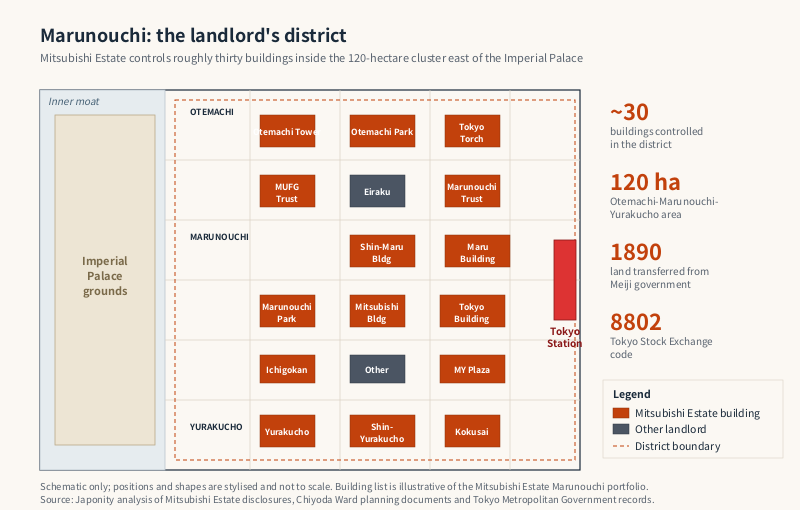

Walk out of Tokyo Station’s red-brick Marunouchi exit and look up. The wall of granite and glass framing the plaza — the Maru Building, the Shin-Maru Building, the Tokyo Building, the Mitsubishi Building, the Marunouchi Park Building — is not just an architectural ensemble. It is, with very few exceptions, a single landlord’s portfolio. Mitsubishi Estate Co., Ltd. controls roughly thirty buildings inside the Otemachi-Marunouchi-Yurakucho district — the 120 hectares wedged between the Imperial Palace moat and the country’s busiest railway station — and that cluster generates rent per square metre higher than any equivalent piece of urban land in Japan. The district hosts every major Japanese megabank, three of the four largest trading houses, the country’s top life insurers, the Tokyo Stock Exchange and the operational hubs of much of the Nikkei 225. The land was transferred from the Meiji government to the founding Iwasaki family in 1890, and over 135 years it has compounded into arguably the most strategically located real estate franchise in any G7 capital. The company built on that land — listed on the Tokyo Stock Exchange under code 8802, descended from the property department of the Mitsubishi zaibatsu, currently led by president Junichi Yoshida since April 2024 — is in many respects a single-asset business with a global edge layered on top.

The 1890 land grant that built a company

The story begins with a fiscal problem. By the late 1880s the Meiji government had relocated its army training grounds away from central Tokyo and was sitting on a stretch of marshy, undeveloped land east of the Imperial Palace moat. Cabinet ministers wanted it sold; nobody in the private sector wanted to buy. The plot was too large, too soggy, too exposed to the obligations of building urban infrastructure from scratch.

In 1890 the government offered the entire 35-hectare parcel to Yanosuke Iwasaki, younger brother of Mitsubishi’s founder Yataro Iwasaki. The price was around 1.5 million yen — equivalent to roughly a tenth of the central government’s annual budget. Yanosuke accepted. Skeptical observers nicknamed the purchase Mitsubishi-ga-hara, the Mitsubishi moor, on the assumption that it would become a money-losing wasteland. Within a decade the Iwasaki family had commissioned the British architect Josiah Conder to design Japan’s first Western-style office buildings on the site. Mitsubishi Ichigokan — the No.1 Building — opened in 1894, followed by a sequence of red-brick blocks that gave the district the nickname Itchō Rondon, “one block of London.”

Mitsubishi Estate Co., Ltd. was formally incorporated in 1937 as the real estate arm of the Mitsubishi zaibatsu. When Occupation antitrust authorities forced the zaibatsu to dissolve after 1945, Mitsubishi Estate emerged as an independent listed company, retaining title to the Marunouchi land. The post-war rebuild — first low-rise blocks designed to preserve sightlines to the Imperial Palace, then the cluster of skyscrapers permitted after 1990s deregulation — has unfolded under a single ownership umbrella that virtually no other downtown district in any major capital can match.

Why Marunouchi rents are different

Analysts have a habit of comparing Tokyo office rents to Manhattan or the City of London. The comparison obscures the most important fact about Marunouchi: rent there is set inside a closed system. Because one landlord owns roughly thirty of the district’s prime buildings, supply, vacancy and lease terms are coordinated in a way that is structurally impossible in fragmented markets. When Mitsubishi Estate takes the Marunouchi Building out of service for redevelopment, supply in the most coveted blocks tightens for everyone. When a tower opens with new specifications, rent benchmarks across the cluster reset upward in lockstep.

The result is durably premium pricing. Effective monthly rents in Marunouchi grade-A buildings have for years run materially above Otemachi, Nihonbashi or Toranomon, even though those districts now offer comparably modern towers. The difference reflects two things that cannot be replicated: a clientele willing to pay for headquarters-grade addresses near the Imperial Palace, and a single landlord curating the district as a whole. That pricing power feeds back into strategic discretion: because the core portfolio generates such durable cash flow, Mitsubishi Estate can run a redevelopment cycle on its own terms, demolishing and rebuilding on a thirty-to-fifty-year cadence without the leverage stress that constrains newer developers.

The redevelopment cycle, building by building

The current Marunouchi skyline is the third or fourth generation of buildings to occupy the same plots. The 1923 Maru Building, originally an eight-storey neoclassical block, was demolished in 1999 and replaced in 2002 by the 36-storey tower that anchors the Tokyo Station front today. The Shin-Marunouchi Building, completed in 2007, replaced a 1950s predecessor. The Tokyo Building was rebuilt as Tokia in 2005. The Marunouchi Park Building, the Otemon Tower, the Otemachi Park Building and a string of others have followed on a rolling schedule disclosed in five-year increments.

Each redevelopment lifts permitted floor area through coordination with Tokyo Metropolitan Government, adds retail and cultural space at street level, and pushes office specifications toward seismic isolation, low-carbon mechanical systems and tenant-grade flexibility legacy buildings cannot match. The architectural rhythm — preserve a fragment of the historic facade, lift the tower well above it — has become a Marunouchi signature. The reconstructed Mitsubishi Ichigokan, completed in 2009 as a faithful re-creation of the 1894 Conder original, operates today as an art museum and visual anchor for the district’s brand story.

The table below sketches the company’s reporting segments and where the Marunouchi engine sits within them.

| Segment | Core activity | Signature assets / projects | Approximate role in profit mix |

|---|---|---|---|

| Commercial Property Business | Office leasing, retail leasing, Marunouchi redevelopment | Marunouchi Building, Shin-Marunouchi Building, Tokyo Building, Otemachi Park Building, Marunouchi area | Largest segment; foundation of group earnings |

| Residential Business | Condominium development, custom homes, residential rental | The Parkhouse brand, Izumi Garden, Yokohama waterfront projects | Cyclical; sensitive to mortgage rates and unit supply |

| International Business | Overseas property investment and development | Rockefeller Group (US), Paternoster Square (UK), Asian logistics & residential | Globalised earnings hedge; growth focus |

| Investment Management | REIT sponsorship, private real estate funds | Japan Real Estate Investment Corporation, MEC Global Partners | Fee-based; capital-light |

| Architectural Design & Engineering | In-house architecture, project management, consulting | Mitsubishi Jisho Sekkei design firm | Strategic capability; supports core development |

| Real Estate Services | Brokerage, property management, hotels | Mitsubishi Jisho House Net, Royal Park Hotels | Diversification; consumer-facing touchpoints |

Rockefeller Center: the deal that defined the bubble — and the unwind

No transaction in Japanese corporate history is more frequently cited as a symbol of the late-1980s asset bubble than Mitsubishi Estate’s 1989 acquisition of a controlling stake in Rockefeller Group, the New York real estate company that owns Rockefeller Center. The headline price — roughly 846 million dollars for an initial 51 percent stake, ultimately raised toward an 80 percent position — coincided with a wave of high-profile Japanese acquisitions in the United States and featured on magazine covers worried about an American economy being swallowed by Tokyo money. The symbolism was reinforced by the property itself: thirteen skyscrapers around an ice rink at the heart of midtown Manhattan.

The financial outcome was less satisfying than the symbolism. Rockefeller Center carried heavy leverage, underlying leases made cash flow more fragile than headline rent rolls suggested, and the early-1990s Manhattan office downturn arrived almost as soon as the acquisition completed. By 1995 the trophy property had filed for Chapter 11 bankruptcy protection. Mitsubishi Estate took substantial write-downs and divested most of its direct ownership interest, while retaining a strategic stake in the surviving Rockefeller Group property-management and development business.

What is less appreciated abroad is that the Rockefeller Group platform has been quietly rebuilt. Rockefeller Group International continues to operate as a Mitsubishi Estate subsidiary, focused on office and industrial development across the eastern United States — particularly New York, New Jersey, Washington, D.C. and selected sunbelt markets. The trophy ice rink may be gone from the balance sheet, but the operating platform survived the unwind, and it is now the vehicle for a much more disciplined U.S. strategy.

London, Paternoster Square and the British footprint

Less famous but more financially successful is the London business. In 2007 the company acquired the Paternoster Square development next to St. Paul’s Cathedral — a mixed-use estate including the home of the London Stock Exchange and a cluster of office buildings let to global investment banks and law firms. A steady accumulation of City and West End office assets followed, and over two decades Mitsubishi Estate has emerged as one of the larger Asian-owned landlords in central London.

The UK strategy has included shopping-centre and mixed-use investment, joint-venture development with British partners and selective sale of stabilised assets to recycle capital. Unlike the bubble-era Rockefeller transaction, the London build-out has been executed with conservative leverage and patient hold periods, delivering the kind of pound-denominated earnings stream that helps offset yen weakness in consolidated accounts.

Outside the U.S. and U.K., the international business now spans logistics warehousing in Southeast Asia, residential development in Australia, and selective data-centre and industrial investments. The overseas portfolio remains small relative to the Marunouchi engine, but its strategic role is significant: it is where management has chosen to allocate the bulk of incremental growth capital over the past decade.

The duopoly with Mitsui Fudosan

To outside observers, Mitsubishi Estate and Mitsui Fudosan look like near-mirror images: both descended from pre-war zaibatsu, both diversified across offices, residential, retail and overseas, both listed in Tokyo with comparable market capitalisation. In practice the two firms have evolved into distinct strategic styles.

Mitsubishi Estate is the Marunouchi specialist. Its identity is bound up with a single high-value district, its redevelopment cycle is anchored to that cluster, and its commercial property segment dominates earnings to a degree no peer matches. Mitsui Fudosan, by contrast, controls more of Nihonbashi, runs a much larger urban shopping-centre business through its LaLaport and Mitsui Outlet Park brands, has been more aggressive in retail-led mixed-use development in places like Toyosu and Tokyo Bay, and operates a substantial hotel and resort portfolio. Mitsui’s overseas mix is more geographically diversified, with significant residential and office presence in the U.S., Asia and Europe.

The contrast plays out in valuations. Mitsubishi Estate tends to be valued on the embedded-value of its Marunouchi land and the predictable cash flow of its office leasing book. Mitsui Fudosan is valued on a broader growth narrative across retail, hospitality and international development. Investors who want near-pure-play exposure to corporate-headquarters Tokyo real estate buy Mitsubishi Estate; investors looking for a more diversified consumer-and-office mix tilt toward Mitsui Fudosan.

Net zero by 2050 and the redevelopment dividend

The redevelopment cycle is also the company’s principal lever for decarbonisation. Mitsubishi Estate has committed to net-zero greenhouse gas emissions across its operations and value chain by 2050, with interim targets aligned to science-based pathways. Because the company controls the entire life cycle of its core buildings, it can pull each redevelopment forward into low-carbon specifications without negotiating with third-party owners.

Recent projects have adopted on-site renewable supply contracts, district energy systems shared across multiple Marunouchi blocks, low-embodied-carbon concrete and steel, and elevated tenant-fit-out standards that ratchet down operational energy intensity. The Tokyo Torch project at Tokiwabashi, a multi-phase Otemachi redevelopment anchored by what will be one of Japan’s tallest towers, was designed from inception around district-scale sustainability targets. Investors increasingly cite Mitsubishi Estate as a beneficiary of the redevelopment dividend — the rare position in which a landlord’s portfolio is structurally on a path to be rebuilt at higher specifications anyway.

Governance and the questions ahead

Mitsubishi Estate’s governance reflects its origin as a flagship Mitsubishi-group company. Junichi Yoshida assumed the presidency in April 2024, succeeding to operational leadership of a firm whose strategic direction is set on a generational cadence. The board operates within the framework expected of a Tokyo Stock Exchange Prime Market listing, but the cultural pull of the Mitsubishi keiretsu — the kinyokai Friday group of affiliated companies — remains a soft but real influence on capital allocation, tenant relationships and cross-shareholdings. Investor-relations communication has shifted over the past decade toward sharper disclosure of return on equity and capital-recycling discipline, partly in response to overseas institutional investors vocal about the gap between the stock price and the appraised value of the Marunouchi land bank.

The strategic questions ahead are recognisable to any single-district landlord with global aspirations. Can Marunouchi sustain its pricing premium as Otemachi and Toranomon offer competing grade-A supply at lower headline rents? Can the overseas business generate returns that justify the management bandwidth it consumes? Can the company navigate the demographic squeeze on residential demand without overcommitting to a condominium market that will shrink in the medium term?

Mitsubishi Estate’s answers, articulated across recent medium-term plans, are characteristically patient. Defend Marunouchi’s premium through quality and cluster stewardship rather than aggressive pricing. Expand selectively overseas where the brand can compete on operational quality rather than balance-sheet scale. Tilt incremental investment toward data centres, logistics and life-sciences real estate. And maintain the redevelopment cycle as both a competitive moat and a transition-finance opportunity.

For overseas investors, corporate occupiers and infrastructure partners thinking about Japan, Mitsubishi Estate is less a single-name investment than a long-duration call option on the continued centrality of the Marunouchi-Otemachi corridor in the global economy.

FAQ

How did Mitsubishi Estate come to own so much of Marunouchi?

The land was sold by the Meiji government to Yanosuke Iwasaki of the Mitsubishi family in 1890 as a single 35-hectare parcel after the army training grounds on the site were relocated. The Iwasaki family commissioned British architect Josiah Conder to design Japan’s first Western-style office blocks there, opening Mitsubishi Ichigokan in 1894. Mitsubishi Estate was formally incorporated in 1937 to consolidate the Mitsubishi zaibatsu’s property holdings, and the Marunouchi land bank — preserved through wartime, the post-war zaibatsu dissolution and successive redevelopments — has remained continuously in the company’s ownership for more than 130 years. Today Mitsubishi Estate controls roughly thirty buildings inside the Otemachi-Marunouchi-Yurakucho district.

What happened to Mitsubishi Estate’s Rockefeller Center investment?

Mitsubishi Estate acquired a controlling stake in Rockefeller Group in 1989 for an initial price of approximately 846 million dollars, eventually accumulating around 80 percent of the company. The acquisition coincided with the late-1980s Japanese asset bubble and a downturn in the Manhattan office market; Rockefeller Center filed for Chapter 11 bankruptcy protection in 1995 and Mitsubishi Estate took significant write-downs, divesting most of its direct ownership of the trophy property. However, Rockefeller Group International remained a Mitsubishi Estate subsidiary and has been rebuilt as a disciplined U.S. office and industrial development platform focused on the New York metropolitan area, the Mid-Atlantic and selected sunbelt markets.

How does Mitsubishi Estate differ from Mitsui Fudosan?

Both companies descend from pre-war zaibatsu and overlap in offices, residential and overseas property, but their centres of gravity differ. Mitsubishi Estate is anchored in the Marunouchi-Otemachi office district, with roughly thirty buildings inside the central Tokyo cluster and a commercial property segment that dominates group earnings. Mitsui Fudosan is more diversified into retail through its LaLaport and Mitsui Outlet Park shopping centres, has a larger hospitality and resort footprint, and operates a more geographically distributed international portfolio. Investors who want concentrated exposure to corporate-headquarters Tokyo real estate tend toward Mitsubishi Estate; those preferring a broader retail-and-mixed-use mix tilt toward Mitsui Fudosan.

What is Mitsubishi Estate’s international business focused on?

The international business spans the United States, the United Kingdom and selected Asian markets. In the U.S., Rockefeller Group International develops and manages office and industrial assets, principally in the New York metropolitan area, New Jersey and Washington, D.C. In the U.K., Mitsubishi Estate owns the Paternoster Square estate next to St. Paul’s Cathedral — including the London Stock Exchange building — and a portfolio of City and West End office assets accumulated since 2007. Across Asia and Australia, the company has built positions in logistics warehousing, residential development and selective data-centre projects. The overseas footprint remains small relative to the Marunouchi engine, but it is where management has allocated the bulk of incremental growth capital over the past decade.

How is Mitsubishi Estate approaching decarbonisation?

The company has committed to net-zero greenhouse gas emissions across its operations and value chain by 2050, with interim targets aligned to science-based pathways. Because Mitsubishi Estate controls the design, construction, operation and eventual redevelopment of its core buildings, it can pull each new project forward into low-carbon specifications — on-site renewable supply contracts, district energy systems, low-embodied-carbon construction materials and elevated tenant fit-out standards. The Tokyo Torch redevelopment at Tokiwabashi in Otemachi, anchored by what will be one of Japan’s tallest towers, has been designed from inception around district-scale sustainability targets.

Working with Mitsubishi Estate

For overseas occupiers seeking a Marunouchi or Otemachi headquarters address, for institutional capital partners considering co-investment in Tokyo office or logistics assets, and for brands looking to anchor flagship retail space in central Tokyo, Mitsubishi Estate is the unavoidable counterparty in the country’s most strategically located property cluster. Japonity introduces qualified overseas companies, investors and operators to Japanese real estate landlords, asset managers and developers through its business matching service. If you are exploring a Tokyo office lease, a real estate joint venture, a flagship retail location or a co-investment with a Japanese landlord, get in touch to start a conversation.

Related from Japonity — Japan’s real estate giants

- Mitsui Fudosan — The aggressive developer — Mid-Town, LaLaport, 50 Hudson Yards

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →