On any given trading day, the value of SoftBank Group’s stake in Arm Holdings — the Cambridge-headquartered chip designer it took back to the Nasdaq in September 2023 — is worth more, on paper, than the entire enterprise value of Nintendo, Sony Financial Group, and Nissan Motor combined. Add the cash flow from listed Japanese telco SoftBank Corp., the residual T-Mobile US position inherited from the 2020 Sprint deal, the Vision Funds’ tangled book of public and private bets, and a freshly announced AI-infrastructure joint venture called Stargate, and the picture comes into focus: SoftBank Group, in 2026, is no longer a Japanese telecom holding company that occasionally dabbles in venture capital. It is one of the largest concentrated bets on the global AI infrastructure stack — and the question for every foreign LP, sovereign fund, and corporate strategist with a Japan file open is whether to treat Masayoshi Son’s machine as a peer, a competitor, or simply an inevitability you cannot route around.

From Saga to SoftBank: the founder problem you cannot ignore

It is impossible to write about SoftBank Group as a corporate entity without writing about its founder. Masayoshi Son, born 1957 in Tosu, Saga Prefecture, to a third-generation Korean-Japanese family, is one of the very few post-war Japanese entrepreneurs whose personal balance sheet, decision-making style, and risk appetite are functionally inseparable from those of the listed company he chairs. He studied economics at the University of California, Berkeley, returned to Japan in his early twenties, and founded SoftBank in Fukuoka in 1981 as a software distributor.

The company’s first transformation came in the late 1990s, when Son moved SoftBank from distribution into internet investing, taking positions in Yahoo! and then in Alibaba in 2000 — a roughly $20 million cheque that, at peak, was reportedly worth in the region of $150 billion, and which has financed almost every subsequent bet. The second transformation was telecom: Vodafone Japan in 2006, the iPhone exclusivity deal that became SoftBank Mobile, and the 2013 acquisition of Sprint. The third — defining the company today — is the Vision Fund era, beginning with the approximately $100 billion SoftBank Vision Fund in 2017, anchored by Saudi Arabia’s Public Investment Fund and Abu Dhabi’s Mubadala, and continued by the internally funded Vision Fund 2 from 2019 onward.

The point worth emphasising, before any discussion of NAV or IRR, is this: SoftBank Group is one of the very few global financial entities where the founder’s personal worldview — Son’s famously long time horizons, his stated 300-year corporate vision, his willingness to take concentrated, sometimes ruinous bets — is the operating system. Any LP or competitor modelling SoftBank without modelling Son is mis-specifying the problem.

The holding structure: what you are actually buying when you buy 9984.T

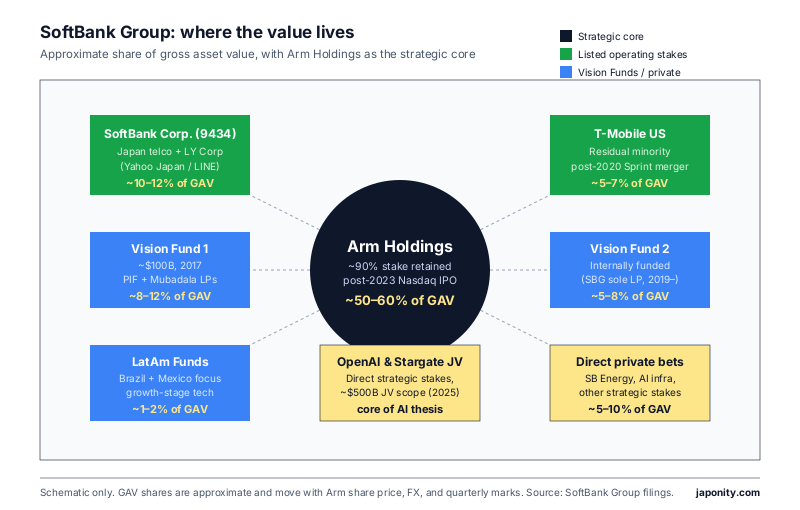

SoftBank Group Corp., listed on the Tokyo Stock Exchange under code 9984, is a pure holding company. It manufactures no phones, operates no networks, and writes no software. Its net asset value is a roll-up of stakes in operating businesses and investment vehicles, and understanding the rough weighting of that roll-up is the single most useful exercise a foreign investor can perform.

The largest line item, by a considerable margin, is the controlling stake in Arm Holdings. Following the Nasdaq re-IPO in September 2023, SoftBank retained approximately 90 percent of Arm and has selectively monetised small portions since. At post-IPO valuations, this single position has at various points accounted for well over half of group gross asset value — a degree of single-stock concentration unthinkable at any conventional asset manager.

The second pillar is the domestic Japanese telecom business, SoftBank Corp. (code 9434), separately listed in Tokyo since 2018 and itself the parent of LY Corporation, the merged Yahoo Japan / LINE entity that operates Japan’s dominant messaging and portal platform. Its dividend stream — among the most reliable in Japanese telecom — is the recurring cash backbone for debt service at the holding-company level.

The third pillar is the residual stake in T-Mobile US. The 2020 merger of Sprint into T-Mobile, after years of regulatory wrangling, left SoftBank as a meaningful minority shareholder. That stake has been monetised in stages, but a residual economic interest plus call options reportedly exercised later continue to feature in the balance sheet.

The Vision Funds sit on top of these foundations. Vision Fund 1 has produced wide dispersion: Coupang and DoorDash on the win column, WeWork as the textbook misfire, Uber as a long saga that ultimately recouped capital. Vision Fund 2, internally funded, has carried both the public-market drawdowns of the 2022 tech selloff and the partial recovery since.

The practical takeaway is that 9984.T is not really one stock. It is a leveraged claim on Arm, a stable claim on Japanese telecom cash flow, a residual claim on US wireless, and a high-variance claim on a portfolio of private and public technology positions — all wrapped in holdco debt and discount.

Inside the NAV: a rough breakdown

SoftBank Group reports its own version of these numbers each quarter. The shape of the NAV — even allowing for daily mark-to-market swings — is best understood at a glance.

| Component | Role in the holding | Approx. share of gross asset value |

|---|---|---|

| Arm Holdings (~90% stake) | Strategic cornerstone; AI-and-mobile chip IP | ~50–60% |

| SoftBank Corp. (listed 9434; incl. LY Corp.) | Domestic telco + Yahoo Japan / LINE platform; dividend backbone | ~10–12% |

| T-Mobile US (residual minority + options) | US wireless exposure inherited from Sprint merger | ~5–7% |

| Vision Fund 1 (PIF / Mubadala anchored) | External-LP fund; mixed realised + unrealised | ~8–12% |

| Vision Fund 2 (internally funded) | On-balance-sheet tech portfolio; high beta | ~5–8% |

| SoftBank Latin America Funds | LatAm growth-stage technology exposure | ~1–2% |

| Direct private investments (incl. OpenAI, Stargate JV) | Strategic AI-stack bets held off-fund | ~5–10% |

| Net debt at holdco | Margin loans, bonds, asset-backed financing | (deducted) |

The exact weights move materially with the Arm share price, the dollar-yen rate, and quarterly marks on the Vision Fund private book. But the shape — an Arm-heavy core, a telco cash-flow base, and an AI-tilted growth tail — is stable across cycles.

The Vision Fund record: what twenty-five quarters of marks actually tell us

It is fashionable in Anglo-American commentary to treat the Vision Funds as a single failed experiment. The record is more interesting than that.

Vision Fund 1, by SoftBank’s own reporting, has at various points shown a cumulative gain against committed capital that places it in the upper half of large global growth-equity vintages, though well behind the best US venture franchises. Dispersion within the fund is enormous: the 2021 Coupang IPO, the DoorDash listing, Uber, and select Chinese e-commerce wins carried the realised P&L; WeWork is the canonical loss, written down repeatedly and ultimately reorganised; several Indian and Latin American positions traded in a wide range, dragged in 2022 and recovering partially since.

Vision Fund 2 is structurally different because SoftBank Group itself is the sole LP. It launched into a more difficult macro tape and has experienced sharper paper losses on private marks, which flow through directly to the parent — one reason group net income has swung between record annual losses and record annual profits in successive fiscal years.

For a foreign LP evaluating future SoftBank-managed vehicles, the relevant signal is not whether VF1 or VF2 “worked” in some binary sense — it is whether SoftBank has demonstrated repeatable edge in a defined slice of growth-stage investing. The honest answer, in 2026, is mixed: cheque-size, network, and conviction-on-demand advantages few competitors match, but an average IRR that has not consistently beaten patient long-only growth strategies at lower cost.

The AI infrastructure pivot: Arm, OpenAI, Stargate, and the new thesis

Since roughly 2023, Son has been unusually explicit about what he believes the next decade of SoftBank will be about: artificial intelligence, and specifically the compute, chip, and energy infrastructure underneath it. Three deals define the pivot.

First, Arm. Holding the controlling stake in the world’s most widely licensed CPU instruction set, at a moment when AI workloads are pushing chip architecture innovation back into every hyperscaler’s roadmap, is the cornerstone. SoftBank has resisted analyst pressure to sell down its Arm position aggressively, treating it as a strategic asset around which other AI-stack investments are positioned.

Second, OpenAI. SoftBank is reported to have taken a substantial direct position, including participation in late funding rounds that valued the company well into the hundreds of billions of dollars. Exact economic terms vary by reporting source, but SoftBank is unambiguously one of the largest non-Microsoft external backers of the frontier model leader.

Third, Stargate. Announced in early 2025 jointly with OpenAI, Oracle, and other partners, Stargate is the AI-infrastructure programme that has come to symbolise the SoftBank thesis: a multi-year plan to build US-sited data-centre capacity, GPU clusters, and energy infrastructure for large-model training and inference. Total programme scope was widely reported at approximately $500 billion, with SoftBank and OpenAI as the lead participants. As with any programme at that scale, the gap between announced and deployed capital will define the next several years.

Around these three sit smaller but strategic positions: SB Energy, the group’s renewable arm pivoting toward dedicated power for AI compute; Vision Fund holdings in AI-adjacent infrastructure; and continued recycling of capital from legacy positions into AI-stack bets.

The bear case, in the company’s own words

SoftBank Group’s own filings are unusually candid about the risks of the strategy. Three stand out.

The first is concentration. With Arm dominating gross asset value and AI-stack bets adding correlated exposure, NAV is structurally more sensitive to a single thematic drawdown — an AI-spending pause, an Arm multiple compression, or both — than at any prior point in the company’s history. The 2022 episode, when Vision Fund marks collapsed alongside the broader US tech selloff, was a preview.

The second is leverage. SoftBank Group operates with sizeable structural debt at the holdco level, much of it secured against listed assets via margin loans. The loan-to-value ratio is managed with explicit policy limits, but in a sharp drawdown that policy can turn procyclical — forced selling of the most liquid assets at the worst moment.

The third is governance. The concentration of decision-making in the founder, the small senior team around him, and the historical reluctance to bring in external constraints have all been flagged by index providers and governance specialists. CFO Yoshimitsu Goto is widely respected as the institutional counterweight, but the basic asymmetry — Son drives strategy, the organisation executes — remains.

Working with SoftBank: counterparty, competitor, or co-investor?

For foreign sovereign funds, corporate venture arms, and family offices building Japan-facing strategies, SoftBank Group is rarely a neutral actor. Three modes of engagement are worth distinguishing.

As a co-investor, SoftBank brings cheque size and pattern recognition in growth-stage technology that few global firms match. Co-investing alongside the Vision Funds in late-stage rounds has been an efficient way for sovereigns and family offices to access large private positions they could not source alone. The trade-off is governance: SoftBank typically wants concentrated rights, and cap-table dynamics post-investment can be heavy.

As a competitor, SoftBank’s cheque size is the central problem. Across AI infrastructure, Japanese tech IPOs, and select sectors in India and Latin America, a foreign fund bidding against SoftBank on the same round will routinely find its bid stretched on valuation. The most successful competing strategies have explicitly avoided head-to-head competition, positioning either earlier in the stage spectrum or in geographies where SoftBank is less active.

As a corporate counterparty — for foreign technology companies considering Japan entry, for chip designers licensing Arm IP, for energy infrastructure firms participating in Stargate-adjacent projects — SoftBank can be one of the most useful single relationships in Tokyo. The group’s reach into the domestic telco, payments, and platform ecosystem via SoftBank Corp. and LY Corporation is unmatched, and Son personally has been willing to sponsor foreign entrants that fit the strategic thesis.

The next chapter: succession, second derivatives, and the Japan question

The question hanging over every long-dated analysis is what the company looks like after Son. He has not publicly committed to a clear succession timeline, and historical experiments with anointed successors — most notably the brief tenure of Nikesh Arora as president in the mid-2010s — did not produce a settled answer. Goto and a small group of senior operators run the day-to-day, but the strategic apex remains the founder.

For Japan as a whole, SoftBank’s trajectory matters out of proportion to its market capitalisation. It is one of the few Japanese corporate vehicles operating at genuine global scale in technology investing, and the only one with credible standing in the AI-infrastructure conversation. Whether its concentrated AI-stack bet pays off will materially affect Japan’s wider narrative as a destination for foreign capital.

The verdict, for now, is that SoftBank Group is neither the runaway success its boosters claim nor the slow-motion accident its critics describe. It is something more specific: a concentrated, leveraged, founder-driven bet on a particular reading of the next decade, at a scale almost no other actor could attempt. For foreign LPs, sovereigns, and corporates, the right posture is sober engagement — on terms that protect against the concentration and governance risks the strategy carries.

FAQ

Who actually owns SoftBank Group, and how large is Masayoshi Son’s personal stake?

SoftBank Group is publicly listed in Tokyo (9984.T) with a broad institutional shareholder base, but Masayoshi Son personally holds approximately a quarter of the outstanding shares through direct and affiliated holdings — a stake that, depending on the share price, is among the largest individual positions in any major Japanese listed company. That holding gives him effective working control of the board agenda even though he is not a majority owner in the formal sense.

How does the Arm Holdings position dominate the SoftBank investment case?

Following the 2023 Nasdaq re-IPO of Arm, SoftBank Group retained approximately 90 percent of the chip designer. At post-IPO valuations, that single position has at times accounted for well over half of SoftBank Group’s gross asset value, making 9984.T functionally a leveraged claim on the Arm equity story — and on the broader AI-chip cycle Arm IP is exposed to.

What exactly is Stargate, and how committed is SoftBank to it?

Stargate is the AI-infrastructure joint venture announced in early 2025 by SoftBank, OpenAI, Oracle, and partners, with a programme scope widely reported at approximately $500 billion over multiple years. It funds US-sited data-centre capacity, GPU clusters, and supporting energy infrastructure for large-model training and inference. SoftBank is one of the two lead participants alongside OpenAI; the gap between announced and actually deployed capital is the variable that will define the programme’s real significance.

How did the WeWork situation end, and what does it tell us about Vision Fund risk?

WeWork, one of Vision Fund 1’s largest single positions, was written down repeatedly after the failed 2019 IPO and subsequent operational and pandemic-era pressures, and was ultimately reorganised through bankruptcy proceedings. It is the textbook case for the concentration and governance risks of the Vision Fund model — large cheques into founder-driven private companies with limited public-market discipline — and it materially shaped the more cautious posture Vision Fund 2 took on subsequent late-stage deals.

Can foreign LPs still invest in a SoftBank-managed fund today?

Vision Fund 2 is internally funded by SoftBank Group itself and not open to external LPs. The original Vision Fund 1, anchored by Saudi Arabia’s PIF and Abu Dhabi’s Mubadala, is closed. Foreign sovereigns and family offices that wish to take exposure to SoftBank-managed deal flow typically do so via co-investment alongside the funds in specific transactions, or by holding the listed SoftBank Group equity (9984.T) directly — each route with very different governance and liquidity profiles.

Working with SoftBank Group

Looking to co-invest alongside SoftBank Group, license Arm-based IP into the Japanese market, participate in AI infrastructure projects connected to the Stargate programme, or scope partnerships with SoftBank Corp., LY Corporation, or Vision Fund portfolio companies in Japan? Get in touch via Japonity’s business-matching service — we connect foreign investors, corporates, and strategic counterparties with the right partners inside Japan’s largest technology holding company.

Related from Japonity — Japan’s digital ecosystems

- Rakuten Group — The points-economy empire and the mobile bet that almost broke it

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →