In July 2021, Sumitomo Mitsui Financial Group announced a strategic alliance with Jefferies Financial Group — a New York mid-market investment bank that, in Wall Street’s old hierarchy, was nobody’s idea of a marquee partner. Four years later, that judgment looks wrong. SMFG has stepped up its stake in Jefferies to roughly 15% or more, the two firms run a joint leveraged finance and M&A platform across the U.S. and Europe, and Jefferies has emerged as one of the fastest-growing investment banks of the cycle. The alliance is the lens for reading modern SMFG: not Japan’s biggest bank, but its most commercially restless — the megabank that bought a 96% stake in Indonesia’s Bank BTPN (rebranded SMBC Indonesia), backed Vietnam’s FE Credit, partnered with India’s Mahindra Finance, and chose Jefferies rather than chase a Morgan Stanley equivalent it could never have. SMFG built its global strategy by being the second-biggest in everything — and treating that as freedom rather than constraint.

The bank built from two trading houses

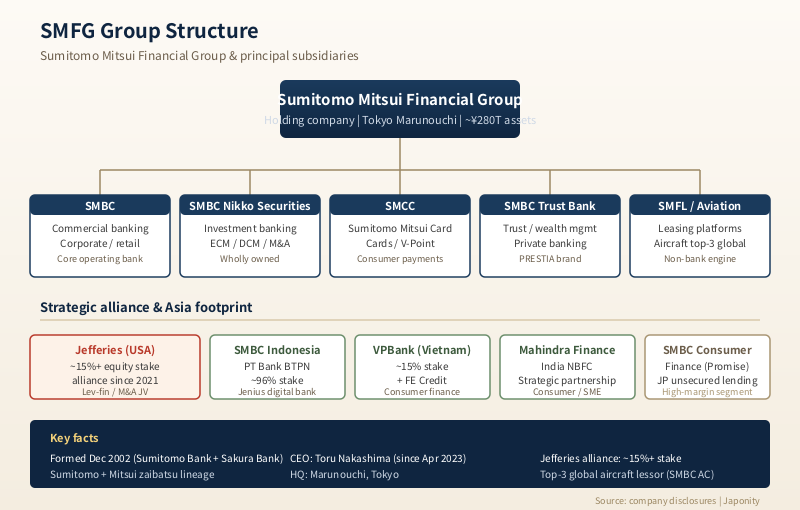

Sumitomo Mitsui Financial Group, known in the markets as SMFG and operating under the SMBC brand, was formed in December 2002 through the merger of Sumitomo Bank and Sakura Bank — the latter itself the product of an earlier merger between Mitsui Taiyo Kobe Bank, which carried the Mitsui zaibatsu lineage. The genealogy matters. Both Sumitomo and Mitsui were among the four pre-war zaibatsu, the diversified industrial-financial conglomerates that dominated the Japanese economy until the U.S. occupation broke them up in 1945. The post-war reassembly into looser keiretsu kept the bank at the centre of each group; the 2002 merger fused two of those centres into one. The result is a megabank whose corporate book reads as a Who’s Who of the Sumitomo and Mitsui groups — Sumitomo Corporation, Sumitomo Mitsui Trust, Mitsui & Co., Mitsui Fudosan, Toyota’s banking partner choices — and a culture descended from the two most commercially aggressive of Japan’s old trading-house cultures.

That culture is the operating signature of the bank. Of the three megabanks, SMFG is the one most willing to take a risk-weighted position, to underwrite a leveraged transaction without a syndicate already in place, to enter a new geography before the macro consensus arrives. Inside Japanese finance it is sometimes called the most “trading-house-like” of the megabanks — a compliment in some quarters, a warning in others. Foreign counterparties evaluating Japanese megabanks usually discover this difference the third time they ask SMFG for a commitment that MUFG or Mizuho have already declined, and find SMBC saying yes — at a price, but yes.

The group structure: holdco, bank, broker, card, leasing

SMFG is the listed holding company; the operating businesses sit underneath it in a structure that mirrors Japan’s segmented financial regulation. Sumitomo Mitsui Banking Corporation (SMBC) is the commercial banking arm and by far the largest entity, headquartered in Marunouchi, Tokyo. SMBC Nikko Securities is the wholly owned investment bank and brokerage — rebuilding from a 2022 stock-price manipulation scandal. Sumitomo Mitsui Card Company (SMCC) anchors the group’s consumer payments franchise. SMBC Trust Bank is the smaller trust-banking arm, focused on private banking and wealth management. SMBC Aviation Capital and Sumitomo Mitsui Finance & Leasing (SMFL) are the leasing platforms, with SMBC Aviation Capital ranking as one of the world’s three largest aircraft lessors.

Around this core sits an expanding ring of regional subsidiaries: SMBC Indonesia (PT Bank BTPN), in which SMFG holds approximately 96% or more; minority stakes in Vietnam’s VPBank at approximately 15%; FE Credit in Vietnam; the Mahindra Finance partnership in India; and a network of branches and JVs across the rest of Southeast Asia. Each is a separately licensed entity, and getting the entity right is the difference between a clean execution and a long approval cycle.

How the three megabanks actually compare

For foreign capital, the practical question is which Japanese megabank to choose for which product. The three are often treated as interchangeable; they are not.

| Dimension | MUFG | SMFG | Mizuho |

|---|---|---|---|

| Total assets (approx.) | ¥400+ trillion | ¥280 trillion | ¥260 trillion |

| Heritage | Mitsubishi (incl. UFJ / Tokai) | Sumitomo + Mitsui (via Sakura) | Fuyo + DKB + IBJ |

| U.S. IB partner | Morgan Stanley (~21% stake, since 2008) | Jefferies (~15%+ stake, since 2021) | None — owns Greenhill |

| Securities arm | JV with Morgan Stanley | SMBC Nikko (wholly owned) | Mizuho Securities (wholly owned) |

| ASEAN consumer-bank footprint | Krungsri (TH), Danamon (ID) | SMBC Indonesia (BTPN), VPBank (VN), FE Credit (VN) | Limited — corporate-led |

| Aircraft leasing | Smaller platform | SMBC Aviation Capital (top-3 globally) | Limited |

| Reputation with foreign sponsors | Conservative blue-chip | Aggressive, deal-hungry, leveraged finance-friendly | Process-heavy, broad coverage |

The differences are real and decision-relevant. MUFG’s signature is scale and conservatism. SMFG’s signature is commercial aggression and a non-bank franchise — leasing, consumer finance, card — that contributes a disproportionately large share of profit relative to the size of its banking balance sheet. Mizuho’s signature is broad corporate coverage with operational fragility that has cost it credibility on multiple occasions, most recently in a series of 2021–2022 IT system outages.

The Jefferies trade, and why it matters

The Morgan Stanley deal cast a long shadow. MUFG’s 2008 investment was a generational counter-cyclical bet that compounded into the most valuable single relationship in Japanese finance. SMFG spent more than a decade looking for a comparable partner and not finding one — Goldman Sachs was independent, JPMorgan was uninterested, Morgan Stanley was taken. The Jefferies alliance, announced in July 2021 with an initial $1.5 billion-plus investment commitment, was a different kind of trade. Jefferies in 2021 was a mid-market house with a strong leveraged finance franchise, a respected M&A advisory business in the middle market, and — crucially — an appetite to grow into the bulge-bracket space being vacated by European banks (Deutsche, Credit Suisse) retrenching from U.S. investment banking.

SMFG’s commitment grew over subsequent tranches. By late 2024 and into 2025, the stake had risen into the mid-teens, with an announced ceiling allowing further accumulation subject to regulatory approval. The two firms jointly cover leveraged finance in the U.S. and Europe, coordinate cross-border Japan-U.S. M&A, and share loan distribution. For Jefferies, the alliance gives access to SMBC’s balance sheet and a deep Japanese corporate client base. For SMFG, it gives U.S. capital markets distribution, a mid-market deal pipeline that fits the bank’s risk appetite, and an equity stake that — like MUFG/Morgan Stanley — generates equity-method earnings.

The trade differs from MUFG/Morgan Stanley in two ways. Jefferies is smaller and more leveraged-finance-tilted, concentrating the alliance in sponsor coverage and credit rather than spreading across equities, wealth and FICC. And Jefferies is run by founder-CEO Richard Handler with an owner-operator mentality, making the relationship more transactional than institutional. In a credit-friendly environment, SMFG/Jefferies is one of the most productive franchises in cross-border finance; in a credit downturn, the concentration becomes a vulnerability.

The SMBC Nikko stock-manipulation scandal and the aftermath

The other defining episode of modern SMFG is the SMBC Nikko stock-price manipulation case. In 2022, Tokyo prosecutors indicted SMBC Nikko Securities and several senior employees, including a former vice-chairman, for alleged market manipulation in block-offering transactions — placing orders to support the share price of specific stocks ahead of secondary offerings. The case produced criminal convictions, leadership changes, FSA penalties, and a significant reputational drag on what had been one of Japan’s leading ECM houses.

For SMFG, the scandal has had three durable effects: lost market share in domestic ECM (picked up by Nomura and Mizuho Securities); a wave of compliance-driven hiring and additional pre-trade controls; and a reinforcement of the strategic logic of the Jefferies alliance, since cross-border M&A involving U.S. counterparties now runs through Jefferies rather than SMBC Nikko. By 2025, Nikko had recovered a portion of its lost share, but the case is the kind of episode that takes a decade to fade from institutional memory.

The ASEAN consumer-finance push

Where MUFG built an ASEAN footprint by buying mid-sized commercial banks (Krungsri in Thailand, Danamon in Indonesia), SMFG took a different route: it leaned into consumer finance and digital banking, on the bet that Southeast Asia’s under-banked retail customer is the higher-margin and faster-growing prize.

The anchor asset is SMBC Indonesia — PT Bank BTPN — in which SMFG accumulated a roughly 96% stake through a multi-stage acquisition completed in the late 2010s. BTPN had a distinctive history as a pension-payment bank serving Indonesia’s retired civil servants, and SMFG built on that base with a digital-banking subsidiary (Jenius) targeted at younger urban customers. In Vietnam, SMBC took an approximately 15% strategic stake in VPBank and separately acquired a substantial position in FE Credit, one of Vietnam’s largest unsecured-consumer lenders. In India, SMFG partnered with Mahindra Finance for consumer and SME lending. The strategic frame is consistent: Japanese yen funding through the parent, deployed via local subsidiaries into local-currency credit, capturing margins no domestic Japanese deployment can match.

The risks are higher. Consumer finance in emerging Asia is structurally exposed to local credit cycles, currency volatility, and regulatory tightening around interest-rate caps. FE Credit in particular has been through a difficult post-pandemic credit cycle, with elevated provisions weighing on returns. The ASEAN earnings contribution carries a wider variance band than the domestic Japanese book, even if the through-the-cycle return is higher.

The non-bank engine: leasing, cards, consumer finance

Strip out the commercial bank and SMFG still has one of the largest non-bank financial franchises in Asia. SMBC Aviation Capital is a top-three global aircraft lessor with a fleet valued in the tens of billions of dollars — the legacy of a 2012 acquisition from RBS at the bottom of the post-crisis leasing cycle. SMFL is the diversified equipment-leasing platform spanning real estate, equipment and structured finance. Sumitomo Mitsui Card Company anchors the V-Point loyalty programme and retailer partnerships, and SMBC Consumer Finance (formerly Promise) handles unsecured consumer lending. Together, these non-bank businesses contribute a share of group pre-tax profit that in good years rivals the domestic commercial bank — a structural feature that differentiates SMFG from MUFG and Mizuho, where the commercial bank dominates the segment mix.

BOJ normalisation and the SMFG earnings algorithm

The BOJ’s exit from yield curve control and negative rates, formalised in 2024 and continuing into 2026, has been the most important macro tailwind for Japanese megabanks in a generation. Roughly half of SMBC’s domestic loan book reprices to short-term yen rates within a year, while household deposit costs reprice very slowly — the standard megabank arithmetic. A sustained 50–100bp rise in short rates would add several hundred billion yen to SMFG’s net interest income annually.

What distinguishes SMFG is the non-bank profit base. Because leasing, cards and consumer finance contribute such a large share of group earnings, overall sensitivity to BOJ rates is somewhat lower than MUFG’s in percentage terms, but the absolute contribution is still material. The offsetting drag is the JGB portfolio, where mark-to-market losses on the AFS book have been significant; SMFG has been shortening duration but the legacy book will take years to roll off. On net, normalisation is accretive to SMFG earnings power, with the non-bank franchise providing stability through the transition.

What foreign counterparties actually get from SMFG

“Working with SMFG” means engaging different entities by product. Foreign IB partners — most importantly Jefferies — engage SMBC’s leveraged finance and corporate banking teams in New York, London and Tokyo. Foreign sponsors seeking committed financing for Japan-outbound or inbound deals usually find SMBC the most willing of the three megabanks to take initial underwriting risk, especially in sponsor-led LBOs.

For Southeast Asian operators, SMFG offers a consumer-credit footprint no other Japanese bank can match. A multinational building distribution in Indonesia, Vietnam or India can use SMBC Indonesia, VPBank or the Mahindra Finance partnership for local-currency working capital and trade finance in ways MUFG’s commercial-bank-led ASEAN strategy cannot easily replicate. For aircraft lessors and airline treasurers, SMBC Aviation Capital and SMFL provide one of the deepest sources of operating-lease finance globally. For foreign card-issuers entering Japan, Sumitomo Mitsui Card Company is one of the two natural domestic partners (the other being MUFG NICOS).

The institutional culture, briefly

SMFG’s culture, descended from the two most commercially aggressive of Japan’s old trading-house lineages, prizes speed, deal completion and willingness to take risk on a single transaction. Of the three megabank CEOs, Toru Nakashima — who took over as group CEO in April 2023 after succeeding Jun Ohta — has been the most willing to articulate an explicit strategy of differentiation through the non-bank franchise and through the Jefferies alliance, rather than competing head-to-head with MUFG on scale or with Mizuho on coverage breadth. The internal slogan is roughly that SMFG should be “the most chosen financial group” — a careful phrasing that does not promise to be the largest.

For foreign counterparties, this culture is both feature and risk. SMBC will say yes faster, take on a complex transaction earlier, and underwrite a larger initial commitment than its peers. But the bank’s risk appetite has occasionally cost it — the SMBC Nikko scandal being the obvious case — and counterparties should price a higher variance of outcomes than they would expect from MUFG. Firms that value speed often prefer SMFG; those that prize predictability default to MUFG.

FAQ

How is SMFG structured, and which entity should I actually engage?

SMFG is a financial holding company with several principal operating subsidiaries: Sumitomo Mitsui Banking Corporation (SMBC) for commercial banking, SMBC Nikko Securities for domestic investment banking and brokerage, Sumitomo Mitsui Card Company (SMCC) for credit cards and consumer payments, SMBC Trust Bank for trust and wealth management, SMBC Aviation Capital for aircraft leasing, and Sumitomo Mitsui Finance & Leasing (SMFL) for equipment leasing and structured finance. Regional subsidiaries include SMBC Indonesia (BTPN), and stakes in VPBank and FE Credit in Vietnam and Mahindra Finance in India. The right entity depends on the product: lending and trade finance go through SMBC; equity and debt underwriting in Japan go through SMBC Nikko; sponsor finance and U.S. cross-border deals are typically run jointly with Jefferies; consumer and SME credit in Southeast Asia goes through the local subsidiaries.

What exactly is the Jefferies relationship today?

SMFG announced an initial strategic alliance with Jefferies Financial Group in July 2021 with a commitment of approximately $1.5 billion-plus, and has since stepped up its equity stake in tranches to approximately 15% or more, subject to regulatory approval for further accumulation. The two firms jointly cover leveraged finance and M&A in the U.S. and Europe, share loan distribution, and coordinate on cross-border Japan-U.S. transactions. The stake is accounted for under the equity method, so a proportional share of Jefferies’ earnings flows to SMFG’s income statement. The alliance is structurally narrower than MUFG’s relationship with Morgan Stanley — concentrated in leveraged finance and sponsor coverage rather than spread across equities, FICC and wealth — but in those concentrated areas it has become one of the most productive franchises in cross-border investment banking.

Why did SMBC choose Jefferies rather than a bulge-bracket partner?

The bulge-bracket banks were either independent (Goldman Sachs), uninterested (JPMorgan), or already partnered (Morgan Stanley with MUFG) by the time SMFG was looking for a U.S. investment banking ally. Jefferies offered something the bulge brackets could not: an owner-operator culture, a leveraged finance franchise that fit SMBC’s risk appetite, and a willingness to share economics and decision-making in a way that a bulge-bracket would not. The trade has been validated by Jefferies’ growth into a top-five investment bank in several U.S. league tables over the alliance period.

Is the SMBC Nikko stock-manipulation scandal still a live risk?

The criminal cases have largely concluded, with convictions and penalties imposed, and SMBC Nikko has rebuilt its compliance infrastructure. The reputational drag in domestic ECM has eased but not fully disappeared — Nomura and Mizuho Securities still pick up a share of mandates that would historically have defaulted to Nikko. For foreign counterparties evaluating SMBC Nikko as a Japan equity execution partner, the firm is operationally sound today, but the case remains a useful reminder that the SMFG group’s commercial-aggression culture carries downside variance as well as upside.

How does SMFG’s ASEAN strategy compare to MUFG’s?

MUFG built its ASEAN footprint primarily through mid-sized commercial bank acquisitions (Krungsri in Thailand, Danamon in Indonesia), aiming for share of the local commercial-banking market. SMFG focused on consumer finance and digital banking (BTPN/SMBC Indonesia, FE Credit, VPBank, Mahindra Finance), aiming for higher-margin unsecured consumer credit. Both strategies are defensible; they reflect different risk-return profiles. MUFG’s strategy is more conservative and steadier; SMFG’s strategy has higher upside but more cyclicality, as the FE Credit experience in post-pandemic Vietnam has illustrated.

Working with SMFG

For foreign investment banks, sponsor financiers, asset managers, corporates and SE-Asia operators evaluating Japanese counterparties, SMFG is the megabank that combines a meaningful balance sheet with the most commercially aggressive culture and the deepest non-bank franchise. The Jefferies alliance has changed the global investment-banking calculus for SMBC; the BTPN, VPBank and Mahindra positions have built a Southeast Asia consumer-credit footprint that no other Japanese institution can match. The bank is rarely the cheapest counterparty on a single transaction, but it is often the fastest to commit and the most willing to lean into a complex structure.

Japonity helps overseas firms — investment banks, sponsors, asset managers and SE-Asia operators — identify the right Japanese counterparty and build introductions that turn a first meeting into a multi-product relationship. See our Business Matching page for how to start a structured engagement with SMFG and its peers.

Related from Japonity — Japan’s megabanks & securities

- MUFG — Japan’s #1 megabank and its Morgan Stanley stake

- Mizuho Financial Group — Japan’s #3 megabank — Greenhill + Rakuten Securities second act

- Nomura Holdings — The Lehman buyout, sixteen years later

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →