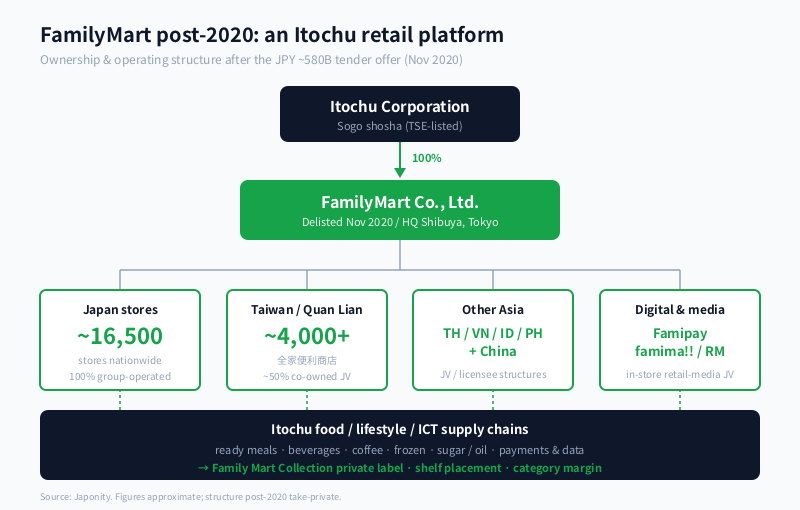

In November 2020, Itochu Corporation completed a tender offer that took FamilyMart Co., Ltd. private at approximately JPY 580 billion, ending the convenience-store chain’s listing on the Tokyo Stock Exchange and folding Japan’s number-two konbini operator — approximately 16,500 stores at home, more than 4,000 across Taiwan via Quan Lian (全家便利商店), and several thousand more from Thailand to Indonesia — fully inside the trading house. The deal was not a rescue. It was a strategic re-architecture: the moment a sogo shosha decided it would rather own the last mile to 15 million Japanese consumers a day than supply it from a distance. Five years on, that bet is reshaping how konbini buy, brand, and bargain.

The Itochu konbini: what the 2020 take-private actually changed

FamilyMart was founded in 1973 inside the Saison Group as an experimental store under Seiyu, spun out as an independent company in 1981, and built up over four decades into Japan’s second-largest convenience-store chain. For most of that history, Itochu was a major shareholder and merchandising partner — first a minority investor, then a roughly 50% owner after the 2016–2018 merger with UNY Group Holdings consolidated the Circle K Sunkus brand into FamilyMart’s network. What changed in 2020 was the elimination of every other public shareholder.

Taking the company off the exchange did three things at once. It removed the quarterly-earnings drag on long-cycle investments — Itochu can now fund private-label R&D, store renovations and overseas expansion without optimising for a TSE narrative. It collapsed the negotiation interface between the trading house’s vast food, textile and energy supply chains and the konbini’s roughly 16,500 retail end-points, allowing transfer pricing, joint procurement and category strategy to be set inside one P&L. And it gave Itochu unilateral control over the most valuable behavioural data set in Japanese physical retail: tens of millions of daily transactions, ticket-by-ticket, weighted heavily towards urban office-worker and convenience-driven consumption that complements e-commerce rather than competes head-on with it.

For foreign brands, licensors and investors trying to read the konbini sector, the practical implication is blunt: FamilyMart is no longer a publicly listed retailer that happens to have a shosha shareholder. It is a wholly-owned Itochu retail platform that happens to operate konbini.

From Seiyu side-project to Japan’s #2 konbini chain

The chain’s founding story is a useful corrective to the assumption that Japan’s konbini sector was always a three-way race. FamilyMart began as a single experimental store opened by Seiyu Stores in Sayama City, Saitama Prefecture in 1973 — the same year Ito-Yokado signed its area licence with Southland for 7-Eleven. For most of the 1970s, FamilyMart was a Seiyu side-project; the standalone operating company that became today’s FamilyMart Co., Ltd. was incorporated in 1981, and the chain spent the 1980s and 1990s scaling under the Saison Group’s distinctive lifestyle-retail philosophy.

The shift towards Itochu accelerated in the 1990s and 2000s as Saison’s broader empire unwound. Itochu progressively raised its stake, becoming the dominant shareholder and aligning FamilyMart with its food-and-distribution business unit. The defining structural move came in 2016, when FamilyMart agreed to merge with UNY Group Holdings, parent of Circle K Sunkus — at the time Japan’s number-three konbini brand. By 2018, the Circle K Sunkus banner had been fully retired and roughly 5,000 stores converted to FamilyMart colours, lifting the chain past Lawson and consolidating the konbini market into the structure recognisable today.

Headquartered in Shibuya, Tokyo, the company under chief executive Kensuke Hosomi (subject to verification against the latest corporate disclosure) now runs the chain as a wholly-owned subsidiary of Itochu, with separately governed but operationally integrated joint ventures across Asia.

Konbini, compared: FamilyMart against 7-Eleven Japan and Lawson

The Japanese convenience-store sector is often described as a triopoly, but the three chains are structurally very different. 7-Eleven Japan sits inside Seven & i Holdings, a listed retail conglomerate that also owns Ito-Yokado and the global 7-Eleven brand. Lawson is majority-owned by Mitsubishi Corporation, with KDDI taking an additional stake to push telecom-retail convergence. FamilyMart is the only one of the three that has been fully delisted and folded into a single sogo shosha parent.

| Indicator | FamilyMart | 7-Eleven Japan | Lawson |

|---|---|---|---|

| Approx. stores in Japan | ~16,500 | ~21,000 | ~14,600 |

| Parent / control | Itochu Corporation (100%) | Seven & i Holdings (listed) | Mitsubishi Corp. + KDDI |

| Listing status | Delisted 2020 | Parent listed (TSE) | Listed (TSE) |

| Flagship private label | Family Mart Collection / Famima Premium | Seven Premium | Lawson Select / Natural Lawson |

| Headline overseas market | Taiwan (~4,000+ stores via Quan Lian) | U.S. (7-Eleven Inc., via parent) | China (Lawson China) |

| Strategic posture | Shosha-integrated retail platform | Global konbini operator | Telecom-retail convergence |

The differences matter for anyone selling into the channel. 7-Eleven Japan negotiates with the discipline of a listed retailer reporting to global shareholders. Lawson increasingly thinks like a telco about loyalty, data and bundling. FamilyMart negotiates with the deep, often patient capital and category logic of a trading house that owns the upstream supply chains feeding its own shelves.

The shosha-konbini loop: vertical integration as competitive moat

The clearest expression of FamilyMart’s post-2020 strategy is the tightening of the loop between Itochu’s upstream businesses and the konbini’s downstream shelves. Itochu’s food division already controls significant capacity in ready-meal manufacturing, beverage importing, frozen food, coffee, sugar and oil. Several of those flows now run preferentially through FamilyMart’s distribution centres, with category margins captured at multiple points along the chain rather than being negotiated away to external suppliers.

The Family Mart Collection (ファミリーマートコレクション) private-label programme, relaunched and expanded under Itochu’s full ownership, is the visible front-end of that integration. Where Seven Premium has historically been positioned as a quality-led national-brand alternative, Family Mart Collection has leaned harder into Itochu-sourced ingredients and supplier relationships, with selected SKUs functioning as a showcase for the trading house’s regional Japan and Asian sourcing capabilities. For foreign food and beverage exporters, the implication is that the conversation about FamilyMart shelves can begin with Itochu’s food division long before it reaches the konbini’s category buyers.

famima!!, Famipay and the digital retail stack

The second pillar of post-2020 strategy is digital. FamilyMart’s famima!! app, Famipay digital wallet and integrations with carrier and platform partners (NTT Docomo, KDDI’s au PAY, and others) form a loyalty and payments layer designed to keep customers inside the FamilyMart ecosystem across both physical visits and adjacent services — from utility bill payments to e-commerce pickup. The strategic objective is recognisable from telco and platform playbooks: turn a high-frequency, low-ticket retail interaction into a recurring digital relationship that yields behavioural data and cross-sell opportunities.

That data, importantly, is now exclusively Itochu’s. There is no minority shareholder to share it with, no quarterly market narrative to justify monetisation strategy against. FamilyMart can — and increasingly does — run experiments in dynamic pricing, AI-driven demand forecasting and in-store digital signage that would be slower to authorise inside a listed holding company. A widely publicised in-store advertising-media joint venture has positioned FamilyMart’s store-network screens as a retail-media inventory pool, monetising attention in the same way platform companies monetise digital ad space.

Taiwan FamilyMart and the Asian flank

The overseas story is dominated, by a wide margin, by Taiwan. Taiwan FamilyMart — locally known as Quan Lian (全家便利商店) — is the island’s second-largest convenience-store chain after 7-Eleven Taiwan, with more than 4,000 stores and a co-ownership structure in which FamilyMart Co., Ltd. holds roughly half of the equity alongside Taiwanese partners. Quan Lian is widely regarded as one of the most innovative convenience-store operators in Asia, with leading positions in fresh coffee, ready meals, frozen food vending and in-store digital experimentation. Several concepts later adopted by FamilyMart Japan — including aspects of the Famipresso fresh-coffee programme — originated or were refined in Taiwan.

Beyond Taiwan, FamilyMart operates or licenses stores across Thailand, China, Vietnam, Indonesia, the Philippines and Malaysia, with mixed performance. Some markets have grown steadily; others have been restructured or partially divested in favour of stronger local partners. The portfolio collectively positions FamilyMart as one of the most pan-Asian convenience-store brands operating today, second in geographic reach only to 7-Eleven globally.

| Segment | Brand / vehicle | Approx. footprint | Ownership posture |

|---|---|---|---|

| Japan stores | FamilyMart | ~16,500 stores | 100% Itochu |

| Taiwan | Quan Lian (全家) | ~4,000+ stores | ~50% co-owned with local partners |

| Southeast Asia | FamilyMart (Thailand / Vietnam / Indonesia / Philippines) | Several hundred to low thousands by market | JV / licensee structures |

| China | FamilyMart China | ~1,500+ stores (selected cities) | JV / licensee, periodically restructured |

| Retail-media & digital | Famipay / in-store media JV | Network-wide | Group-controlled platforms |

Why this matters for foreign buyers, licensors and investors

For foreign companies, FamilyMart’s post-2020 structure changes the practical playbook in three ways. First, listing on FamilyMart shelves is increasingly inseparable from a conversation with Itochu’s relevant business unit — food, lifestyle, ICT or general products. The shosha is not a passive shareholder; in many categories it is effectively the gatekeeper. Foreign brands that approach the konbini cold without an Itochu-side relationship often find the dialogue moves slowly.

Second, the Taiwan flank offers an underused entry point. Quan Lian has historically been more open to experimental SKUs, regional partnerships and overseas brand pilots than FamilyMart Japan, and successful Taiwan rollouts can become useful proof points when re-pitching to Tokyo headquarters. For Asia-focused brands, Quan Lian deserves to be treated as a peer entity to FamilyMart Japan rather than a satellite.

Third, the take-private has changed how FamilyMart partners with platform and telecom players. Without minority-shareholder gravity, the company can write longer, deeper and more exclusive contracts on payments, advertising and data — but it can also choose to bring those capabilities in-house. Foreign fintech, ad-tech and AI vendors selling into FamilyMart should expect a “build, partner or buy” decision that defaults more often to “build inside Itochu” than it did before 2020.

The strategic question for the next five years

The interesting unknowns sit at three frontiers. The first is whether the Itochu integration ultimately produces a step-change in private-label penetration and category margin, or whether the shosha discount on retail execution closes against more disciplined operators like 7-Eleven Japan. The second is whether Taiwan-style innovation can be reliably exported back to Japan — particularly in store automation, fresh food and digital experience — at a pace that compensates for Japan’s flat population. The third is whether FamilyMart’s retail-media and Famipay layers can credibly compete with platform-scale digital ad and payments incumbents, or whether they remain accessory businesses to the physical store network.

None of these questions are settled. What is settled is the corporate structure under which they will be answered: FamilyMart will face them as an Itochu subsidiary, not as a listed konbini. That is the lens through which every supplier conversation, every digital partnership and every overseas pilot should now be read.

FAQ

Is FamilyMart still a public company?

No. FamilyMart was delisted from the Tokyo Stock Exchange in November 2020 after Itochu Corporation completed a tender offer that took the company 100% private at approximately JPY 580 billion in aggregate. It now operates as a wholly-owned subsidiary of Itochu.

How does FamilyMart compare in size to 7-Eleven Japan and Lawson?

FamilyMart operates approximately 16,500 stores in Japan, placing it second behind 7-Eleven Japan (approximately 21,000 stores) and ahead of Lawson (approximately 14,600 stores). All three figures fluctuate quarter to quarter; “approximately” should be taken seriously.

What is the relationship between FamilyMart and Taiwan’s Quan Lian (全家)?

Quan Lian is Taiwan’s number-two convenience-store chain, operating more than 4,000 stores under the FamilyMart brand. FamilyMart Co., Ltd. holds roughly 50% of the equity alongside Taiwanese partners. Quan Lian is widely regarded as one of the most operationally innovative konbini operators in Asia.

How do foreign brands get listed on FamilyMart shelves?

The most reliable path increasingly runs through Itochu Corporation’s relevant business division (food, lifestyle, ICT or general products) rather than direct outreach to FamilyMart’s category buyers alone. Pilot programmes, regional rollouts and Taiwan-first launches via Quan Lian are common bridging strategies.

What is Famipay and how does it fit into FamilyMart’s strategy?

Famipay is FamilyMart’s proprietary digital wallet and loyalty layer, integrated with the famima!! app and partner payment systems. It is the principal vehicle through which FamilyMart converts high-frequency physical retail interactions into a recurring digital customer relationship and behavioural data set.

Working with FamilyMart

If you are a foreign brand, distributor, licensor or investor looking to engage FamilyMart or its Itochu parent — whether for shelf placement, private-label supply, Taiwan-first pilots through Quan Lian, retail-media partnerships or M&A discussions — Japonity helps structure the introduction. Start with our Business Matching service to map the right counterparties inside the FamilyMart and Itochu retail ecosystem.

Related from Japonity — Japan’s convenience-store chains

- Seven & i Holdings — The convenience-store empire targeted by Couche-Tard

- Lawson — The konbini now jointly owned by Mitsubishi Corp and KDDI

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →