Honda Motor Co., Ltd. is the world’s largest motorcycle manufacturer by units sold, shipping approximately 19 to 20 million two-wheelers a year — more than the next three competitors combined. Yet outside Japan, the company is filed almost entirely under “automaker,” a framing that fundamentally misreads where Honda’s resilience comes from. As the industry resets around electric vehicles and Honda quietly walks back from on-again, off-again merger talks with Nissan in early 2025, the parallel businesses that nobody benchmarks — power products, marine engines, and a small business jet that has outsold Cessna in its segment — are doing more strategic work than the carmaker’s quarterly slides admit.

A company built sideways, not vertically

Honda is the outlier of post-war Japanese industrial history. It has no zaibatsu lineage, no pre-war heritage business, and no protective keiretsu wrapped around it. Soichiro Honda founded the company in Hamamatsu in 1948 by bolting surplus military radio generators onto bicycles. The pairing with Takeo Fujisawa — Honda the engineer, Fujisawa the financier and merchant — produced a company that has, for seventy-seven years, refused to behave like its peers.

Toyota built itself on the loom-to-cars Toyoda family arc and a vertically interlocked supplier network. Nissan grew through the Ayukawa zaibatsu and post-war state support. Honda did neither. It went straight at exports, raced motorcycles before anyone in Tokyo thought that was a serious idea, opened a U.S. factory in Marysville, Ohio in 1982 before any Japanese carmaker had built passenger cars in America, and treated horizontal diversification — into outboard motors, lawn mowers, generators, and eventually jets — as the natural expression of an engine company. The result is a portfolio that no other automaker has, and arguably none can now replicate.

The segment mix nobody draws correctly

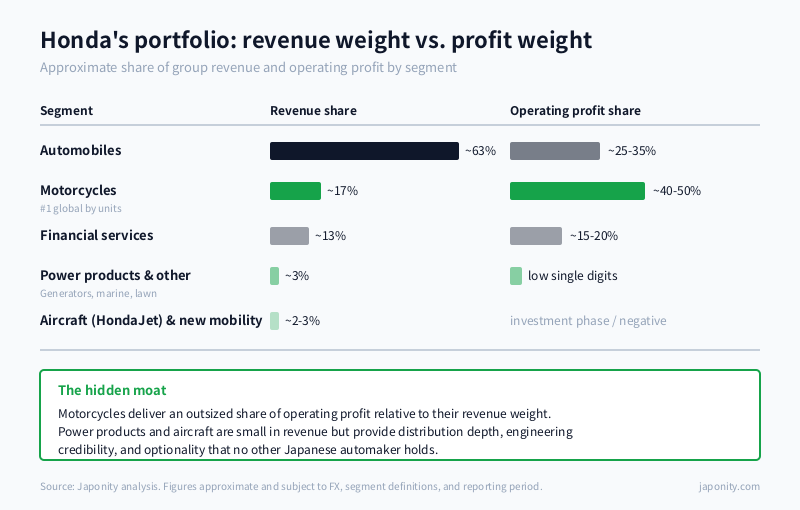

If you only read the headline revenue numbers, Honda looks like a mid-sized automaker with a side business. The unit economics tell a different story. The table below summarises the rough shape of Honda’s consolidated operations across its main segments — note especially the disproportion between motorcycle revenue share and motorcycle operating profit share.

| Segment | Approx. share of group revenue | Approx. share of operating profit | Strategic role |

|---|---|---|---|

| Automobiles | ~63% | ~25-35% | Volume, brand, technology platform |

| Motorcycles | ~17% | ~40-50% | Profit engine, emerging-market dominance |

| Financial services | ~13% | ~15-20% | Captive finance, dealer support |

| Power products & other | ~3% | Low single digits | Engine-platform halo, distribution depth |

| Aircraft (HondaJet) and new mobility | ~2-3% | Currently negative / investment phase | Long-dated optionality |

Segment economics fluctuate with foreign exchange, raw materials, and incentives, but the structural pattern has held for years: motorcycles produce a disproportionate share of Honda’s profits relative to their revenue weight. That is the hidden moat. It is also why a bad year in autos — say, a slow EV ramp or a tariff shock — does not push Honda into the kind of existential rethink that has consumed Nissan since 2023.

The motorcycle business is a different company in disguise

Honda sells motorcycles, scooters, and small utility two-wheelers in roughly 150 countries. The dominant geographies are India, Indonesia, Vietnam, Thailand, the Philippines, and Brazil, with significant presence in Pakistan, Nigeria, and Mexico. The Honda Dream, Wave, Activa, and PCX series are not products in the Western sense — they are infrastructure. They move office workers in Hanoi, deliver food in São Paulo, and serve as the family car in Tier-2 Indian cities.

This business looks nothing like the auto business. Average selling prices sit in the hundreds of dollars rather than tens of thousands. Capital intensity per unit is a fraction of a car’s. Dealer networks reach into towns that no Toyota showroom would justify. Most importantly, the technology cycle is far slower: a 110cc commuter engine designed in the 2010s remains commercially competitive in 2026, while the equivalent automotive powertrain has been through three regulatory rewrites.

That slower cycle is what makes motorcycle profit unusually durable. Honda does not need to bet the farm on every emissions regime change in the way automakers must. And because motorcycles in emerging markets are buying their first form of mechanised transport, the long-run growth path is structurally different from saturated four-wheel markets in the U.S., Europe, and Japan.

Power products: the boring business that keeps the lights on

Honda Power Products — generators, water pumps, tillers, lawn mowers, outboard marine engines, and snow blowers — is small in revenue terms but does three jobs that matter. First, it gives Honda a global service and distribution footprint in non-automotive retail (hardware stores, marine dealers, agricultural co-ops) that no rival automaker has. Second, the small-engine R&D feeds straight back into motorcycle and automotive engine programs. Third, it provides a low-risk testbed for new powertrain ideas, including portable batteries and small-displacement hybrids, before they need to scale.

It is also Honda’s quietest export business. In categories like outboard marine motors and portable generators, the company sits in the global top three by share. Buyers in those segments are price-sensitive industrial customers — landscapers, contractors, fishermen, disaster-relief agencies — who reorder by habit, not by marketing campaign. That stickiness is invisible in the consolidated P&L but very real on the ground.

HondaJet: the moonshot that actually worked

Honda Aircraft Company, headquartered in Greensboro, North Carolina, launched the HondaJet HA-420 in 2015 after roughly three decades of internal R&D. The defining feature — engines mounted on pylons above the wings — was an aerodynamic gamble that improved cabin space and reduced drag. The HondaJet has been the world’s most-delivered very light jet in multiple recent years, repeatedly outshipping Embraer’s Phenom 100 and the Cessna Citation M2 in its size class. A larger HondaJet 2600 (also branded as the Echelon) has been in development for mid-size missions.

In financial terms, the aircraft business has not been a needle-mover for the group. In strategic terms it has been disproportionately valuable: it is proof that Honda can take a clean-sheet, multi-decade engineering project from research to certified product, in a market where Japanese industrial credibility was historically thin. That track record matters when investors ask whether Honda can credibly execute on a clean-sheet EV architecture in the late 2020s.

Autos: a deliberately slower EV reset than Toyota’s

Honda’s 2024-2026 EV strategy reads as a course correction from earlier, more aggressive timelines. The company has scaled back near-term EV production volume targets and pushed more weight onto hybrids in the medium term, especially in North America, where its Civic and CR-V hybrids continue to anchor U.S. retail share. The flagship pure-EV effort — the Honda 0 Series, previewed at CES — is targeted for launch from 2026, built on a clean-sheet architecture rather than on a retrofit of existing platforms.

This is not the same bet as Toyota’s. Toyota’s hybrid-led, multi-pathway strategy is a deliberate refusal to over-index on BEV ahead of grid and battery readiness. Honda’s revision is more pragmatic: a recognition that its earlier EV volume ambitions outran what its battery supply, cost curve, and dealer network could absorb. The partnership with General Motors for a shared mid-size EV platform was dissolved in 2024, after which Honda re-committed to in-house architecture work alongside a battery joint venture with LG Energy Solution in Ohio.

Acura, the premium brand launched in the U.S. in 1986 (the first Japanese luxury marque, predating Lexus and Infiniti), is being repositioned around performance EVs, with the Acura ZDX as a transitional product built on GM’s Ultium platform before the in-house architecture comes online.

The Nissan talks: what they were, and what they revealed

The most strategically significant event of the past eighteen months was the Honda–Nissan merger discussion that became public in late 2024 and collapsed by February 2025. Reported terms involved an integration under a new holding company, with Mitsubishi Motors potentially joining as a third participant. The discussions did not survive disagreements over governance, equity ratios, and how much of Nissan’s restructuring burden Honda would absorb.

For Honda, the episode revealed several things at once. It confirmed that management views scale and shared platforms as a real constraint in the EV transition, especially against Chinese competition. It also confirmed that Honda will not accept terms that compromise its engineering autonomy — a non-negotiable for a company whose identity rests on independent technical work. The collapse leaves Honda pursuing scale through narrower technology partnerships (Sony for the Afeela EV brand, LG for batteries, IBM for next-generation semiconductors) rather than full corporate integration.

Robotics and the long tail of “what if”

Honda’s robotics work has been one of the most-watched and least-monetised programs in Japanese industry. ASIMO, the humanoid robot first demonstrated in 2000 and formally retired from active demonstrations in 2022, never became a product. Its successor research has spread into walking assist devices, the UNI-CUB personal mobility seat, and contributions to disaster-response robotics after Fukushima.

In the current generative-AI and humanoid-robotics cycle, where Tesla, Figure, 1X, and several Chinese firms are racing to commercialise bipedal robots, Honda’s institutional knowledge in balance, actuation, and human-scale robotics is suddenly relevant in a way it was not five years ago. Whether that translates into a product line, a licensing business, or a research-only contribution remains open. For overseas partners, the relevant point is that the IP and the talent are real, and Honda is open to selective collaboration in adjacent fields.

The supplier ecosystem: open, not closed

Unlike Toyota’s tightly interlocked supplier network, Honda’s procurement is comparatively open. Long-standing relationships with Keihin (now part of Hitachi Astemo), Showa, Nissin Kogyo, F.C.C., Musashi Seimitsu, Yutaka Giken, and others form the core of the Japanese supply base, but Honda has historically been more willing than Toyota to source from non-affiliated and overseas suppliers, particularly for electronics, batteries, and software.

This matters for foreign companies looking to enter Honda’s supply chain. The barrier is engineering credibility, not group membership. Suppliers with differentiated capability in battery cells, power semiconductors, ADAS software, lightweight materials, and high-precision casting have historically had viable paths to qualify, with Tier-1 engagement typically beginning through a North American or Asian regional engineering centre rather than through Tokyo headquarters.

Why Honda still warrants its own thesis

The cleanest way to think about Honda is to refuse the auto-only lens. It is a portfolio of engine-platform businesses with very different cycles, geographies, and customer profiles, held together by an engineering culture that has stayed remarkably consistent across three generations of leadership. The motorcycle business funds optionality. The power-products business deepens distribution. HondaJet proves clean-sheet capability. The auto business is the most visible and most volatile, but it is no longer the sole load-bearing wall.

The 2026 EV reset will be judged on whether the 0 Series architecture is genuinely cost-competitive at the cell and platform level, and whether Honda can hold its hybrid lead in North America long enough to fund the BEV ramp. Both questions are open. What is not open is whether Honda has the engineering depth and balance-sheet patience to run the experiment. It does — because the rest of the company is doing other work in the meantime.

FAQ

Who owns Honda Motor Co., Ltd.?

Honda is a publicly listed company on the Tokyo Stock Exchange (ticker 7267) and the New York Stock Exchange (HMC). There is no controlling shareholder and no founding-family ownership block — the Honda family exited its equity position decades ago. The largest shareholders are typically Japanese trust banks acting on behalf of institutional investors, alongside global asset managers. Cross-shareholdings exist with selected suppliers and partners but are modest compared to Toyota Group structures.

How serious is Honda’s EV strategy compared to Toyota’s?

Honda has committed publicly to a 100% electrified vehicle line-up (BEV and FCEV combined) by 2040, with the Honda 0 Series as the in-house BEV architecture launching from 2026. Compared with Toyota’s hybrid-first, multi-pathway approach, Honda is leaning slightly more aggressively toward pure BEV in the late 2020s while still relying on hybrids to defend North American share in the medium term. Neither company is staking the business on a single powertrain pathway.

Why is Honda the world’s largest motorcycle maker, and is that position durable?

Honda holds the global #1 position because of decades of brand trust in emerging Asia and Latin America, a manufacturing footprint that produces locally for local markets (India, Indonesia, Vietnam, Thailand, Brazil), and a product range that covers everything from sub-150cc commuters to large-displacement leisure motorcycles. The position is durable in the short to medium term; the main long-run risk is electrification in two-wheelers, where Chinese, Indian, and Taiwanese manufacturers are pushing aggressively. Honda has begun rolling out electric commuter models but is not yet the share leader in EV two-wheelers.

What is HondaJet and why does it matter?

HondaJet is the very light jet produced by Honda Aircraft Company in Greensboro, North Carolina. The HA-420 has been the most-delivered jet in its size class in recent years. Strategically, the aircraft business is not a major profit contributor, but it demonstrates that Honda can execute long-cycle, clean-sheet engineering programs — a credibility marker that is relevant when assessing the company’s ability to deliver its in-house EV architecture.

What happened with the Honda–Nissan merger talks?

Honda and Nissan publicly explored an integration under a new holding company starting in December 2024, with Mitsubishi Motors as a potential third party. The talks collapsed in February 2025 over disagreements on governance and equity terms. Honda has since signalled that it will pursue scale through narrower technology partnerships — including collaborations with Sony (Afeela), LG Energy Solution (batteries), and others — rather than full corporate integration. The two companies retain selective cooperation in specific technology areas.

Working with Honda and its supply ecosystem

For overseas suppliers, technology partners, and licensors, the practical entry points to Honda are diverse: powertrain components, battery materials, ADAS and software, lightweight materials, and aftermarket distribution for power products are all live engagement areas. Tier-1 qualification typically begins through Honda’s regional engineering centres in North America (Ohio), Europe (Frankfurt/Offenbach), and Asia rather than through Tokyo headquarters, with the exception of advanced R&D programs.

Beyond the corporate Tier-1 path, Honda’s broader supplier ecosystem — Hitachi Astemo, Musashi Seimitsu, F.C.C., Yutaka Giken, Showa, and dozens of independent component makers — is itself a substantial market for foreign component, materials, and software suppliers. Many of these companies operate outside the Anglophone industry press and are not easy to reach cold.

If your company supplies battery materials, power electronics, motor components, software, lightweight metals, or specialist services relevant to Honda’s transition — or if you are looking to license Japanese technology in motorcycles, power products, or robotics into your home market — Japonity’s business matching service can help structure a credible first conversation with the right counterparty in Japan.

Related from Japonity — Japan’s automakers

- Toyota Motor Corporation — Multi-pathway powertrain strategy from the world’s #1 automaker

- Nissan Motor — Post-Ghosn, post-Honda — what the Renault entanglement still means

- Mazda Motor Corporation — The Hiroshima underdog that bet on internal combustion

- Subaru Corporation — The boxer-engine niche player that built America

- Suzuki Motor — India’s market king — Maruti Suzuki’s ~40%+ share

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →