When Warren Buffett unveiled in August 2020 that Berkshire Hathaway had quietly accumulated stakes of just over 5 percent in each of Japan’s five general trading houses, the news landed with the curiosity of an oracle endorsing an institution most Western investors could not properly name. Mitsubishi Corporation and Mitsui & Co. attracted the loudest commentary. Itochu earned admiration for its consumer-facing pivot. Marubeni was talked about as the turnaround story. The fifth name, Sumitomo Corporation, was mentioned almost as an afterthought — the conservative one, the steady one, the one whose share-price chart over the preceding decade looked like the heart-rate monitor of a sleeping patient. Yet for Buffett, that boring quality was the point. Sumitomo Corporation is the sogo shosha that earns its keep not by riding the iron-ore super-cycle to euphoric heights, but by owning the unglamorous infrastructure of Japanese commerce — steel-products distribution, cable television, leasing, auto retail finance, food trading — and by refusing, decade after decade, to leverage its way to a flashier return on equity. It is, in many ways, the most Sumitomo of the Sumitomo companies: a 430-year-old merchant house that still talks in board meetings about “the spirit of enterprise that does not pursue easy profits.”

A 17th-century copper merchant becomes a 21st-century trading house

The Sumitomo name predates almost every other corporate group in Japan and most in the world. The family’s commercial history is conventionally dated to 1590, when Soga Riemon, a Buddhist priest turned merchant, opened a shop in Kyoto and began refining copper using a Western technique called nanban-buki that separated silver from raw ore. His successors moved into mining itself and in 1691 took possession of the Besshi copper mine in what is now Ehime Prefecture, on Shikoku. For the next 283 years, until Besshi was finally closed in 1973, the Sumitomo family ran one of the largest and most technologically advanced copper-mining operations in Asia, and used the cash flow to expand into banking, warehousing, forestry, and eventually heavy industry.

The trading house that today carries the Sumitomo name is, by Japanese corporate standards, a relatively young expression of this lineage. It traces its founding to December 1919, when the Sumitomo zaibatsu established Osaka Hokkokai Kaisha, originally as a real-estate management vehicle for the family’s holdings in Osaka’s developing port and warehouse district. Renamed Sumitomo Building Company in 1921, it gradually absorbed trading functions during the war economy of the late 1930s and was reorganised in 1944 as Sumitomo Shoji Kaisha — Sumitomo Trading Company. When the American Occupation dissolved the zaibatsu in 1945, the trading arm was forced to operate temporarily under the neutral name Nippon Kensetsu Sangyo before recovering the Sumitomo identity in 1952. It listed on the Tokyo and Osaka stock exchanges in 1949 and 1950, and assumed its current English name, Sumitomo Corporation, in 1978.

That late start matters. Mitsui and Mitsubishi had been integrated trading houses since the Meiji era; Sumitomo did not become a full-spectrum sogo shosha until the 1950s. The consequence, visible in every annual report since, is that Sumitomo Corporation built its franchise less around the romance of exploration and resource discovery than around the slower, less cyclical work of domestic and intra-Asian distribution. It is the trading house that learned, by necessity, to make money in a country at peace.

The portfolio: where Sumitomo actually earns its money

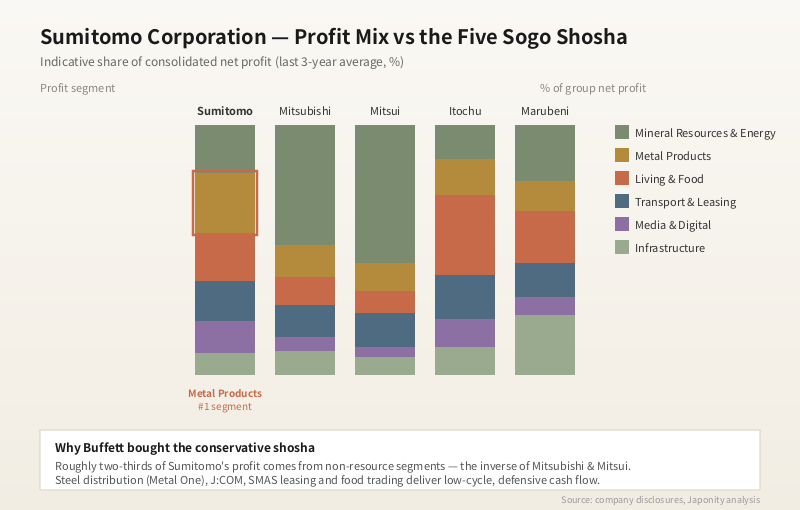

Sumitomo Corporation reports through six business units, and the shape of the mix is the single most important fact to grasp about the company. Unlike Mitsubishi Corporation, whose profit is dominated by mineral resources and LNG, or Mitsui & Co., where iron ore alone can swing group earnings by hundreds of billions of yen in a single year, Sumitomo’s portfolio is striking for what it does not contain: it has no major iron-ore operation, no major LNG equity position, and a relatively modest oil-and-gas footprint.

| Sumitomo Corporation business unit | Representative assets | Cycle exposure |

|---|---|---|

| Metal Products | Sumitomo Mitsui Steel Distribution (Sumisho-Mitsui Metal One JV with Mitsubishi Corp, 50/50), steel pipe trading, aluminium | Moderate, distribution-led |

| Transportation & Construction Systems | Sumitomo Mitsui Auto Service (SMAS) leasing, aircraft leasing (SMBC Aviation Capital co-investment), construction machinery, automotive dealerships in Asia | Low to moderate |

| Infrastructure | Power generation (gas, renewables), water concessions, EPC equity | Moderate, regulated |

| Media & Digital | Jupiter Telecommunications (J:COM) co-ownership with KDDI, SCSK (IT services, listed), advertising and digital media | Low, subscription-led |

| Living Related & Real Estate | Asahi Drinks Industry-affiliated food distribution, Tomod’s drugstore chain (former), supermarkets in Asia, residential development, Sumisho Tobacco JV | Low, defensive |

| Mineral Resources, Energy, Chemical & Electronics | Ambatovy nickel project (Madagascar), San Cristobal silver-zinc (Bolivia), copper interests, exited Banpu thermal coal | High but smaller in absolute terms than peers |

Roughly two-thirds of Sumitomo’s consolidated net profit comes from non-resource segments in a typical year — a ratio almost exactly the inverse of Mitsubishi Corporation’s during a strong commodity cycle. In years when iron ore and coking coal collapse, this is precisely why analysts at Daiwa and SMBC Nikko describe Sumitomo as “the defensive shosha.” In years when commodities boom, the same structure is why Sumitomo’s share price lags. Buffett, characteristically, appears to find the trade-off acceptable.

Steel distribution: the quiet monopoly

Among Sumitomo’s businesses, the one that deserves the most attention from anyone trying to understand Japanese industrial supply chains is Metal One, properly Sumisho Metal One. Established in 2003 as a 50/50 joint venture with Mitsubishi Corporation, Metal One is the largest steel-products distributor in Japan and one of the largest in the world, handling more than 20 million tonnes a year of plate, sheet, structural steel, pipe and specialty products. It buys from Nippon Steel, JFE, Kobe Steel and others, holds inventory in regional service centres, performs first-stage processing such as cutting and slitting, and supplies the country’s automotive, shipbuilding, construction, machinery and white-goods manufacturers.

Recent reporting suggests that the Metal One joint-venture structure is under review and that the two parents have discussed restructuring or dissolving the JV in favour of more direct ownership of distinct regional and product franchises. Whatever the outcome, the underlying point is the same: Sumitomo controls, alone or jointly, the dominant channel by which Japanese steel reaches Japanese factories. It is not a glamorous business — gross margins are thin, the inventory cycle is brutal — but it is the kind of asset that earns predictable returns in a country whose manufacturers prize long, stable supplier relationships above all else.

J:COM and the strange shape of Sumitomo’s media bet

The other unusual concentration in Sumitomo’s portfolio is media. Jupiter Telecommunications, known commercially as J:COM, is Japan’s largest cable television and broadband operator, serving roughly 5.5 million households. Sumitomo began building the J:COM franchise in the mid-1990s, eventually consolidating it as a majority-owned and publicly listed subsidiary by 2010. In 2013–2014, Sumitomo and KDDI executed a complex transaction that took J:COM private, with KDDI emerging as the controlling shareholder and Sumitomo retaining a substantial minority economic interest. Sumitomo subsequently increased its participation in adjacent media assets, leaving it with one of the deepest exposures to Japan’s pay-TV-and-broadband bundle of any sogo shosha. Combined with SCSK, its listed IT services subsidiary, this gives Sumitomo a “media and digital” segment that contributes a steadier, lower-cycle profit stream than peers can match.

Food, leasing and the unsexy core

The Living Related & Real Estate segment is the part of Sumitomo Corporation that least resembles the cliché of the resource-hunting trading house, and is also the part most likely to grow in the next decade. The group operates supermarket chains in Vietnam (FujiMart, a joint venture with BRG), and Singapore and runs a substantial food-trading book through partnerships with manufacturers including Asahi Soft Drinks and various Asahi Group affiliates in beverages and processed foods. It controls Sumisho Tobacco, the joint venture with Japan Tobacco that distributes cigarettes domestically. It builds and operates condominiums in Tokyo, Osaka and increasingly in Southeast Asia. None of this is exciting; all of it is, in aggregate, very profitable.

Transportation & Construction Systems is similarly defensive. Sumitomo Mitsui Auto Service, a 50/50 venture with Sumitomo Mitsui Financial Group, is the largest auto-leasing company in Japan with more than 900,000 vehicles under management. The group also co-invests with SMBC in SMBC Aviation Capital, one of the world’s three largest aircraft lessors. These leasing franchises generate the sort of contractual, multi-year cash flow that allows Sumitomo to commit to mineral-resource investments without the balance-sheet anxiety that has periodically afflicted Mitsui and Marubeni.

The hard lessons: Madagascar and the resource book

For all its conservatism, Sumitomo is not immune from the resource project that goes wrong. The most visible example is the Ambatovy nickel-cobalt project in Madagascar, in which Sumitomo holds a major equity stake alongside Korea Resources Corporation. Commissioned in the early 2010s at a total project cost of around USD 8 billion, Ambatovy has consistently underperformed its design throughput, has required multiple impairment charges, and was effectively idled during the worst of the COVID-19 period. Sumitomo’s San Cristobal silver-zinc mine in Bolivia and its earlier participation in the Madagascar tar-sands study have similarly produced cycles of impairment.

The lesson the company appears to have drawn is one of disciplined exit. In the early 2020s, Sumitomo announced and largely completed its withdrawal from thermal coal trading and equity, exiting the Banpu coal partnership in Indonesia and committing to net-zero thermal-coal exposure. It has shifted its upstream resource emphasis toward copper, where it holds positions including Sierra Gorda in Chile in partnership with KGHM and South32, and toward nickel and lithium with future battery-supply-chain optionality. The portfolio is still cyclical, but it is smaller as a share of group profit than at any time in the last twenty years.

Governance, leadership and the Buffett endorsement

Sumitomo Corporation is led from its headquarters at the Otemachi Place complex in central Tokyo. Masayuki Hyodo served as president and chief executive officer from April 2018 to March 2024, navigating the company through the late stages of the commodity downturn, the pandemic, the thermal-coal exit and the initial Berkshire Hathaway investment. He was succeeded in April 2024 by Shingo Ueno, a career Sumitomo executive whose background spans the steel and infrastructure businesses and who has signalled continuity rather than reinvention as his theme. Cross-shareholdings with Sumitomo Mitsui Banking Corporation, Sumitomo Life and Sumitomo Mitsui Trust remain meaningful, although they have been gradually reduced under the broader pressure on Japanese corporates to release capital.

Berkshire Hathaway has, in the years since the original 2020 disclosure, modestly increased its stakes in all five sogo shosha and indicated a long-term horizon. For Sumitomo specifically, the Buffett endorsement has done something subtle but significant: it has given a global audience a reason to look at a company whose merits — low debt, diversified profit, generous shareholder returns, predictable governance — were never likely to be appreciated in a market that rewards growth narratives.

The wider Sumitomo Group: what Sumitomo Corp is not

It is worth clarifying, because Western readers routinely conflate them, that Sumitomo Corporation is one of several large publicly listed entities in the broader Sumitomo Group keiretsu. Sumitomo Chemical (the chemical and agro-chemical major), Sumitomo Electric Industries (wire, harnesses, optical fibre), Sumitomo Heavy Industries (machinery, shipbuilding), Sumitomo Metal Mining (copper, gold, nickel), Sumitomo Mitsui Financial Group (banking, via the post-2001 SMBC merger with Sakura Bank) and Sumitomo Realty & Development are all separate listed companies with their own governance, their own boards and their own share registers. They share the Sumitomo name and the heritage of the Besshi copper mine, but they do not consolidate into Sumitomo Corporation and their financial results have no direct effect on its accounts. The Sumitomo Group’s coordinating body, the White Water Society (Hakusui-kai), exists chiefly as a forum and a symbol, not as an operating holding structure.

This matters for non-Japanese counterparties. A company exploring a partnership with “Sumitomo” needs to know whether it is approaching the trading house, the chemicals major, the wire manufacturer or the bank, because the cultures, decision-making cycles and capital allocations are genuinely different. Sumitomo Corporation, the subject of this profile, is the merchant. It buys, sells, distributes, invests and divests. It is the entity that takes a minority equity stake in a partner overseas, helps it secure offtake or financing, and stays alongside it for decades.

FAQ

Is Sumitomo Corporation the same company as Sumitomo Chemical or Sumitomo Electric?

No. Sumitomo Corporation is the general trading company (sogo shosha) of the Sumitomo Group. Sumitomo Chemical, Sumitomo Electric Industries, Sumitomo Heavy Industries, Sumitomo Metal Mining, Sumitomo Mitsui Financial Group and Sumitomo Realty & Development are separately listed companies within the broader Sumitomo Group, each with its own board, management and shareholders.

Why did Warren Buffett buy Sumitomo Corporation in 2020?

Berkshire Hathaway invested in all five major sogo shosha simultaneously, attracted by their low valuation multiples, high free-cash-flow generation and globally diversified portfolios. Sumitomo specifically appealed because of its lower commodity-cycle exposure, conservative balance sheet, consistent dividend record and the optionality embedded in its leasing, media and food-distribution businesses.

What is Metal One and why is it important?

Metal One is the largest steel-products distributor in Japan, established in 2003 as a 50/50 joint venture between Sumitomo Corporation and Mitsubishi Corporation. It supplies Japan’s automotive, shipbuilding, construction and machinery manufacturers with plate, sheet, structural steel and pipe, handling more than 20 million tonnes annually.

Does Sumitomo Corporation still own J:COM cable television?

Sumitomo Corporation co-owns J:COM with KDDI. In a 2013–2014 transaction the two companies took J:COM private with KDDI as the controlling shareholder and Sumitomo retaining a significant minority economic interest. J:COM remains Japan’s largest cable television and broadband provider with roughly 5.5 million household subscribers.

What is the difference between Sumitomo Corporation and Mitsubishi Corporation?

Both are sogo shosha, but their profit mixes differ. Mitsubishi Corporation derives a larger share of profit from mineral resources and LNG and is therefore more cyclical. Sumitomo Corporation has lower upstream resource exposure and earns proportionally more from steel-products distribution, leasing, media and food-related businesses, making its earnings more stable across commodity cycles.

Working with Sumitomo Corporation

Companies seeking distribution, equity partnership, offtake or market entry support in Japan and across Asia frequently engage Sumitomo Corporation when stability, long-term commitment and a relatively conservative governance style are priorities. Japonity’s business matching service introduces overseas manufacturers, brand owners and project sponsors to the appropriate Sumitomo Corporation business unit and to other Japanese trading and operating partners. We help frame the opportunity, prepare introduction materials in Japanese business etiquette, and accompany the first round of dialogue. Please contact us if you would like to be introduced.

Related from Japonity — Japan’s sogo shosha (trading houses)

- Itochu Corporation — The consumer-oriented sogo shosha Buffett bet on

- Mitsubishi Corporation — The biggest sogo shosha — Lawson take-private and consumer pivot

- Mitsui & Co. — The trading house most exposed to the energy transition

- Marubeni Corporation — The textile-to-electrons shosha — power IPP, Helena, Gavilon

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →