In January 2025, Koichi Minato — president of Fuji Television Network — bowed at a press conference and resigned. Within months, an independent committee would conclude that one of Japan’s most powerful commercial broadcasters had mishandled an allegation of sexual assault against superstar talent Masahiro Nakai, allowing internal hush-money mechanics to substitute for proper compliance. By April 2025, Fuji Media Holdings — the Tokyo-listed holding company (TSE: 4676) that sits over Fuji TV, Nippon Broadcasting System, and a roughly 30 percent stake in Sankei Shimbun — was facing the loudest activist campaign in Japanese media history, led by Dalton Investments, alongside engagements from Daniel Loeb’s Third Point and James Rosenwald’s Rising Sun Management. For foreign media-rights buyers, IP licensees, and broadcast partners, the question is no longer whether Fuji is a stable counterparty. It is whether the 2025 governance reset will finally unlock a balance sheet that has, for two decades, been more interesting than the prime-time schedule it funded.

From Daiba tower to holding company: the FCG architecture

Fuji Television Network was founded in 1957 and went on air in 1959, the latest of Tokyo’s five commercial keyhole broadcasters to launch. For four decades it operated as a single broadcasting company at the centre of the Fujisankei Communications Group (FCG) — a sprawling conglomerate identity that bound together broadcasting, print, radio, music, film and real estate under a shared editorial sensibility associated with the late chairman Nobutaka Shikanai and, from the 1980s onward, Hisashi Hieda. The group’s signature was its move in 1997 to a Kenzo Tange-designed headquarters in Tokyo’s Odaiba waterfront district, a futuristic silver-sphere building that became the literal and symbolic centre of Japanese commercial media at the peak of the post-bubble television economy.

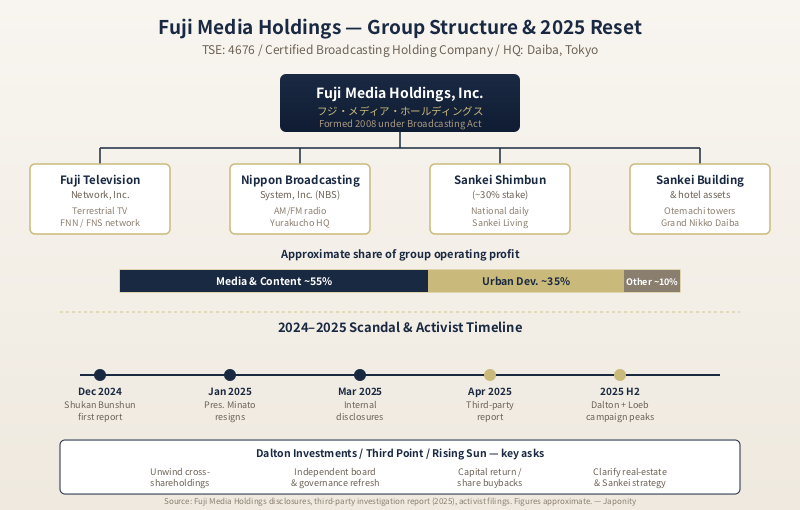

The legal structure that exists today, however, dates from October 2008. Following revisions to Japan’s Broadcasting Act that permitted “certified broadcasting holding companies” (認定放送持株会社), Fuji Television reorganised itself into Fuji Media Holdings, Inc., with the operating broadcaster spun out as a wholly owned subsidiary. The reform was designed to give Japanese broadcasters the corporate flexibility to diversify beyond the regulated terrestrial business while ring-fencing the broadcast licence. Fuji Media Holdings is now listed on the Tokyo Stock Exchange Prime market under code 4676; the operating broadcaster sits below it, alongside radio operator Nippon Broadcasting System (NBS, ニッポン放送), and the holding company maintains a strategic stake of approximately 30 percent in Sankei Shimbun, one of Japan’s five national daily newspapers.

Why Fuji mattered: the FNN/FNS network and the “Fuji decade”

To understand why the 2025 crisis was so consequential, it helps to remember what Fuji once was. Through the 1980s and again from 2004 to 2010, Fuji Television led Japan’s four commercial broadcasters in average-day household ratings — the so-called “three-crown” (三冠王) victories across all-day, prime, and golden-time blocks. Its national reach is organised through two affiliated networks: Fuji News Network (FNN), the news federation, and Fuji Network System (FNS), the programming federation, which together bind 28 regional terrestrial stations into a nationwide footprint covering essentially the entire Japanese population.

That footprint funded extraordinary programming production. Fuji’s variety, drama and animation divisions shaped a generation of Japanese popular culture; the broadcaster’s stakes in Pony Canyon (music and home video), Dinos Cecile (TV shopping), and the Sankei Building real-estate portfolio extended the franchise into adjacent rents. By the mid-2010s, however, Fuji’s ratings had collapsed to fourth place among the four commercial broadcasters, a position from which it has not meaningfully recovered. Younger viewers had migrated to streaming and YouTube; the company’s response — heavier reliance on the talent-agency system and an increasingly conservative editorial line — narrowed rather than widened the audience.

The balance-sheet story foreign investors actually care about

For a foreign analyst opening Fuji Media Holdings’ securities report, the surprising fact is not the broadcaster but the buildings. Approximately one-third of the group’s operating profit, in normal years, comes not from advertising but from the Sankei Building real-estate portfolio — office towers in central Tokyo, anchored by the headquarters block in Otemachi and the Daiba complex itself. Add the financial assets — listed cross-shareholdings, cash, and the Sankei Shimbun stake — and a substantial share of the group’s enterprise value sits outside the regulated broadcast business.

| Segment | Description | Approx. share of operating profit |

|---|---|---|

| Media & Content | Fuji TV terrestrial broadcasting, Nippon Broadcasting radio, FOD streaming, content licensing | ~55% |

| Urban Development & Tourism | Sankei Building portfolio, Grand Nikko Tokyo Daiba, Toei Hotel chain | ~35% |

| Other (advertising, IT, music, lifestyle) | Pony Canyon, Dinos Cecile, Kyodo Television, Sankei Living Newspapers | ~10% |

This mix is the entire investment case — and the entire activist case. Dalton Investments, the Los Angeles-based Japan specialist co-founded by James Rosenwald, has argued for years that Fuji Media Holdings trades at a persistent discount to the sum-of-its-parts value because the broadcasting franchise is a poor steward of the surrounding capital. Cross-shareholdings with banks, advertisers and group companies, in this view, lock up balance sheet without producing returns. By early 2025 — with the Nakai scandal exposing the governance weakness Dalton had long alleged — the activist case shifted from a niche valuation argument to a mainstream one.

The Nakai Masahiro scandal: anatomy of a governance failure

The crisis broke in late December 2024, when the weekly magazine Shukan Bunshun reported that Masahiro Nakai — the former SMAP member and one of Japan’s most bankable television talents — had sexually assaulted a woman in June 2023, and that Fuji Television Network had become entangled in the matter. Subsequent reporting and the eventual third-party investigation report established a sequence that would have been damaging for any broadcaster but was particularly so for Fuji given its long-standing dependence on the talent-agency relationships that underpinned its variety schedule.

According to the third-party committee’s report, published in late March / early April 2025, the woman had been introduced to Nakai in a context involving a Fuji Television employee; the alleged assault took place at Nakai’s residence; settlement was negotiated outside formal legal channels; and Fuji Television’s senior management was aware of the matter for an extended period without escalating it through the broadcaster’s compliance or HR functions, or to the holding-company board. The committee concluded that the broadcaster had failed in its duty of care to the woman, that its internal harassment-response architecture was inadequate, and that the failure reflected structural problems in the way Fuji managed talent and senior-producer power.

The corporate response was severe. Koichi Minato, president of Fuji Television Network, resigned in January 2025, as did Shuji Kano, the long-serving senior executive who personified the broadcaster’s relationship with the talent-agency system. Hisashi Hieda, then the eighty-eight-year-old chairman of Fuji Media Holdings and architect of the group’s modern structure, stepped down from his board roles. By March 2025, Fuji Television had disclosed an unusual level of internal information, including investigation findings and remediation plans. The April 2025 report itself — running to several hundred pages — became one of the most-cited corporate-governance documents in recent Japanese media history.

The broadcaster four-way: where Fuji now sits

The Nakai scandal arrived as Japan’s four commercial keyhole broadcasters were already diverging sharply. Nippon Television Holdings, owner of NTV and (since 2023) Studio Ghibli, had pulled clearly into first place on ratings, content equity, and digital strategy. TBS Holdings was monetising drama and anime IP aggressively through global streaming partnerships. TV Asahi, owner of perennially strong news and family-entertainment franchises, sat in stable third. Fuji had been fourth on ratings for most of the previous decade; what changed in 2025 was that it was also now fourth in trust.

| Group | TSE code | Operating broadcaster | Key holdings | 2024 prime-time rating rank |

|---|---|---|---|---|

| Nippon TV Holdings | 9404 | Nippon Television | Studio Ghibli, Tytan Hulu Japan stake, Yomiuri Shimbun ties | 1st |

| TBS Holdings | 9401 | Tokyo Broadcasting System | BS-TBS, Akasaka real estate, anime/drama IP, Tokyo Dome stake | 2nd |

| TV Asahi Holdings | 9409 | TV Asahi | Doraemon/Crayon Shin-chan franchises, Asahi Shimbun affiliation | 3rd |

| Fuji Media Holdings | 4676 | Fuji Television Network | Nippon Broadcasting, Sankei Shimbun stake, Sankei Building, Pony Canyon | 4th |

Among the four, Fuji is the most real-estate heavy, the most exposed to a single talent-agency model, and now the most contested at the shareholder register.

Dalton, Loeb, Rosenwald: the activist coalition

Dalton Investments’ campaign on Fuji Media Holdings pre-dates the Nakai scandal — Dalton had been a holder for years and had publicly questioned cross-shareholdings and capital allocation since at least 2023. What 2025 produced was a coalition. Daniel Loeb’s Third Point disclosed a stake; Rising Sun Management, a Dalton spin-off vehicle run by James Rosenwald, intensified public engagement; and several domestic Japanese institutional investors, traditionally quiet, began voting against management resolutions at shareholder meetings.

The activist asks have been unusually specific. First, the unwinding of cross-shareholdings — the legacy stakes Fuji holds in domestic listed companies and that those companies hold in Fuji — which Dalton estimates locks up tens of billions of yen of unproductive capital. Second, governance reform at the holding-company level, including more genuinely independent directors and a clearer separation between the operating broadcaster and the asset-rich holding company. Third, capital return — share buybacks funded from the financial-asset stack rather than from broadcasting cash flow. Fourth, strategic clarity on the Sankei Shimbun stake, the Daiba hotel assets, and the real-estate portfolio, all of which sit awkwardly inside a “certified broadcasting holding company” structure.

Fuji Media Holdings’ response through 2025 has been the most accommodative posture the group has shown in its history. Cross-shareholding reductions have been announced; a new chairman and president have committed publicly to capital-efficiency targets; the third-party investigation’s recommendations have been adopted in their entirety; and the holding-company board has been refreshed.

What the reset means for foreign partners

For foreign media-rights buyers, IP licensees and broadcast-format partners, the practical question is whether 2025 changes the way Fuji does business. On the evidence so far, the answer is: yes, slowly, and in ways that foreign counterparties should welcome.

First, the talent-agency dependency that produced the Nakai failure is being unwound. Fuji has publicly committed to direct-with-individual contracts, more robust harassment-response procedures, and a reduced reliance on a small group of legacy talent houses. For overseas format owners and rights agents, this should mean clearer counterparty signatures, faster decision cycles, and a lower risk that a deal is held hostage to a single agency relationship.

Second, the content-licensing function is being professionalised. Fuji’s drama and animation catalogues — historically licensed in opaque bundles to regional Asian broadcasters — are being repositioned for global streaming buyers. The group’s animation production stakes, music rights through Pony Canyon, and theatrical co-financing arrangements all become more accessible as the holding company is pushed toward transparent capital allocation.

Third, the real-estate side of the group is, for the first time, openly discussable. The Daiba hotel complex, the Sankei Building portfolio in Otemachi, and the group’s tourism assets are the kind of holdings that Western hospitality and real-estate investors have been seeking exposure to in Japan’s reflation cycle. A Fuji that treats these as strategic — rather than as ballast for the broadcaster — opens partnership conversations that simply could not happen in 2023.

The risks that remain

Three risks deserve attention. The first is regulatory: as a certified broadcasting holding company, Fuji Media Holdings is subject to foreign-ownership caps and structural constraints under the Broadcasting Act. Any radical separation of the real-estate and broadcasting businesses would require regulatory navigation and political handling. The second is editorial: the Sankei Shimbun affiliation gives the group a distinctive conservative editorial voice that some advertisers and international partners find awkward, and the activist campaign has not directly addressed the Sankei relationship. The third is execution: governance announcements are easier than governance follow-through, and the Japanese activist record is mixed. Whether the 2025 reset produces durable change or reverts to the institutional defaults that produced the Nakai failure is, ultimately, the question on which foreign partners will judge the next three years.

FAQ

Is Fuji Media Holdings the same company as Fuji Television?

Fuji Media Holdings, Inc. (TSE: 4676) is the listed certified broadcasting holding company formed in 2008. Fuji Television Network, Inc. is the operating terrestrial broadcaster sitting below it as a wholly owned subsidiary. The group also includes Nippon Broadcasting System (radio), a stake of approximately 30 percent in Sankei Shimbun, the Sankei Building real-estate portfolio, Pony Canyon, and several hotel assets.

What exactly was the Nakai Masahiro scandal?

In December 2024, weekly magazine reporting alleged that television talent Masahiro Nakai had sexually assaulted a woman in June 2023, and that Fuji Television had been entangled in the matter, including through a Fuji employee’s involvement in the introduction and handling. A third-party investigation report published in spring 2025 concluded that the broadcaster had failed in its duty of care and had structural weaknesses in harassment response. Fuji TV president Koichi Minato resigned in January 2025; chairman Hisashi Hieda stepped down; remediation measures were adopted.

Who is Dalton Investments and what are they asking for?

Dalton Investments is a Los Angeles-based asset manager specialising in Japan, co-founded by James Rosenwald. Together with engagement from Daniel Loeb’s Third Point and Rosenwald’s Rising Sun Management vehicle, Dalton has pressed Fuji Media Holdings to unwind cross-shareholdings, refresh governance, return capital to shareholders, and clarify strategy on the Sankei Shimbun stake, the Daiba hotels, and the Sankei Building real-estate portfolio.

Why does a TV broadcaster own so much real estate?

The Sankei Building was a core asset of the Fujisankei group long before the 2008 holding-company restructuring; central-Tokyo office and hotel real estate has historically been treated as strategic balance sheet for the group. In recent years it has come to represent approximately one-third of operating profit — a structural feature that is now central to the activist case for separation or restructuring.

What does this mean for licensing Fuji content overseas?

The 2025 reset is pushing Fuji’s content licensing toward professionalised, transparent, direct-with-buyer relationships. Drama, animation, and music rights — historically bundled through legacy intermediaries — are being repositioned for global streaming buyers and format partners. Foreign buyers should expect clearer counterparty processes and reduced friction from talent-agency intermediation.

Working with Fuji Media Holdings

Japonity supports overseas media-rights buyers, format licensees, real-estate co-investors, and IP partners exploring engagements with Fuji Media Holdings and other Japanese broadcasting groups. We can help frame the right counterparty within the group structure, brief on the post-2025 governance environment, and arrange introductions through appropriate channels. Start a conversation with our business-matching team to discuss a Fuji-related partnership, licensing deal, or co-investment idea.

Related from Japonity — Japan’s media & broadcasting

- Nikkei Inc. — Japan’s $1.3B Financial Times-owning newspaper

- The Asahi Shimbun Company — Japan’s #2 newspaper and the politicized media question

- The Yomiuri Shimbun — Japan’s #1 newspaper by circulation — the conservative-establishment paper

- Nippon Television Holdings — Japan’s #1 commercial broadcaster + Studio Ghibli + Hulu Japan

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →