When Warren Buffett’s Berkshire Hathaway disclosed its 5% stakes in Japan’s five major sogo shosha in August 2020, Marubeni Corporation — the smallest of the five by revenue but arguably the most distinctive in portfolio composition — was the surprise inclusion. Where Mitsubishi and Mitsui anchor on LNG and iron ore, where Itochu thrives on consumer goods, and where Sumitomo leans into media and real estate, Marubeni occupies a quieter but increasingly strategic niche: one of the world’s largest independent power producers, a top-tier global grain and fertiliser merchant via its US subsidiaries, and the most renewable-energy-tilted of the Big Five. With a net IPP capacity exceeding 11 gigawatts and roughly a quarter of that already from renewables — a share rising fast — Marubeni is positioning itself as the green-energy specialist among Japan’s general trading houses. This is the story of a 1858 textile partnership that became a global merchant of electrons, calories, and fertiliser.

From Omi cloth merchant to Marubeni-Iida

Marubeni traces its origins to 1858, when Chubei Itoh I — a 17-year-old Omi merchant from what is today Shiga Prefecture — began travelling between Osaka and Nagasaki selling linen cloth. The same Chubei Itoh founded the trading operation that would, after the post-war zaibatsu dissolution, split into two of today’s five major sogo shosha: Itochu Corporation and Marubeni. The two firms share a common ancestor but evolved very different cultures — Itochu became the consumer-facing trader, while Marubeni took a more industrial path through textiles, machinery, and eventually energy and agriculture.

The name “Marubeni” derives from the company’s old trademark — a circle (maru) around the character beni (紅, meaning crimson) — which Chubei Itoh used to mark his bolts of cloth. The modern corporate form took shape in 1949 as Marubeni-Iida Co. Ltd., born from the post-war breakup of the Daido Boeki and Itoh conglomerates under General MacArthur’s deconcentration directives. It was renamed simply Marubeni Corporation in 1972, by which point textiles were no longer the centre of gravity. Like its peers, Marubeni had quietly diversified into chemicals, metals, machinery, foodstuffs and project finance, becoming a fully fledged sogo shosha in the post-war sense: a trading-house-cum-investment-firm-cum-project-developer that profits less from import-export margins than from owning slices of the global supply chain itself.

The fifth Buffett pick: why Marubeni was different

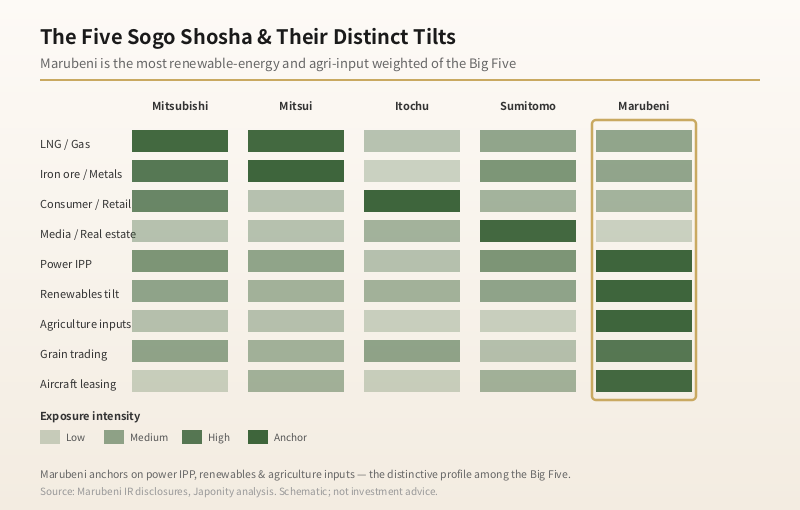

Berkshire Hathaway’s 2020 disclosure of stakes in all five major trading houses was, in many ways, a bet on Japan Inc.’s deep value and dollar cash-flow durability. But each of the five offers a distinct exposure profile. Marubeni’s was — and is — the most concentrated in two areas that few outside Japan associated with shosha at the time: independent power generation and agricultural inputs.

This positioning has aged well. As global capital has rotated toward energy transition and food security themes, Marubeni’s portfolio looks less like a legacy conglomerate and more like a curated bet on the two underlying flows that matter most to a decarbonising, geopolitically fractured world: electrons and calories. Buffett, in subsequent annual letters, has hinted at this — praising the trading houses’ “long-term-oriented” capital allocation and their unusually generous dividend policies. Berkshire has since raised its average stake across the five toward 10%, with Japanese regulators waiving the standard disclosure threshold under a bilateral understanding.

The business segment portfolio

Marubeni reports its operations across approximately 16 business segments, organised under broader groupings of Lifestyle, Materials, Energy & Metals, Power & Infrastructure, and Food & Agriculture. The portfolio is unusually balanced — no single segment dominates earnings the way iron ore does at Mitsubishi or convenience stores do at Itochu.

| Business group | Segment | Notes |

|---|---|---|

| Lifestyle | Lifestyle | Apparel, footwear, lifestyle goods (echo of textile heritage) |

| ICT & Real Estate | Information & Communication | IT services, data centres, software distribution |

| Materials | Living-essential Materials | Rubber, salt, packaging materials |

| Materials | Forest Products | Pulp, paper, building materials; Daishowa-Marubeni pulp JV |

| Materials | Chemicals | Petrochemicals, methanol, lithium-ion battery materials |

| Energy & Metals | Energy | LNG, oil & gas upstream, trading |

| Energy & Metals | Metals & Mineral Resources | Copper, aluminium, iron ore, coking coal |

| Power & Infrastructure | Power Business | IPP, renewable energy generation, retail power |

| Power & Infrastructure | Plant | Industrial plant engineering and project finance |

| Transportation | Aerospace & Ship | Aircraft leasing (Aircastle), shipping |

| Finance | Finance & Leasing | PE funds, leasing, project finance |

| Machinery | Construction & Industrial Machinery | Komatsu and other heavy-equipment distribution |

| Food & Agriculture | Agriculture | Helena Agri-Enterprises (US), fertiliser (Gavilon Fertilizer) |

| Food & Agriculture | Food I | Grains, oilseeds, sugar; merchandising and origination |

| Food & Agriculture | Food II | Processed foods, beverages, foodservice distribution |

| Steel | Iron & Steel | Steel products distribution, tubular goods |

Electrons: the IPP powerhouse

Marubeni’s Power Business segment is, by most rankings, among the top ten independent power producers in the world by net generation capacity. As of recent disclosures, the company holds equity interest in roughly 11.5 gigawatts of net generation capacity across more than 20 countries, with a deliberate strategic tilt toward emerging Asia, the Middle East, and increasingly Europe and the Americas for renewables.

What distinguishes Marubeni from its peers is the composition of that capacity. Where Mitsubishi and Sumitomo entered power generation primarily through gas-fired plants in the 1990s, Marubeni was an earlier and more aggressive mover into renewable energy. The company committed in 2018 to halve its coal-fired capacity by 2030 and to reach net zero on its power portfolio by 2050 — targets that were, at the time, among the most ambitious from any major Japanese trading house. Since then, Marubeni has scaled back new coal development, divested several thermal assets, and accelerated investment in offshore wind (notably the UK’s Gunfleet Sands and Triton Knoll projects), large-scale solar across Southeast Asia and the Middle East, and battery storage in Australia and Europe.

The retail electricity arm — Mieux Energy, partnered with TEPCO — adds a downstream piece in Japan’s deregulated power market. Combined with the company’s growing position in green hydrogen and ammonia value chains (a partnership with HyAxiom in fuel cells and various offtake agreements for clean ammonia from the Gulf), Marubeni is making the clearest energy-transition bet of the five Big Five trading houses.

Calories: Gavilon, Helena and the agri-platform

Marubeni’s other distinctive bet is in the agricultural value chain — and here the story turns trans-Pacific. In 2012, Marubeni acquired US grain merchant Gavilon Holdings for approximately $3.6 billion (then about ¥280 billion), instantly making it one of the largest grain originators in North America, alongside ABCD majors Archer Daniels Midland, Bunge, Cargill and Louis Dreyfus. The deal — at the time the largest overseas acquisition ever by a Japanese trading house — gave Marubeni direct origination capacity for corn, wheat, soybeans and other commodities at hundreds of US grain elevators, integrating into Marubeni’s grain trading flows back to Asia.

The strategic logic was clean — Marubeni was already one of the largest grain importers into Japan and Asia, and owning the upstream origination would convert volatile trading margins into more stable, structural ones. The execution was harder than expected. Margin pressure, US-China trade frictions, and the difficulty of integrating a Nebraska-based merchant into a Tokyo-listed shosha drove Marubeni to take impairments on the deal in subsequent years. In 2022, Marubeni divested Gavilon’s grain trading division to Viterra (the Glencore-backed grain major) for approximately $1.13 billion, while keeping the more profitable fertiliser distribution arm, now operated as Gavilon Fertilizer.

Yet that wasn’t a retreat from agriculture — it was a refocus. Marubeni had quietly built another US agricultural giant decades earlier: Helena Agri-Enterprises, acquired in the 1990s, is one of the largest distributors of crop protection chemicals, seeds, fertiliser and agronomic services to US farmers, with hundreds of locations across rural America. Helena combined with Gavilon Fertilizer makes Marubeni the largest non-American owner of US agricultural input distribution — a structurally advantaged position as climate volatility and precision-agriculture spending grow.

Aircraft, pulp and the other big bets

Beyond electrons and calories, Marubeni runs several smaller but globally significant businesses. Aircastle, the US-headquartered aircraft leasing company in which Marubeni holds a 75% stake (alongside Mizuho Leasing), owns and leases more than 250 commercial jets to airlines worldwide — a business that, despite pandemic turbulence, has emerged as one of the more durable post-COVID franchises in transportation finance.

The pulp and paper business, anchored by the Daishowa-Marubeni International joint venture in Canada, is a quiet but profitable contributor — producing northern bleached softwood kraft pulp prized by Asian tissue and paper manufacturers. The Chemicals segment is becoming an increasingly important growth platform, with Marubeni building positions in lithium battery materials and methanol-to-ammonia fuel pathways that connect to its energy transition strategy.

Even the apparently legacy Lifestyle segment has been quietly revived through value-added bets — Marubeni owns or co-owns several premium apparel brands (including a long partnership with WHIZ LIMITED and stakes in fashion logistics platforms), and runs one of Japan’s larger third-party logistics operations for apparel and footwear brands seeking entry to the Japanese market.

Masumi Kakinoki and the management transition

Masumi Kakinoki, who became President and CEO in April 2019, has overseen Marubeni’s most consequential strategic pivots — the coal reduction commitment, the Gavilon refocus, and an explicit emphasis on shareholder returns that has lifted the dividend payout ratio and brought the stock price to multi-decade highs. Kakinoki, an energy-business veteran who rose through Marubeni’s power IPP operations, exemplifies a generational shift among shosha leadership: less M&A-trophy oriented, more disciplined on capital, and more vocal about sustainability and governance.

Under Kakinoki, Marubeni adopted a mid-term management plan (“GC2024” followed by “GC2027”) that explicitly targets capital efficiency (ROE in the mid-teens), portfolio rotation (a steady stream of asset divestments funding green-energy investment), and an absolute reduction in coal exposure. The Tokyo Otemachi headquarters — Marubeni’s striking building across from Tokyo Station — has become a venue for some of the more thoughtful corporate-strategy communications among Japan Inc.’s biggest names.

How Marubeni compares to its four peers

It is worth being precise about Marubeni’s place among the five. By revenue and net income, Marubeni is the smallest of the Big Five — typically posting roughly half of Mitsubishi Corporation’s earnings in a given year. But by composition, it is arguably the most strategically focused:

- Mitsubishi Corporation — anchored on LNG, copper, automotive and convenience stores. Largest by earnings.

- Mitsui & Co. — heavily weighted to iron ore (Vale partnership) and LNG. The most resource-tilted.

- Itochu — consumer goods, retail (FamilyMart), textiles. The most domestically Japanese-consumer-oriented.

- Sumitomo — media, real estate, infrastructure, copper. The most diversified into services.

- Marubeni — power IPP, agriculture, aircraft leasing, pulp. The most renewable-and-agri-tilted.

For an investor or partner trying to gain Asian exposure to specifically renewable energy infrastructure plus agricultural inputs — without buying a pure-play utility or a pure-play agri-merchant — Marubeni is the cleanest single name in the listed Japanese universe.

FAQ

Who founded Marubeni and when?

Marubeni traces its origins to 1858, when Chubei Itoh I — the same Omi merchant who founded the trading lineage that became Itochu — began travelling between Osaka and Nagasaki to sell linen cloth. The modern corporate entity was established in 1949 as Marubeni-Iida Co. Ltd. after the post-war dissolution of pre-war zaibatsu and renamed Marubeni Corporation in 1972.

Why is Marubeni one of Warren Buffett’s “five sogo shosha” picks?

Berkshire Hathaway disclosed 5% stakes in all five major Japanese trading houses in August 2020. Marubeni’s distinctive appeal was its outsized exposure to independent power production (one of the world’s top ten IPPs), agricultural inputs (Helena Agri-Enterprises and Gavilon Fertilizer in the US), and renewable energy — the most green-energy-tilted of the Big Five.

What happened with Marubeni’s acquisition of Gavilon?

Marubeni acquired US grain merchant Gavilon for approximately $3.6 billion in 2012, the largest overseas acquisition by a Japanese trading house at the time. After years of margin pressure, Marubeni divested Gavilon’s grain trading arm to Viterra for around $1.13 billion in 2022 but retained the more profitable fertiliser distribution arm (now Gavilon Fertilizer), which remains a core part of its US agriculture platform.

How big is Marubeni’s renewable energy portfolio?

Marubeni holds equity interest in roughly 11.5 gigawatts of net power generation capacity across more than 20 countries, with renewables already representing a significant and rapidly growing share. The company has committed to net zero on its power portfolio by 2050 and to halving its coal-fired capacity by 2030 — among the most ambitious targets in Japanese shosha sector.

Who is the current CEO of Marubeni?

Masumi Kakinoki has served as President and CEO since April 2019. A career energy-business executive who rose through Marubeni’s power IPP operations, he has driven the company’s coal reduction commitment, Gavilon portfolio refocus, and the GC2024 and GC2027 mid-term management plans emphasising capital efficiency and shareholder returns.

Working with Marubeni

If your organisation is exploring partnership with Marubeni Corporation — whether for renewable energy project development, agricultural input distribution, aircraft leasing, supply chain origination, or any of its 16 business segments — Japonity can help facilitate introductions and structure a credible approach. We work with international companies seeking to engage with Japan’s major trading houses and their global operating subsidiaries. Visit our business matching service to start a conversation about how to align your proposition with Marubeni’s portfolio priorities.

Related from Japonity — Japan’s sogo shosha (trading houses)

- Itochu Corporation — The consumer-oriented sogo shosha Buffett bet on

- Mitsubishi Corporation — The biggest sogo shosha — Lawson take-private and consumer pivot

- Mitsui & Co. — The trading house most exposed to the energy transition

- Sumitomo Corporation — The conservative shosha — steel distribution and J:COM

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →