In the geography of Japanese capitalism, Chubu Electric Power Co., Inc. (中部電力, TYO: 9502) occupies a singular position: the regional utility for the prefectures (Aichi, Mie, Gifu, Shizuoka, Nagano, parts of Fukui) that also happen to host Toyota Motor Corporation, the country’s largest manufacturing complex, and a constellation of suppliers whose electricity demand has shaped Japan’s industrial gravity for seventy years. Today Chubu Electric is two companies stitched into one. Through JERA — its 50/50 joint venture with Tokyo Electric Power Company (TEPCO) Fuel & Power, established in 2015 — it is the world’s largest single buyer of liquefied natural gas, with annual procurement of roughly 30+ million tonnes. And as a domestic utility, it remains the operator of Hamaoka Nuclear Power Plant, the five-reactor Shizuoka facility that has sat idle since May 2011, when then-Prime Minister Naoto Kan requested a voluntary shutdown citing seismic risk. The contrast — global LNG kingmaker abroad, politically stranded nuclear operator at home — defines Chubu Electric’s strategic position better than any single financial metric.

The Toyota utility

Chubu Electric was founded on May 1, 1951, as part of the postwar reorganization that split Japan’s electricity sector into nine regional monopolies, each with vertical integration over generation, transmission, and retail in its geographic service area. The company drew the territory covering Aichi, Mie, Gifu, Shizuoka, Nagano, and parts of Fukui — collectively the Chubu region — and headquartered itself in Nagoya, the manufacturing capital that would become synonymous with Toyota and its supply chain.

That geographic accident shaped everything. The Chubu region today produces approximately a third of Japan’s manufacturing output by value, anchored by Toyota Motor in Toyota City, Aichi, and rippling outward through Denso, Aisin, Toyota Industries, JTEKT, Toyota Tsusho, and thousands of tier-2 and tier-3 suppliers. Automotive assembly, machine tools, ceramics, chemicals, and precision components — all electricity-intensive — give Chubu Electric a customer mix that skews heavily industrial and high-load-factor compared with TEPCO (Kanto, more residential and commercial) or Kansai Electric (Osaka manufacturing, also industrial but more diversified).

The relationship with Toyota is not merely commercial. Toyota Tsusho, Toyota’s general trading arm, holds an equity stake in Chubu Electric and has long been a partner in fuel procurement and overseas energy projects. The utility’s load profile, its capital expenditure cycles, and even its political stance on energy policy have been calibrated, implicitly or explicitly, to keep one of the world’s largest industrial customers competitive against Korean, German, and Chinese rivals whose home utilities offer cheaper power.

Hamaoka: the nuclear plant that stopped

For decades, Chubu Electric’s answer to industrial electricity demand was Hamaoka Nuclear Power Plant, a five-reactor complex in Omaezaki, Shizuoka Prefecture, sited directly on the Pacific coast above the predicted epicentre of a long-anticipated Tokai megathrust earthquake. Hamaoka was, in the planning logic of the 1970s and 1980s, the obvious site: close to Tokyo Bay’s transmission backbone, close to Chubu’s industrial load centre, and on land that the utility could secure. The seismic exposure was acknowledged but managed through engineering.

That calculus collapsed on March 11, 2011. Two months after Fukushima Daiichi failed under combined seismic and tsunami loading, then-Prime Minister Naoto Kan publicly requested that Chubu Electric voluntarily suspend operations at Hamaoka. The request was politically extraordinary — Kan had no statutory authority to order a shutdown — but Chubu Electric complied, taking units 4 and 5 offline (units 1 and 2 had already been retired, and unit 3 was already in periodic inspection). The entire plant has remained idle since.

The restart politics at Hamaoka differ materially from those at Kansai Electric’s Ohi and Takahama plants in Fukui Prefecture, which have returned to service since 2018. Three factors compound the difficulty. First, the Tokai earthquake risk is uniquely high — Japan’s Cabinet Office officially designates the area as a high-probability seismic zone. Second, Shizuoka’s prefectural governor, like several of his predecessors, has remained sceptical of restart, and local consent under the Nuclear Regulation Authority’s post-Fukushima review framework is politically necessary even where not strictly legally binding. Third, the plant sits in an evacuation-difficult coastal corridor between Tokyo and Nagoya, magnifying the political cost of any safety incident.

Chubu Electric has invested heavily — by reported estimates well above ¥400 billion — in tsunami walls, seismic reinforcement, and filtered venting systems at Hamaoka. As of 2026 the company maintains its formal intention to restart units 3 and 4 once Nuclear Regulation Authority review concludes and local consent is obtained. The market, however, prices Hamaoka largely as a stranded asset.

JERA: the workaround that became the strategy

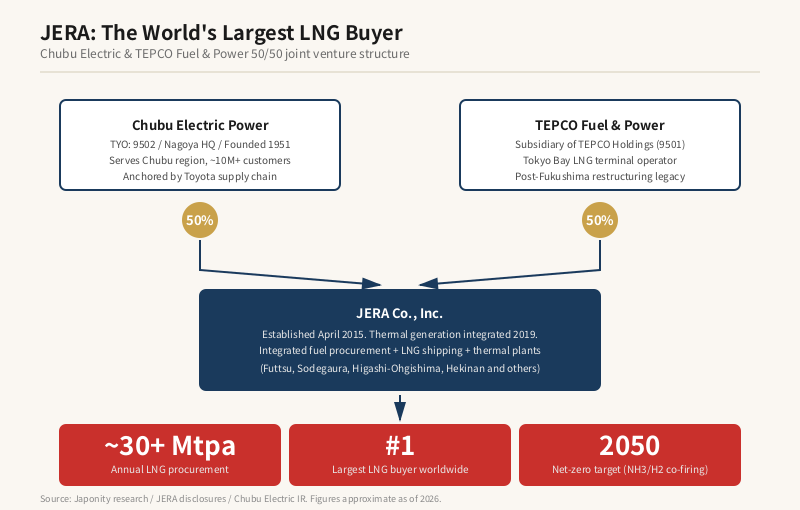

The nuclear shutdown forced an answer to a simple question: where would the replacement electrons come from? The answer, executed jointly with TEPCO, was JERA.

JERA was incorporated in April 2015 as a 50/50 joint venture between Chubu Electric and TEPCO Fuel & Power, with the explicit aim of integrating the two utilities’ upstream fuel procurement, LNG shipping, and thermal power generation businesses. By 2019 the integration had extended to domestic thermal power plants. Today JERA owns and operates a fleet of LNG and coal-fired stations across Japan — including the Tokyo Bay LNG terminals at Futtsu, Sodegaura, and Higashi-Ohgishima — and procures LNG from a portfolio of long-term contracts with Australia, Qatar, the United States, and Russia (with the latter increasingly constrained by sanctions risk).

The scale is hard to overstate. JERA’s annual LNG procurement of roughly 30+ million tonnes per annum makes it the single largest LNG buyer on the planet, ahead of CNOOC, Korea Gas Corporation, and any European utility. JERA’s purchasing decisions move spot prices at the Japan-Korea Marker. Its tenders set benchmark contract structures. Its decarbonisation roadmap — co-firing ammonia at coal plants, hydrogen at LNG plants, with pilot programmes already underway at Hekinan in Aichi — is, by virtue of scale, effectively setting Asian thermal-fleet decarbonisation pathways.

For Chubu Electric specifically, JERA serves three strategic functions. It hedges the Hamaoka stranded-asset risk by securing a fuel pipeline large enough to replace nuclear capacity without exposing the utility to spot-market price shocks. It provides earnings diversification away from the regulated domestic retail business, which has been progressively liberalised since 2016. And it creates a vehicle for participation in upstream gas equity, shipping, and trading that an individual regional utility could not credibly build.

Comparing Japan’s major utilities

To situate Chubu Electric against its peers, the table below summarises the key metrics for the three largest regional utilities by sales:

| Utility | HQ / Region | Service area population | Industrial anchor | Nuclear status (2026) |

|---|---|---|---|---|

| TEPCO Holdings (9501) | Tokyo / Kanto | ~45 million | Diversified service / finance | Kashiwazaki-Kariwa restart pending |

| Chubu Electric (9502) | Nagoya / Chubu | ~17 million; ~10M+ customer accounts | Toyota and automotive supply chain | Hamaoka 5 units all idle since 2011 |

| Kansai Electric (9503) | Osaka / Kansai | ~20 million | Diversified manufacturing, electronics | Ohi, Takahama, Mihama operating |

Two patterns stand out. First, Chubu Electric is the most industrially concentrated of the three: a higher share of its electricity sales flows to a single sector (transport equipment manufacturing) than any peer. Second, it is uniquely without operating nuclear capacity, which structurally raises its fuel cost exposure relative to Kansai Electric and shapes its strategic reliance on JERA.

The retail liberalisation pressure

Japan’s full retail electricity market liberalisation took effect in April 2016, opening the residential and small commercial segments to competition for the first time. Chubu Electric responded by spinning off its retail arm as Chubu Electric Power Miraiz Co., Inc. in 2020, alongside a separate transmission and distribution subsidiary (Chubu Electric Power Grid). This unbundling is regulatory — it satisfies the legal separation requirements of the liberalised market — but it has also created a structural earnings problem common to all the legacy utilities: the regulated grid business is stable but capped on returns, the competitive retail business faces margin pressure from new entrants, and the generation business is increasingly dependent on JERA and on whatever post-Hamaoka decarbonisation pathway emerges.

The result has been a strategic pivot, accelerated under CEO Kingo Hayashi (appointed 2020) and continuing under Kazuhiro Higashi, who took over the CEO role in subsequent years, toward what management describes as a “comprehensive energy business operator” model — adding distributed energy services, demand response platforms, district heating, EV charging infrastructure, and overseas renewables investment to the traditional utility core.

Decarbonisation: LNG, hydrogen, ammonia

Chubu Electric’s net-zero target is 2050, in line with Japan’s national commitment, and its 2030 interim goal is to reduce domestic CO2 emissions by approximately 50% from 2013 levels. The pathway, executed largely through JERA, has three layers.

The first is the continued expansion of LNG capacity as a transitional fuel, displacing coal and providing dispatchable balancing for renewables. The second is ammonia co-firing at coal plants — JERA’s Hekinan Thermal Power Station in Aichi has been a flagship pilot site for 20% ammonia co-firing, with plans to scale toward higher blend ratios. The third is hydrogen co-firing at LNG plants, plus equity participation in upstream blue and green hydrogen and ammonia production projects in the Middle East, Australia, and the United States.

The strategic logic is that Japan’s geography — limited land for utility-scale solar, no significant transboundary grid interconnection, and seismic constraints on new nuclear — makes a pure-renewables pathway physically difficult. Importing molecular energy (hydrogen, ammonia, LNG, biofuels) is the alternative, and JERA’s scale gives Chubu Electric a credible platform to do it.

Revenue mix and financial profile

Chubu Electric reports consolidated revenue in the range of ¥3.5–4.0 trillion in recent fiscal years, with the precise figure tracking LNG and coal input costs as well as electricity sales volumes. The revenue mix is broadly: regulated transmission and distribution (stable margin, capped returns); competitive retail (volume-driven, thin margins under retail liberalisation); JERA-related fuel and generation (the share of profit attributable to the 50% stake, which has been the dominant earnings contributor in years of favourable LNG pricing); and other businesses including overseas investments, gas retail, and energy services.

The Tokyo Stock Exchange listing (code 9502) trades primarily on three signals: LNG spot price (favourable for JERA in tight markets, unfavourable when JERA’s long-term contracts price below spot); yen-dollar exchange rate (LNG and coal are dollar-denominated imports); and any incremental news on Hamaoka restart. Of these, the third has been close to a binary option for over a decade — out of the money, but with significant upside if struck.

What Chubu Electric means for foreign partners

For international companies, Chubu Electric is relevant on three axes. First, as a counterparty in LNG supply: any large LNG project targeting Asian buyers will, sooner or later, encounter JERA’s procurement team. Second, as an industrial energy customer interface: foreign equipment makers, software vendors, and EPC contractors selling into the Chubu region’s manufacturing base will find Chubu Electric a relevant grid and retail counterparty. Third, as a strategic investor in clean-energy infrastructure: through JERA and directly, Chubu Electric has been an active investor in overseas wind, solar, hydrogen, and ammonia projects, and is open to consortium partnerships with foreign developers.

FAQ

Why did Chubu Electric shut down Hamaoka Nuclear Power Plant?

In May 2011, two months after the Fukushima Daiichi accident, then-Prime Minister Naoto Kan publicly requested that Chubu Electric suspend operations at Hamaoka, citing the plant’s exposure to the predicted Tokai megathrust earthquake and its coastal location. The shutdown was voluntary — Kan had no statutory authority to order it — but Chubu Electric complied. All five units have remained idle since.

What is JERA and why is it significant?

JERA is a 50/50 joint venture between Chubu Electric and TEPCO Fuel & Power, established in 2015 to integrate the two utilities’ fuel procurement and thermal power generation. With annual LNG procurement of roughly 30+ million tonnes, JERA is the world’s largest single buyer of liquefied natural gas, and its purchasing decisions materially affect global LNG pricing.

How is Chubu Electric tied to Toyota?

Chubu Electric serves the Chubu region (Aichi, Mie, Gifu, Shizuoka, Nagano, parts of Fukui), which is the home base of Toyota Motor Corporation and its supplier ecosystem. Toyota Tsusho, Toyota’s general trading arm, holds an equity stake in Chubu Electric, and the relationship spans long-term electricity supply, fuel procurement partnerships, and overseas energy project consortia.

How does Chubu Electric’s nuclear position differ from Kansai Electric’s?

Kansai Electric has restarted multiple reactors at Ohi, Takahama, and Mihama in Fukui Prefecture since 2018, where local political consent has been more achievable. Chubu Electric’s Hamaoka plant in Shizuoka faces uniquely high Tokai earthquake risk, persistent prefectural-level political resistance, and an evacuation-sensitive coastal corridor, making restart materially harder despite significant safety investment by the utility.

What is Chubu Electric’s decarbonisation strategy?

The company targets net-zero by 2050, with an interim 2030 goal of approximately 50% CO2 reduction from 2013 levels. The pathway, executed largely through JERA, combines expanded LNG capacity as a transitional fuel, ammonia co-firing at coal plants (with the Hekinan station as a flagship pilot), hydrogen co-firing at LNG plants, and equity investment in overseas renewables and clean-fuel production.

Working with Chubu Electric

Foreign LNG suppliers, clean-energy developers, industrial equipment makers, and energy-services vendors targeting Japan’s manufacturing heartland will find Chubu Electric — directly or through JERA — a strategically central counterparty. If your organisation is exploring partnership, procurement, or investment touchpoints with Chubu Electric or other Japanese utilities, Japonity’s business matching service can help open the conversation. Visit /business-matching/ to start a structured introduction.

Related from Japonity — Japan’s electric & gas utilities

- TEPCO Holdings — Japan’s largest utility, still rebuilding from Fukushima

- Kansai Electric Power — Japan’s most nuclear-dependent utility

- Tokyo Gas — Japan’s largest gas utility — and an LNG arbitrageur

- Osaka Gas — Japan’s #2 gas utility and its US oil-and-gas pivot

Want to source Japanese products beyond these company profiles? Japonity also runs a Japan Sourcing Hub — a research-grade catalogue of 1,185 verified Japanese food products and 200+ overseas EC stores, ready for B2B procurement.

Interested in Japanese business opportunities?

Whether you're looking for technology partners, engineering talent, or market insights — we can help connect you with the right Japanese organizations.

Get in Touch →