Walk into a DON DON DONKI on Singapore’s Orchard Road at one o’clock in the morning and the sensory load is immediate: a wall of fluorescent yellow price-tag posters in handwritten kanji, the recorded chime of “Miracle Shopping” looping at low volume, frozen wagyu and Hokkaido melon at one end, a tower of Calbee potato chips stacked four metres high at the other, a queue of tourists comparing tax-free receipts, and almost no clear sightlines between aisles. Repeat the experience in Hong Kong, Taipei, Bangkok and Kuala Lumpur — DON DON DONKI now operates more than thirty stores across Asia outside Japan — and the chain begins to look less like a quirky discount format and more like the most successful overseas projection of a Japanese retail concept since UNIQLO. Behind that store sign sits Pan Pacific International Holdings, Tokyo Stock Exchange code 7532, the company formerly known as Don Quijote Holdings, the most profitable major mass-retailer in Japan on a sales-per-square-metre basis. PPIH is the anti-Aeon — narrow where Aeon is federated, late-night where Aeon closes at ten, compressed where Aeon is sprawling — and its rise is a useful corrective to the idea that Japan’s retail giants all converge on the same suburban mall.

From an Asakusabashi thrift shop to a Tokyo-listed conglomerate

The chain’s founding story is closer to a Tokyo street-trader anecdote than a corporate origin myth. In 1980, Takao Yasuda, a former real-estate professional, opened a small thrift-and-discount shop called “Just” in Asakusabashi, a wholesale district in eastern Tokyo. The shop sold whatever Yasuda could acquire cheaply — bankruptcy stock, surplus inventory, end-of-season goods — and stayed open late into the night to catch shift workers on their way home. Yasuda discovered, almost by accident, that the busiest selling hours were after ten in the evening, and that customers seemed to enjoy the chaotic, packed-to-the-ceiling display that resulted from a shop with too much inventory and too little space.

The first store carrying the Don Quijote name opened in Fuchu, western Tokyo, in 1989, codifying that formula into a deliberate format: late-night hours, deep discounts, and a visual merchandising style the company called “compressed display” (atsuryoku chinretsu) or, more colourfully, “jungle merchandising.” Don Quijote Co., Ltd. listed on the Tokyo Stock Exchange in 1996 and adopted the Don Quijote Holdings name as it diversified. In 2019, reflecting the rapid growth of its overseas business, the holding company renamed itself Pan Pacific International Holdings. The corporate headquarters sit in Meguro, central Tokyo, and the group reports operating revenue measured in trillions of yen across a domestic store network exceeding seven hundred locations.

Compressed display and the economics of chaos

The single most important thing to understand about Don Quijote is that its store layout is not an accident, and it is not bad design. It is the operational engine of the business model. Where a typical Japanese GMS organises shelves in clean parallel rows with sightlines down each aisle, a Don Quijote store is designed to make the customer slow down, get slightly lost, and discover products by collision rather than by search. Ceiling-high stacks of cardboard cases, hand-lettered yellow price posters in dense clusters, narrow zigzag aisles, upbeat soundtracks, and an assortment that mixes cosmetics, instant noodles, suitcases, gold bars, sushi knives and fancy-dress costumes within metres of each other — none of this is haphazard. It is a deliberate productivity choice that solves a particular retail problem.

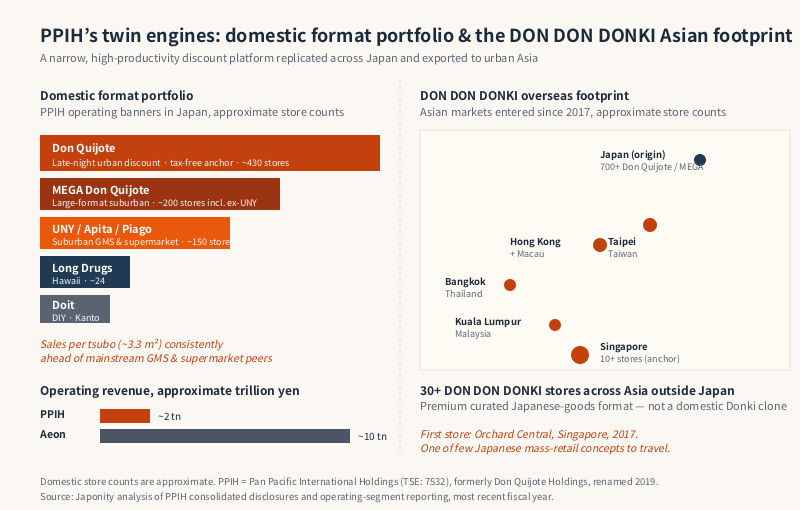

That problem is space. Japanese urban retail rents are among the highest in the world, and the productivity metric that matters for a discount retailer is sales per square metre, not sales per store. By packing roughly fifty thousand stock-keeping units into a footprint an Aeon GMS would fill with ten thousand, Don Quijote effectively buys five times the assortment depth from the same lease. The compressed display also turns browsing into entertainment, lifting average ticket size and dwell time. Industry observers credit Don Quijote with one of the highest sales-per-tsubo (one tsubo equals approximately 3.3 square metres) figures of any major Japanese retailer, comfortably ahead of mainstream supermarket and GMS chains.

Late-night opening hours compound the productivity advantage. Urban Don Quijote stores in Tokyo, Osaka and tourist districts often operate twenty-four hours, and even suburban locations typically stay open until two or three in the morning. The format captures four overlapping customer segments — shift workers, late-evening urbanites avoiding daytime crowds, group tourists landing in the evening who want to shop before sleeping, and the social-event impulse buyer looking for last-minute supplies. Few rival chains compete for any of them after ten in the evening.

The tax-free tourist channel

The second pillar of the model is dominance of the tax-free retail channel for inbound visitors. Japan’s consumption-tax-free shopping system has expanded dramatically over the last decade, and Don Quijote has built one of the most efficient tax-free counter infrastructures in the country. Major urban stores in Shinjuku, Shibuya, Ginza, Dotonbori and Asakusa devote significant floor space to multilingual tax-free counters, with staff conversant in Mandarin, Korean, Thai, English and Vietnamese.

The economic effect has been meaningful. Inbound tourism is a high-margin channel because foreign visitors buy higher-priced electronics, cosmetics and confectionery rather than the low-margin daily groceries that anchor a domestic basket. The chain is one of the largest single retail beneficiaries of the post-2013 inbound-tourism boom, and its store siting in central Tokyo and Osaka has been openly designed around proximity to tourist arteries and hotel clusters.

The format portfolio

Beyond the flagship Don Quijote banner, PPIH operates a deeper portfolio of domestic and overseas formats than most outside observers realise. The table below simplifies a complicated group structure that has expanded substantially through acquisitions over the last decade.

| Format / banner | Operating company | Positioning | Approximate footprint |

|---|---|---|---|

| Don Quijote | Don Quijote Co., Ltd. | Late-night urban discount, compressed display, tax-free anchor | Several hundred stores across Japan |

| MEGA Don Quijote | Don Quijote Co., Ltd. | Large-format suburban variant with full grocery | Roughly two hundred stores, including converted UNY locations |

| UNY / Apita / Piago | UNY Co., Ltd. | Suburban GMS and supermarket, central Japan stronghold | Approximately one hundred and fifty stores |

| DON DON DONKI | Pan Pacific Retail Management (Asia) | Premium Japanese-goods discount format for overseas markets | More than thirty stores across Singapore, Hong Kong, Taiwan, Thailand, Malaysia, Macau |

| Long Drugs | Long Drugs Stores, Ltd. | Hawaii-based grocery and drugstore chain | Roughly two dozen stores across the Hawaiian islands |

| Doit | Doit Co., Ltd. | Home centre and DIY format | Small chain in Kanto region |

| Other specialty | Various subsidiaries | Pet supplies, electronics, real-estate development | Niche footprints, group-supportive |

Two acquisitions in particular reshaped the group. In 2014, Don Quijote acquired the Long Drugs chain in Hawaii, gaining a foothold in a market that is both a tourism destination for Japanese travellers and an ethnic-Japanese consumer cluster in its own right. More transformatively, between 2017 and 2019 Don Quijote acquired a controlling stake in UNY Co., Ltd. — the central-Japan-based GMS and supermarket operator — from FamilyMart UNY Holdings (now FamilyMart Co., Ltd.), in a transaction that gave PPIH access to roughly one hundred and fifty UNY, Apita and Piago stores concentrated in Aichi, Gifu and surrounding prefectures.

The UNY acquisition was strategically unusual. UNY was a struggling traditional GMS operator with declining same-store sales. Don Quijote’s bet was that it could selectively convert UNY stores into MEGA Don Quijote locations, applying compressed-display and late-night hours to the larger format, while running the remainder as supermarket-anchored regional chains. Several years on, the thesis has played out as planned: dozens of former UNY stores have been re-flagged as MEGA Don Quijote with measurable productivity uplifts, while the unconverted UNY, Apita and Piago stores continue to serve as a base of grocery volume in central Japan.

DON DON DONKI: the only Japan-retail overseas play that actually works

The most interesting strategic story in PPIH today is DON DON DONKI, the overseas format that the group operates through Pan Pacific Retail Management (Asia). DON DON DONKI is not a clone of the Japanese Don Quijote. It is a deliberate repositioning: a premium curated Japanese-goods destination, with a heavier emphasis on Japanese-imported fresh food, frozen wagyu, sushi-grade seafood, Hokkaido dairy, Japanese fruit, ready-to-eat onigiri and bento, and branded snack and confectionery imports, sold in a compressed-display environment that retains the visual energy of the Japanese original.

The first DON DON DONKI opened in Singapore’s Orchard Central in 2017 and was an immediate commercial success. Singapore now hosts more than ten DON DON DONKI stores. Hong Kong followed with a Tsim Sha Tsui flagship, and the chain expanded to Taiwan, Thailand and Malaysia, with Macau also added. The overall overseas store count has now exceeded thirty, with most stores operating profitably and several flagship locations among the highest-grossing Japanese retail outlets anywhere outside Japan.

What makes DON DON DONKI strategically rare is that very few Japanese mass-retail concepts have travelled. Aeon’s overseas business is largely a Japanese suburban mall adapted for ASEAN. Seven-Eleven’s overseas success in the United States, Taiwan and Thailand depends substantially on local franchising. MUJI and UNIQLO are specialty rather than mass-retail. The mainstream Japanese supermarket and discount-store playbook has otherwise produced a long list of overseas failures over the past three decades. DON DON DONKI’s combination of premium positioning, Japanese-import sourcing, compressed-display theatre and late-night hours has cracked a code that most rivals have not even attempted.

The economic logic is distinctive. DON DON DONKI is not selling Japanese groceries cheaply to expatriates. It is selling the experience of being inside a Japanese discount store to an aspirational urban Asian consumer who associates Japanese branding with quality, safety and trend. The format converts brand affinity for Japan — built over decades by anime, tourism and consumer-electronics history — into measurable basket size in markets where Japan-themed retail had previously been fragmented across small specialty shops.

PPIH against the Japanese retail giants

The clearest way to understand PPIH’s position is to compare it with the two larger conglomerates, Aeon and Seven & i Holdings. On consolidated revenue, PPIH is the smaller player — roughly two trillion yen of operating revenue against Aeon’s ten trillion and Seven & i’s broadly similar figure. On operating margin and on sales productivity per square metre, however, PPIH consistently runs ahead of Aeon and is in the same conversation as Seven & i’s 7-Eleven Japan business.

The contrast is structural. Aeon’s model is to build a regional mall, cross-subsidise the format zoo with mall rental income, and capture middle-class suburban spending through breadth. PPIH’s model is to take a single high-productivity urban discount format and replicate it ruthlessly in tourist arteries, late-night neighbourhoods and former GMS sites converted into MEGA Don Quijote. Aeon optimises for share of wallet across a family’s whole week. PPIH optimises for the impulse basket, the tourist haul and the late-night purchase. Both strategies have produced durable businesses, but only PPIH has translated its domestic productivity into an overseas franchise that earns its own returns.

Governance, succession and the post-Yasuda generation

Takao Yasuda, the founder, stepped back from day-to-day management in the late 2000s and has remained a significant shareholder and supervisory presence rather than an operational chief executive. The group has cycled through several generations of management since, with Koji Ohara serving as a long-time president and group chief executive across much of the UNY acquisition, and Naoki Yoshida subsequently elevated into senior group leadership. The pattern resembles other large Japanese founder-led retailers — Fast Retailing and Nitori among them — where the founder retains symbolic weight while professional management runs the operating businesses.

The group’s medium-term plan, articulated across recent investor communications, leans on three vectors. First, continued conversion of UNY-format stores into MEGA Don Quijote and selective new openings in Japan. Second, aggressive overseas expansion of DON DON DONKI, with additional Asian openings and exploration of further markets beyond the current footprint. Third, deeper integration of the tourist-channel and tax-free infrastructure with inbound-tourism services such as multilingual payments, hotel partnerships and airport-arrival promotions.

What PPIH gets right that nobody else has copied

The temptation, when reviewing a successful Japanese retailer, is to attribute its performance to cultural factors — service standards, fresh-food quality, customer attentiveness — that are hard to replicate. PPIH cannot be explained that way. Don Quijote is, by Japanese retail standards, notably scruffy. The stores are crowded, the lighting is fluorescent, and the operational discipline of a 7-Eleven Japan is conspicuously absent. What PPIH has instead is a clear-headed view of three structural realities the rest of Japanese mass-retail has been slower to confront: urban floor space is the binding constraint on retail economics, tourist and late-night demand are durable rather than cyclical, and overseas Asian consumers will pay a premium for an authentic Japanese discount-store experience rather than a localised supermarket.

None of these insights are proprietary, and none require Japanese cultural capital to execute. They are, however, very difficult to combine into a coherent format without abandoning the comfort of suburban-mall conventionality. PPIH abandoned that comfort forty years ago in a thrift shop in Asakusabashi, and the rest of the industry is still catching up.

FAQ

Is Pan Pacific International Holdings the same company as Don Quijote?

Yes. Pan Pacific International Holdings (Tokyo Stock Exchange code 7532) is the renamed holding company that was previously known as Don Quijote Holdings. The company adopted the Pan Pacific name in 2019 to reflect the growth of its overseas business and the diversification of its format portfolio beyond the original Don Quijote banner. The flagship Don Quijote discount-store chain remains the largest operating subsidiary, and is sometimes referred to colloquially as “Donki.”

What is the difference between Don Quijote and DON DON DONKI?

Don Quijote is the original Japanese domestic discount-store banner, operating roughly seven hundred stores across Japan with late-night hours, compressed-display merchandising and a broad price-led assortment. DON DON DONKI is the overseas format, operated by Pan Pacific Retail Management (Asia), and is positioned as a premium curated Japanese-goods destination rather than a discount store. DON DON DONKI emphasises imported Japanese fresh food, frozen wagyu, Hokkaido dairy and branded confectionery, and operates more than thirty stores across Singapore, Hong Kong, Taiwan, Thailand, Malaysia and Macau.

How big is PPIH compared with Aeon and Seven & i Holdings?

PPIH is significantly smaller than either Aeon or Seven & i on top-line consolidated revenue. PPIH reports operating revenue measured in the low single-digit trillions of yen, against Aeon at approximately ten trillion yen and Seven & i in a broadly comparable range. On operating margin and on sales-per-square-metre productivity, however, PPIH ranks among the most efficient mass-retailers in Japan and outperforms Aeon’s general-merchandise-store segment on most comparable productivity metrics.

Why did Don Quijote acquire UNY?

PPIH acquired a controlling stake in UNY Co., Ltd. from FamilyMart UNY Holdings in stages between 2017 and 2019, gaining approximately one hundred and fifty UNY, Apita and Piago stores concentrated in central Japan. The strategic thesis was that selective UNY stores could be converted into MEGA Don Quijote large-format discount stores, applying the compressed-display playbook to a larger footprint, while the remaining UNY, Apita and Piago supermarkets would continue to serve as a base of grocery volume in the Tokai region. Several years on, dozens of conversions have been completed with measurable productivity uplifts.

What is Long Drugs and how does it fit into the group?

Long Drugs Stores, Ltd. is a grocery and drugstore chain in Hawaii that Don Quijote acquired in 2014, with roughly two dozen stores across the Hawaiian islands. The acquisition gave PPIH a foothold in a market that combines Japanese inbound tourism with a substantial ethnic-Japanese resident consumer base, and serves as a learning ground for overseas operational management distinct from the DON DON DONKI Asian format. Long Drugs operates under its own banner and is positioned as a local grocery chain rather than a Japan-themed retail concept.

Working with PPIH

For Japanese food manufacturers, branded consumer-goods suppliers, overseas private-label producers and inbound-tourism service partners, PPIH offers an unusually concentrated distribution opportunity in a Japanese retail landscape that is otherwise fragmented across hundreds of regional chains. The DON DON DONKI overseas format is also one of the few reliable channels for Japanese food and consumer-goods exporters to reach Asian urban consumers at meaningful scale without building their own retail footprint. Japonity introduces qualified overseas brands, exporters and capital partners to Japanese retailers, real-estate developers and consumer-goods operators through its business matching service. If you are exploring a Japan-market entry, a tax-free retail partnership, a DON DON DONKI sourcing relationship or a tourist-channel collaboration, get in touch to start a conversation.

Related from Japonity — Japan’s mass retail & discount giants

- Aeon Group — Japan’s biggest retailer by sales — and ASEAN’s largest mall network

- Nitori Holdings — Japan’s IKEA — the 36-year profit-growth streak

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →