Yamato Holdings Co., Ltd. — better known to most of Japan by the parent-and-kitten silhouette of its Kuroneko (Black Cat) Yamato brand — moves approximately 2.5 billion parcels a year through its Takkyubin home-delivery network, the highest single-operator volume in the country and roughly 40-plus per cent of the domestic parcel market. It is the company that taught Japan to ship perishables, ski gear, golf clubs, and refrigerated osechi across the archipelago overnight. It is also, since January 2024, the company that very publicly began unwinding parts of its capacity-sharing relationship with Amazon Japan — a decision that exposed the structural collision between Japanese labour-compliance reform, e-commerce volume growth, and a domestic last-mile that had been quietly subsidising the cheapest fulfilment promises on the internet.

A brand older than the parcel business it invented

Yamato Transport was founded in 1919 in Tokyo by Yasuomi Ogura, a generation before the postal monopolies and rail networks that would shape twentieth-century Japanese logistics. For its first five and a half decades the company was a commercial trucker — moving cargo for department stores, factories, and government clients — competing within the narrow margins of B2B freight against larger rivals like Nippon Express. It was a successful but unremarkable business inside an industry that had no household consumer brand.

The break came in 1976, when Masao Ogura — the founder’s son and then president — launched Takkyubin (宅急便), a door-to-door parcel service aimed at individual senders. The proposition was radical for its time: a single flat price per size category, pickup from the sender’s home, next-day delivery to anywhere in Japan, and a service-quality guarantee. Japan’s parcels at the time were handled almost entirely by the state-owned postal service or by ad-hoc rail-freight arrangements; neither offered a credible consumer product. Takkyubin’s first-year volume was modest, but within a decade it had reframed the category. The Kuroneko Yamato mark — a black mother cat carrying a kitten in her mouth, suggesting careful handling — became one of the most recognisable corporate logos in Japan.

The corporate structure was reorganised in 2005, when the operating company spun its listed parent into Yamato Holdings Co., Ltd., with Yamato Transport Co., Ltd. continuing as the principal operating subsidiary alongside a cluster of adjacent businesses in moving, e-commerce fulfilment, financial settlement, and Asian cross-border logistics. The head office sits in Tokyo’s Chuo Ward, in the Ginza district.

The Takkyubin franchise and what it actually is

Takkyubin is best understood not as a delivery service in the Western sense, but as a piece of Japanese consumer infrastructure. Roughly 2.5 billion parcels a year — about 7 million on an average day, with peaks well above that during the December gift season and the early-summer mid-year gift cycle — flow through the network. Convenience stores act as drop-off and pickup points at nearly every major chain. Yamato’s own service counters in residential neighbourhoods accept walk-in shipments. A national grid of distribution centres and route trucks delivers within 24 to 48 hours across almost the entire country, including specialised cold-chain (Cool Takkyubin) and time-of-day options.

The economics of this network are built on density. Last-mile parcel delivery has near-zero marginal cost when a driver is already passing a given street; the same driver visiting that street with one parcel instead of twelve is the difference between profit and loss. For most of the post-1976 period, Yamato’s density advantage over rivals — particularly outside major metropolitan areas — was structural, and it translated into pricing power and margin stability that the broader Japanese trucking industry rarely enjoyed.

| Operator | Approx. share of Japan parcel market | Brand/service identifier | Strategic profile |

|---|---|---|---|

| Yamato Transport (Yamato Holdings) | ~40-45% | Kuroneko Yamato / Takkyubin | Largest network, premium service tier |

| Sagawa Express (SG Holdings) | ~25-30% | Hikyaku | B2B-leaning, recent gains in B2C from Amazon shift |

| Japan Post | ~20-25% | Yu-Pack | Universal-service mandate, postal integration |

| Other (DHL, FedEx, regionals, Amazon Flex) | ~5-10% | Various | Cross-border and gig-style capacity |

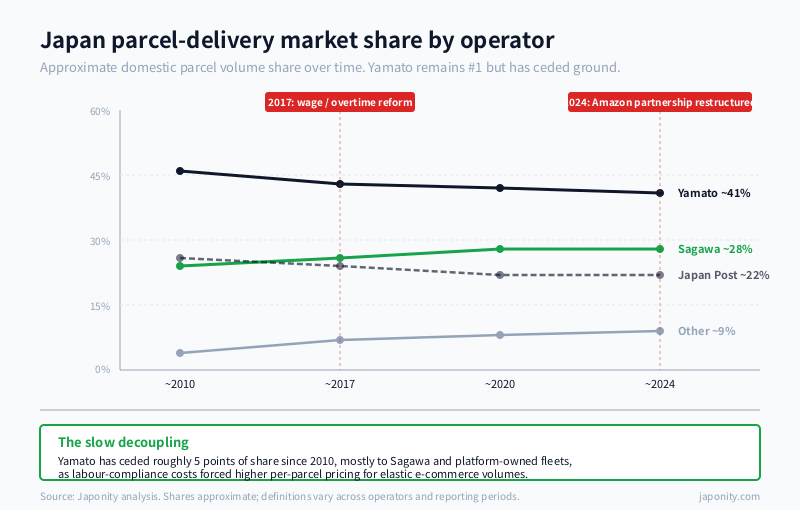

Shares are approximate, fluctuate quarter to quarter, and are reported under inconsistent definitions across operators (parcels versus all small freight, B2B versus B2C, etc.). What is not in dispute is the order: Yamato, Sagawa, Japan Post, with a long tail of regional and international carriers and the more recent intrusion of e-commerce platforms operating their own delivery fleets.

The 2017 reckoning: when Takkyubin had to raise prices

For most of its history Takkyubin’s pricing barely moved. The same Y1,000-range flat fee for a typical box-sized shipment held year after year, even as e-commerce drove parcel volumes from roughly 1 billion a year in the early 2000s to nearly twice that by the mid-2010s. The model assumed that volume growth could be absorbed by adding routes and capacity at the margin. What it did not assume — and what eventually broke — was that the underlying driver labour pool could grow with it.

In 2017, internal whistleblowing and union pressure surfaced widespread overtime-payment compliance failures at Yamato Transport, with thousands of drivers identified as having worked unpaid hours over a multi-year period. The company announced a large back-pay programme — reported at the time at approximately Y19 billion — and, more consequentially, accepted that the existing operating model could not be sustained without structural change. Three things followed in quick succession. Yamato raised base Takkyubin tariffs for the first time in twenty-seven years. It capped daily parcel volumes for high-volume contract shippers. And it began renegotiating per-parcel rates with its largest e-commerce customer.

That largest customer was Amazon Japan.

The Amazon Japan problem

Amazon entered Japan in 2000 and over the following decade and a half built the country into one of its largest international markets. From the start, the bulk of Amazon Japan’s last-mile delivery sat on Yamato’s network — the operator with the country’s deepest residential coverage and most reliable next-day service. That partnership made Amazon’s “free Prime delivery” promise economically credible in Japan in a way that few other markets matched. It also concentrated a disproportionate share of Yamato’s parcel volume on a single customer paying near the bottom of the company’s pricing schedule.

The 2017 rate renegotiation began to rebalance that relationship. Yamato pushed Amazon’s per-parcel pricing upward and signalled that capacity for Amazon volumes would be controlled rather than elastic. Amazon’s response, over the following years, was to diversify its delivery base: shifting volume to Sagawa for parts of the country, expanding its own AmazonFlex gig-driver network for dense urban routes, contracting with smaller regional carriers, and in some segments running an in-house Amazon Logistics operation. By the early 2020s, Yamato was no longer the dominant carrier of Amazon Japan parcels in the way it had been a decade earlier.

In January 2024, Yamato formally announced a further restructuring of the partnership, including the transfer of certain Amazon-related delivery volumes — particularly mail-format small items — that had been carried under specific contract arrangements. The company framed the move as part of its broader cost-discipline programme; the trade press read it as the latest stage in a multi-year decoupling. Either reading is consistent with the same underlying fact: Yamato is no longer willing to be the price-taker for Japan’s largest e-commerce platform, and Amazon Japan no longer needs Yamato to be its primary last-mile.

What the segments look like behind the headline business

Yamato Holdings is not a one-product company, although the parcel business dominates the group P&L. Reporting categories have been reorganised in recent years, but the practical segments break out roughly as follows. Retail and Industrial parcel delivery — the Takkyubin core and its B2B counterpart — generates the majority of group revenue and is the company’s principal margin engine on a normalised basis. E-Business and contract logistics encompasses warehousing, fulfilment, and supply-chain services for corporate customers, including the platforms-and-3PL businesses that have absorbed more investment as Takkyubin volumes have plateaued. Home Convenience covers moving services, on-demand household pickups, and the consumer-side adjacencies that draw on the same driver network. International logistics — historically smaller and more cyclical — covers cross-border forwarding, particularly within Asia, and has been a focus of selective M&A.

The strategic rationale of this portfolio has shifted. In the 1990s and 2000s, the adjacencies functioned as natural extensions of a driver-heavy network with spare capacity. Since 2017, the logic has inverted: as the parcel core has had to absorb wage and compliance costs that compress margin, the higher-margin contract logistics and B2B platform businesses are being positioned as the growth lever. Yamato is, in effect, trying to look more like a diversified logistics group and less like a parcel monopoly.

Driver labour and the structural ceiling

Behind every story about Japanese parcel volume sits the same demographic constraint. The country’s working-age population has been shrinking for over two decades, and the truck-driver labour pool has shrunk faster than the average, weighted toward older drivers approaching retirement. In April 2024, new regulations capping truck-driver overtime hours — colloquially the “2024 problem” — formally came into effect, tightening the supply of available driving labour at exactly the moment that e-commerce growth was projected to drive parcel volumes higher.

The implication is that the marginal cost of a parcel in Japan is rising even if fuel and fixed costs stay flat. Yamato’s response has been twofold: invest in automation and sorter throughput at distribution centres to reduce the labour content per parcel, and continue to raise prices for the volume-elastic part of its customer book (large e-commerce platforms) while protecting the consumer-facing Takkyubin tariff. The company has also expanded its convenience-store and locker-based delivery options, both to reduce the failed-delivery re-attempt rate (a major source of unproductive driver hours in Japan, where a high share of residential deliveries historically missed the recipient on the first attempt) and to push some of the last-mile labour cost off the driver and onto the customer.

Leadership and governance

Yamato Holdings has been led by a sequence of presidents drawn from inside the operating business, in keeping with the company’s strong internal-promotion culture. Makoto Kigawa served as president and chairman through the early 2010s and remains a defining figure in the company’s modern strategy. The current president and representative director, Yutaka Nagao, took the role in April 2024, taking over the executive direction of the group through the post-Amazon-restructuring period and the implementation of the 2024 driver-hour regulations. Investors generally read the current leadership as cost-disciplined and willing to accept slower top-line growth in exchange for margin recovery — a posture that contrasts with the volume-maximising mindset of the pre-2017 era.

The investor case, and what to watch

For investors and corporate counterparties, the Yamato thesis turns on three variables. First, can the company raise per-parcel pricing fast enough to outrun labour-cost inflation? The 2017-2024 cycle suggests yes, but only with material customer churn at the bottom of the price book. Second, can the contract logistics and B2B platform businesses scale to a size where they materially reshape the group margin, rather than remaining adjacencies? This is the harder bet; the competitive set there includes Mitsui-Soko, Nippon Express, and global 3PLs with deeper international networks. Third, what happens to the parcel-market structure when Amazon, Rakuten, and other platforms continue building their own delivery capacity — does Yamato re-emerge as the premium-tier carrier for everything those platforms cannot or will not move, or does it lose share at the high end as well?

For foreign companies looking at Japan, Yamato is also the cleanest single proxy for understanding Japanese last-mile logistics. Cross-border sellers, perishable exporters, subscription-box operators, and DTC brands all eventually have to make a decision about which network — Yamato, Sagawa, Japan Post, or a platform’s own fleet — to depend on. The pricing, capacity, and service-tier choices that get made in those decisions are increasingly driven by the same forces visible in Yamato’s own financials: an ageing driver workforce, a regulator that has decided unpaid overtime is no longer tolerable, and an e-commerce sector that grew faster than the country’s logistics labour supply could.

FAQ

What is the difference between Yamato Holdings and Yamato Transport?

Yamato Holdings Co., Ltd. is the listed parent company, established in its current form in 2005. Yamato Transport Co., Ltd. is the principal operating subsidiary that runs the Takkyubin parcel-delivery business under the Kuroneko Yamato brand. Other group subsidiaries operate adjacent businesses in moving services, contract logistics, e-commerce fulfilment, and international forwarding.

What is Takkyubin and why does it matter?

Takkyubin (宅急便) is Yamato’s branded door-to-door parcel-delivery service, launched in 1976. It introduced fixed-price, next-day, home-pickup-and-delivery parcels to Japan as a consumer product. The service effectively created the modern Japanese B2C parcel market and remains the country’s largest single delivery network, handling approximately 2.5 billion parcels a year.

How big is Yamato’s share of the Japanese parcel market?

Approximately 40 to 45 per cent of domestic parcel volume, depending on the definition used. Sagawa Express follows at roughly 25 to 30 per cent and Japan Post at approximately 20 to 25 per cent, with the remainder split among regional carriers, international integrators, and platform-owned fleets such as Amazon Flex.

Why did Yamato break with Amazon Japan in 2024?

The relationship was reshaped, not severed. After the 2017 driver overtime-compliance episode forced Yamato to raise prices and cap volumes for its largest customers, Amazon Japan progressively diversified its last-mile delivery across Sagawa, Amazon Flex, regional carriers, and its own logistics arm. In January 2024 Yamato announced a further restructuring that transferred certain mail-format small-item volumes off its network, formalising a years-long decoupling.

What is the “2024 problem” for Japanese logistics?

In April 2024, regulatory caps on truck-driver overtime hours came into effect, tightening the supply of available driving labour at the same time as e-commerce-driven parcel volumes continue to rise. The combination puts upward pressure on per-parcel costs across the industry and is the proximate cause of the latest round of Yamato tariff increases and capacity-rationing decisions.

Working with Yamato Holdings

Yamato Holdings is the natural counterparty for any organisation moving small parcels at scale in Japan — including cross-border sellers, perishable exporters, subscription-commerce operators, and DTC brands evaluating last-mile partners. If you are scoping a Japanese fulfilment build, benchmarking carrier pricing across Yamato, Sagawa, and Japan Post, or assessing logistics partners for a Japan market-entry plan, Japonity can introduce qualified contacts and structure a market-fit conversation. Start with our business-matching service.

Related from Japonity — Japan’s retail and last-mile logistics

- Seven & i Holdings — The convenience-store empire targeted by Couche-Tard

- Aeon Group — Japan’s biggest retailer by sales — and ASEAN’s largest mall network

- Lawson — The konbini now jointly owned by Mitsubishi Corp and KDDI

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →