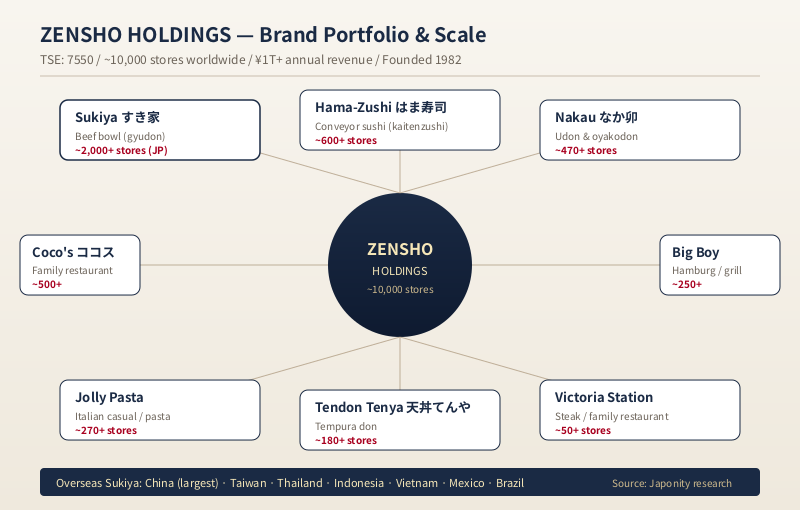

Approximately 10,000 stores worldwide. Around ¥1 trillion in annual revenue. The largest beef-bowl chain in Japan — Sukiya, with roughly 2,000+ outlets, more than Yoshinoya. Conveyor-belt sushi at scale through Hama-Zushi. Family restaurants via Coco’s and Big Boy. And a 44-year founder-CEO, Kentaro Ogawa, who started with a single Sukiya counter in Yokohama in 1982 and has compounded the business into the country’s largest restaurant operator by sales. Zensho Holdings (TSE: 7550) is not the most famous Japanese restaurant brand abroad. But by store count, revenue, vertical integration and overseas pace, it has quietly become the most consequential.

From one Yokohama counter to a ¥1 trillion empire

The Zensho story is, in many ways, the longest continuous founder-led compounding story in Japan’s restaurant industry. In June 1982, a 33-year-old Kentaro Ogawa — a former Yoshinoya manager — opened a single Sukiya beef-bowl shop in Yokohama. The concept was almost defiantly unoriginal: a cheap, fast bowl of beef over rice, the same dish that had defined Yoshinoya since the late 19th century. What was different was Ogawa’s conviction that the category had room for a second national champion, and that the second mover could win on price, menu variation and supply chain depth.

Forty-four years later, Ogawa is still chairman and CEO. Sukiya alone now operates approximately 2,000+ stores in Japan — more than Yoshinoya’s roughly 1,200 — and the parent group, Zensho Holdings, runs around 10,000 restaurants across more than a dozen brands and ten countries. Group revenue has crossed the ¥1 trillion mark, making Zensho the largest restaurant operator in Japan by sales, ahead of Skylark (the Gusto/Bamiyan operator) and McDonald’s Japan.

For a country whose food service sector is famous abroad mainly through individual brands — Yoshinoya, Mos Burger, Ichiran, Coco Ichibanya — Zensho’s quiet aggregation of categories is a structurally important story. It is, in effect, Japan’s answer to Yum! Brands or Inspire Brands: a multi-format restaurant holding company built by acquisition and conversion, with one founder at the top and a deeply integrated upstream food supply chain.

The portfolio: one company, ten formats, 10,000 stores

Zensho’s distinguishing feature is breadth of format. Where Yoshinoya remains essentially a single-brand business and Skylark is concentrated in family restaurants, Zensho has assembled a portfolio that covers nearly every Japanese casual dining category — beef bowl, conveyor sushi, family restaurant, udon/oyakodon, hamburg steak, pasta, tempura, hand-pulled noodles — each operated at scale.

| Brand | Category | Approx. stores | Acquired / Founded |

|---|---|---|---|

| Sukiya (すき家) | Beef bowl (gyudon) | 2,000+ (Japan); overseas in 7+ countries | Founded 1982 |

| Nakau (なか卯) | Udon & oyakodon | 470+ | Acquired 2005 |

| Hama-Zushi (はま寿司) | Conveyor sushi (kaitenzushi) | 600+ | Founded by group 2002 |

| Coco’s (ココス) | Family restaurant | 500+ | Acquired from Skylark group |

| Big Boy | Hamburg steak / grill | 250+ | Acquired Japan rights from BBI USA |

| Jolly Pasta | Pasta / Italian casual | 270+ | Acquired |

| Victoria Station | Steak / family restaurant | 50+ | Acquired |

| Tendon Tenya (天丼てんや) | Tempura don | 180+ | Acquired 2018 |

| Ringer Hut affiliate / hand-pulled noodles | Chinese noodle & misc. | Various | Various |

| Group total | Multi-format | ~10,000 worldwide | — |

The economic logic of the portfolio is straightforward but rarely executed well in Japan: one back-end — central kitchens, frozen logistics, beef and rice procurement, a captive trading subsidiary in Australia and the United States for beef sourcing — feeds many front-ends. Sukiya’s gyudon, Nakau’s oyakodon and Hama-Zushi’s salmon nigiri sit on top of a shared procurement layer that gives Zensho leverage no single-brand peer can match. Beef bought for Sukiya’s bowls underwrites the hamburg steaks at Big Boy and the steak plates at Victoria Station. Rice contracts negotiated for Sukiya are amortised across Nakau’s udon sets and Hama-Zushi’s nigiri.

Why Sukiya, not Yoshinoya, became Japan’s largest beef-bowl chain

Outside Japan, Yoshinoya is the better-known name — the orange-and-black sign, the 19th-century origin story, the listing in New York. Inside Japan, Sukiya has been the larger operation by store count for over a decade. The reasons are instructive for anyone studying Japanese consumer markets.

First, menu breadth. Yoshinoya stayed close to its original lineup for decades — gyudon, a few variants, curry, breakfast sets. Sukiya from the mid-1990s pushed aggressively into cheese gyudon, kimchi gyudon, ontama (poached egg) gyudon, eel sets, curry, even a vegetarian-friendly nasubi (eggplant) variant. The result was higher average ticket, more daypart coverage and stronger appeal to families and women — a segment Yoshinoya historically under-indexed against.

Second, suburban roadside expansion. Yoshinoya is heavily weighted to urban station-front locations. Sukiya, from the outset, built a roadside-friendly format with parking lots and drive-through-style takeaway, making it the default beef bowl of suburban Japan and small-city ring roads. As Japanese consumption shifted toward car-based suburban life over the 2000s and 2010s, Sukiya’s geographic mix paid off.

Third, price discipline through vertical integration. Zensho’s captive trading and processing operations — beef from Australia and the United States, rice purchased on long-term contracts, central commissaries — let Sukiya hold its standard gyudon at a low end of the market for long stretches. Yoshinoya, dependent more on third-party suppliers, has historically had less flexibility.

Zensho vs Skylark vs Yoshinoya: three different bets

The Japanese listed restaurant universe is dominated by three groups, each with a distinctly different strategy.

Skylark Holdings bet on family restaurants — Gusto, Bamiyan, Jonathan’s, Syabu-yo — concentrated in Japan, with a recent push into delivery and table-side robots. Its revenue is roughly ¥350 billion, store count around 3,000, and overseas presence modest.

Yoshinoya Holdings bet on a focused beef-bowl franchise with selective international expansion — Hanamaru Udon, Withlink and overseas Yoshinoya stores in the US, Southeast Asia and China. Revenue is in the ¥170 billion range, group stores around 3,000 including overseas.

Zensho bet on multi-format aggregation plus aggressive Sukiya overseas. Revenue passed ¥1 trillion. Store count around 10,000. By any of the standard metrics — revenue, store count, vertical integration depth — Zensho has built the largest operation of the three, and by some margin.

What is striking is that this gap has widened over the past decade, not narrowed. Skylark has been working through demographic headwinds in the family restaurant category. Yoshinoya has been managing through public controversies and a more cautious overseas pace. Zensho has compounded, year after year, by buying brands in adjacent categories — Coco’s, Big Boy, Jolly Pasta, Tendon Tenya — and adding store density in regions and dayparts where its existing brands were under-represented.

Overseas: Sukiya’s quietly aggressive playbook

Yoshinoya is the Japanese beef bowl that most non-Japanese consumers have heard of abroad, thanks to a US presence that dates back to the 1970s. But measured by overseas store count and pace of opening over the past five years, Sukiya is now arguably the more globally aggressive operator.

Sukiya operates in China (its largest overseas market, with stores in Shanghai, Beijing and a growing list of secondary cities), Taiwan, Thailand, Indonesia, Vietnam, Mexico and Brazil. The Brazil operation is particularly interesting: a Sukiya store in São Paulo serves both gyudon to Japanese-Brazilian diaspora communities (Brazil hosts the largest Japanese-descended population outside Japan) and curiosity-driven Brazilian diners discovering the format. Mexico is a more recent push.

The strategic logic of Sukiya overseas is different from Yoshinoya’s. Yoshinoya has tended to position itself as a Japanese cultural export — the original gyudon, with the brand’s heritage as part of the proposition. Sukiya positions itself more as an everyday value chain: cheap, fast, customisable, family-friendly. In China, that has made it competitive against local fast-food formats rather than against premium Japanese restaurants. In Southeast Asia, it has fit into the mall food court and standalone roadside model with relatively little localisation drama.

The overseas footprint is still small relative to the Japan business — likely under 10% of total stores — but the growth rate is high enough that within a decade, Zensho’s overseas store count could realistically approach four figures.

Vertical integration: why Zensho looks more like a trading house than a restaurant chain

To understand why Zensho can run roughly 10,000 stores across so many formats without margin collapse, one has to look upstream. The group operates a network of captive procurement and processing subsidiaries that more closely resemble a small sōgō shōsha than a restaurant operator.

On beef, Zensho purchases from Australia and the United States directly through subsidiaries, processes domestically through its own plants, and runs a national cold-chain logistics operation. On rice, it has long-term contracts with Japanese producers and operates its own rice-milling. On seafood for Hama-Zushi, it has direct relationships with fisheries and aquaculture suppliers. On vegetables, it operates contract farms.

This vertical integration matters in two ways. First, it gives Zensho cost stability through commodity cycles — a defensive moat in an industry where most operators are price-takers on inputs. Second, it gives the group the ability to launch new brands or extend existing ones into new categories with confidence in the supply side. When Zensho added Tendon Tenya in 2018, the tempura oil and shrimp supply chain plugged into existing infrastructure rather than being built from scratch.

For inbound trading partners — particularly Australian beef exporters, American rice and protein suppliers, and Southeast Asian seafood producers — Zensho is among the most significant Japanese restaurant-sector counterparties to know.

The founder factor: 44 years of compounded conviction

Kentaro Ogawa, born in 1948, has been chairman and CEO of Zensho since founding Sukiya in 1982. That is by some distance the longest continuous founder-CEO tenure in Japan’s listed restaurant industry, and one of the longest in Japanese consumer business generally. By comparison, Yoshinoya has cycled through multiple leaders since the founding Matsuda family; Skylark is professionally managed; McDonald’s Japan is a subsidiary.

The founder factor has had two visible effects on the business. First, capital allocation has consistently favoured long-horizon, often counter-cyclical acquisitions — buying Coco’s from Skylark’s troubled period, picking up Big Boy Japan from a struggling US parent, taking Tendon Tenya off the market in 2018. Second, the group has remained relatively low-profile in mainstream English-language business media despite its scale, in part because Ogawa himself has cultivated a deliberately quiet leadership style.

The succession question is, inevitably, becoming more visible as Ogawa enters his late seventies. Zensho has not publicly named a clear successor outside the chairman track, and the management team has been progressively professionalised over the past decade. How the group navigates the post-founder transition — and whether it preserves the multi-brand discipline that distinguishes it from peers — will be one of the more consequential succession stories in Japanese consumer business in the coming decade.

What Zensho’s scale means for partners abroad

For non-Japanese companies, Zensho matters in three concrete ways.

First, as a buyer. The group is a major end-market for Australian beef, US rice and grain, Southeast Asian seafood and aquaculture, and Latin American agricultural products. Any supplier in those categories with credible scale should know Zensho’s procurement organisation.

Second, as a real estate counterparty. With roughly 10,000 stores, Zensho is among the largest restaurant-sector tenants in Japan, and one of the more important new-store openers in target Asian markets. Mall operators, developers and roadside-site brokers in China, Indonesia, Thailand and Vietnam routinely engage with Zensho on site pipelines.

Third, as a model. For US or European multi-brand restaurant groups studying how to operate a portfolio of formats on top of a shared back-end at national scale, Zensho is one of the most useful global case studies. It has done what Inspire Brands and Yum! have done in the US, but with a uniquely Japanese twist: deep vertical integration upstream, founder-led capital discipline, and an emphasis on suburban-and-roadside format rather than urban concentration.

FAQ

Is Zensho Holdings publicly listed?

Yes. Zensho Holdings is listed on the Tokyo Stock Exchange Prime Market under the ticker 7550. It is a constituent of major Japanese mid-and-large-cap indices and is widely held by domestic institutional investors and increasingly by overseas funds focused on Japanese consumer compounders.

Is Sukiya bigger than Yoshinoya in Japan?

Yes, by store count. Sukiya operates approximately 2,000+ stores in Japan, compared with roughly 1,200 for Yoshinoya. Sukiya overtook Yoshinoya in Japan store count over a decade ago and has maintained the lead since.

Does Zensho own Coco Ichibanya, the curry chain?

Not in full. Zensho has historically been associated with the broader Japanese restaurant industry’s ownership landscape, but Coco Ichibanya is a separately listed and operated company. Zensho operates its own curry offerings primarily through Sukiya’s curry menu and dedicated curry sub-brands rather than through Coco Ichibanya.

Where can foreign suppliers reach Zensho’s procurement function?

Zensho’s headquarters is in Minato-ku, Tokyo. Procurement is run through both the holding company’s centralised function and through dedicated trading subsidiaries — particularly for imported beef and seafood. Suppliers typically engage via Japanese trading houses, direct sales offices in source countries, or industry associations.

What is Zensho’s biggest overseas market?

China is currently Zensho’s largest overseas market by Sukiya store count, with operations in Shanghai, Beijing and an expanding set of secondary cities. Taiwan, Thailand, Indonesia, Vietnam, Mexico and Brazil are also active markets, with the Brazilian operation notable for serving the large Japanese-descended community in São Paulo.

Working with Zensho

If your company is an agricultural exporter, a food technology provider, a real estate developer with site pipeline in Japan or target Asian markets, or a brand looking at acquisition partnerships in Japan’s restaurant sector, Zensho is among the most consequential operators in the country to engage with. Japonity helps overseas partners identify the right entry points into Japan’s largest food service group — from beef and rice supply, to mall and roadside site development, to format and menu collaboration — through our business matching service.

Related from Japonity — Japan’s food retail, restaurants and konbini

- Seven & i Holdings — The convenience-store empire targeted by Couche-Tard

- Lawson — The konbini now jointly owned by Mitsubishi Corp and KDDI

- FamilyMart — The Itochu-owned konbini, five years after the take-private

- Yamazaki Baking — Japan’s bread-konbini double helix — supplying ~50% of konbini bread

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →