Rakuten Group is approximately one hundred and ten million Japanese consumers held inside a single membership identifier, a points wallet that quietly clears across e-commerce, banking, brokerage, travel and a mobile network — and a balance sheet that has lost the rough equivalent of a trillion yen building the youngest of those businesses. It is also the only Japanese listed company that has, since 2010, conducted its internal meetings in English. The combination of consumer-finance ambition, telco moonshot, and self-imposed language reform under founder Hiroshi Mikitani makes Rakuten the most interesting — and the most awkwardly understood — Japanese conglomerate of the past decade.

The shape of the company

Rakuten was founded in 1997 in a small Setagaya office under the name MDM (Marketing Design Mall) by Hiroshi Mikitani, a former Industrial Bank of Japan banker and Harvard MBA who had left the bank after the 1995 Kobe earthquake. The first product was Rakuten Ichiba, a hosted-merchant marketplace closer in design to a digital shopping arcade than to Amazon’s first-party fulfilment model: small and mid-sized Japanese retailers, then nearly absent from the internet, paid a monthly fee plus revenue share to operate their own branded storefronts on a shared platform. By the mid-2000s Ichiba had become the largest e-commerce property in Japan; today it hosts in the order of fifty thousand merchants and remains the company’s profit core.

The corporate structure has since expanded into a holdings tree of roughly seventy operating units organised into three reported segments: Internet Services (Ichiba, Travel, Books, Card, advertising), FinTech (Bank, Securities, Insurance, Payment) and Mobile (the consumer carrier plus Rakuten Symphony, the OpenRAN infrastructure-software business). Mikitani still serves as chairman, president and CEO, an unusually consolidated set of titles for a TSE Prime-listed company of this size, and the founding family retains a significant equity stake. Headquarters moved in 2015 from Shinagawa to a purpose-built campus in Futakotamagawa in western Tokyo — a deliberate signal of the company’s identity as a technology firm rather than a traditional Marunouchi-style conglomerate.

The points engine, and why it is the moat

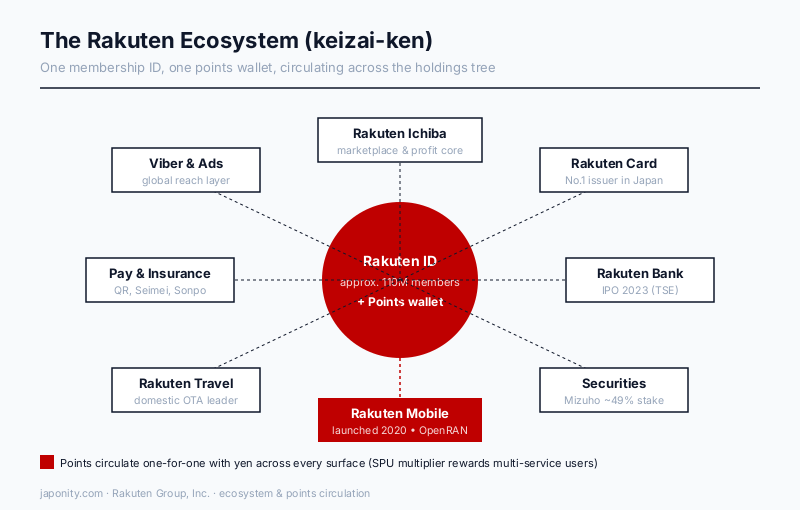

If you ask a Japanese consumer what Rakuten is, the answer is rarely “an e-commerce site.” It is “the points.” The Rakuten Ecosystem — internally referred to as the keizai-ken, or economic sphere — runs on a single membership ID through which Rakuten Points accrue on every transaction across Ichiba, Rakuten Card, Rakuten Bank, Rakuten Securities, Rakuten Travel, Rakuten Mobile, Rakuten Pay, the Seimei and Sonpo insurance subsidiaries, and a long tail of partners ranging from McDonald’s Japan to Daikoku Drug. Points are spendable one-for-one with yen across the entire network, and a multiplier programme (Super Point Up, or SPU) rewards customers who use multiple Rakuten services with progressively higher accrual rates on Ichiba purchases.

The strategic effect is twofold. First, the marginal cost of customer acquisition for any new Rakuten service is close to zero, because the existing membership base — above one hundred million Japanese consumers, with a meaningful fraction in active monthly use — can be cross-sold through the SPU multiplier. Second, the switching cost for a Rakuten customer is materially higher than for an Amazon or Yahoo Japan customer, because leaving Rakuten means leaving points balances, points-earning rates and the bundled discount logic behind. Rakuten’s lead in Japan on this dimension is, for now, unchallenged.

FinTech: a quietly larger business than most outsiders realise

Rakuten Card is the largest credit-card issuer in Japan by number of cards in force and by transaction volume — a position it built within roughly fifteen years by giving away the points-accrual advantage to Ichiba shoppers. Rakuten Bank, listed separately on the Tokyo Stock Exchange in April 2023 (Japan’s largest IPO of that year), is the country’s largest pure-internet bank by deposits and account count, with deeply integrated funnels from Ichiba checkout and the membership identifier. Rakuten Securities is the second-largest online broker in Japan after SBI Securities, with roughly ten million accounts and an outsized share of new NISA (tax-advantaged retail brokerage) sign-ups under the 2024 reform.

FinTech is the unsung profit centre. While Internet Services generates most of the headline revenue, FinTech contributes the bulk of consolidated operating profit, and has done so consistently through the period in which Rakuten Mobile was burning cash on network construction. Securities was the first piece to be partially externalised: Mizuho Financial Group acquired approximately twenty per cent of Rakuten Securities Holdings in 2022 and lifted the stake to roughly forty-nine per cent in 2023, giving Rakuten cash for the mobile build-out while keeping the operating brand under group control. Bank remains majority-owned post-IPO.

The Rakuten Mobile bet, by the numbers

Until 2019, Japan’s mobile market was a near-perfect oligopoly. NTT Docomo, KDDI (au) and SoftBank Mobile shared roughly ninety per cent of consumer subscribers between them, sustained ARPU above the OECD median, and faced regulatory pressure from successive Suga-era cabinets to cut prices. Mikitani’s response was to apply for a full fourth-carrier licence using spectrum allocated to new entrants in 2018, and to build the network from scratch on a cloud-native, vendor-disaggregated, OpenRAN architecture — a design philosophy that, on paper, lets the operator buy radio hardware from one vendor, baseband software from another, and orchestration from a third, with each layer running on commodity x86 servers rather than purpose-built telco appliances.

| Carrier | Approximate subscriber share (2024) | Architecture | Operating margin posture |

|---|---|---|---|

| NTT Docomo | ~35 per cent | Legacy 4G/5G, vendor-stack | Mature, profitable |

| KDDI (au, UQ, povo) | ~27 per cent | Legacy 4G/5G, multi-brand | Mature, profitable |

| SoftBank Mobile (SB, Y!mobile, LINEMO) | ~22 per cent | Legacy 4G/5G, multi-brand | Mature, profitable |

| Rakuten Mobile | ~ low double digits | Cloud-native, OpenRAN | Heavy losses, narrowing |

Commercial launch came in April 2020. Five years and approximately one trillion yen of cumulative segment losses later, the network covers the overwhelming majority of the Japanese population through a combination of own-build sites and a roaming agreement with KDDI that Rakuten is steadily phasing out as coverage gaps close. Subscriber count crossed eight million in 2024 and has continued to climb through 2025 under a single-tariff “Rakuten Saikyo Plan” priced aggressively against the legacy three. Monthly cash-burn has narrowed materially, and the segment is widely expected to reach EBITDA breakeven inside the medium-term plan window. Net profitability remains a harder question and depends on roaming-cost reductions, ARPU stability and the trajectory of the corporate-debt refinancing the mobile build has forced.

The strategic question that foreign observers most often miss is that Rakuten Mobile is not, in the long run, only — or perhaps even primarily — a consumer carrier. It is the reference deployment for Rakuten Symphony.

Symphony: the export play that almost no one in Japan talks about

Rakuten Symphony, established in 2022 by consolidating the network-software assets that Rakuten Mobile had developed for its own use, sells cloud-native, vendor-disaggregated telco infrastructure software — Symworld, the orchestration platform; Symware, integrated hardware-software stacks; and consulting and integration services — to other carriers. Customers and partners announced to date include 1&1 in Germany (a greenfield OpenRAN deployment), Ligado in North America, and a series of pilot engagements across the Gulf, Southeast Asia and Africa.

The pitch is that the conventional radio-access-network stack — dominated globally by Ericsson, Nokia, Huawei and Samsung — is overpriced, hardware-coupled, and operationally inflexible compared to a cloud-native equivalent. Rakuten built and operates the world’s largest OpenRAN deployment at its Japanese network, and a buyer can therefore acquire battle-tested software rather than vendor-marketing slides. Whether the business succeeds at scale is genuinely open — Tier 1 OpenRAN adoption has been slower than its advocates expected, and the conventional vendors have responded with their own cloud-native roadmaps. But for any telco executive evaluating 5G core or radio infrastructure for the second half of the decade, Symphony is now on the shortlist, which would have been unthinkable in 2018.

The strategic logic for the group is that, if Symphony works, the mobile losses become the cost of building the proof-of-concept that the export business sells against. If it does not, mobile remains a domestic consumer business that has to earn back the build cost on its own. Foreign analysts who model the two separately tend to mis-rate the consolidated entity.

Englishnization, and why the language policy still matters

In 2010 Mikitani announced that, within two years, all internal Rakuten meetings, documentation and email would be conducted in English — including in offices that had no non-Japanese staff at all. The policy, branded Englishnization, was widely mocked at the time inside Japan, including by senior figures at Honda and at the keidanren employers’ federation. Implementation was uneven; English fluency requirements were eventually tied to internal promotion, with TOEIC score thresholds for managerial bands.

Fifteen years on, the policy has produced a measurable set of outcomes. Rakuten’s senior-engineering workforce is meaningfully more international than that of any comparable Japanese listed firm — Indian, European and ASEAN engineers staff substantial fractions of the platform and FinTech teams, and Symphony’s senior leadership operates almost entirely in English with a global rather than Japanese centre of gravity. Cross-border M&A is faster because integration teams share a default language. The cultural cost, by contrast, has been real: Japanese workforce engagement scores in the early years were poor, attrition among older mid-managers ran above sector norms, and the perception inside Japan is still that Rakuten is “the English company,” with all the cultural distance that label carries.

For foreign firms thinking about partnerships, the language policy has a specific practical implication. Rakuten is the rare Japanese counterparty where an English-speaking foreign executive can negotiate substantively without a translator at every step, where contracts are routinely drafted in English first, and where the operational rhythm of joint ventures does not require the host of work-around routines that an MUFG, a Mitsubishi Corporation or a Sony engagement still demands. This is a structural advantage Rakuten has, perhaps under-monetised externally, that almost no other Japanese conglomerate can replicate.

What does not translate

For all its English-speaking surface, Rakuten’s success outside Japan has been mixed. The points-ecosystem moat is a Japan-specific construct, dependent on the density of partner merchants, the integration with domestic banking and the cultural saliency of point accrual that does not transfer to the United States or Europe. Buy.com, acquired in 2010 and rebranded Rakuten.com in the United States, did not establish a sustainable second-tier marketplace and was wound down after several years. PriceMinister in France, Play.com in the United Kingdom, and a string of smaller emerging-market marketplaces were similarly retreated from or restructured during the 2017–2019 portfolio cleanup. The lesson Rakuten internalised, with some reluctance, is that the keizai-ken does not lift-and-shift.

What did stick abroad is more interesting. Viber, the consumer messaging app acquired in 2014 for approximately nine hundred million dollars, has retained substantial scale in Eastern Europe, the Balkans, the Middle East and parts of Southeast Asia, and now serves as a distribution endpoint for Rakuten Ads. Rakuten Advertising is a meaningful affiliate and performance-marketing platform in the United States and Europe. The 2015 Lyft equity stake, although since reduced, returned a significant gain when Rakuten partially sold down post-IPO. The Walmart eBooks partnership combining Walmart’s distribution with Rakuten Kobo’s reader platform ran for several years before being unwound. The FC Barcelona main-shirt sponsorship from 2017 to 2022 and the long-running Golden State Warriors jersey-patch deal gave Rakuten brand visibility in markets where the underlying marketplace was retreating — a deliberate decoupling of brand and e-commerce strategy.

Governance, succession and the founder question

Hiroshi Mikitani turned sixty in 2025. He continues to combine the roles of chairman, president and chief executive, with no publicly named successor and a track record of dismissing the question when it is asked at investor events. The corporate posture is built around his strategic preferences — consumer breadth, language internationalisation, the willingness to absorb a decade of mobile losses to seed an infrastructure-software business — in a way that would be hard for any external successor to inherit without strategic discontinuity. The board has independent directors in the majority but operates within a clear founder-led culture, closer in spirit to a SoftBank under Masayoshi Son than to a Toyota or a Sony. For foreign minority investors this is a known feature rather than a hidden risk: the Rakuten equity story is, in practice, a bet on Mikitani’s capital-allocation judgment plus the mechanical recovery of the mobile segment toward breakeven.

Reading Rakuten

Three takeaways. First, the value of the Rakuten Ecosystem is real but local — it is the best living example outside East Asia’s super-app cluster of how a points-and-membership architecture can knit together a conglomerate’s consumer surfaces, and the right place to study for foreign retailers and fintechs designing loyalty programmes that aim for more than rebate marketing. Second, the mobile business should not be evaluated in isolation from Symphony: the strategic case for absorbing the consumer-carrier losses depends almost entirely on whether Symphony commercialises as a global telco-infrastructure vendor. Third, the English-language policy is not corporate theatre — it is the most consequential operational decision Rakuten has made for foreign engagement, and the reason foreign partners can move at a pace with Rakuten that almost no other Japanese conglomerate currently permits.

FAQ

Who is Hiroshi Mikitani and what is his background?

Mikitani founded Rakuten in 1997 and has served continuously as its chief executive since inception, currently combining chairman, president and CEO roles. Before Rakuten he was a banker at the Industrial Bank of Japan (one of the predecessors of Mizuho), interrupted by a Harvard MBA. He has been an influential public voice on Japanese deregulation, e-commerce policy and language-internationalisation, including a period as a member of the government’s industrial competitiveness council. He retains a substantial founder shareholding and direct strategic control over the group; succession planning has not been publicly disclosed.

Is Rakuten Mobile profitable yet?

Not at the net level. The mobile segment has accumulated roughly one trillion yen of cumulative operating losses since commercial launch in 2020, although the quarterly cash burn has narrowed materially since 2023 as own-network coverage has grown, roaming costs paid to KDDI have fallen, and ARPU has stabilised under the consolidated Rakuten Saikyo Plan tariff. EBITDA-level breakeven for the segment is widely expected within the current medium-term plan window. Net profitability is a separate and harder question that depends on refinancing of the corporate debt the mobile build was funded with.

What is Rakuten Symphony actually selling, and to whom?

Symphony sells cloud-native, vendor-disaggregated mobile-network software and integrated stacks — radio-access-network orchestration, 5G core, operations and integration services — to telco operators worldwide. Customers and partners disclosed publicly include 1&1 in Germany, Ligado in North America, and a set of operators across the Gulf, Southeast Asia and Africa. The pitch is that conventional radio-access-network stacks (Ericsson, Nokia, Huawei, Samsung) are overpriced and operationally rigid compared to a cloud-native OpenRAN equivalent, and that Rakuten has the only proven nationwide reference deployment of the cloud-native approach.

Does Rakuten really operate in English internally?

Yes, since the Englishnization mandate took effect in 2012. Internal meetings, documents, email and intranet are nominally English-default; English fluency requirements are tied to managerial promotion through TOEIC thresholds. Implementation is uneven across operating units — some Japanese-facing consumer teams operate substantially in Japanese in practice — but at the level the foreign partner engages with (corporate development, Symphony, platform engineering, international ad-tech), English is genuinely the working language. This is unusual among Japanese listed companies and is a material practical advantage for foreign counterparties.

What happened with Viber, the Lyft stake and the Walmart partnership?

Viber, acquired in 2014 for approximately nine hundred million dollars, remains a Rakuten subsidiary and retains substantial active-user scale in Eastern Europe, the Balkans, the Middle East and Southeast Asia; it has been progressively integrated into Rakuten Ads as a distribution endpoint. The Lyft equity stake taken in the 2015 pre-IPO round was retained through the public listing and partially sold down subsequently, producing a meaningful realised gain. The Walmart eBooks partnership, which combined Walmart’s distribution with Rakuten Kobo’s reader platform, ran for several years and was unwound; the Kobo e-book business itself continues globally. None of these is treated as a strategic core today, but together they illustrate Rakuten’s willingness to take cross-border equity-and-partnership bets that other Japanese conglomerates would not.

Working with Rakuten

The right way to engage with Rakuten depends on which surface of the group is in scope. A foreign retailer thinking about marketplace placement should approach Rakuten Ichiba’s category teams in Futakotamagawa, ideally with a Japanese-language merchandising plan even though the corporate working language is English. A foreign fintech, payments or card-network partner should engage with Rakuten Card and Rakuten Bank separately and treat the FinTech segment as a network of related but operationally distinct businesses. A foreign telco buyer or systems integrator should treat Rakuten Symphony as a standalone software vendor with its own global commercial team headquartered increasingly in the United States. Brand sponsors and licensors should approach Rakuten Marketing in their home market rather than the Tokyo head office.

Across all of these, the practical advantage Rakuten offers foreign partners — and the reason it deserves to be on the shortlist for any Japan engagement that has a digital or consumer-finance angle — is that the contractual, operational and managerial interface is genuinely bilingual. Negotiating cycles are shorter, integration plans are clearer, and post-signing operating reviews can be conducted without the layered translation that almost every other Japanese counterparty still requires.

Japonity’s Business Matching service introduces qualified foreign companies — marketplace operators, payments and card-network partners, telco infrastructure buyers, ad-tech vendors, sports and entertainment sponsors — to the right Rakuten operating unit and the right point of contact within it. Engagements are scoped from a single introduction through to a structured market-entry programme. If you are evaluating Rakuten as a partner and want to start the conversation with the right business unit rather than the front-door switchboard, tell us what you are looking for.

Related from Japonity — Japan’s digital ecosystems

- SoftBank Group — From PHS reseller to Arm + Stargate AI infrastructure giant

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →