When Tokyo Gas took a major equity stake in Castleton Commodities International (CCI) — the US-based merchant energy trader formerly known as Louis Dreyfus Highbridge Energy — in 2016, it signalled something larger than a portfolio diversification. Japan’s largest city-gas utility, which has piped methane into Tokyo households since 1885, was repositioning itself as a global LNG arbitrageur. Add the Cove Point and Cameron offtakes from US Gulf Coast liquefaction, the long-suspended but still-contracted Mozambique LNG project, the half-century relationship with Brunei LNG, and the 2016–2017 deregulation that broke open Japan’s electricity and gas retail markets — and Tokyo Gas (TYO: 9531) looks less like a regulated utility and more like a Tokyo-headquartered, vertically integrated energy major with one foot in 12 million-plus domestic meters and the other in Henry Hub.

From 1885 Gas Lamps to a Global Energy Trader

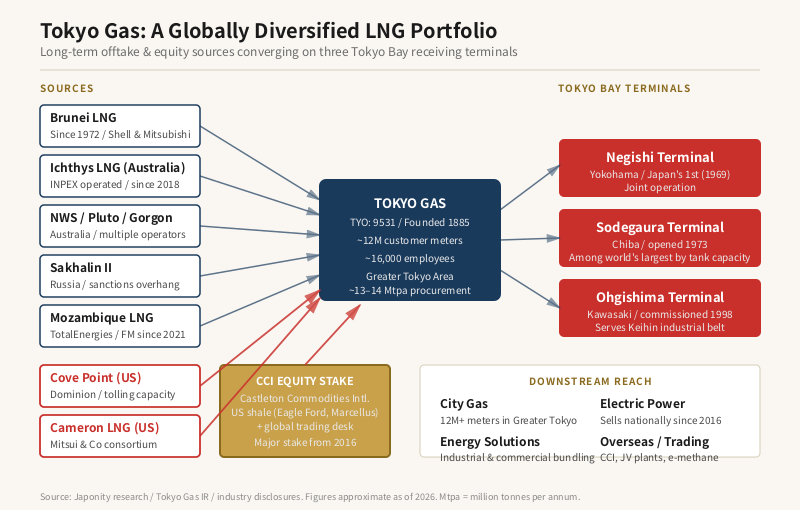

Tokyo Gas Co., Ltd. (東京瓦斯株式会社, Tōkyō Gasu) was incorporated in October 1885, when gas lighting was still the dominant municipal infrastructure for modernising Tokyo. Headquartered in Minato-ku, Tokyo, the company today serves approximately 12 million customer meters across the Greater Tokyo Area — encompassing Tokyo, Kanagawa, Saitama, Chiba, Ibaraki, Tochigi, and Gunma prefectures — making it not only Japan’s largest city-gas utility by volume but one of the largest urban gas distributors in the world.

For most of its first century, Tokyo Gas’s business model was straightforward: import town gas feedstock (initially coal-derived, later naphtha, and from 1969 onward, liquefied natural gas), distribute through a pipeline network now exceeding 60,000 kilometres, and bill a regulated monopoly customer base. That model was upended twice in quick succession — first by the global LNG market’s transformation from rigid long-term contracts into a liquid spot market, and second by Japan’s domestic deregulation that simultaneously freed Tokyo Gas to compete nationally and exposed its home territory to invasion by Tokyo Electric Power Company (TEPCO), Osaka Gas, and a swarm of new entrants.

The Three Receiving Terminals: Japan’s LNG Front Door

Tokyo Gas’s physical backbone is its three LNG receiving terminals, all located on Tokyo Bay. Negishi LNG Terminal in Yokohama, jointly operated with JERA’s predecessor since 1969, was Japan’s first LNG receiving facility. Sodegaura LNG Terminal in Chiba, opened in 1973 and now one of the largest LNG storage facilities in the world by tank capacity, anchors deliveries from Southeast Asia, Australia, and increasingly the US Gulf. Ohgishima LNG Terminal in Kawasaki, commissioned in 1998 and expanded since, serves the Keihin industrial belt.

Together, these terminals handle approximately 13–14 million tonnes of LNG annually for Tokyo Gas’s own demand — and serve as wholesale hubs from which Tokyo Gas resells regasified gas to other Japanese utilities, IPPs (independent power producers), and increasingly, electricity generation joint ventures. The terminals are not just receiving infrastructure; they are strategic optionality, allowing Tokyo Gas to swing cargoes between Asian buyers when arbitrage opens.

The CCI Stake: A Bet on Merchant Energy

In April 2016, Tokyo Gas announced a major equity investment in Castleton Commodities International (CCI), the Connecticut-headquartered merchant energy company that had been spun out of Louis Dreyfus Highbridge Energy in 2013. CCI controls upstream US shale gas and oil assets — notably in the Eagle Ford and Marcellus basins — alongside power generation, midstream pipelines, and a global physical and financial trading book covering crude, refined products, natural gas, power, and LNG.

For Tokyo Gas, CCI is three things at once. First, it is upstream equity exposure to US shale — a hedge against the spot LNG prices Tokyo Gas itself must pay to import the molecule. Second, it is a trading desk in North America and Europe with deep insight into Henry Hub, TTF, and JKM (Japan-Korea Marker) spreads, allowing Tokyo Gas to optimise its global cargo book. Third, it is a learning vehicle: the cultural and operational distance between a regulated Japanese utility and a merchant energy trader is vast, and CCI gives Tokyo Gas an inside view of how trading houses make money in volatile commodity markets — a capability Tokyo Gas is steadily internalising.

The LNG Sourcing Portfolio

Tokyo Gas’s LNG procurement portfolio is one of the most geographically diversified of any single buyer in the world. The table below summarises the principal long-term and equity-linked sources.

| Source Project | Country / Operator | Tokyo Gas Role | Status |

|---|---|---|---|

| Brunei LNG | Brunei / Shell & Mitsubishi consortium | Long-term offtaker since 1972 | Active, contract extensions |

| Cove Point LNG | USA / Dominion Energy | Tolling capacity holder (with Sumitomo) | Active since 2018 |

| Cameron LNG | USA / Mitsui & Co. operated consortium | Offtake via consortium structure | Active since 2019 |

| Mozambique LNG | Mozambique / TotalEnergies operated | Long-term offtaker | Force majeure declared 2021, restart pending |

| Ichthys LNG | Australia / INPEX operated | Long-term offtaker | Active since 2018 |

| Pluto / Gorgon / NWS | Australia / Various | Offtake contracts | Active |

| Sakhalin II | Russia / Gazprom-led | Long-term offtaker | Active but under sanctions overhang |

| CCI Equity | USA / CCI (Tokyo Gas equity) | Upstream & trading exposure | Active since 2016 |

What this portfolio does is give Tokyo Gas optionality across three dimensions: geography (Atlantic basin vs. Pacific basin), pricing index (oil-linked vs. Henry Hub-linked vs. spot JKM), and tenor (legacy 20-year contracts rolling into shorter, more flexible structures). When Mozambique LNG went into force majeure in 2021 following the Cabo Delgado insurgency, Tokyo Gas could rebalance through US Gulf cargoes and spot purchases — exactly the resilience the diversification was designed to deliver.

2016–2017 Deregulation: The Domestic Pivot

For decades, Japan’s energy sector operated as a series of regional monopolies: ten regional electric utilities (TEPCO in Tokyo, Kansai Electric in Osaka, etc.) for power, and roughly 200 city-gas utilities (Tokyo Gas, Osaka Gas, Toho Gas being the big three) for gas, each protected within its own service territory. Then in April 2016, retail electricity sales were fully deregulated. In April 2017, retail city-gas sales followed.

The strategic implication for Tokyo Gas was immediate. The company began aggressively selling electricity into its own service territory — directly competing with TEPCO Energy Partner — by leveraging its existing 12 million-meter customer relationship and bundled gas-plus-power offerings. Conversely, TEPCO and other regional utilities (and new entrants like SoftBank’s SB Power, Mitsubishi’s MC Retail Energy, and several telco-energy joint ventures) began selling gas in Tokyo. Tokyo Gas has, by most counts, gained more electricity customers than it has lost gas customers — the cross-sell economics favour the incumbent with deeper household trust and a denser meter footprint.

To supply that electricity, Tokyo Gas has built or partnered into a fleet of gas-fired power plants — Ohgishima Power Station, Kawasaki Natural Gas Power, and equity stakes in numerous IPPs — collectively giving it generation capacity in the high single-digit gigawatts. The company has also moved into renewables, with offshore wind investments and a stated ambition to grow its renewable portfolio significantly through the late 2020s.

Tokyo Gas vs. Osaka Gas vs. Toho Gas

Japan’s “big three” city-gas utilities each dominate their respective metropolitan area, but their strategic postures differ meaningfully.

| Metric (approx.) | Tokyo Gas (9531) | Osaka Gas (9532) | Toho Gas (9533) |

|---|---|---|---|

| Founded | 1885 | 1897 | 1922 |

| HQ | Minato, Tokyo | Osaka | Nagoya |

| Customer meters | ~12 million | ~7 million | ~2.7 million |

| Annual revenue (consol.) | ~JPY 2.5–3 trillion | ~JPY 1.7–2 trillion | ~JPY 0.7 trillion |

| Employees (consol.) | ~16,000+ | ~21,000+ | ~7,000+ |

| LNG terminals | 3 (Negishi, Sodegaura, Ohgishima) | 2 (Senboku I & II) | 1 (Yokkaichi) |

| Distinctive international play | CCI equity, US shale, Cove Point | US Freeport LNG, real estate & materials | Smaller international footprint |

Tokyo Gas’s distinctive bet is its merchant-trading orientation via CCI and its dense US Gulf offtake position. Osaka Gas, by contrast, has built a more diversified non-energy business — including real estate, materials, and a large overseas E&P arm — while Toho Gas remains primarily focused on its Chubu home market with selective international exposure.

Business Segments and B2B Revenue Mix

Tokyo Gas’s consolidated reporting breaks the business into roughly five segments: City Gas, Electric Power, Energy Solutions (industrial gas, on-site energy services, district heating & cooling), Overseas (upstream, LNG trading, CCI), and Other (real estate, engineering, IT services).

Household gas is the most visible business but no longer the largest profit pool. Electric power has grown rapidly post-deregulation, and energy solutions — particularly large-scale industrial and commercial customers buying heat, power, and gas as bundled services — generates outsized margin. The Overseas segment, including CCI, can swing significantly with commodity prices: in years of LNG price spikes (2022–2023), upstream equity contributions were material; in calmer years they are modest.

For international counterparties, the most relevant fact is that Tokyo Gas is genuinely a B2B-international company. Its procurement teams in Tokyo, Houston, and Singapore are continuously in market for LNG cargoes, shipping capacity, hedging instruments, and upstream equity opportunities. It is one of the few Japanese utilities with the in-house trading sophistication to engage on Henry Hub-indexed structures, FOB optionality, and destination-flexible contracts.

Decarbonisation: Hydrogen, e-Methane, and the Long Transition

Tokyo Gas has committed to a “Compass 2030” strategic vision (and successor plans) that places carbon neutrality by 2050 at the centre, with the most distinctive feature being its bet on e-methane (synthetic methane) — methane produced by combining green hydrogen with captured CO₂. The logic is straightforward: Tokyo Gas’s pipeline network and 12-million-meter customer base are designed for methane molecules. If those molecules can be made carbon-neutral, the existing distribution infrastructure remains valuable for decades. Tokyo Gas is partnering with US, Middle Eastern, and Australian players on demonstration-scale e-methane projects, with a long-term ambition to blend e-methane into the city-gas supply at increasing concentrations through the 2030s and 2040s.

Hydrogen, ammonia co-firing in power generation, CCUS (carbon capture, utilisation, and storage) tied to upstream equity, and offshore wind round out the transition portfolio. The unifying thesis is that Tokyo Gas’s competitive advantage — the pipes, terminals, customer relationships, and global procurement reach — can be preserved through the energy transition if the molecules flowing through them change.

Leadership and Governance

Tokyo Gas is listed on the Tokyo Stock Exchange Prime Market under code 9531. As of recent disclosures, Takashi Uchida serves as Chairman (会長) and Shinichi Sasayama as President (社長) — readers should verify against the latest company disclosures, as Japanese utility leadership transitions tend to follow a multi-year cycle. The company employs approximately 16,000 people on a consolidated basis across roughly 150 group companies in Japan and abroad.

Shareholding is broad and stable: Japanese institutional investors and trust banks hold the majority, with a meaningful long-term foreign institutional base. Like most Japanese utilities, Tokyo Gas is influenced by — though not formally subject to — METI (Ministry of Economy, Trade and Industry) policy on energy security, LNG procurement diplomacy, and carbon-neutrality roadmaps.

Capital allocation discipline has tightened in recent years. The company has signalled a willingness to recycle capital out of mature domestic distribution assets and into higher-return international LNG, US shale, and renewable platforms — a posture that distinguishes it from more conservative regional Japanese utilities. Buybacks and dividend progression have been used to communicate that discipline to a steadily internationalising shareholder base, and Tokyo Gas has been an early adopter among Japanese utilities of TCFD-aligned climate disclosure and explicit scenario analysis tied to its e-methane transition pathway.

FAQ

Is Tokyo Gas a government-owned utility?

No. Tokyo Gas is a privately held, publicly listed company on the Tokyo Stock Exchange (code 9531). It has no Japanese government equity. It is, however, regulated by METI for tariffs, network access, and safety, and operates within Japan’s national energy security framework.

How does Tokyo Gas differ from TEPCO?

Tokyo Gas is a city-gas utility (distributing methane via pipelines), while TEPCO is an electric power utility. Historically they served the same Greater Tokyo geography in non-overlapping business lines. Since the 2016–2017 deregulation, they compete head-on — Tokyo Gas now sells electricity, and TEPCO now sells gas, in each other’s traditional service territories.

What is the significance of the CCI investment?

Tokyo Gas’s major equity stake in Castleton Commodities International (taken in 2016) gives it direct exposure to US shale gas and oil production, plus a global merchant energy trading capability. It is one of the most aggressive international moves by any Japanese city-gas utility, and gives Tokyo Gas trading insight that most peers must source through third-party brokers.

What is e-methane and why does Tokyo Gas care about it?

E-methane is synthetic methane made from green hydrogen and captured CO₂, producing a molecule chemically identical to natural gas but with a net-zero carbon footprint. For Tokyo Gas, e-methane is a strategic bridge that preserves the economic value of its existing pipeline network and customer relationships through the energy transition — rather than stranding them.

How can international partners engage with Tokyo Gas?

Tokyo Gas maintains active commercial offices and procurement teams in Tokyo, Houston, Singapore, and other LNG hubs. Engagement typically takes one of several forms: LNG cargo sales (spot or term), upstream equity co-investment, midstream infrastructure partnerships, technology licensing (especially around e-methane, hydrogen, and energy efficiency), or industrial energy solutions partnerships in Japan.

Working with Tokyo Gas

For LNG producers, midstream developers, hydrogen technology companies, offshore wind partners, and industrial energy customers looking to engage Tokyo Gas — or to understand the broader Japanese city-gas, LNG procurement, and energy-transition landscape — Japonity’s business matching service can help structure introductions, brief on counterparty positioning, and identify the right entry point. Visit /business-matching/ to begin.

Related from Japonity — Japan’s electric & gas utilities

- TEPCO Holdings — Japan’s largest utility, still rebuilding from Fukushima

- Kansai Electric Power — Japan’s most nuclear-dependent utility

- Chubu Electric Power — Toyota’s home-region utility and the JERA LNG empire

- Osaka Gas — Japan’s #2 gas utility and its US oil-and-gas pivot

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →