term credit banks collapsed into three megabank groups: MUFG, Sumitomo Mitsui Financial Group (SMFG) and Mizuho Financial Group. MUFG inherited the Mitsubishi keiretsu’s blue-chip corporate book, UFJ’s Kansai and SME exposure, and a trust banking franchise that would later anchor its asset management ambitions.

The group’s principal entities map onto Japan’s segmented financial regulation. MUFG Bank — renamed in 2018 from The Bank of Tokyo-Mitsubishi UFJ — is the commercial banking arm and the entity foreign treasurers actually transact with. Mitsubishi UFJ Trust and Banking Corporation is the trust bank, handling pension administration, real estate trusts and roughly ¥80 trillion in assets under custody and management. Mitsubishi UFJ Morgan Stanley Securities, a joint venture established in 2010 as the operational embodiment of the 2008 alliance, is the domestic investment banking and brokerage arm. Mitsubishi UFJ NICOS handles consumer credit; ACOM, partially owned, anchors consumer finance. Mitsubishi UFJ Kokusai Asset Management and the AM businesses inside the trust bank run the asset management franchise.

This is not a holding-company veneer over a single bank. Each subsidiary has its own license, its own regulator, and — critically for foreign counterparties — its own approval workflow. Routing a yen syndicated loan, a JGB repo, and a J-REIT custody mandate to “MUFG” in practice means engaging three different legal entities with three different relationship teams.

The Morgan Stanley trade, in slow motion

The October 2008 investment is now studied in business schools as a case in counter-cyclical capital allocation, but at the time it was a near-run thing. MUFG converted preferred shares into common equity in 2009, lifting its stake to roughly 22%, and has held it broadly steady since. The arithmetic has been extraordinary: $9 billion deployed at a depressed valuation against a U.S. bulge-bracket franchise that has since tripled in earnings power, with cumulative dividends well into the billions. More important than the mark-to-market, however, is the strategic option value it conferred.

The alliance produced two operating joint ventures in Japan. Mitsubishi UFJ Morgan Stanley Securities handles institutional equities, debt capital markets and M&A advisory for large corporate clients. Morgan Stanley MUFG Securities, the smaller of the two, focuses on fixed income, currencies and commodities for non-Japanese institutional clients. The split was designed to avoid the JV becoming a captive distribution channel — Morgan Stanley keeps its global flow business, MUFG keeps its corporate relationships, and Japan gets a hybrid franchise that punches above either parent’s domestic weight. In league tables, the JV consistently sits in the top three for Japan-related ECM and M&A.

The less appreciated benefit is funding. MUFG is the largest dollar-funded Japanese institution, and the Morgan Stanley relationship gives it preferential access to U.S. capital markets, repo facilities and dealer balance sheets at moments when cross-currency basis swaps widen. In the March 2020 dollar shortage, MUFG’s USD funding costs moved materially less than Japanese peers without comparable U.S. relationships.

How the three megabanks actually differ

For foreign capital, the practical question is not whether to bank with a Japanese megabank but which one. The three are often treated as interchangeable; they are not. Each has a different gravitational centre, balance sheet shape and risk appetite, and these differences matter when negotiating a credit facility, mandating an underwriter or selecting a custodian.

| Dimension | MUFG | SMFG | Mizuho |

|---|---|---|---|

| Total assets (approx.) | ¥400+ trillion | ¥280 trillion | ¥260 trillion |

| Heritage keiretsu | Mitsubishi (incl. UFJ / Tokai) | Sumitomo + Mitsui | Fuyo + Dai-Ichi Kangyo + IBJ |

| Foreign business strength | Strongest USD funding; Asia retail (Krungsri, Danamon) | Aircraft leasing; project finance; U.S. consumer (Jenius) | U.S. DCM franchise; European corporate |

| Securities arm | JV with Morgan Stanley | SMBC Nikko (wholly owned) | Mizuho Securities (wholly owned) |

| Trust banking | Mitsubishi UFJ Trust (largest) | SMBC Trust (smaller) | Mizuho Trust (mid-size) |

| Reputation with foreign issuers | Conservative, blue-chip corporate | Aggressive, deal-hungry | Process-heavy, broad coverage |

MUFG’s signature is scale and conservatism: the largest deposit base, the deepest dollar funding, the most institutional trust franchise. SMFG, the offspring of two trading houses, is the most commercially aggressive and the leader in non-bank businesses such as aircraft leasing (SMBC Aviation Capital) and consumer finance (SMBC Consumer Finance, formerly Promise). Mizuho, the product of a three-way merger of Fuyo, Dai-Ichi Kangyo and the Industrial Bank of Japan, has the broadest corporate coverage but has historically been the most operationally troubled, with several high-profile IT outages.

Segment mix: where the profits actually come from

MUFG’s external image is that of a Japanese commercial bank, but the segment disclosures tell a more interesting story. Domestic banking — the famously low-margin business of lending Japanese deposits to Japanese borrowers at sub-1% spreads — accounts for less than a third of consolidated profit before tax. The largest single contributor is the global commercial banking and global corporate & investment banking segment, which includes overseas lending, trade finance, and the project finance book that has made MUFG one of the world’s largest non-Chinese cross-border lenders.

The trust bank contributes a steady stream of fee income — pension administration, real estate trusts, stock transfer agency services — that is largely insensitive to interest rate cycles. The asset management business, which combines the trust bank’s institutional franchise with Mitsubishi UFJ Kokusai’s retail mutual funds, runs roughly ¥80 trillion in AUM. Consumer finance, through NICOS and ACOM, is the highest-margin business but also the most cyclical and the most exposed to regulatory tightening around interest-rate caps.

The equity contribution from Morgan Stanley, accounted for under the equity method, is a separately disclosed line and has averaged several hundred billion yen annually — a single non-Japanese investment now generates a meaningful share of group profit and effectively diversifies MUFG away from pure JGB-curve sensitivity.

The Asia footprint that nobody noticed being built

While Western financial journalists were fixated on the Morgan Stanley deal, MUFG quietly assembled what is now the largest commercial banking footprint in Southeast Asia held by any non-ASEAN institution. The two anchor acquisitions are Bank Danamon Indonesia, of which MUFG holds approximately 92% after a multi-year accumulation completed in 2019, and Bank of Ayudhya (Krungsri) in Thailand, controlled since 2013. The group also holds significant stakes in Security Bank in the Philippines and VietinBank in Vietnam, and runs full-service branches across the rest of the region.

The strategic logic is demographic. Japan’s deposit base is enormous but its loan demand is structurally weak; ASEAN economies have the opposite problem — credit-hungry borrowers and a less developed local deposit base. MUFG channels Japanese yen funding through swap markets into local-currency lending in Bangkok, Jakarta and Manila, capturing a wider net interest margin than any domestic Japanese deployment could produce. The same logic explains the 2022 sale of Union Bank — a California commercial bank acquired in the 1980s — to U.S. Bancorp for approximately $8 billion in cash and stock: U.S. consumer banking offered scale without margin, while ASEAN consumer banking offers margin with scale potential.

BOJ policy normalisation and the great margin question

For most of the past decade, MUFG’s domestic banking business has been an exercise in profitless prosperity: enormous deposit shares accumulating at near-zero rates, deployed into JGBs yielding less than the cost of operations. The Bank of Japan’s gradual exit from yield curve control and negative interest rates, formalised in 2024 and continuing into 2026, has reset the arithmetic.

Every 25-basis-point rise in short-term yen rates flows almost mechanically through MUFG’s net interest margin, because deposit pass-through in Japan is famously sticky — savers do not chase rate, and the regulatory environment discourages aggressive repricing of household deposits. Analysts estimate that a return to a 0.5–1.0% short rate environment, sustained for a year, would add hundreds of billions of yen to MUFG’s pre-provision operating profit, with limited offsetting credit losses given the conservative domestic book.

The risk runs in the other direction too. MUFG holds the largest JGB portfolio of any private institution; mark-to-market losses on the available-for-sale book have already been material as long-end yields have risen. The bank’s response has been to shorten duration aggressively, but the legacy book will take years to roll off. For foreign investors, this is the central macro question on Japanese megabanks: do you own MUFG for the loan-book repricing or do you discount it for the JGB drag? The honest answer is both, in shifting proportions.

What foreign counterparties actually get

For a non-Japanese bank, asset manager or corporate borrower, “working with MUFG” can mean a dozen different things, and getting the entity right is the difference between a smooth execution and a six-month relationship-building exercise. Foreign investment banks typically engage Mitsubishi UFJ Morgan Stanley Securities for joint underwriting on Japan-related transactions, treating it both as a competitor in some mandates and a co-lead in others. Foreign asset managers engage Mitsubishi UFJ Trust for custody, fund administration and pension distribution; the trust bank’s institutional client list reads as a who’s who of global asset managers operating in Japan.

Foreign corporates seeking yen-denominated funding — whether through a Samurai bond, a syndicated loan, or a bilateral facility — typically deal with MUFG Bank’s global corporate banking division. The bank is the largest single source of dollar trade finance to Asian importers, and the largest non-U.S. participant in U.S. syndicated lending; foreign corporates often encounter MUFG first as an agent or co-lead on a U.S. facility before they realise they are dealing with a Japanese institution. For foreign private equity sponsors, the relevant entity is typically MUFG Bank’s leveraged finance team in Tokyo, increasingly partnered with the Morgan Stanley JV for sponsor coverage.

The institutional culture, briefly

MUFG remains, culturally, the most conservative of the three megabanks. The Mitsubishi heritage matters: decision-making is consensus-driven, the corporate culture privileges long-term client relationships over transactional pricing, and the bank’s risk appetite is calibrated to outlast cycles rather than win league tables. Hironori Kamezawa, who took over as CEO in 2021 with a background in risk management and digital strategy, has accelerated cost discipline and pushed digital transformation — including a multi-year investment in cloud migration and a digital-only banking initiative — without departing from the conservative institutional template.

For foreign counterparties, this culture is both a feature and a friction. The feature: MUFG honours commitments, holds the line on covenants only when warranted, and behaves consistently across cycles. The friction: decisions take longer than at a U.S. or European bulge-bracket competitor, internal credit approval requires more documentation, and the relationship has to be earned over multiple transactions rather than priced on a single mandate. Foreign firms that treat MUFG as a transactional counterparty rarely get the bank’s best terms; those that invest in the relationship find MUFG to be the most reliable Japanese counterparty available.

FAQ

How is MUFG structured, and which entity should I actually engage?

MUFG is a financial holding company with four principal operating subsidiaries: MUFG Bank (commercial banking), Mitsubishi UFJ Trust and Banking (trust and asset administration), Mitsubishi UFJ Morgan Stanley Securities (the JV for investment banking and brokerage in Japan), and Mitsubishi UFJ NICOS / ACOM (consumer finance). The right entity depends on the product. Lending and FX go through MUFG Bank; custody, pension and J-REIT business go through the trust bank; equity and debt underwriting in Japan go through the Morgan Stanley JV.

What exactly is the Morgan Stanley relationship today?

MUFG holds an equity stake of roughly 21–22% in Morgan Stanley, acquired during the 2008 financial crisis for approximately $9 billion. The stake is accounted for using the equity method, so a proportional share of Morgan Stanley’s earnings flows to MUFG’s income statement. Operationally, the two firms run two joint ventures in Japan — Mitsubishi UFJ Morgan Stanley Securities for the domestic franchise, and Morgan Stanley MUFG Securities for non-Japanese institutional clients — alongside ongoing collaboration in loan-marketing, project finance and corporate advisory globally.

Can MUFG lend in foreign currencies, and at what scale?

Yes. MUFG is one of the largest non-U.S. lenders in the dollar syndicated loan market and a top participant in dollar-denominated trade finance, project finance and aircraft finance. Its U.S. dollar funding base is the largest among Japanese institutions, drawing on a long-standing primary dealer presence, a large commercial paper programme, and the deposit franchise of the former Union Bank (sold to U.S. Bancorp in 2022 but still anchoring funding relationships). For a foreign corporate looking for a multi-currency relationship bank in Asia, MUFG is typically the most fungible counterparty across yen, dollar, baht, rupiah and renminbi.

How does the cross-currency basis swap market affect doing business with MUFG?

The JPY-USD cross-currency basis — the premium that a holder of yen pays to swap into dollars — has structural reasons to remain negative: Japanese institutions are large net buyers of foreign-currency assets and need to hedge them. MUFG sits on both sides of this trade as one of the largest dealers in JPY-USD swaps, which means foreign counterparties get tight pricing on cross-currency hedging but also bear the basis when swapping dollar liabilities into yen. For a U.S. corporate issuing a Samurai bond, MUFG’s swap pricing is often the difference between an attractive all-in cost and an uneconomic one.

How does Bank of Japan policy normalisation affect MUFG’s earnings?

Materially and directly. Roughly half of MUFG’s domestic loan book reprices to short-term yen rates within a year, while household deposit costs reprice very slowly. A sustained 50–100bp rise in short rates is estimated to add several hundred billion yen to net interest income annually, before any offset from credit losses. The other side of the trade is mark-to-market pressure on the JGB and JPY-denominated bond portfolio, which has already produced material unrealised losses on the available-for-sale book. Net of both effects, BOJ normalisation is generally accretive to MUFG’s earnings power, but with a transitional drag from the legacy bond book.

Working with MUFG

For foreign investment banks, asset managers, corporates and private equity sponsors evaluating Japanese counterparties, MUFG is rarely the cheapest option on a single transaction — but it is, by structural design, the most fungible. The combination of the largest yen deposit base, the deepest non-U.S. dollar funding franchise, the Morgan Stanley alliance and an ASEAN footprint nobody else has replicated makes it the default relationship bank for foreign capital entering Japan. The bank’s conservatism is real, but so is its reliability; engaging the right subsidiary, with the right product, on the right time horizon turns the relationship into a multi-decade compounder rather than a single mandate.

Japonity helps overseas firms identify the right Japanese counterparty — banking, trust, securities or asset management — and build the introductions that turn a first meeting into a multi-product relationship. See our Business Matching page for how to start a structured engagement with MUFG and its peers.

Related from Japonity — Japan’s megabanks & securities

- Sumitomo Mitsui FG (SMFG) — Japan’s #2 megabank and the Jefferies alliance

- Mizuho Financial Group — Japan’s #3 megabank — Greenhill + Rakuten Securities second act

- Nomura Holdings — The Lehman buyout, sixteen years later

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →