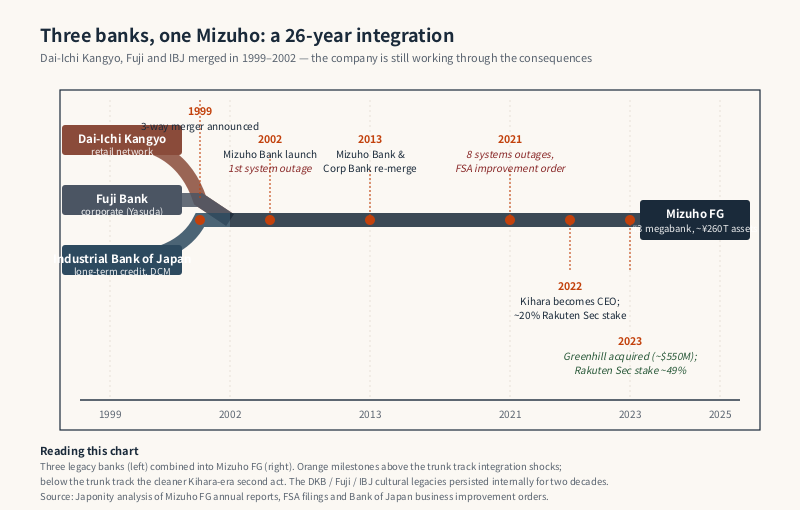

Three banks. Twenty-six years. One name that still struggles to feel like a single company. Mizuho Financial Group was born at the turn of the millennium from a corporate marriage that, on paper, should have produced Japan’s strongest financial institution: Dai-Ichi Kangyo Bank, the largest retail lender of its era; Fuji Bank, the blue-chip wholesale franchise; and the Industrial Bank of Japan, the prestigious long-term credit house that had financed Japan’s postwar industrial miracle. Instead, the combined entity has spent most of its life as the smallest of Japan’s three megabanks, and the most accident-prone — twice forced by regulators into business improvement orders after catastrophic IT systems outages, and bruised in 2023 by a securities-business scandal at a moment when peers were already pulling ahead. Yet Mizuho is also writing a quieter, more confident second act. The roughly $550 million acquisition of New York boutique Greenhill & Co., completed in December 2023, gave it a credible global M&A franchise. A stepped-up stake in Rakuten Securities is reshaping its retail position. And under chief executive Masahiro Kihara, in place since April 2022, the group is being run with a discipline that earlier eras lacked. This is the story of how Japan’s #3 megabank is trying to finally become one company.

The 1999 mega-merger that created a bank too big to integrate

To understand Mizuho is to understand the era that produced it. In the late 1990s Japan’s banking sector was in the worst crisis of the postwar period. Non-performing loans from the bursted bubble had hollowed out balance sheets; the 1997 collapse of Yamaichi Securities and Hokkaido Takushoku Bank had shaken confidence; and Tokyo’s regulators were quietly steering the industry toward consolidation. Survival, for any single bank, was no longer a guaranteed outcome.

In August 1999 three banks announced what was then the largest financial merger in world history. Dai-Ichi Kangyo Bank — itself the product of an earlier 1971 combination and Japan’s largest retail bank by branch count — would combine with Fuji Bank, the bluest of blue-chip wholesale lenders descended from the prewar Yasuda zaibatsu, and the Industrial Bank of Japan, the long-term credit bank whose underwriting had bankrolled Nippon Steel, Toyota, and most of the country’s heavy industry. The new group, named Mizuho (“瑞穂”, an archaic poetic reference to abundant rice harvests and a literary name for Japan itself), formally launched in 2000 as a financial holding company.

The strategic logic was unimpeachable. Dai-Ichi Kangyo brought a national retail network. Fuji brought corporate banking depth. IBJ brought debt capital markets, project finance, and the relationships that came with eight decades of long-term industrial lending. On paper, this was a universal bank to rival Citigroup or Deutsche Bank, with combined assets of approximately ¥140 trillion at formation — the largest banking group in the world at the time.

The execution, however, exposed a flaw that would haunt the group for two decades. Rather than collapse the three banks into one operating subsidiary immediately, the group preserved separate legal entities organised by customer segment. Mizuho Bank was created in 2002 to handle retail and SME business; Mizuho Corporate Bank handled large corporates. The three predecessor cultures, IT systems, personnel files, and unwritten rules survived inside what was nominally one company. Internal jokes about “the DKB faction”, “the Fuji faction” and “the IBJ faction” were not jokes — they described how promotions, postings, and project ownership were actually allocated well into the 2010s.

The three predecessor banks at a glance

| Predecessor | Founded | Franchise strength | Legacy inside Mizuho |

|---|---|---|---|

| Dai-Ichi Kangyo Bank (DKB) | 1971 (DKB merger) | Largest retail branch network in Japan | Retail bank backbone, individual lending |

| Fuji Bank | 1880 (Yasuda Bank lineage) | Premium corporate banking, ex-Yasuda zaibatsu | Mid- and large-corporate relationships |

| Industrial Bank of Japan (IBJ) | 1902 | Long-term credit, DCM, project finance | Mizuho Securities, debt capital markets, industrial relationships |

This three-legged identity has been Mizuho’s defining feature and its most persistent problem. Even today, more than a quarter-century after the merger announcement, current and former senior officials will speak privately about which of the three lineages a particular executive belongs to. No other Japanese megabank carries this kind of internal genealogy.

Systems outages and the cost of unfinished integration

If the cultural fault lines were the merger’s invisible cost, the IT systems were the visible one. The three predecessor banks had run on entirely different mainframe architectures — Fujitsu for DKB, IBM for Fuji, Hitachi for IBJ. Rather than choose one platform and migrate, the post-merger group attempted to stitch them together with relay systems. The cost of this decision became spectacularly clear on the first business day of the new entity.

On 1 April 2002, the day the customer-facing reorganisation took effect, Mizuho Bank’s payment systems collapsed. ATMs went dark, direct debits failed, salary transfers were delayed for hundreds of thousands of accounts, and tax payments were corrupted at scale. The Financial Services Agency issued a business improvement order. For the rest of the decade Mizuho pursued a multi-billion-dollar replacement of its core banking system — a project named MINORI — that suffered repeated delays and at one point became one of the most expensive private-sector IT efforts in Japanese history, with cumulative spend approaching ¥400 billion by the time it was finally completed in 2019.

Eighteen months later, in February 2021, the new system failed too. Roughly 5,000 ATMs froze with customer cards trapped inside; passbooks were swallowed; online banking was disrupted. Over the following months further incidents accumulated — eight separate disruptions in a single year. In November 2021 the FSA and Ministry of Finance issued formal business improvement orders, an extraordinarily rare regulatory response. Then-CEO Tatsufumi Sakai resigned in early 2022, succeeded by Masahiro Kihara, a veteran of Mizuho Corporate Bank’s international division.

The outages were not merely operational. They had a strategic cost: at exactly the moment when MUFG and SMFG were pulling ahead in scale, profitability, and overseas expansion, Mizuho was forced to spend management attention on remediation. The “lost decade of integration” became the lost decade of growth as well.

How Mizuho compares with MUFG and SMFG

Among Japan’s three megabank groups, Mizuho is consistently ranked third by total assets, market capitalisation, and net profit. The gap is not enormous, but it is structural — and reflects, in part, the integration tax described above.

| Group | Approx. total assets | Domestic retail footprint | Global signature |

|---|---|---|---|

| MUFG (Mitsubishi UFJ) | ~¥400 trillion | Largest, post-UFJ merger | Morgan Stanley alliance (~24% stake), US regional bank presence |

| SMFG (Sumitomo Mitsui) | ~¥290 trillion | Strong urban + corporate focus | Jefferies alliance, Asia ex-Japan expansion |

| Mizuho FG | ~¥260 trillion | Mid-tier retail, strong large-corporate base | Greenhill (M&A advisory), Rakuten Securities stake |

The differences are revealing. MUFG long ago took the decision to lean on a US franchise (its Morgan Stanley stake remains the single most valuable strategic asset in Japanese finance). SMFG, smaller and more disciplined, leans on Asia-ex-Japan growth and a sharper-edged corporate culture. Mizuho, sitting in the middle, has historically lacked a definitive overseas story — until Greenhill.

The Greenhill acquisition and the M&A bet

In May 2023 Mizuho announced an all-cash agreement to acquire Greenhill & Co., the New York-listed independent investment bank co-founded in 1996 by Robert Greenhill, formerly a senior banker at Morgan Stanley. The transaction valued Greenhill at approximately $550 million, closed in December 2023, and immediately rebranded the boutique as “Greenhill, a Mizuho affiliate”. The deal carried strategic weight out of proportion to its modest dollar value.

For Mizuho, Greenhill solved a long-standing problem: the group had global corporate banking presence but lacked credibility in cross-border M&A advisory, the highest-margin and most reputationally important business in investment banking. Building such a franchise organically takes a generation; acquiring an established team with restructuring and capital advisory specialisation compressed that timeline dramatically. The combined platform now serves Japanese corporates pursuing outbound acquisitions, US companies needing access to Japanese capital, and the broader US mid-market advisory business that Greenhill had cultivated for nearly three decades.

The bet is reminiscent in spirit, if not in size, of MUFG’s Morgan Stanley investment in 2008 — a contrarian-timed acquisition of a US franchise during a period when American boutiques were trading at depressed multiples. Whether Greenhill produces returns at MUFG-Morgan-Stanley scale will not be known for years, but the strategic signal is clear: Mizuho is no longer content to be the domestically focused option.

Rakuten Securities and the retail second front

In parallel with the wholesale move, Mizuho is restructuring its retail position. In November 2022 it acquired an approximately 20% stake in Rakuten Securities, the online brokerage subsidiary of e-commerce group Rakuten and one of the two dominant retail brokers in Japan alongside SBI Securities. In 2023 the stake was raised to approximately 49%, giving Mizuho a near-joint-venture position in one of the fastest-growing retail franchises in the country.

The logic mirrors the broader shift in Japanese household finance. With the launch of the expanded NISA tax-advantaged investment programme in 2024, household financial assets — historically ~50% in cash deposits, by far the highest share in any G7 economy — are tilting toward equities and mutual funds. Online brokers, not traditional bank branches, are capturing the flow. Rather than fight a losing battle with its branch network, Mizuho has bought a meaningful stake in the channel that customers are actually using. The Rakuten Securities partnership also opens a connected ecosystem of payments, credit cards, and points that Mizuho cannot replicate alone.

The 2023 IBSPK matter and the credibility cost

The cleaner second act has not been without setbacks. In 2023 Mizuho Securities was sanctioned by the Securities and Exchange Surveillance Commission for an episode involving improper handling of customer information in connection with block-trade and IPO-related activity. The incident — referenced in media coverage as the IBSPK matter, after the codename of the internal investigation — produced administrative orders, public apologies, and senior personnel changes. For a securities arm already living in the shadow of larger rivals Nomura, Daiwa, and SMBC Nikko, the timing was unfortunate.

The institutional response, however, has been notably different from earlier eras. Where the 2021 systems outage saw months of public confusion about accountability, the 2023 securities matter produced rapid disclosure, clear remediation steps, and visible governance changes. Whether this signals a durable cultural shift, or simply a more polished communications operation, is the question that matters most to investors and clients.

Mizuho group structure today

The group operates today through four principal subsidiaries: Mizuho Bank (commercial banking, retail and corporate), Mizuho Trust & Banking (trust services, pensions, asset administration), Mizuho Securities (investment banking, including the Greenhill platform and the legacy IBJ Securities franchise), and Mizuho Research & Technologies (research, IT, and consulting). The holding company is listed on the Tokyo Stock Exchange under code 8411, and group headquarters sit in the Marunouchi business district, directly across from Tokyo Station and within walking distance of MUFG and SMFG. Total employees number approximately 50,000 worldwide.

For overseas counterparties, two practical observations matter. First, Mizuho Corporate & Investment Banking is the entry point for most cross-border work — debt issuance, structured finance, project finance, and increasingly M&A advisory through the Greenhill platform. Second, English-language documentation, IR disclosure, and senior-level English fluency at Mizuho are among the best of any Japanese bank, reflecting the IBJ heritage of decades of international syndication work.

The Kihara era and what comes next

Masahiro Kihara, who became group CEO in April 2022 after the systems-outage resignations, represents a generational shift. A career corporate banker who spent formative years in New York and on cross-border financing, Kihara has framed his tenure around three priorities: stabilising operations, completing the cultural integration that the merger never finished, and finding a defensible global niche. The Greenhill deal and Rakuten Securities stake are the most visible outputs.

The unresolved questions remain significant. Can Mizuho close the profitability gap with MUFG and SMFG without a transformational deal? Will the Greenhill platform scale into a credible global M&A franchise, or remain a respectable mid-market shop with a Japanese parent? And, most uncomfortably, has the integration of the three predecessor cultures actually completed — or merely retreated from public view?

For all that, the Mizuho of 2026 is a more coherent institution than the Mizuho of 2016. It is still Japan’s #3 megabank. But it is also, for the first time in its history, a bank that knows what kind of #3 it wants to be.

FAQ

Which three banks merged to form Mizuho?

Mizuho Financial Group was formed at the turn of the millennium from the combination of Dai-Ichi Kangyo Bank, Fuji Bank, and the Industrial Bank of Japan (IBJ). The holding company formally launched in 2000, and Mizuho Bank as a customer-facing operating subsidiary launched in April 2002.

How does Mizuho rank among Japan’s megabanks?

Mizuho is the third-largest of Japan’s three megabank groups by total assets, market capitalisation, and net profit, after MUFG (Mitsubishi UFJ Financial Group) and SMFG (Sumitomo Mitsui Financial Group). The three groups together account for the majority of large-corporate banking activity in Japan.

What were the Mizuho systems outages?

Mizuho Bank suffered two major IT systems failures: the first on 1 April 2002 immediately after the merger, and the second in February 2021 followed by multiple further incidents through that year. Both events triggered formal business improvement orders from Japanese regulators and senior management changes.

Why did Mizuho acquire Greenhill & Co.?

The acquisition of New York-based independent investment bank Greenhill & Co., completed in December 2023 for approximately $550 million, gave Mizuho an established global M&A advisory franchise — a capability the group had historically lacked despite its corporate banking scale. The combined platform serves Japanese outbound M&A, US mid-market deals, and cross-border capital advisory.

What is Mizuho’s stake in Rakuten Securities?

Mizuho acquired an approximately 20% stake in Rakuten Securities in 2022 and raised it to approximately 49% in 2023, giving the group a near-joint-venture position in one of Japan’s two dominant online retail brokerages. The move positions Mizuho for the household-finance shift toward equities accelerated by the expanded NISA programme.

Working with Mizuho

For overseas companies exploring debt financing, cross-border M&A advisory, structured finance, or Japan-market entry through a megabank partner, Mizuho’s corporate and investment banking division and the Greenhill platform are the primary points of engagement. Japonity helps qualified international counterparties navigate introductions to Japanese megabank groups and their advisory arms.

Explore business matching with Japonity →

Related from Japonity — Japan’s megabanks & securities

- MUFG — Japan’s #1 megabank and its Morgan Stanley stake

- Sumitomo Mitsui FG (SMFG) — Japan’s #2 megabank and the Jefferies alliance

- Nomura Holdings — The Lehman buyout, sixteen years later

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →